- The Roofer Conflict: Roofers have a financial incentive to push for a claim. Never sign an Assignment of Benefits (AOB) agreement before an independent claim evaluation.

- The ACV vs RCV Trap: If your policy pays Actual Cash Value (ACV) for a 15-year-old roof, heavy depreciation means your payout will likely be minimal after deductibles.

- Hidden Deductibles: In storm-prone states, wind and hail deductibles are often a percentage (1% to 5%) of your home’s total value, making out-of-pocket costs much higher than standard deductibles.

- Long-Term Consequences: Filing for minor, cosmetic damage isn’t worth the five-to-seven-year mark on your CLUE report and the resulting premium surcharge or non-renewal risk.

The Knock on the Door and the AOB Trap

In my years of reviewing property claims, the most common scenario I see starts exactly the same way: a severe storm rolls through, and a few days later, a friendly roofer knocks on your door. They offer a free inspection, show you photos of chalk-circled hail hits, and confidently tell you, “You should definitely file a claim. Your insurance will pay for a whole new roof.”

It sounds straightforward. You have damage, you have insurance, and you have a contractor ready to do the work. But let me stop you right there. Your roofer says you should file. The question is whether that advice reflects your financial interests, or theirs.

I am not demonizing roofers. I work with fantastic, ethical roofing contractors every week. However, roofers who do insurance work have a built-in financial incentive to recommend filing a claim. It is how they secure the job.

<strong⚠️ Warning: The biggest trap I see here is the Assignment of Benefits (AOB) agreement. Many roofers will ask you to sign an AOB upfront so they can deal with the insurance company directly. Never do this before evaluating the claim. Signing an AOB signs away your control over your own settlement.

