- Never sign a public adjuster contract on the spot immediately following a major storm or disaster. Take time to read the specific terms.

- Ensure the contract explicitly states whether the fee percentage applies to the entire claim settlement or only to the new money the adjuster recovers above your prior offer.

- Most regulated states require a rescission period (usually 3 to 5 business days) allowing you to cancel the contract without owing any fees.

- Watch out for severe red flags like Assignment of Benefits (AOB) language, requests for upfront fees, or contracts that lack a clear termination clause.

The High-Pressure Reality of Signing a Claims Contract

Most public adjuster contracts are signed in the chaotic days immediately following a massive property loss. Whether your kitchen just caught fire or a severe windstorm tore the roof off your home, you are stressed, distracted, and motivated to act fast. Someone shows up at your door, presents themselves as an expert, and offers to take over the headache of dealing with the insurance company. They hand you a clipboard and tell you to just sign on the dotted line.

In my years of working in property claims, I have seen hundreds of homeowners sign these agreements without reading a single paragraph. That is precisely when reading carefully matters the most. Your signature on a public adjuster agreement legally binds you, alters how your insurance company interacts with you, and dictates exactly how much money will be deducted from your final settlement check.

Before you commit to representation, you need to understand that the terms written on that paper matter far more than the verbal promises the salesperson makes. This guide will walk you through exactly what a fair public adjuster contract looks like, the clauses that protect you, and the hidden traps that should make you walk away immediately. If you have not yet found an adjuster and are looking for advice on vetting them before you even get to the contract stage, you should read our guide on checking credentials and verifying licenses first.

What a Standard Public Adjuster Contract Must Include

A professional and legally compliant contract will protect both you and the adjuster. It should leave no room for ambiguity about what is being represented, how long the representation lasts, and how the compensation is calculated. When you sit down to review the agreement, verify that these specific elements are clearly written out.

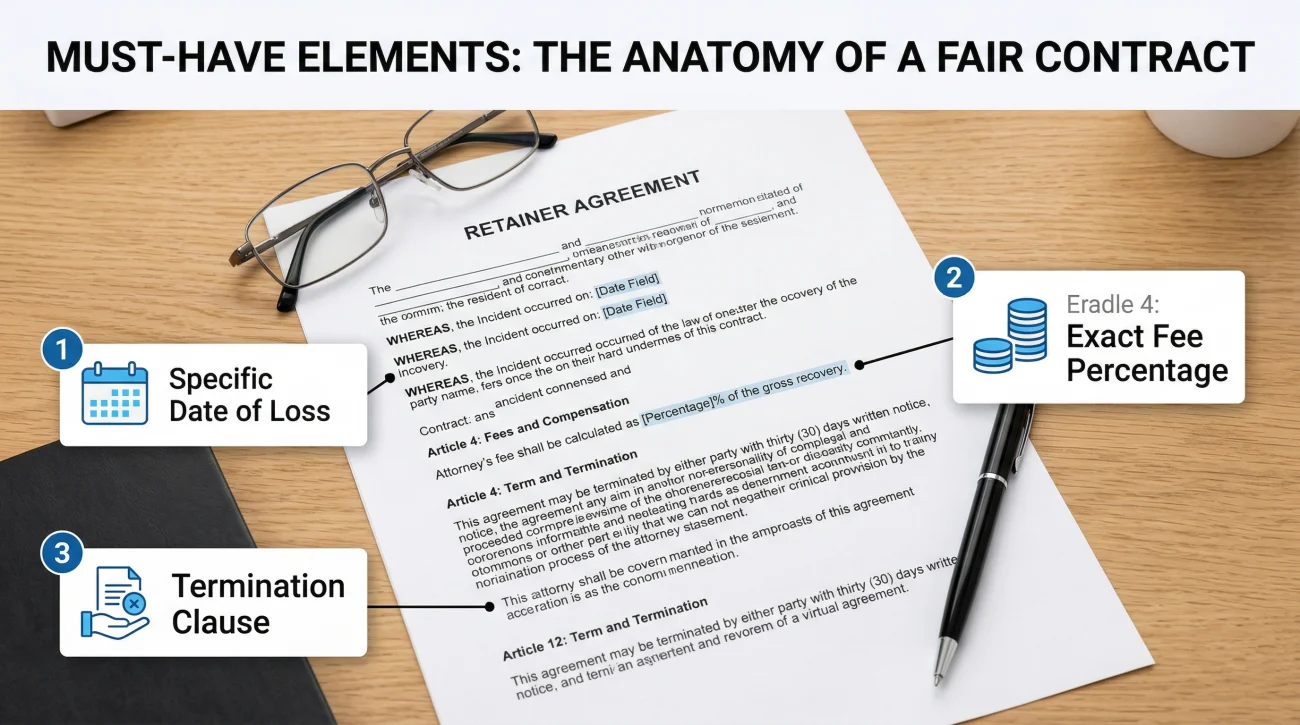

Specific Identification of the Loss Event

The contract must explicitly state the date of loss, the type of peril (such as a windstorm, fire, or burst pipe), and the specific property address being represented. A contract should never be a blank check for all future claims. I have reviewed bad contracts that contained vague language allowing the public adjuster to claim a percentage of any insurance payout the homeowner received for the next five years. The scope of representation must be strictly limited to the current, specific damage event.

Clear Fee Calculation Mechanics

The fee structure is the most critical part of the document. The contract must state the exact percentage the adjuster will charge. More importantly, it must define what that percentage is applied to. A fair contract will make a clear distinction between the total settlement and the increase above any prior offer from the insurance company.

💡 Pro Tip: Do not just accept a verbal “I charge ten percent.” Look at the contract language. Does it say “10 percent of the total settlement” or “10 percent of any supplemental funds recovered”? The difference in your net payout is massive.

