- Most standard replacement cost policies use a “two-check system” to pay out claims. The first check you receive is almost never the final settlement amount.

- The first check represents Actual Cash Value (ACV), which is the cost to repair the damage minus depreciation for age and wear.

- To get the withheld money (Recoverable Depreciation), you must complete the repairs and submit final contractor invoices before your policy’s strict deadline.

- If you finish the repairs for less than the total estimate, the insurance company keeps the difference.

The Shock of the First Settlement Check

I have sat at a lot of kitchen tables with homeowners who just opened the envelope from their insurance company. The reaction is almost always the same. They look at the check, look at the estimate from their contractor, and realize the insurance payment is thousands of dollars short. Panic sets in. They assume the claim was underpaid and that they will have to cover the gap out of their own savings.

Understanding ACV vs RCV home insurance mechanics is the key to solving this discrepancy. The insurance industry relies on a specific accounting method to pay out damages, and they rarely explain it clearly in their letters.

Today, I am going to walk you through exactly what that withheld money is, and the specific steps you need to take to release the rest of your repair funds.

What Actual Cash Value (ACV) Means in Practice

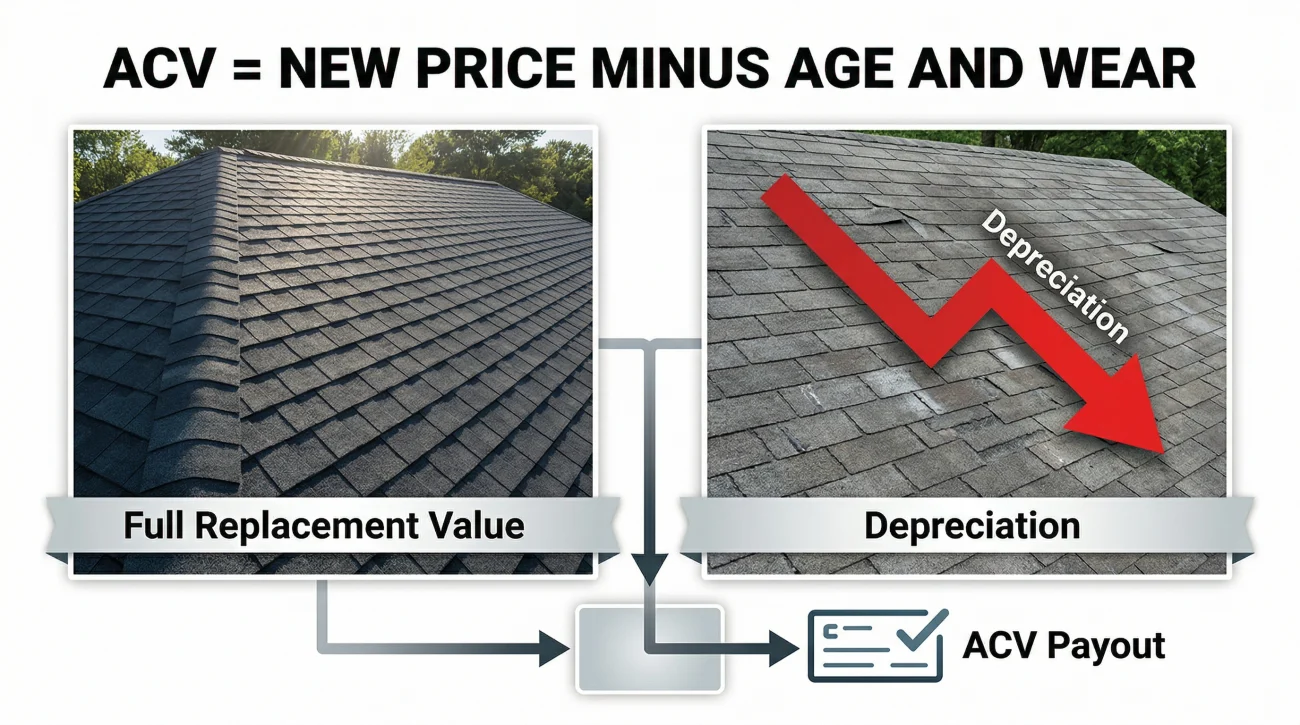

To understand why your initial payment is lower than the repair bid, we need to start with Actual Cash Value, commonly referred to as ACV. When an adjuster calculates your payout, they do not just look at what a new roof or a new hardwood floor costs today. They look at how old your current damaged property is.

