- A public adjuster is the only licensed insurance professional in the claims process whose financial interest is entirely aligned with yours.

- They do not work for the insurance company; they work exclusively for the policyholder to document damage, interpret policy language, and negotiate the settlement.

- Public adjusters are paid on a contingency fee basis, meaning they take a percentage of the settlement, and you pay nothing upfront.

- Not every claim needs a public adjuster, but they are highly effective for large losses, complex damage, or when you face a significant gap between a contractor estimate and the insurer offer.

- Always verify a public adjuster’s state license and carefully read their contract fee structure before signing anything.

The Overwhelming Reality of Handling a Major Claim Alone

If you have just heard the term “public adjuster” for the first time, you are not alone. In my experience, most homeowners only encounter this profession after a difficult event, usually when they are already deep into a frustrating property claim. You are likely searching for answers because a contractor mentioned them, a neighbor suggested you hire one, or you simply feel like you are losing a battle with your insurance company and need professional backup.

When you start researching what these professionals do, you will quickly notice a pattern. Nearly every guide out there was written by an adjusting firm. Naturally, those articles are inherently biased. They will tell you that you absolutely must hire them for every single claim. This guide is different.

I have sat across from insurance adjusters on hundreds of claims. I know exactly where the process breaks down, how scopes of work get minimized, and when homeowners are genuinely outmatched by the system. My goal here is to give you a complete, honest, and neutral overview. You need to understand what a public adjuster actually is, how they operate, and what they cost before you ever let one look at your policy.

If you want to explore our full library of resources regarding these professionals, you can browse our complete public adjuster library. But before you make any decisions or sign any contracts, you need to understand exactly what you would be hiring.

What Is a Licensed Public Adjuster?

A public adjuster is a licensed insurance professional who works exclusively for the policyholder, not the insurance company. This is the fundamental definition you must understand. In the complex triangle of a property damage claim, they are the only adjusting professional whose financial interest is directly aligned with yours.

They are licensed and regulated at the state level by the Department of Insurance. This means they must pass state exams, carry surety bonds, maintain continuing education credits, and adhere to a strict code of ethics. They are legally authorized to read your insurance policy, advise you on your coverages, document your property damage, and negotiate directly with your insurance carrier on your behalf.

Many homeowners assume that their contractor can simply handle the insurance company for them. This is a very common mistake. In most states, it is entirely illegal for a roofing contractor or a restoration company to negotiate an insurance claim on your behalf unless they also hold a public adjuster license. This is known as the Unauthorized Practice of Public Adjusting. A contractor can discuss their own estimate, but they cannot debate policy coverages, negotiation depreciation, or argue case law with a desk adjuster. A licensed public adjuster can.

“I frequently see claims stall out for weeks because a homeowner let a well-meaning contractor try to argue policy language with the insurance company. The desk adjuster simply shuts the conversation down. Only you, your attorney, or your licensed public adjuster can legally negotiate the terms of your policy.”

