- Canceling is possible: You can usually withdraw a claim before payment is issued, but the record of filing may still appear on your CLUE report.

- Reopening is common: A closed claim can often be reopened if you discover hidden damage during repairs or if you are claiming your recoverable depreciation within the policy deadline.

- Documentation drives the reopening: To successfully reopen a file, you must provide new, documented evidence (like a contractor’s change order) that was not assessed in the original settlement.

Understanding the Reversible Nature of Claims

Filing a home insurance claim feels like a definitive, irreversible action. You hit submit, the gears start turning, and many homeowners assume they are just locked into whatever happens next. But from my experience sitting on both sides of property damage files, I can tell you that the process is not always a one-way street.

I frequently speak with homeowners who either panicked after filing and want to back out, or who feel entirely defeated because their adjuster closed their file before all the repairs were funded. The truth is, you have the ability to cancel a claim you just filed, and in many specific scenarios, you can reopen a claim that was already closed.

Whether you are trying to protect your future premium rates by withdrawing, or fighting for additional repair funds on a closed file, the mechanics of how you handle the paperwork matter. Below, I will walk you through exactly how to cancel an active claim, the specific conditions that allow you to reopen a closed one, and the operational steps you need to take to do either without compromising your property.

Can You Cancel a Home Insurance Claim After Filing?

Yes, in most cases, you can withdraw a home insurance claim. However, the timing of your cancellation dictates how complicated the process will be and what financial obligations you might face.

If you have simply reported the damage and the adjuster has not yet issued a payment, cancelling is usually as straightforward as sending a written notice of withdrawal to your desk adjuster. If a check has already been issued, even if you haven’t cashed it, the process becomes slightly more bureaucratic, as the insurer must void the payment and close the accounting on the file.

Field Note: In my day-to-day work, the most common cancellation scenario I see happens right after the homeowner gets their first contractor estimate. They realize the total repair cost is only $100 over their deductible. Filing a claim for a $100 net payout is almost never worth the long-term rate increase, so they rightly choose to withdraw.

The CLUE Report Reality

There is one vital caveat to cancelling: withdrawing a claim does not necessarily erase it from your insurance history. Insurance companies use a shared database called the Comprehensive Loss Underwriting Exchange (CLUE). When you call to report an incident, a record is often created immediately.

Even if you withdraw the claim and receive zero dollars, the CLUE report may still show a “zero-pay claim.” While a zero-pay claim has less impact on your future premiums than a large payout, multiple zero-pay claims can still flag you as a higher-risk homeowner. If you are currently debating whether to hit submit or pay out of pocket, it is crucial to understand how to weigh the financial impact of filing before making the call.

The Danger of Withdrawing Prematurely

A common strategic mistake I see is a homeowner who hastily withdraws a claim, pays for a seemingly small repair out of pocket, and then discovers the damage is actually catastrophic once walls are opened. They try to call their insurer back and file a “new” claim for the bigger damage. You cannot do this. The date of loss remains the same. Instead of filing anew, you would have to petition to reopen the withdrawn claim, which can be procedurally difficult. Always get a professional assessment of the damage before making the final decision to cancel.

Calling the general 1-800 claims hotline and verbally saying “nevermind, cancel it,” without asking for written confirmation.

Emailing your assigned adjuster to withdraw, requesting an email back confirming the claim is closed with zero payout, and keeping that document for your records.

Can a Closed Home Insurance Claim Be Reopened?

This is perhaps the most common question I get from homeowners staring at a letter that says “Claim Closed.” The short answer is yes. A closed home insurance claim can absolutely be reopened under the right conditions. An insurance company closing a file is simply an administrative action on their end; it does not legally bar you from submitting new evidence if your policy deadlines have not expired.

However, you cannot reopen a claim simply because you are unhappy with the original settlement amount. You must have a contractual or evidence-based reason. Here are the most common legitimate reasons claims are reopened, along with one major exception.

