- Most standard home insurance claims take between a few weeks to a few months to fully resolve.

- A realistic timeline depends heavily on the severity of the damage, the responsiveness of your adjuster, and whether a catastrophe event has caused a local backlog.

- There is a distinct difference between a legitimate delay caused by complex repair estimates and an intentional delay used as a negotiation tactic.

- Documenting every interaction and keeping a tight communication log is your best defense against a stalled process.

The Reality of Claim Timelines: Why Waiting is the Hardest Part

Filing a property damage claim is stressful enough. But for many homeowners, the most exhausting part of the process is the waiting. You submit your photos, you file the paperwork, and then you sit in a state of limbo, wondering exactly how long does a home insurance claim take to actually settle.

I have reviewed hundreds of claim files from both sides of the desk. In my experience, the uncertainty of the timeline often causes more anxiety than the property damage itself. Homeowners frequently ask me if their specific delay is normal or if they are being ignored on purpose.

The truth is that timelines vary wildly. A simple, isolated water leak might be closed out in three weeks. A complex fire loss involving multiple structures could take a year. However, every standard claim follows a predictable sequence. Understanding how long each stage should realistically take gives you a benchmark. When your claim starts to deviate significantly from that benchmark, you will know it is time to escalate.

Stage-by-Stage: A Realistic Claim Timeline

To accurately answer how long your home insurance claim will take, we have to break the process down into its operational stages. Insurance carriers do not process a file all at once. It moves from department to department, and each transfer adds time.

If you want a broader view of what happens conceptually at each step, reviewing the standard steps of a settlement is highly recommended. Below is the timeframe breakdown for those specific steps.

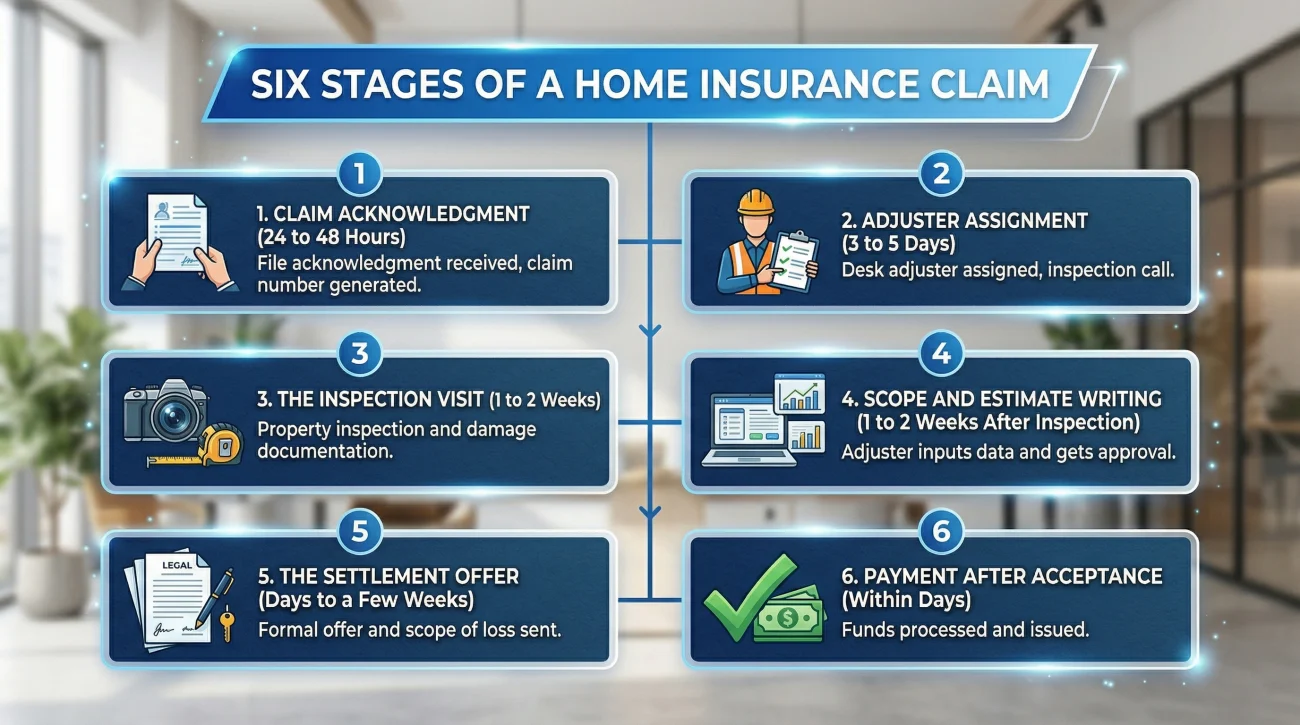

Stage 1: Claim Acknowledgment (24 to 48 Hours)