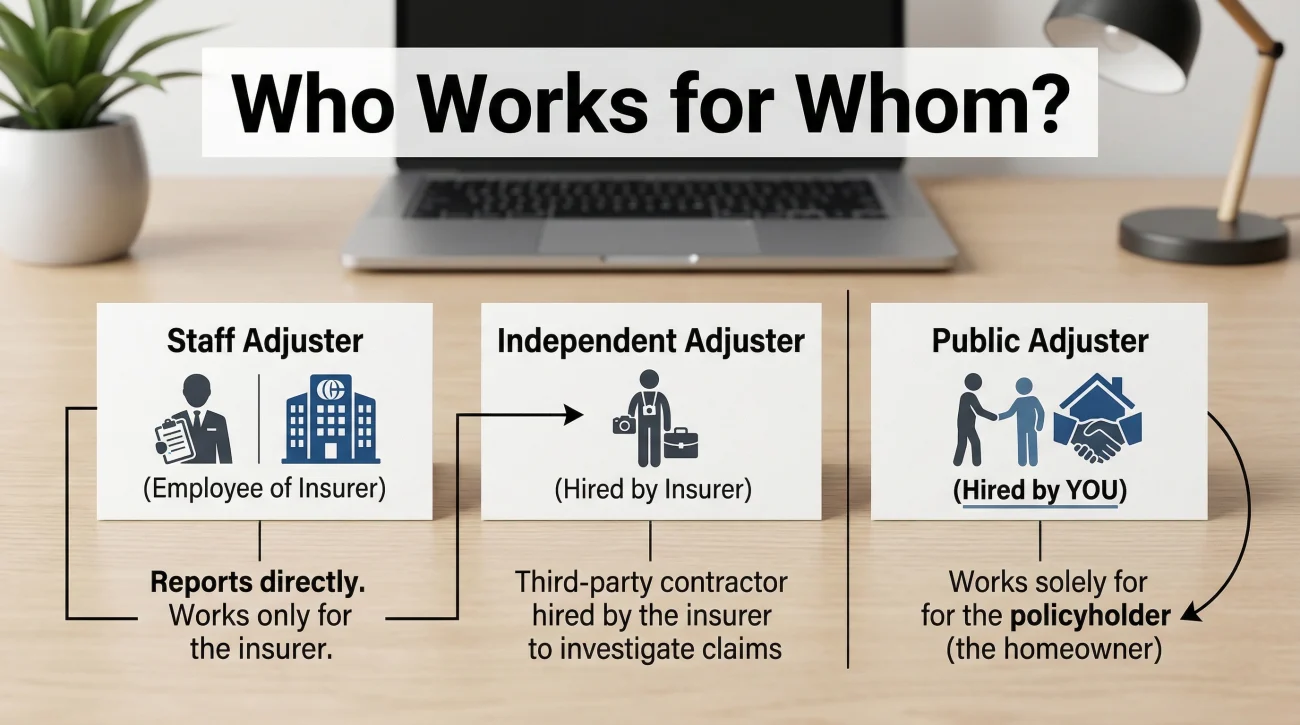

The Three Types of Adjusters in the Field

Confusion often stems from the fact that there are three different types of adjusters who might show up at your house after a disaster. Knowing exactly who works for whom is your first line of defense in managing your claim properly.

1. The Staff Adjuster (Company Adjuster)

This person is a direct employee of your insurance company. They are paid a salary by the carrier. Their job is to inspect the damage, determine what the policy covers, and write an estimate based on the insurance company guidelines. They are usually professional and polite, but you must remember that their ultimate loyalty and paycheck come from the insurer.

2. The Independent Adjuster

The name here is highly misleading for most homeowners. An “independent” adjuster does not work for you. They are freelance adjusters or employees of a third-party adjusting firm hired by your insurance company. Insurers use them when they have a high volume of claims, like after a major hurricane or a severe freeze event. They act as the eyes and ears of the insurance company, but they still report directly to the carrier. Their goal is to close files quickly and efficiently for the insurer.

3. The Public Adjuster

As we established, this is the only adjuster you hire. They work for you, the public. Their job is to thoroughly investigate the loss, document every single damaged item, and build a competing estimate to present to the insurance company. For a complete three-way comparison of who each professional works for and why it matters to your payout, see our detailed breakdown of a public adjuster vs insurance adjuster.

Assuming the adjuster sent by the insurance company is there to find every single penny you are owed and maximize your payout.

Treating the insurance company adjuster politely but understanding they represent the company’s financial interests, while a public adjuster represents yours.

Understanding whose side each adjuster is on is the first step, but knowing exactly what a public adjuster does once they step onto your property is what determines the actual value they bring to your file.

What Do They Actually Do During a Claim?