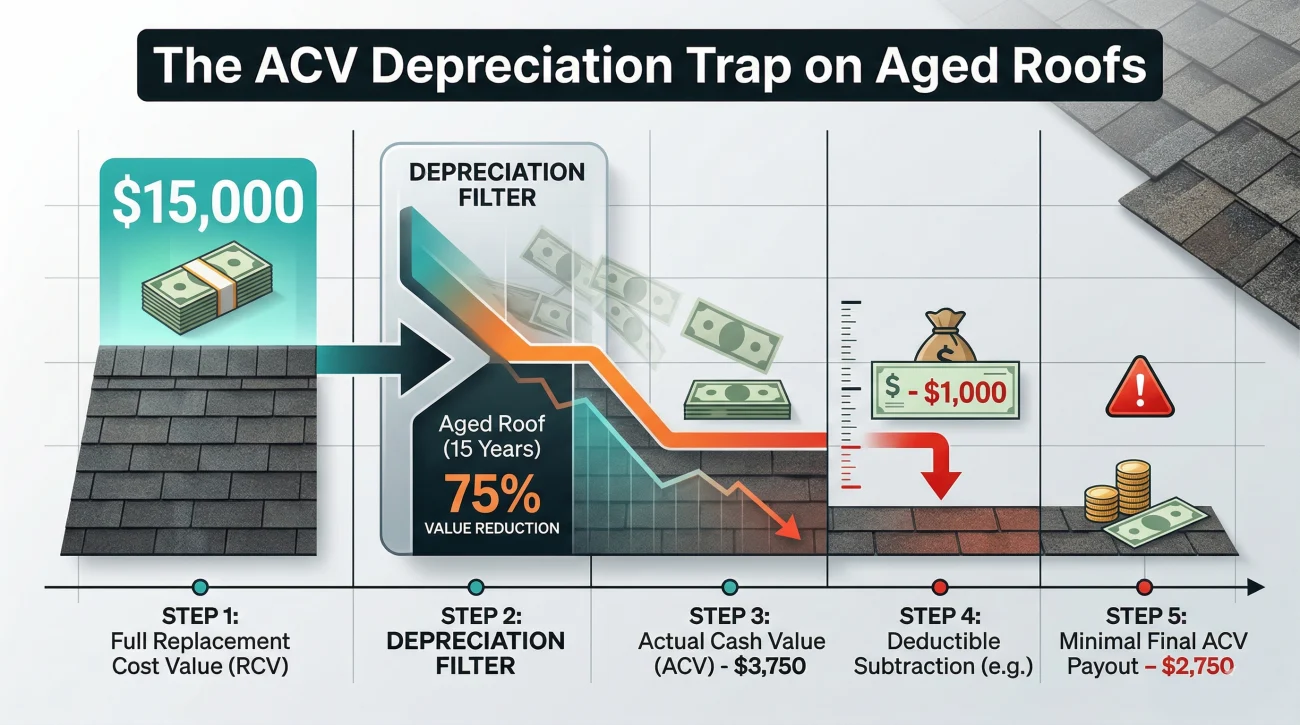

The Biggest Settlement Surprise: ACV Depreciation on Aged Roofs

If I had a dollar for every homeowner who thought their insurance would automatically cut a check for a brand-new $15,000 roof, I wouldn’t need to write this guide. The single most important variable in the roof filing decision is understanding how your policy values your roof.

Many homeowners have what is called an Actual Cash Value (ACV) endorsement on their roof, especially if it is over 10 years old. If your policy pays ACV rather than Replacement Cost Value (RCV) for the roof surface, the insurer will apply significant depreciation based on the roof’s age and condition.

In a recent case I reviewed in the Midwest, a homeowner had a 15-year-old roof with an expected 20-year lifespan. Because of their ACV policy, the insurer depreciated the payout by roughly 75%. Once their deductible was subtracted from that depreciated amount, their net payout was barely enough to cover a minor repair.

Before you even pick up the phone to file, you must check your policy declarations page: do you have ACV or RCV on your roof specifically?

The Wind and Hail Deductible Math

Here is another trap I see homeowners fall into constantly. You probably know your standard homeowner’s deductible, maybe it is $1,000 or $2,500. But if you live in a storm-prone state, there is a very high chance you have a separate, much higher deductible specifically for wind and hail damage.

These are usually percentage deductibles, typically ranging from 1% to 5% of your home’s total dwelling coverage. If your home is insured for $400,000 and you have a 2% wind and hail deductible, your out-of-pocket responsibility for a storm-damaged roof is $8,000 before the insurance pays a dime. Failing to calculate your actual wind and hail deductible is the quickest way to file a claim that yields zero payout.

The Hidden Cost of Code Upgrades (Ordinance or Law)

In my case files, the second biggest financial shock after ACV depreciation is discovering your policy does not cover building code upgrades. When you replace a roof, local building codes often require upgrades that weren’t mandated when your house was built, such as specific ventilation systems, new roof decking, or advanced drip edges.

If your policy lacks Ordinance or Law coverage, the insurance company will only pay to replace what was there, not what the city now requires. I have seen homeowners stuck with thousands of dollars in out-of-pocket expenses just to bring their new, insurance-approved roof up to current municipal code.