1. Newly Discovered, Related Damage

Adjusters scope what is visible. Contractors tear into walls and find what is hidden. It is incredibly common for a repair crew to remove damaged drywall only to find that water saturated the subfloor, or that a fire melted electrical wiring behind the studs. If this new damage is a direct result of the original covered event, you can request a claim reopening to submit a “supplement.” Keep in mind, complex repairs often reveal damage in phases. It is entirely acceptable to submit multiple supplements as the tear-out progresses, provided you document each phase thoroughly.

2. Contractor Pricing Changes

Sometimes the scope of damage is correct, but the local market realities change. If your insurer approved a roof replacement in October, but severe weather hits and local labor rates skyrocket by November, your original settlement may no longer cover the job. To successfully reopen for a pricing dispute, you cannot just tell the adjuster your contractor is more expensive. You must present a line-item comparison. I always advise homeowners to have their contractor draft a formal change order or an updated Xactimate estimate that mirrors the insurer’s formatting, making it impossible for the desk adjuster to ignore the mathematical reality.

3. Claiming Recoverable Depreciation

If you have a Replacement Cost Value (RCV) policy, your first check was likely reduced by depreciation. Once you complete the repairs and have the final invoices, you must essentially “reopen” the dialogue with the insurer to claim that held-back money. Understanding how the recoverable depreciation deadline works is critical here, as this is the one reopening scenario that has a strict, hard-coded expiration date in your policy.

4. When You Cannot Reopen: The Settlement Release Trap

There is one scenario where reopening is almost impossible: if you accepted a cash settlement and signed a full and final release. Insurers sometimes offer a lump sum upfront to close the file permanently. Once you sign that release, you forfeit the right to submit supplements, even if you find massive hidden damage later. Avoid signing a release until your contractor has assessed the full scope of repairs.

💡 Pro Tip: When you need to reopen a claim for new damage, do not let your contractor throw away the damaged materials before the adjuster can verify them. Take extensive photos, stop the work in that specific area, and notify the desk adjuster immediately.