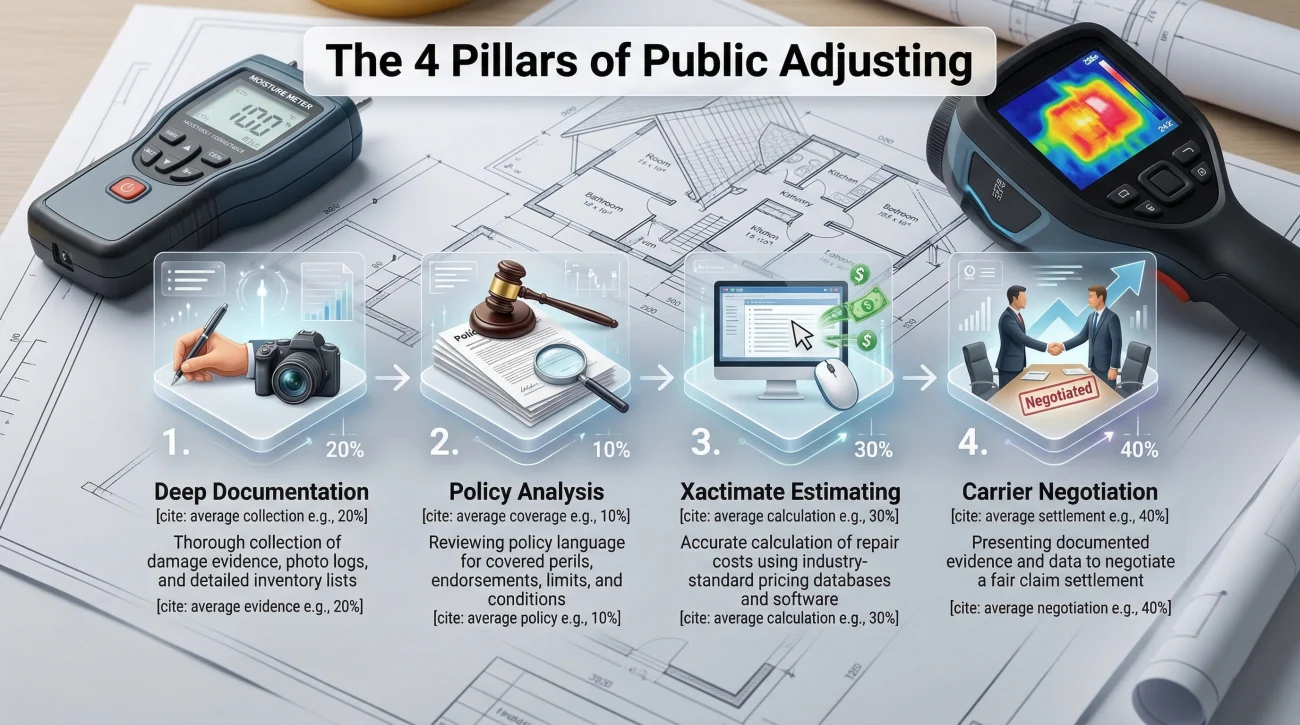

Understanding how a public adjuster works requires looking past the general idea of “negotiation” and diving into the daily mechanics of claim management. When you hire one, they essentially take over the heavy lifting of the entire process. Here is what that looks like in practice.

The Deep Documentation Phase

The first physical step is a massive documentation effort. A standard insurance adjuster might spend forty-five minutes walking through a flooded house. A thorough public adjuster might spend four hours in that same house. They will pull back baseboards, use thermal imaging cameras to find trapped moisture, measure rooms down to the inch, and document collateral damage that the insurance company completely ignored.

I have seen countless initial insurance estimates that leave out obvious line items like drywall tape, paint blending, debris removal, or the cost to detach and reset appliances. The public adjuster’s job is to catch all of these missing elements.

Policy Interpretation

Your insurance policy is a dense legal contract. The public adjuster will read the entire document, including all endorsements and exclusions. They look for specific coverages you might not know you have, such as code upgrade coverage (Ordinance or Law), mold remediation limits, or Additional Living Expenses (ALE). They use this deep understanding of the contract to argue why certain items must be paid.

Building the Competing Estimate

Once the damage is documented, the public adjuster uses specialized estimating software (usually Xactimate, which is the same software the insurance companies use) to build their own estimate. This is crucial. When you negotiate with an insurance company, you cannot just ask for a lump sum. You have to argue line item by line item. The public adjuster speaks their language and provides the exact documentation required to justify the cost. For more context on how this software dictates your timeline and payout, see our complete guide to the home insurance claim process.

Taking Over Carrier Communication

One of the most immediate changes after you sign a representation contract is the shift in communication. The public adjuster formally notifies the insurer that they are your authorized representative. From that moment, the desk adjuster must route all correspondence, phone calls, and emails through your professional advocate.

In my experience, this is often the biggest relief for homeowners. You are no longer fielding stressful phone calls during your workday, nor are you being pressured to accept a verbal offer over the phone. While this formal routing can sometimes extend the overall timeline of the claim, most homeowners describe this shift as the single biggest operational relief of the process.

Filing Post-Settlement Supplements

A public adjuster’s job does not always start on day one. A very common scenario I see involves homeowners who have already received and cashed an initial insurance check. Weeks later, their contractor begins demolition and discovers extensive hidden damage behind the walls.

As long as you have not signed a final settlement release, a public adjuster can step in, document this newly discovered damage, and file a formal supplement. They force the insurance company to reopen the scope of work and negotiate the additional funds required to finish the job correctly.

Seeing these steps in action helps demystify the process, but just as important is identifying the specific claim patterns where this level of intervention truly changes the outcome in your favor.