ACV is essentially the Replacement Cost Value (the price of brand new materials and labor today) minus depreciation (the loss in value due to age, wear, and tear). The older the damaged item, the higher the depreciation, and the lower your ACV payment will be.

In my claim reviews, the most common point of confusion is depreciation. Homeowners think of their house as appreciating in value. But adjusters view individual building materials like a car driving off a lot. A ten-year-old asphalt shingle roof is functionally worth less than a brand new one, and the settlement reflects that reduced value.

The insurance company pays you this depreciated value upfront so you have seed money to hire a contractor and start the repair work.

Assuming this initial payment is the final offer and paying the remaining balance out of pocket.

Banking the ACV check to start repairs, and setting a reminder to request the depreciation release once the work is done.

What Replacement Cost Value (RCV) Means in Practice

Replacement Cost Value, or RCV, is the total, real-world cost to repair or replace your damaged property with materials of similar kind and quality, at today’s market prices, without deducting a single penny for age or wear.

If your policy includes RCV coverage, it means the insurance company has promised to make you whole. However, they hold back the depreciation amount until you prove that you are actually doing the work. This withheld money is called “recoverable depreciation.”

This withholding phase is a completely normal part of the broader home insurance claim process, but it requires your active participation to complete. To see exactly how this math plays out in the real world, let us look at the actual life cycle of your claim money.

How the Two-Check System Actually Works

Let us say a severe storm ruins your roof, and your contractor says a full replacement will cost 20,000 dollars. Your roof is 15 years old. Here is how the adjuster structures your payout.

| Claim Stage | Insurance Calculation | What Happens in Reality |

|---|---|---|

| Initial Settlement | RCV ($20,000) minus Depreciation ($8,000) | You receive Check 1 for $12,000 (ACV). |

| Repair Phase | Depreciation ($8,000) is held in reserve. | You use the $12,000 to buy materials and start the job. |

| Completion | You submit the final $20,000 contractor invoice. | You receive Check 2 for $8,000 (Recoverable Depreciation). |

The Payout Formula:

Complete Repairs + Submit Final Invoice + Request Depreciation Release = Second Check

If you have an RCV policy, the money sitting in that depreciation column belongs to you. But because it is a reimbursement model, you have to incur the cost first by completing the repairs before the insurer will release the holdback.

How to Verify Your Coverage on the Declarations Page

The rules of this system were established when you originally selected your policy protections. To know exactly what you are entitled to, you need to look at your Declarations Page (usually the first few pages of your policy packet).

- 📄 Look for “Replacement Cost”: If your policy lists “Replacement Cost on Dwelling” or “Personal Property Replacement Cost,” you are eligible for the two-check system.

- 📄 Look for “Actual Cash Value”: If your policy specifically states ACV or lists older items (like a 20-year-old roof) under an ACV endorsement, your first check truly is your final check. The depreciation is “non-recoverable.”

- 📄 Look for “Extended Replacement Cost” (ERC): Some premium policies include ERC, which pays an extra 10% to 50% above your policy limit if local construction costs spike after a disaster. If you have this, you have an additional safety net beyond standard RCV.

What Happens If Your Repairs Cost Less Than the Estimate?

A common scenario I see is when a homeowner manages to find a contractor who will do the job for less than the adjuster’s total RCV estimate. For example, the adjuster estimates $20,000, but your contractor bills you $18,000 for the completed work.

Do you get to keep the extra $2,000? No. Insurance operates on an “actual spend” basis. The insurer will only release enough recoverable depreciation to cover the exact amount you were billed. If you spend less than the estimate, the insurance company keeps the difference. You cannot profit from a property damage claim.

But even when you do spend the full amount, getting that second check released is not an automatic process.