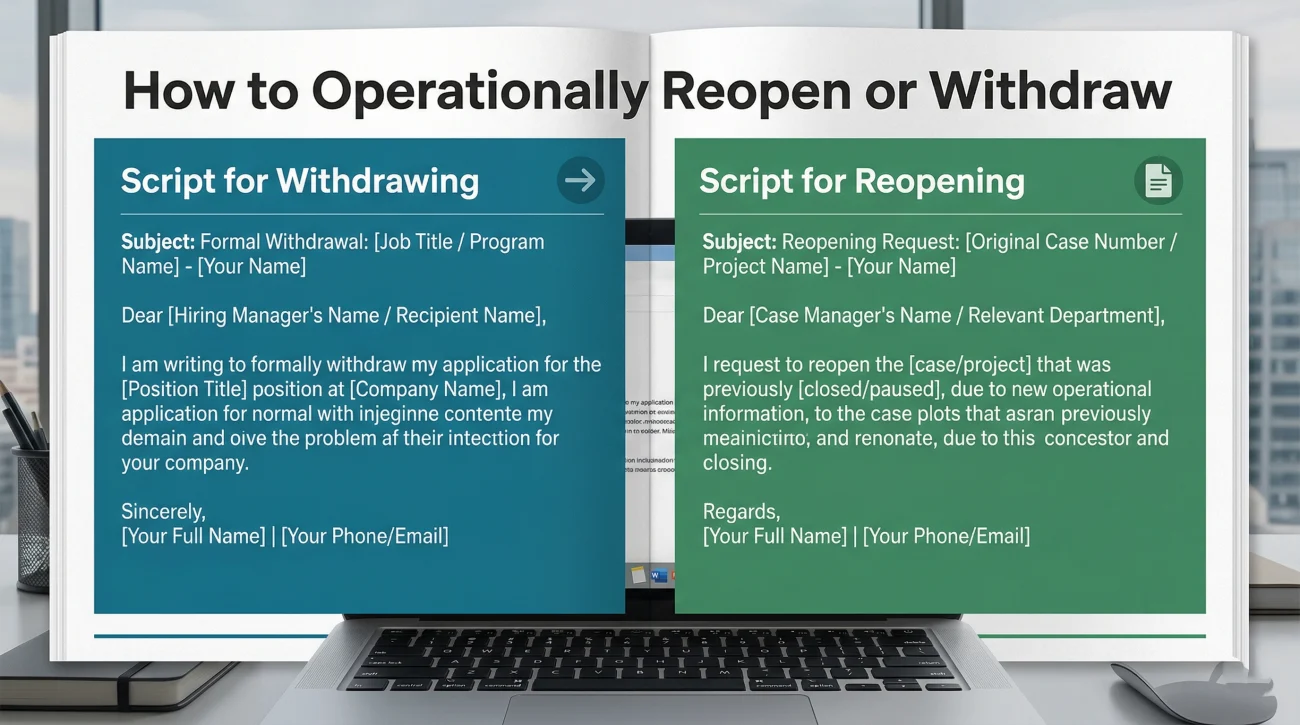

How to Operationally Reopen or Withdraw

Insurance runs on documentation. A phone call is a conversation; an email is a record. Knowing you have the right to withdraw or supplement is only half the battle. The other half is communicating that intent clearly so the adjuster processes it without unnecessary pushback. Below are two templates you can adapt based on your situation.

Script for Withdrawing a Claim

If you have decided the repair cost does not justify the premium hike, use this template to formally close the loop:

Subject: Formal Withdrawal of Claim # [Your Claim Number] – [Property Address]

Hello [Adjuster Name],

I am writing to formally withdraw Claim # [Your Claim Number] for the incident reported on [Date]. After further evaluation, I have decided not to proceed with this claim.

Please close this file as a zero-pay claim. I kindly request a brief email confirmation from you stating that the claim has been withdrawn and closed with no payment issued.

Thank you for your time,

[Your Name]

Script for Reopening for a Supplement

If your contractor found hidden damage, you must notify the insurer before that damage is covered up by new repairs. Use this phrasing:

Subject: Supplemental Damage Notice / Request to Reopen Claim # [Your Claim Number]

Hello [Adjuster Name],

I am writing regarding Claim # [Your Claim Number]. During the repair process, my contractor uncovered additional damage directly related to the original event that was not visible during your initial inspection.

Specifically, we found [briefly describe the new damage, e.g., moisture in the subfloor beneath the removed cabinets]. I have attached photos of the newly exposed damage, along with my contractor’s supplemental estimate to address it.

Please reopen this file for supplemental review. Let me know if you need to schedule a re-inspection before my contractor proceeds with this portion of the work.

Thank you,

[Your Name]

Do Home Insurance Claims Expire?

A common source of anxiety is the fear that a claim will simply “time out.” There is a difference between the deadline to file a claim and the lifespan of a claim that is already in the system.

Once you have successfully filed a claim, the open claim itself does not generally expire. If the insurer is waiting on you to provide a contractor estimate, the claim might be administratively moved to a “closed” status due to inactivity, but it has not expired legally. You can simply submit the document to wake it back up.

However, there is one major expiration clock you must watch: the deadline to complete repairs and claim your RCV supplement. Most standard policies give you 180 days to 2 years from the date of loss (or the date of the ACV payment) to actually do the work and request the rest of your money. If you miss this deadline, that specific money does expire. To see where this deadline fits into the standard progression of a claim, always review your initial settlement letter; the date is usually printed clearly on page one or two. Missing these deadlines is one of the most common ways homeowners leave money on the table, but deadlines are not the only procedural trap you need to watch for.

Signs Your Claim Situation Requires Professional Review

Managing the lifecycle of a claim often requires recognizing when the process has stopped serving your interests. If you are reading this because you feel stuck with a closed file or a bad settlement, you need to look for specific operational red flags.

Here are the clear signs that your specific situation requires a closer look before you accept the outcome:

- Cancellation Regret: You cancelled a claim thinking the damage was minor, but later discovered massive hidden issues (like mold behind the drywall) and are unsure if the window to reopen the original file has closed.

- Missed Scope: Your claim was administratively closed by the adjuster, but your contractor’s final invoices include necessary code upgrades or secondary damage that were never accounted for in the initial payout.