General Scenarios Where a Public Adjuster Changes Outcomes

Not every claim requires professional representation. If you are dealing with a small, straightforward loss or damage that falls below your deductible, hiring an adjuster simply costs you a fee unnecessarily. You can likely handle the paperwork yourself or rely on a standard contractor estimate if the insurer is agreeable.

Howvever, public adjusters typically change outcomes in specific scenarios: large or complex losses, claims involving multiple damage types, or when you face a massive gap between your contractor’s estimate and the insurer’s initial offer. Describing these general scenarios is different from determining whether your specific claim actually qualifies. That decision depends entirely on your damage type, your policy language, and your current offer.

If your settlement feels low relative to your contractor’s estimate, or your adjuster visit was short for a significant loss, those patterns are worth a professional review. To determine whether bringing in an expert makes sense for your specific situation, I strongly recommend getting a free claim review.

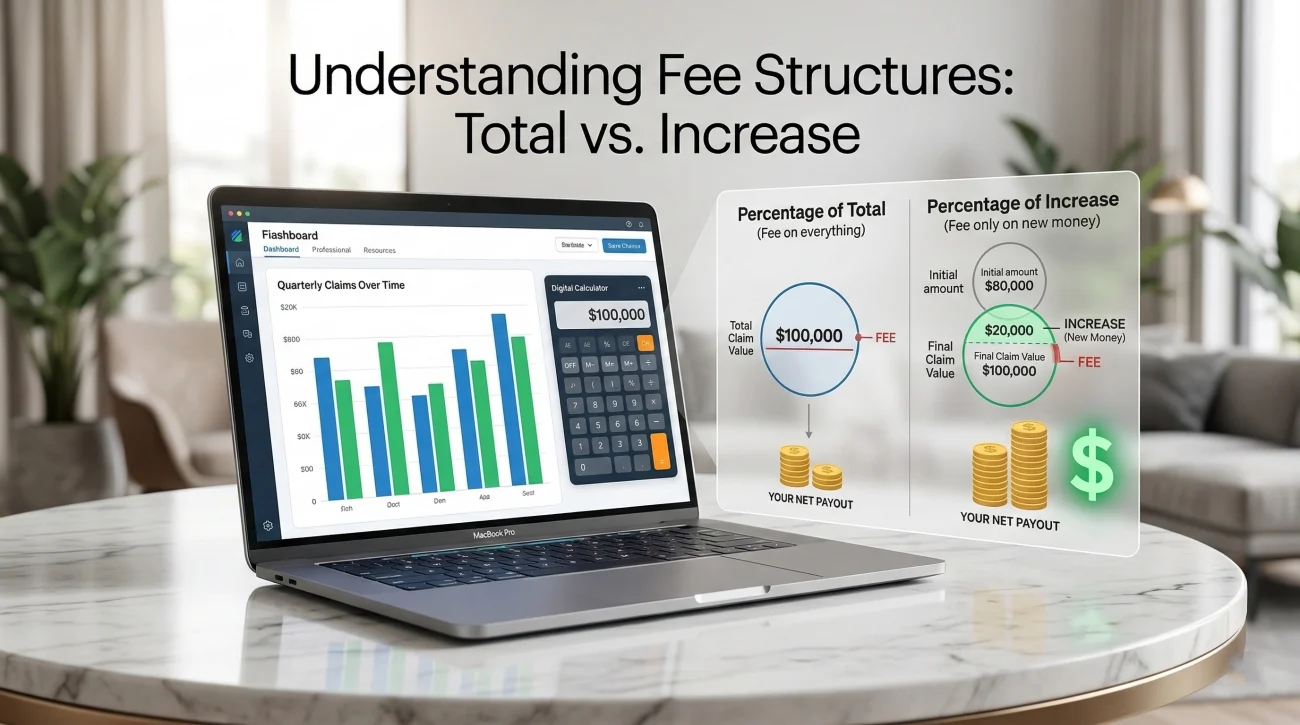

How Much Does a Public Adjuster Cost?

Homeowners are often hesitant to seek help because they assume they will have to pay an expensive hourly rate out of pocket. This is not how the industry works. Public adjusters operate on a contingency fee basis. This means they do not get paid unless you get paid.

Typically, a public adjuster will charge a percentage of the settlement, usually ranging from 10% to 20% depending on state regulations and claim size. However, there is a critical distinction in how this fee is applied, and you must understand it before signing any contract. There are two very different fee structures:

Structure 1: Percentage of the Total Settlement. If the adjuster charges 15% of the total settlement, and the final payout is $30,000, their fee is $4,500. They take a cut of every dollar the insurance company pays, including what was offered before they were hired.