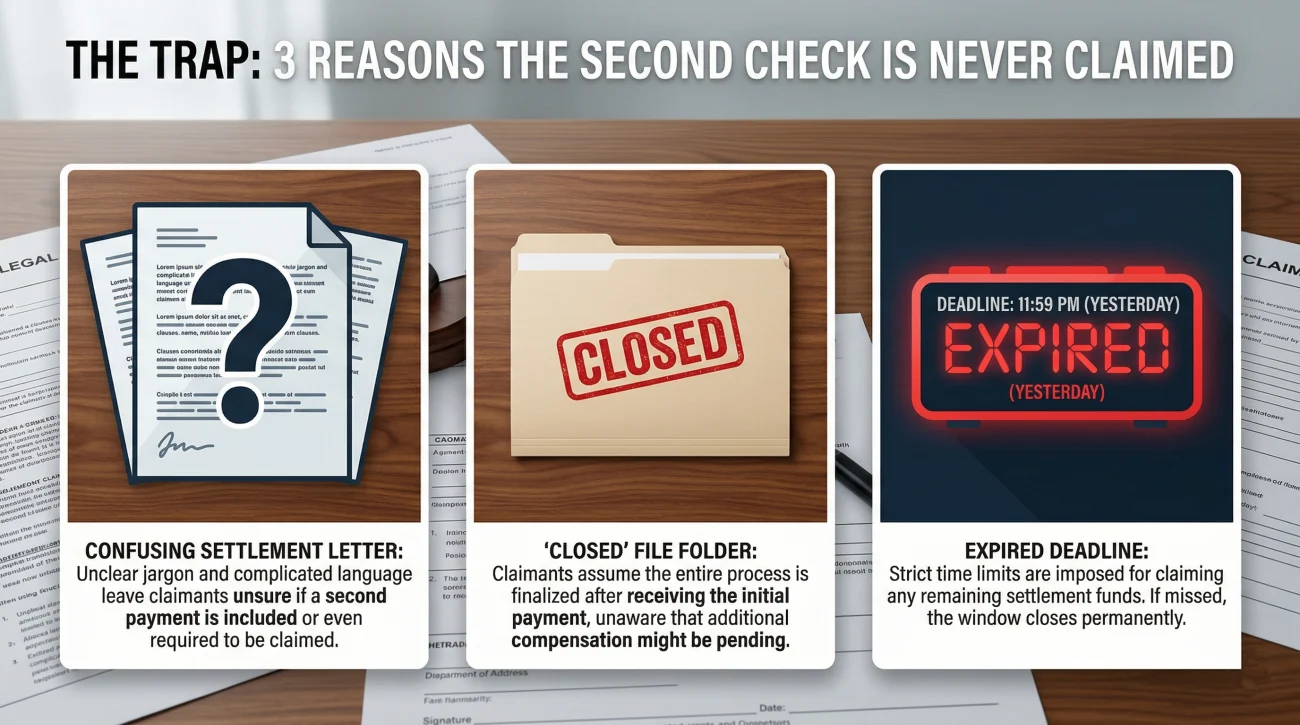

Why Most Homeowners Miss the Second Check

Every year, insurance companies hold onto millions of dollars in unclaimed recoverable depreciation. Based on my experience, this happens for three specific reasons:

1. Confusing Settlement Letters

When the adjuster sends the first check, the accompanying letter is often filled with dense accounting tables. Because the check matches the lower ACV number, homeowners assume that is all they get.

2. Assuming the Initial Payment is Final

If no one explicitly outlines the reimbursement process, it is easy to assume the claim is closed once the first payment clears.

I frequently speak with homeowners who only realized they missed their second check because their contractor called asking why they hadn’t paid the final balance. They assumed the insurance money was tapped out, not realizing the rest was just waiting to be claimed.

3. Missing the Hidden Deadline

You do not have forever to claim your withheld funds. Almost all RCV policies feature a strict deadline for completing repairs and requesting the depreciation holdback—typically 180 days, one year, or two years from the date of the loss.

📌 Note: If you miss the recoverable depreciation deadline, the insurer can legally keep the held-back money forever, even if you eventually finish the repairs.

How to Claim Your Recoverable Depreciation

Getting your withheld money requires you to manage the paperwork actively. The insurance company will not send an inspector out to check if you finished the work; the burden of proof is entirely on you.

First, get your deadline confirmed in writing immediately.

Subject: Clarification on Recoverable Depreciation Deadline – Claim #[Your Claim Number]

Hello [Adjuster Name],

I am reviewing the initial settlement estimate for my recent claim. I see that $[Amount] has been held back as recoverable depreciation.

Could you please confirm in writing the exact date by which I need to submit my final repair invoices to claim this depreciation holdback? Please also reference the specific policy form and section number that dictates this deadline.

Thank you,

[Your Name]

Once the work is done, you must submit proof. It is vital to learn the habit of maintaining a strict documentation file throughout the process.

In my experience, homeowners often send a chaotic pile of hardware store receipts to their adjuster, which just gives the desk reviewer an excuse to delay the release. Group your invoices by trade—roofing, drywall, painting—and match them directly to the line items in the adjuster’s estimate.

When you send the final organized invoice, state clearly that the work is complete and you are formally requesting the release of the withheld depreciation.