- Unfair Refusal: You submitted a valid contractor supplement for newly discovered damage, but the insurer is refusing to reopen the claim, citing ambiguous policy language or claiming the damage is unrelated to the original event.

If your claim was closed but your contractor’s numbers are much higher than your payout, it helps to understand why your initial estimate might have been insufficient in the first place.

What If They Refuse to Reopen?

If you submit a valid supplement and the insurer refuses to reopen the file, you are not out of options. Depending on the reason for denial, you can request a formal Appraisal (a binding dispute resolution process built into most policies) or escalate through your insurer’s formal complaint process or seek outside professional review.

The Next Step: Cancelling or reopening a claim heavily involves interpreting your policy terms and navigating your insurer’s specific administrative practices. If you have a closed claim that was severely under-settled, or if you found missed scope during repairs, you do not have to fight the reopening battle alone. Consider having a licensed public adjuster evaluate your closed file for missed scope before you accept the financial loss.

Final Thoughts on Managing Your Claim Status

The status of your insurance claim, whether open, closed, or withdrawn, is fundamentally an administrative label used by the insurance company. It is not an absolute final judgment on your property.

If you realize early on that filing was a mistake because the damage is minor, protect your premium by formally withdrawing in writing. Conversely, if your file is closed but your home is not fully repaired due to missed damage or withheld depreciation, do not let the word “closed” intimidate you. Gather your contractor’s documentation, take clear photos of the new evidence, and assert your right to reopen the file for a supplement. Keep your communication strictly in writing, and always focus the conversation on the physical evidence of the damage.

❓ FAQ

⏱️ How long do I have to cancel a home insurance claim?

You can typically cancel a claim at any point before the insurance company issues a payment. If they have already sent a check, you must return it uncashed and request the file be closed as a zero-pay claim.

📈 Will my rates go up if I withdraw my claim?

They might. As mentioned earlier, even a withdrawn claim can appear as a zero-pay claim on your CLUE report, which some insurers use to assess your overall risk profile.

🚪 Can a closed home insurance claim be reopened after a year?

Yes, if you discover new damage directly related to the original event, provided your policy’s deadline for filing supplements has not passed. You will need strong documentation proving the damage is from the old event.

💸 What happens when you withdraw a home insurance claim after getting a check?

If you have the physical check, do not cash it. Contact your adjuster, return the check, and request written confirmation that the claim is closed with zero payout. If it was direct deposited, you will need to arrange a refund to the insurer.

📑 Do I need a lawyer to reopen a claim?

No, not for a standard reopening due to newly discovered damage or a supplement. You usually just need a contractor’s estimate and photos. However, if the insurer refuses to reopen a valid supplement in bad faith, professional representation, whether a public adjuster or an attorney, may be necessary.

🔍 Can I reopen a claim if my contractor finds more damage?

Yes, this is the most common reason to reopen a claim. This is called filing a supplement. You must provide the insurer with photos of the newly exposed damage and a revised estimate from your contractor.

❌ Can you cancel a home insurance claim online?

While some insurer portals have a cancellation button, it is highly recommended to email your assigned desk adjuster directly. This ensures you have a permanent, timestamped written record of your request to withdraw.

⏳ Do home insurance claims expire if I don’t fix the damage right away?

The open claim itself does not technically expire. However, as noted in the timeline section above, the deadline to claim your recoverable depreciation check is strictly enforced by the insurer.

📝 How do I write a letter to withdraw my claim?

Keep it brief and factual. State your claim number, address, and write: “I am formally withdrawing this claim and request that the file be closed with no payment issued. Please provide email confirmation.”

🛑 Can the insurance company refuse to reopen my claim?

Yes. They will usually refuse if the policy deadlines have expired, if the new damage is deemed unrelated to the original event, or if you signed a full and final settlement release.

Understanding the whole process changes how you handle each stage.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

Low offers and scope disputes are common. These explain what to do.

- 5 patterns that signal your settlement is probably short

- Who the adjuster at your door actually works for

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When a denial needs legal leverage, not just negotiation

- Four paths to fight a denial, including one most homeowners miss

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.