Once you hit submit or finish your initial phone call, the clock starts. Most standard policies and state regulations expect the insurance company to acknowledge receipt of your claim promptly. This does not mean they have made a decision. It simply means a claim number has been generated and the file exists in their system. You should receive an email or a letter confirming this within one to two days.

Stage 2: Adjuster Assignment (3 to 5 Days)

After acknowledgment, the file is routed to a dispatch team. They must assign an adjuster to your case. In normal conditions, you will hear from the assigned adjuster within three to five days to schedule an inspection. If the dispatch team assigns someone but they never call to schedule within that first week, your timeline is already off track. If a major storm recently hit your area, this assignment timeline can stretch to two weeks because local independent adjusters are completely booked.

Stage 3: The Inspection Visit (1 to 2 Weeks)

The adjuster will typically visit your property within a week or two of making contact. The actual visit might only take an hour or two. During this time, they take photographs, measure rooms, and document visible damage. It is crucial to remember that their timeline for this visit dictates the pace of the rest of the claim. If they have to reschedule, your entire timeline shifts backward.

Stage 4: Scope and Estimate Writing (1 to 2 Weeks After Inspection)

This is the stage where homeowners get the most frustrated. The adjuster has left, and days go by with silence. What is actually happening is that the adjuster is back at their desk, inputting measurements into estimating software like Xactimate. They have to line-item every piece of drywall, flooring, and paint. Then, their manager often has to review and approve the estimate before it can be shared with you. A one to two-week turnaround here is standard operational procedure.

Stage 5: The Settlement Offer (Days to a Few Weeks)

Once the estimate is approved internally, the desk adjuster will send you a formal settlement offer along with a copy of their scope of loss. If your claim is straightforward, you might get this within a few days of the estimate being finalized. If your claim involves separate limits for personal property, dwelling, and temporary housing, the math takes longer.

Stage 6: Payment After Acceptance (Within Days)

If you agree with the scope and the settlement offer, the actual payment processing is relatively fast. Most carriers will issue a direct deposit or mail a physical check within a few business days of you accepting the terms.

Field Note: I often notice that the most common point where files stall is between Stage 3 and Stage 4. Adjusters take hundreds of photos but frequently fall behind on the actual data entry required to generate the estimate. If you are going to experience a legitimate bottleneck, it almost always happens right here.

What Legitimately Extends the Timeline

Not every delay is a sign of bad faith. Claims processing is a heavily administrative task, and certain variables will naturally slow the machinery down. Understanding these legitimate hurdles helps you manage your expectations and avoid unnecessary frustration.

Large or Complex Losses

A simple kitchen leak involves replacing cabinets and flooring. A severe fire involves structural engineering reports, smoke remediation specialists, and complex inventory lists for ruined personal items. The more damage types present, the longer the review takes. Multi-peril claims simply cannot be processed in the same timeframe as minor single-issue events.

Catastrophe Events vs. Normal Conditions

When a hurricane, widespread hail storm, or major freeze hits a region, insurance companies are flooded with thousands of claims overnight. They often deploy independent adjusters from out of state to handle the sudden volume. In these catastrophe scenarios, every single stage of the timeline is stretched. A standard three-day wait for an adjuster assignment can easily become a three-week wait, and estimate writing can take double the normal time as the entire local infrastructure is overwhelmed.

Mortgage Company Involvement

If you have a mortgage, your lender is likely listed on your policy. For larger payouts, the insurance company will make the check out to both you and your mortgage servicer. Getting the mortgage company to endorse the check and release the funds requires entirely separate administrative steps. They often enforce their own draw schedules, require third-party inspector visits to verify repair progress, and release funds in strict stages. This administrative layering can easily add weeks to your final payment timeline.

| Situation | Expected Delay Impact |

|---|---|

| Local severe weather event | Adds 2 to 4 weeks to inspection scheduling |

| Need for a specialized contractor | Adds 1 to 3 weeks for additional reports |

| Mortgage company endorsement | Adds 2 to 4 weeks for check processing |

| Disputes requiring re-inspection | Adds 3 to 6 weeks for a second visit |

When Delay Becomes a Strategy

While administrative backlogs are real, delay is sometimes used as a psychological lever. The longer a claim remains unresolved, the more financial and emotional pressure builds on the homeowner. Eventually, exhaustion sets in, making a low settlement offer look much more appealing than another month of fighting.