When the Depreciation Calculation Itself is a Problem

While the holdback system is normal, the math behind it is not always fair. Adjusters have discretion when deciding how much to depreciate an item, and they rely on standardized lifespan schedules. For context, here is how long adjusters typically expect materials to last before applying heavy depreciation:

- 🏠 Asphalt Shingle Roofs: 15 to 25 years

- ❄️ HVAC Systems: 15 to 20 years

- 🪵 Hardwood Flooring: 50+ years

- 🎨 Interior Paint: 5 to 7 years

If an adjuster decides your hardwood floor is in “below average” condition based on a few scratches, they might apply a 50 percent depreciation rate instead of a normal 10 percent rate. This drastically reduces your seed money. If your initial payout is so small that you cannot even afford to hire a contractor to start the work, the entire system breaks down.

⚠️ Warning: Adjusters sometimes mistakenly apply depreciation to labor costs or raw building materials (like nails and 2x4s) that do not lose value over time. In many states, depreciating labor is strictly prohibited by law.

How to Challenge the Math

You do not have to accept their calculation as final. Many states follow the “Broad Evidence Rule,” meaning the adjuster cannot just look at the age of the item; they must consider its actual condition, upgrades, and maintenance history.

If you feel the calculation is artificially low, or if the total estimate falls severely short of your contractor’s quote, you have specific mechanisms to fight back. You can invoke the Appraisal clause in your policy to force an independent review, or you can bring in your own representation to correct the scope and depreciation schedules.

Signs Your Claim Process Has Stalled

The mechanics of property insurance settlements are intentionally complex. Here are the clearest signs that your claim has hit a wall and money is still sitting with the insurer:

- 📉 The initial payment you received was significantly lower than the written estimate your contractor provided.

- 🛠️ You completed all the property repairs months ago, but you never submitted the final contractor invoices to the insurance adjuster.

- 🛑 The depreciation percentage applied to your property seemed excessively high, preventing you from even starting the repairs.

Final Thoughts

Do not let confusing accounting terminology prevent you from claiming what it actually costs to rebuild your home. Read your declarations page, confirm your deadlines in writing, and always follow through with the final paperwork.

❓ FAQ

🧐 Why is my first insurance check so low?

The first check is typically the Actual Cash Value (ACV), representing the replacement cost minus depreciation. The remaining money is held back until you prove repairs are underway or completed.

⏳ How long do I have to claim recoverable depreciation?

Deadlines vary by policy, but typically range from 180 days to two years from the date of the loss. You must ask your adjuster to confirm this date in writing.

🛠️ Do I have to use the insurance company’s contractor to get RCV?

No. You have the right to hire any licensed contractor of your choice. Submitting their final invoice will trigger the release of the withheld funds.

🧾 What if my repairs cost less than the RCV estimate?

The insurance company will only pay up to the actual amount you spent. If your contractor finishes the job for less than the total estimate, the insurer keeps the difference.

🚫 Can I keep the ACV check and not do the repairs?

Yes, but if you do not complete the repairs, you forfeit your right to claim the recoverable depreciation. You will only ever receive the initial depreciated amount.

📝 How do I prove I finished the repairs?

You must submit a final, paid-in-full invoice from your contractor, or an invoice showing the remaining balance due, along with a formal written request to release the funds.

📉 Can I negotiate the depreciation percentage?

Yes. If the adjuster applied an excessive depreciation rate based on an incorrect assessment of your property’s condition, you can challenge the calculation using independent evidence or the appraisal clause.

🏚️ Does receiving an ACV check mean my policy is bad?

Not necessarily. Almost all RCV policies issue an ACV check first. However, if your declarations page explicitly says you have an “ACV Only” policy, you will not receive a second check regardless of repairs.

💵 Will they send the second check to my mortgage company?

If you have a mortgage, the lender is usually listed as a payee on both checks. You will likely have to send the second check to your mortgage servicer for endorsement before using the funds.

🙋♀️ What happens if I miss the deadline for the second check?

If you fail to submit invoices before the policy deadline, the insurance company will permanently keep the recoverable depreciation funds, and your claim will be closed.

Understanding the whole process changes how you handle each stage.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

Low offers and scope disputes are common. These explain what to do.

- 5 patterns that signal your settlement is probably short

- Who the adjuster at your door actually works for

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When a denial needs legal leverage, not just negotiation

- Four paths to fight a denial, including one most homeowners miss

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.