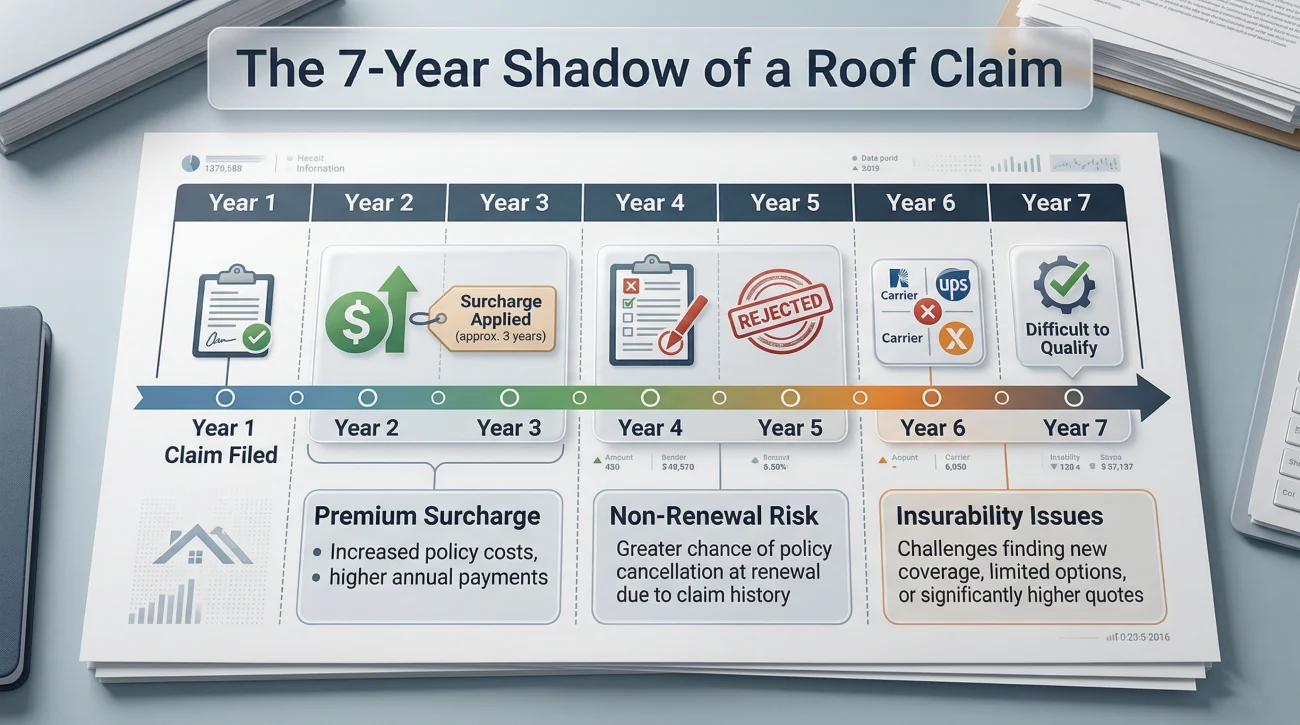

The CLUE Report: How Roof Claims Haunt Your Record

Every claim you file goes into a database called the CLUE (Comprehensive Loss Underwriting Exchange) report. In my experience, insurers are particularly sensitive to roof claims, specifically hail and wind events.

When you file a roof claim, it stays on your record for typically five to seven years. In today’s high-risk insurance markets, a recent roof claim does not just mean a surcharge impact on your future premiums. It can actually affect your insurability. If you decide to shop for a new carrier, or if you plan to sell your home within the next couple of years, that roof claim will be flagged by new insurers. Some may refuse to write a policy at all; others may strictly exclude future roof coverage.

When You Should Almost Always File

Despite the warnings, there are absolutely times when filing is the right financial decision. You should strongly consider filing if:

- ✅ There is significant, undeniable structural damage (e.g., a tree limb pierced the decking, severe internal leaking).

- ✅ A full roof replacement is clearly required, not just a few patched shingles.

- ✅ The damage stems from a widely documented, severe storm event with an established, recent date of loss.

- ✅ You have verified that your policy provides RCV for the roof and the repair cost massively exceeds your deductible.

When to Think Carefully Before Calling Your Insurer

Conversely, I advise homeowners to hit the brakes and do the math if:

- ⚠️ Your roof is nearing the end of its expected lifespan and an ACV policy applies.

- ⚠️ Your percentage wind/hail deductible eats up 80% or more of the estimated repair cost.

- ⚠️ This would be your second property claim of any kind within a five-year window.

- ⚠️ The damage is purely cosmetic (like small hail dents on metal vents) with no threat to the structural integrity of the roof.

Process Red Flags: When to Stop and Re-evaluate

Even if the math makes sense, the way the claim unfolds can ruin your settlement. Pause immediately if you encounter these situations:

- The Rush Job: A contractor is pressuring you to sign a binding contract before the insurance adjuster has even visited the property.

- The Date Blur: You are not sure exactly when the storm happened. If you guess the wrong date, the insurer will deny the claim based on weather records.

- The Hidden Discovery: You are filing for storm damage that actually happened eight months ago, but you only noticed it now because a ceiling stain appeared.

- The Partial Offer: The insurer has already inspected and offered to replace half your roof, but your contractor says the old shingles can’t be matched.

Adjuster Visit Prep: What to Do Before They Arrive

If you decide to file, the adjuster’s visit is the most critical moment. Preparation is everything. Do not throw away torn shingles or broken materials; they are physical evidence.

Before the adjuster arrives, make sure you have completed the following three essential steps:

- 1. Tarp the leak: Mitigate further damage immediately to protect your interior.

- 2. Document with photos: Take date-stamped photos of the exposed damage before the tarp goes on.

- 3. Confirm in writing: Get the adjuster’s visit date and time confirmed via email.

Once your physical evidence is secure, the next step is deciding who will be there to represent you during the inspection. Many homeowners ask if their roofer should be present when the adjuster arrives. Having your contractor there to point out physical damage they found is helpful. However, remember that the contractor cannot argue policy language for you. If the adjuster says, “This isn’t covered,” your contractor has no legal authority to dispute the policy interpretation.