In my time reviewing claim operations, I have noticed distinct patterns that separate a busy adjuster from a stalling tactic. A key indicator is the cyclical document request. You submit everything asked of you, the adjuster goes silent for weeks, and then suddenly asks for a document you already sent.

This cyclical approach keeps you waiting while checking their internal compliance boxes. For a deeper understanding of how unexplained delays, repetitive requests, and premature lowball offers fit into a broader negotiation approach, recognizing common adjuster tactics will help you spot the mechanics at play.

But how do you know when you have reached that point of escalation?

Signs Your Claim Timeline Has Crossed Into a Problem

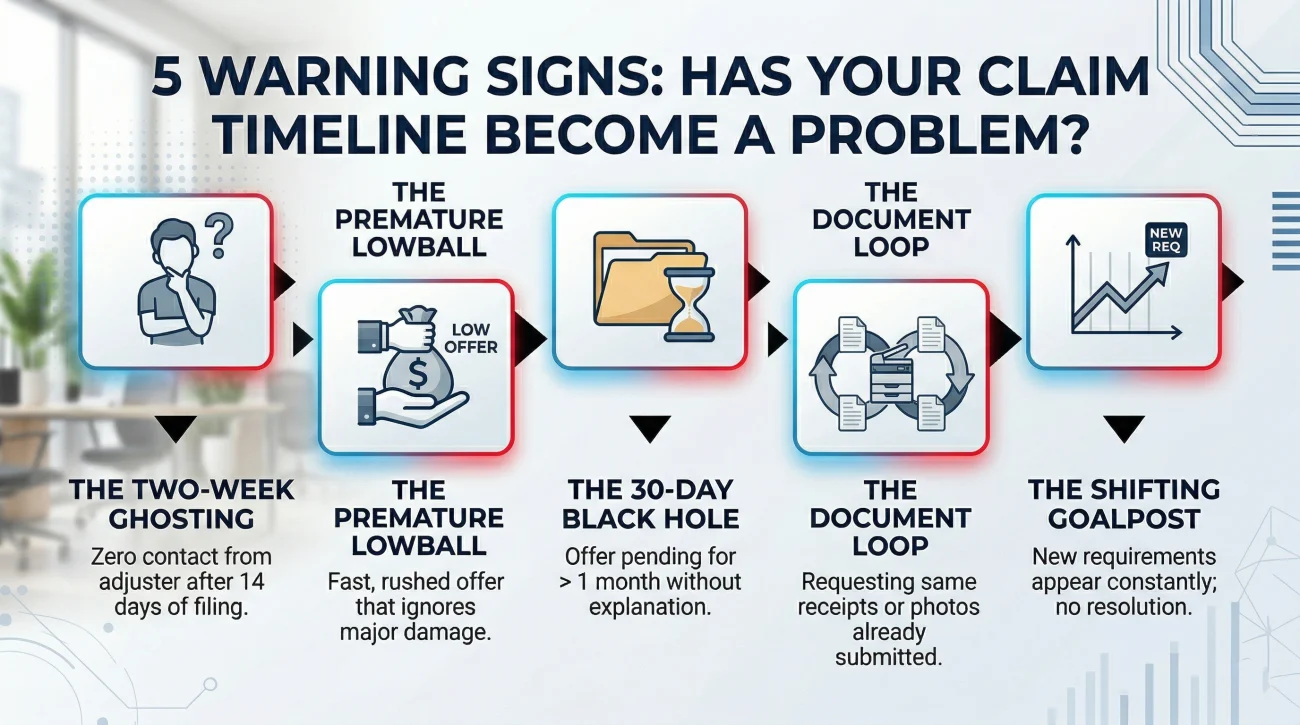

Waiting is normal, but being ignored is not. You need to know exactly when your timeline has crossed the boundary from standard administrative processing into a mismanaged or strategically delayed file. If you are experiencing the frustration of an endless wait, compare your situation against these clear warning signs.

