- You have the legal right to choose your own licensed contractor for home insurance repairs. You are not required to use the insurer’s preferred network.

- Preferred contractor networks offer convenience and streamlined communication, but the contractor’s primary business relationship is with the insurance company.

- If your chosen contractor’s estimate is higher than the insurance settlement, the gap is usually a scope or pricing difference that can be negotiated.

- Signing an Assignment of Benefits (AOB) transfers your claim rights to the contractor, removing you from the payment process but also eliminating your oversight.

Navigating the “Preferred” Contractor Pressure

Getting your home insurance claim approved is only the first hurdle. Almost immediately after the adjuster issues a settlement, you will likely face the next major decision: who is actually going to fix your house. At this stage, many homeowners are handed a list of the insurance company’s preferred contractors and are led to believe this is the only path forward.

In my experience reviewing property claims and scope disputes, the contractor selection phase is where homeowners feel the most unnecessary pressure. The confusion usually stems from how insurers present their vendor networks. They offer a streamlined process with a pre-approved builder, which sounds great when your kitchen is torn apart. But what happens if you already have a trusted local contractor you want to use?

I frequently sit across from homeowners who are unhappy with the repair work being done on their home, only to hear them say they felt they had no choice but to use the company the adjuster sent. They did not realize they possessed the absolute right to hire anyone they wanted.

The goal here is not to avoid the insurer’s network entirely, but to make an informed choice. To protect your property and your settlement, we need to break down your actual rights regarding contractor selection, what happens when estimates collide, and the specific paperwork traps you must avoid before any hammers start swinging.

Your Right to Choose Your Own Contractor

Let us clarify the most important rule of the repair phase. You generally have the right to select any licensed, insured contractor of your choosing to complete the repairs on your property. Your home belongs to you, not your insurance carrier.

The insurance company’s contractual obligation is to indemnify you. This means they are required to provide the funds necessary to restore your property to its pre-loss condition, subject to the limits and deductibles of your policy. Because their obligation is strictly financial, they do not have the authority to dictate who specifically performs the labor on your private property.

If an adjuster or a desk representative implies that your claim will only be fully covered if you use their specific vendor, that is incorrect. While the insurer has the right to cap their payout at the fair market rate for the repairs, they cannot force you to use a specific builder to achieve that rate.

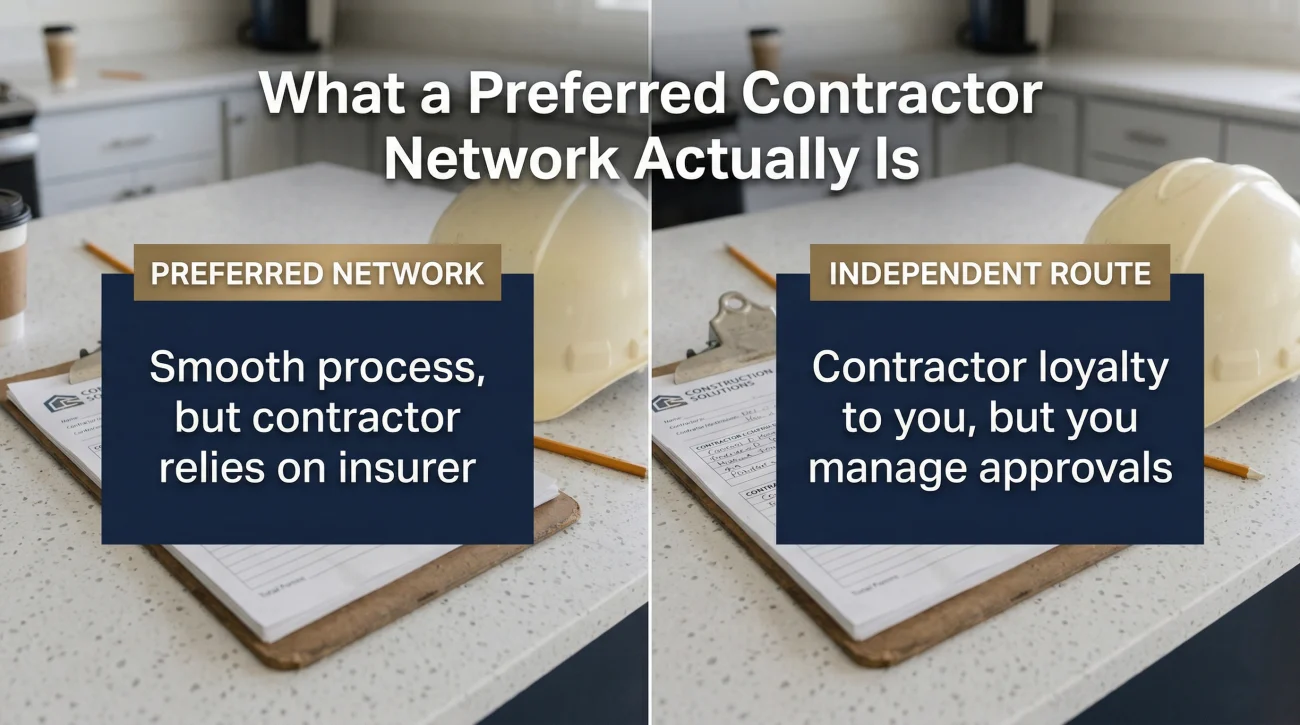

What a Preferred Contractor Network Actually Is

To understand why insurers push their own networks, you have to look at the mechanics of the system. Most major insurance carriers maintain a “preferred” or “managed repair” network. These are independent contracting companies that have signed pre-agreed pricing structures and service level agreements with the insurance carrier.