The Real Difference Between a Roofer and a Public Adjuster

This brings us to a crucial distinction that most homeowners misunderstand. I often hear, “My roofer is handling the insurance claim for me.” Let me be clear: a roofer assesses physical damage and measures squares of shingles. A public adjuster reads and enforces the insurance policy.

Why does this matter? Let’s take the “partial offer” scenario. The insurance company agrees there is damage, but only wants to pay to replace the back slope of your roof. Your roofer says the new shingles won’t match the sun-faded front slope, leaving your house looking like a checkerboard. A roofer can complain about this, but a public adjuster steps in to argue the matching provisions outlined in your policy, forcing the insurer to pay for a full roof replacement to maintain a uniform appearance.

Relying on your contractor to argue policy terms with the desk adjuster.

Hiring a licensed advocate to interpret the contract and negotiate the financial settlement.

Final Thoughts: Don’t Guess with Your Roof

The roof filing decision ultimately turns on variables you can control: confirming your ACV or RCV status, calculating your actual deductible, verifying code upgrade coverage, and understanding your CLUE exposure. Knowing how these fit into the full filing decision framework is what separates a successful restoration from a financial nightmare.

💡 Pro Tip: Before you file a claim, and certainly before you sign an AOB with a roofer, get an independent scope assessment from a licensed public adjuster. We can tell you what your insurance will actually cover, handle the policy negotiations, and ensure you are not leaving money on the table.

❓ FAQ

🏠 Should I file a claim for a 15-year-old roof?

It depends entirely on your policy. If you have an Actual Cash Value (ACV) policy, the heavy depreciation on a 15-year-old roof means your net payout will likely be very small after the deductible. If you have a Replacement Cost Value (RCV) policy, it may be worth it if the damage is severe.

💨 Does my insurance go up if I file a wind damage claim?

Typically, yes. Even though wind is considered an “Act of God,” most insurers will apply a claims surcharge to your premium at your next renewal. This rate increase generally lasts for three to five years.

💸 What is a wind and hail deductible?

It is a separate, often much higher deductible that applies specifically to storm damage. Instead of a flat fee (like $1,000), it is usually a percentage (like 1% or 2%) of your home’s total insured dwelling value.

🔍 Will my insurance drop me if I file a roof claim?

A single roof claim rarely results in outright cancellation, but it can trigger a non-renewal if you live in a high-risk market, if it is your second claim in a short period, or if the insurer is actively trying to reduce their exposure in your zip code.

🔨 Is cosmetic hail damage worth claiming?

Rarely. If the hail only caused minor visual dents but didn’t compromise the structural integrity or waterproofing of the shingles, the payout will be minimal, but you will still suffer the full penalty of a rate increase and a mark on your CLUE report.

📅 How do insurance companies verify the storm date?

Insurers cross-check the date of loss you provide against national catastrophe databases and historical meteorological records. If their data shows no hail or high winds in your zip code on that exact date, your claim will likely be denied.

📝 Can my roofer handle the insurance claim for me?

A roofer can provide a repair estimate and meet with the adjuster to point out physical damage. However, legally, they cannot negotiate the policy terms or act as your claims advocate. Only a licensed public adjuster or an attorney can legally represent your financial interests.

📉 What does ACV mean for my roof replacement?

ACV stands for Actual Cash Value. It means the insurance company will deduct the value of the “used up” lifespan of your roof before paying you. If your roof was expected to last 20 years and is 10 years old, they may deduct 50% of the replacement cost right off the top.

🤝 Should I hire a public adjuster for roof damage?

If your claim is large, if you have a complex percentage deductible, if the insurer is only offering a partial replacement, or if building code upgrades are involved, hiring a public adjuster is the best way to ensure an accurate, independent scope of damage is presented.

☔ Should I tarp my roof before the adjuster comes?

Yes. You have a duty in your policy to mitigate further damage. Tarping a leaking roof prevents interior water damage. Just make sure to take clear, date-stamped photos of the exposed damage before the tarp goes on to preserve the evidence for the adjuster.

Filing is just the beginning. These cover what the rest of it looks like.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

That gap is common and usually closeable. These explain how.

- 5 patterns that signal your settlement is probably short

- Who the adjuster at your door actually works for

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When a denial needs legal leverage, not just negotiation

- Four paths to fight a denial, including one most homeowners miss

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.