- 📍 The Two-Week Ghosting: You filed the claim, but have had zero contact from an assigned adjuster within 14 days of filing.

- 📍 The Premature Lowball: Strangely, your offer arrived within days of a brief, rushed inspection, leaving out major sections of damage. A fast offer is often as problematic as a long wait.

- 📍 The 30-Day Black Hole: Your settlement offer has been pending review for more than a month with absolutely no explanation for the hold-up.

- 📍 The Document Loop: The adjuster is requesting the exact same receipts or photos you have already submitted via email or portal.

- 📍 The Shifting Goalpost: Every time you manage to get them on the phone, they produce a brand new requirement rather than offering a resolution.

Timeline delays and premature, incomplete offers almost always appear together in the same claim file. When an insurer is overwhelmed or poorly managing a file, the resulting scope of damage is rarely accurate. If your situation matches these patterns, the question is not just how long the claim will take, but whether the final number will even be correct when it arrives.

If you are trapped in this loop, getting a free professional claim review can force the insurer to take the file seriously. A professional steps in, audits the timeline, takes over the communication, and reviews whether the claim was fully scoped in the first place.

Final Thoughts on Managing the Wait

You have a life to live, and your home is likely your biggest asset. Watching it sit in disrepair while you wait on an insurance timeline is incredibly taxing. By understanding what a normal timeframe looks like, you can protect yourself from unnecessary anxiety.

Keep your records tight, communicate exclusively in writing when deadlines are missed, and do not be afraid to bring in an expert if the delay feels intentional. Especially for high-stakes repairs like severe roof damage, getting a second set of eyes early on can prevent a month-long delay from turning into a denied claim.

Finally, remember that the timeline clock does not completely stop once that first payment arrives. If you have a replacement cost policy, claiming your depreciation holdback involves its own strict deadline. Understanding how the two-check system works ensures you do not miss out on the final phase of your settlement.

❓ FAQ

⏱️ How long does a home insurance claim take from start to finish?

Most standard claims take between 30 to 60 days to resolve completely. Complex claims involving severe fire or water damage can take several months, while widespread catastrophe events will extend timelines significantly due to adjuster shortages.

🤷♂️ Why is my home insurance claim taking so long to process?

Delays are usually caused by an adjuster backlog, the need for specialized contractor reports, or mortgage company involvement. However, repeated requests for the same documents or unexplained silence can indicate a stall tactic.

📞 How long does an insurance adjuster have to contact you?

While standard industry practice is to make initial contact within a few business days, actual legal timelines vary by state. Check your policy for the specific timeline language, keeping in mind that severe weather events often grant carriers more leeway.

🛑 What happens if the insurance company is ignoring me?

If your calls and emails are ignored for weeks, you should escalate the issue. Send a written notice of delay to the adjuster’s manager, document the lack of response, and consider consulting a public adjuster to intervene.

💸 How long does it take to get the settlement check?

Once you formally accept the settlement offer, the insurance company typically issues payment within a few business days. If your mortgage lender is on the check, their endorsement process can add a few extra weeks.

🏠 Does a large claim take longer to settle?

Yes. Large claims require more extensive inspections, specialized damage reports (like mold or structural engineering), and multiple levels of internal management approval, all of which legitimately extend the timeline.

📑 How long do I have to submit additional documents?

You should submit requested documents as quickly as possible to avoid resetting the adjuster’s internal review clock. Check your specific policy language, as most require prompt compliance to keep the claim active.

🕵️ Can the insurance company delay my claim on purpose?

Insurers know that financial pressure makes homeowners more likely to accept lower offers. While most delays are administrative, intentional stalling tactics do exist, often taking the form of cyclical document requests and unexplained silence.

📅 How often should I call my insurance adjuster for an update?

If a promised deadline passes, follow up the next business day. Instead of calling daily, send a concise weekly email requesting a status update to create a permanent, trackable communication log.

📝 Will hiring a professional speed up my claim?

A public adjuster cannot force an insurer to issue a check faster, but they take over the administrative burden, prevent the insurer from using stall tactics, and ensure the scope of loss is thoroughly documented to avoid back-and-forth disputes.

Understanding the whole process changes how you handle each stage.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

Low offers and scope disputes are common. These explain what to do.

- 5 patterns that signal your settlement is probably short

- Who the adjuster at your door actually works for

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When a denial needs legal leverage, not just negotiation

- Four paths to fight a denial, including one most homeowners miss

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.