Using a preferred contractor is fundamentally a convenience service. It is not a scam, but it is a business arrangement that prioritizes efficiency. Because these contractors already agree with the insurer’s pricing software, the approval process is very fast. The contractor and the adjuster speak the same language and often bypass the homeowner entirely when discussing scope changes.

When you use a preferred contractor, the process is smoother, but the contractor relies on the insurance company for their ongoing stream of business. Their ultimate loyalty often leans toward the entity feeding them regular work.

When you hire your own independent contractor, their sole loyalty is to you. However, you will have to act as the middleman (or hire a professional to do so) to ensure their estimate gets approved by the carrier.

Neither path is inherently wrong, provided you understand the dynamics at play. If speed and administrative ease are your top priorities, the network works well; if maintaining direct control over the repair quality and scope is your goal, hiring an independent contractor is the better route.

When Your Contractor’s Estimate is Higher Than the Settlement

If you decide to hire your own local contractor, you will almost certainly run into the most common hurdle: a significant pricing gap. Your contractor hands you an estimate for $25,000 to rebuild your flooded living room, but the insurance adjuster’s settlement check is only for $18,000.

Many homeowners panic at this stage, assuming they must pay the $7,000 difference out of pocket or abandon their chosen contractor. This is rarely true. The gap between the two numbers is simply a negotiation starting point.

I regularly see claim files where the repair process dragged on for months simply because the independent contractor’s real-world bid did not match the desk adjuster’s software output. This gap is entirely normal, but it paralyzes homeowners who do not expect it.

Your local contractor is quoting the actual cost of labor, materials, and overhead in your specific zip code right now. The insurance adjuster likely built their settlement using standardized pricing software. Understanding how Xactimate pricing works is crucial here. The software relies on aggregated regional averages that can easily fall behind real-world market spikes, especially after a regional storm.

When this gap occurs, your contractor will need to submit a detailed, line-by-line comparison showing exactly where the adjuster missed local pricing realities or omitted necessary construction steps. If you find yourself stuck in this back-and-forth, knowing the exact steps to take when a home insurance claim estimate is too low will dictate whether you successfully bridge the gap or end up paying out of pocket.

Why Contractors Ask to See Your Estimate First

This pricing friction is exactly why many roofing and restoration contractors will ask to see your insurance estimate before providing their own bid. They want to cap their quote to the adjuster’s numbers to avoid a prolonged negotiation with the insurer. While this speeds up the start of work, it often means the true scope of your damage is never independently assessed. If the adjuster missed vital code upgrades or hidden damage, a contractor simply matching their estimate will often skip those items or cut corners to stay within the restricted budget.

The Assignment of Benefits (AOB) Question

As you gather estimates from independent contractors, especially roofers or emergency water mitigation teams, you may be asked to sign an Assignment of Benefits (AOB) form before they begin work. You must understand exactly what this document does before putting your name on it.

An AOB is a legal document that transfers your rights under your insurance policy directly to the contractor. Once signed, the contractor essentially becomes “you” in the eyes of the insurance company for the purpose of that specific repair. The insurer will write checks directly to the contractor, and the contractor will negotiate directly with the desk adjuster.

“I hereby assign any and all insurance rights, benefits, and proceeds under my applicable policy to [Contractor Name] for services rendered or to be rendered…”

Contractors favor AOBs because it guarantees they get paid without having to chase the homeowner for the insurance check. However, it completely removes your oversight. If the contractor does poor work, or if they inflate the bill and drain your policy limits, you have surrendered your leverage. You can no longer withhold the insurance funds because the funds are not legally yours anymore.

⚠️ Warning: Never sign an AOB if you feel rushed or if the document contains blank spaces regarding the scope of work. You can always authorize direct payment to a contractor through a standard payment directive without signing over your entire claim rights via an AOB.

Can You Be Your Own Contractor?

While navigating AOBs and independent contractor estimates can feel overwhelming, some homeowners consider bypassing the hiring process entirely to manage the repairs themselves. Technically, acting as your own general contractor is possible in many situations. Practically, it creates a massive documentation burden that usually ends up costing the homeowner significant time, and potentially money if the final payout is rejected.