Structure 2: Percentage of the Increase (New Money). If the insurer already offered you $10,000, and you hire a public adjuster who pushes the final settlement to $30,000, they only take their 15% fee from the $20,000 of “new money” they generated. In this scenario, their fee is only $3,000.

This is an important distinction because the second model aligns the adjuster’s incentive directly with the value they add. Understanding these exact public adjuster fees is critical before you proceed.

| Scenario (Insurer initially offered $10,000) | Public Adjuster Fee (15%) | Your Final Net Payout |

|---|---|---|

| No Adjuster (You accept the $10k offer) | $0 | $10,000 |

| Fee on Total Settlement (Claim settles at $30k) | $4,500 | $25,500 |

| Fee on Increase Only (Claim settles at $30k) | $3,000 | $27,000 |

💡 Pro Tip: Always read the fee structure in the contract carefully. Make sure you understand exactly what settlement funds are subject to the fee. Ask if their fee applies to your Additional Living Expenses (ALE) or just the dwelling coverage. You want total clarity before signing.

Clarifying the math before you sign is essential, but even a fair fee structure won’t protect you if you hire the wrong professional. I’ve seen homeowners overlook a few critical red flags in the heat of the moment.

Common Mistakes When Hiring Representation

Bringing in a professional can save a claim, but hiring the wrong one can create a nightmare. In my operational experience, homeowners usually fall into a few predictable traps when selecting representation.

Mistake 1: Hiring the “Storm Chaser”

After a major hurricane or hail storm, out-of-state public adjusters will often flock to the area. They knock on doors, promise massive payouts, and pressure homeowners into signing contracts on the spot. Never hire an adjuster who shows up uninvited to your front door demanding a signature. Take your time, do your research, and prefer local experts who know the regional building codes and contractors.

Mistake 2: Failing to Verify the License

Hiring an unlicensed representative can instantly derail your claim, as insurers will legally refuse to communicate with them. Always look up their credential on your state’s Department of Insurance website before you engage.

Mistake 3: Signing Without an Exit Clause

Sometimes, a relationship simply does not work out. The adjuster might stop returning your calls, or they might push you to accept a lowball offer just so they can collect a quick fee. Before you sign a public adjuster contract, ensure there is a clear termination clause that explains what happens if you decide to fire them. You do not want a bad adjuster placing a lien on your property.

How to Vet a Good Public Adjuster

If you have decided that your claim requires professional help, you need to interview at least two or three candidates. Do not just hire the first person you find on Google. Treat this like hiring a key executive for your business, because you are handing them control of your largest financial asset. For a deeper dive into license verification, see our guide on how to find a licensed public adjuster.

Here is a safe, practical script you can use when calling a prospective firm to gauge their experience and operational style:

Hello, my name is [Your Name] and I am dealing with a [Water/Fire/Roof] claim with [Insurance Company Name].

The carrier has offered a settlement that is significantly lower than my contractor’s estimate. Before we discuss signing a contract, I would like to know:

1. Are you personally licensed in my state, and how many claims similar to mine have you handled in the past year?

2. Do you handle the estimating in-house using Xactimate, or do you outsource it?

3. How often do you communicate updates to your clients, and will I have a direct point of contact?

4. What is your standard fee structure for a claim at this stage?

I am looking for a professional who will thoroughly document the scope and keep me informed throughout the negotiation.

Listen carefully to their answers. Instead of vague promises about getting you a massive payout, a reliable professional will immediately provide their state license number and clearly explain whether their fee applies to the total claim or just the new money.

Getting these clear answers during an interview is your best defense against a bad experience. Once you have a qualified professional you can trust, you can finally stop fighting the insurance company and start focusing on your recovery.

Final Thoughts on Protecting Your Claim

The claims process is inherently imbalanced. The insurance company has teams of experts, sophisticated software, and vast financial resources. You have a damaged house and a confusing policy. A public adjuster levels that playing field.

You do not need to hand over control for every minor bump or scrape your house suffers. However, when you are facing a severe loss, hidden damage, or a carrier that simply refuses to acknowledge the reality of your repair costs, bringing in a dedicated advocate is often the smartest financial decision you can make. Document everything, verify their license, read the contract, and let the professional handle the fight so you can focus on putting your life back together.

Explore Our Complete Public Adjuster Library

Understanding the baseline role of a public adjuster is just the first step. Because every property claim involves different damage types, policy constraints, and timeline pressures, I have put together a dedicated library of resources to help you navigate your specific situation. Whether you are vetting candidates, decoding fee structures, or fighting a denied claim, these detailed guides will show you exactly what to expect.

| Category Guide | What You Will Learn |

|---|---|

| Public Adjuster Pros and Cons: The Honest Assessment Most Homeowners Never See | An honest, unbiased look at the real advantages and disadvantages of hiring representation, including when it might cost you more than it saves. |

| How Much Does a Public Adjuster Cost? Fees Explained Before You Sign Anything | A deep dive into contingency fee mechanics, how state caps work, and the critical difference between a percentage of the total versus a percentage of the increase. |

| Public Adjuster Contract: What to Read Before You Sign and What Are the Red Flags | What your contract must contain, hidden clauses to avoid, your rescission period rights, and what happens if you need to cancel. |

| How to Find a Licensed Public Adjuster: What to Check Before You Trust Anyone | Step-by-step instructions on verifying state licenses, spotting unlicensed storm chasers, and the exact questions to ask during an interview. |

| How Does a Public Adjuster Work? The Process and Timeline From First Call to Final Check | The exact sequence of events and timeline expectations once you sign a representation agreement, including how insurer communication changes. |

| Public Adjuster on Your Insurance Check: What It Means and What to Do Next | Why their name appears on your settlement check, how the endorsement process works, and what to do if the name is unfamiliar. |

| Public Adjuster vs. Attorney for Insurance Claims: Which One Your Situation Actually Needs | A clear role comparison to help you decide whether your claim requires a scope and valuation expert or legal intervention. |

| When to Hire a Public Adjuster: The Three Windows and When It’s Too Late | The optimal timing for bringing in help, and how to know if your settlement window has definitively closed after cashing a check. |

| Can a Public Adjuster Help With a Denied Insurance Claim? What They Can and Cannot Do | How to determine if your denial is a partial scope dispute they can fight, or a full coverage legal issue requiring an attorney. |

❓ FAQ

🧐 What exactly is a public adjuster?

A public adjuster is an independent, state-licensed insurance professional hired by a policyholder to help evaluate, document, and negotiate a property damage claim against their insurance company.

💰 How much do public adjusters take from a claim?

They typically charge a contingency fee ranging from 10% to 20%. You usually pay nothing upfront, and they only get paid when the insurance company pays you. The exact calculation depends on the fee structure; some charge on the total settlement, others only on the increase. See the fee section above for the key difference.

🛑 Can my insurance company drop me if I hire a public adjuster?

Generally speaking, your right to representation is protected, though specific non-renewal rules vary by state. In most states, insurers cannot legally penalize you simply for hiring a licensed professional to manage your claim.

⏱️ When is the best time to hire a public adjuster?

The best time is usually right after a severe loss or immediately after you receive an initial estimate from the insurer that is drastically lower than your contractor’s repair bid.

🤷♂️ Do I really need a public adjuster for a small leak?

Usually, no. If the damage is minor, easily visible, and straightforward to fix, hiring representation will unnecessarily cost you a percentage of a small settlement.

📝 Are public adjusters licensed professionals?

Yes. They must be licensed by the Department of Insurance in the state where the property is located, pass rigorous exams, and carry specific bonds to operate legally.

🤝 Can my roofing contractor act as my public adjuster?

Generally, no. As mentioned earlier, negotiating policy terms without a specific public adjuster license is illegal in most states. Your contractor can only discuss their own repair estimate.

⏳ How long does a claim take when you use a public adjuster?

While an adjuster takes over the workload, the negotiation process can actually extend the timeline of the claim. Fighting for a larger, accurate settlement often takes weeks or months longer than simply accepting a fast, lowball offer.

🚫 What happens if the public adjuster gets me nothing extra?

If you signed a contract based strictly on “new money” recovered, they will not get paid a fee if they fail to increase the insurance company’s original settlement offer.

🔍 How do I know if a public adjuster is legitimate?

See Mistake 2 above: license verification through your state’s Department of Insurance portal is the single most important step before signing anything. Avoid anyone who pressures you to sign immediately after a storm.

A public adjuster is one tool. These explain when and why it matters.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

Underpayment patterns vary by what caused the damage. These break each one down.

- How to tell if your situation actually warrants hiring one

- The difference between the adjuster you hired and the one who showed up

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When a denial needs legal leverage, not just negotiation

- Four paths to fight a denial, including one most homeowners miss

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.