If your policy pays Replacement Cost Value (RCV), the insurer will initially issue a check for the depreciated value of the damage. To unlock the final payment, you must prove that the repairs were actually completed and that you incurred the full cost. Understanding the mechanics of ACV vs RCV home insurance payouts is vital if you take this route.

If you plan to manage the project yourself, you must maintain a meticulous paper trail to satisfy the insurer’s proof of repair. This means saving every single material receipt from the hardware store, retaining all formal subcontractor invoices, keeping a dated daily log of your own labor hours, and taking detailed before-and-after photographs of the structural work before closing up the walls. If you cannot provide a professional-level accounting of the costs, the insurer will likely withhold the depreciation recovery. Furthermore, if unexpected damage is found behind the walls during the DIY repair, you will be responsible for filing a home insurance claim supplement entirely on your own.

Signs Contractor Decisions Are Complicating Your Claim

The transition from the settlement offer to the physical repair work should be straightforward. If you find the process stalling, it is usually because the relationship between your chosen contractor and the insurer has broken down. Look for these specific red flags:

- You feel forced into the network: You were explicitly told by a phone representative that you must use their preferred contractor to maintain your coverage or guarantee the work. This is a pressure tactic.

- Your repairs are stalled over a pricing deadlock: Your independent contractor cannot get the insurer to agree on local material costs, leaving your family living in a torn-up construction zone with increasing mold risks and mounting pressure from your mortgage company.

- You lost visibility into your own claim: You signed an Assignment of Benefits form early on, and as warned, you have completely lost oversight of the negotiations and claim funds.

- Your contractor wants the adjuster’s estimate first: A contractor refuses to provide an independent bid, indicating they want to cap their quote to the adjuster’s numbers rather than assessing the true scope of your damage.

Final Thoughts on the Repair Transition

Choosing the right contractor is ultimately about finding an advocate for your property. But even the best independent contractor is a builder, not an insurance policy expert. When the negotiation stalls, relying on a construction professional to argue policy language and pricing models with a desk adjuster is a mismatch that often leaves the homeowner paying the difference.

The most dangerous scenario is when your independent contractor and the insurance company fundamentally disagree on the scope of the damage, leaving you stuck in the middle with an insufficient check. If your chosen contractor cannot get the insurer to accept a realistic repair estimate, getting a free claim review from a licensed public adjuster is the safest next step. A public adjuster can step in to translate your contractor’s real-world bids into the exact Xactimate formatting the insurance company requires, forcing a resolution on the scope before you sign any repair contracts.

❓ FAQ

🔨 Can my insurance company force me to use their contractor?

No. In standard property claims, you have the legal right to choose any licensed and insured contractor to perform the repairs. The insurer’s network is an optional convenience, not a requirement.

📄 Should I show my roofing contractor my insurance estimate?

It is generally best to get an independent bid from the contractor first to see their honest assessment of the damage. Showing the insurance estimate upfront often causes contractors to simply match the adjuster’s numbers rather than scoping the real cost.

🔄 Can I change my contractor in the middle of an insurance claim?

Yes, but it can be complicated if you have already signed contracts or an Assignment of Benefits. If you simply received an estimate but signed nothing, you are free to switch contractors at any time.

💰 How does my own contractor get paid by the insurance company?

Typically, the insurance company writes the settlement check to you (and your mortgage company, if applicable). You are then responsible for paying your independent contractor according to the schedule in your construction contract.

✍️ What is an Assignment of Benefits form?

An AOB is a legal document that transfers your insurance claim rights to a third party, usually a contractor. It allows them to bill and collect directly from the insurer, but it removes your control over the claim funds.

🏗️ Do I have to use a licensed contractor for insurance repairs?

While you can legally hire an unlicensed handyman in some jurisdictions, insurers usually require invoices from licensed professionals to release the final depreciation holdback (RCV payments) for major structural work.

🛠️ Can I be my own contractor and keep the leftover insurance money?

You can act as your own contractor, but you cannot legally profit from a claim. If your policy pays Replacement Cost, the insurer will only reimburse the exact amount you can prove you spent on materials and allowable labor.

📉 What happens if my contractor is cheaper than the insurance estimate?

If your final repair cost is lower than the total estimate, the insurance company will only pay the actual incurred cost. They will not pay you the difference to keep as profit.

📈 What if my contractor charges more than the insurance check?

You do not automatically have to pay the difference. Your contractor must submit a supplement to the insurance company with documentation proving why the original adjuster’s estimate was insufficient for the local market.

🛑 Can the insurance company deny my claim if I use my own builder?

No. They cannot deny coverage for a legitimate loss just because you rejected their preferred vendor network. They are only obligated to pay the fair market rate for the repairs, regardless of who does the work.

Filing is just the beginning. These cover what the rest of it looks like.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

That gap is common and usually closeable. These explain how.

- 5 patterns that signal your settlement is probably short

- Who the adjuster at your door actually works for

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When a denial needs legal leverage, not just negotiation

- Four paths to fight a denial, including one most homeowners miss

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.