Duration of Representation and Termination

The agreement should outline the duration of the contract and what happens if the claim takes longer than expected. It must also include a clear termination clause detailing exactly how either party can walk away from the agreement. If the contract does not explain how to cancel it, you should not sign it.

The Rescission Period: Your Emergency Exit

In most states that actively regulate public adjusters, consumer protection laws mandate that these contracts include a rescission window. A rescission period is a specific timeframe, typically 3 to 5 business days after signing, during which you can cancel the contract without penalty and without owing a single dollar.

This “cooling-off” period exists specifically because lawmakers know that homeowners are incredibly vulnerable right after a disaster. It allows you to sign the document, take a breath, have an attorney or trusted family member review it, and back out if you realize the terms are predatory.

Key Point: Know whether your state requires a rescission period and verify it is explicitly printed in your contract before signing. If your state requires it and the contract omits it, the adjuster is operating unethically or illegally.

If you decide to exercise your right to rescind, you must do so exactly as the contract dictates. This usually requires sending a formal written notice of cancellation via certified mail or verified email before the deadline expires. A simple phone call is never enough to legally break the contract.

Major Red Flags to Watch For in the Fine Print

When you are understanding the role of a licensed public adjuster, you learn that they are supposed to be your advocate. However, unethical operators use complex contract language to trap homeowners. If you see any of the following items in an agreement, hand the clipboard back and walk away.

Requests for Any Upfront Fees

Public adjusters work on a contingency basis. They only get paid when you get paid. If a contract asks for a “retainer,” an “inspection fee,” or any upfront payment before they have recovered money from your insurer, it is a severe red flag. Legitimate public adjusters assume the financial risk of evaluating your claim.

Assignment of Benefits (AOB) Language

This is one of the most dangerous clauses a homeowner can sign. An Assignment of Benefits legally transfers your rights under your insurance policy directly to the public adjuster or contractor. If you sign an AOB, the insurance company will write the checks directly to the other party, and you lose total control over your own claim. In most states, this practice is heavily restricted or entirely prohibited for public adjusters. Verify your state’s Department of Insurance regulations, but as a general rule, never sign away your actual policy rights.

Charging Fees on Prior Undisputed Offers

Imagine your insurance company has already inspected your roof and offered you $15,000. You think it should be $25,000, so you bring in an adjuster to fight for the extra $10,000. A predatory contract will apply their 20 percent fee to the full $25,000, meaning you pay them $3,000 out of the money the insurer was already willing to give you. A fair contract will only apply the fee to the “new money” they secure above that initial $15,000 offer. For a complete mathematical breakdown of how this works, read our guide on how public adjuster contingency fees are calculated.

Signing an agreement that simply states “Adjuster receives 15% of all claim proceeds.”

Signing an agreement that states “Adjuster receives 15% of all supplemental proceeds recovered above the carrier’s initial $15,000 undisputed offer.”

What Happens Immediately After You Sign the Contract

If you navigated those red flags and signed a fair agreement, the dynamic of your claim is about to alter drastically. I constantly hear from homeowners who are caught off guard by how fast the process changes the moment the ink dries on a public adjuster agreement. Once you sign, the adjuster will send a formal “Letter of Representation” to your insurance company. This document legally notifies the carrier that you have hired professional representation.

The immediate consequence is that the insurance company will stop talking to you. I have seen homeowners panic because their carrier suddenly refuses to answer a simple email about their own house. By law, once an insurer knows you are represented by a public adjuster, their desk adjusters and field inspectors must route all communications, emails, and settlement offers through your representative. Your phone will stop ringing. If you call the insurance company for an update, they will politely tell you that they are only permitted to speak with your public adjuster.

This change happens incredibly fast, often within 24 hours of signing. If you are not prepared for this communication blackout, it can feel like you have lost control of your home. A good public adjuster will explain this shift and set up a weekly communication schedule with you so you never feel out of the loop.

Can You Fire a Public Adjuster After You Sign?

Understanding these standard procedures matters most when things are going well. But what if you have already signed a bad contract and need to get out? One of the most common questions I get from panicked homeowners is whether they are permanently stuck if they hire the wrong person. The short answer is yes, you can fire a public adjuster. However, the contract termination clause determines exactly what you will owe when you do.

If you cancel within the legal rescission period, you owe nothing. If you terminate the contract weeks or months into the process, after the adjuster has performed physical inspections, built Xactimate estimates, and negotiated with the carrier, they are legally entitled to be compensated for their labor. This is known in legal terms as “quantum meruit” or the reasonable value of services rendered.

I once saw a homeowner terminate a PA contract because they felt the adjuster was ignoring them. A month later, the insurer finally agreed to pay a $40,000 supplement based directly on the estimate that fired PA had submitted. The PA legally placed a lien on the settlement check for their percentage, and the homeowner was shocked. But the contract’s termination clause clearly supported the PA’s right to the fee for the work already submitted.

Always review the termination clause before signing, not after you are angry. Understand exactly how they calculate this penalty if you break the agreement early—some specify an hourly rate, while many others use a vague “percentage of work completed” clause that can lead to surprisingly massive bills for a broken contract.

Signs Your Public Adjuster Contract Needs Immediate Attention

It is deeply unsettling to realize that the person you hired to fix your insurance nightmare might be creating a new one. I frequently review files for homeowners who are desperate to switch representatives because their current adjuster went completely silent the moment the contract was signed. If you have already signed an agreement and are reading this with a sinking feeling in your stomach, you need to evaluate your position objectively.

Here are the clearest signals that your contract situation needs immediate review:

- 🛑 The contract contained blank fields or vague descriptions of the damage that the adjuster promised to “fill in later.”

- 🛑 The contract does not specify whether the fee applies to the full settlement or only to the recovery above your prior offer.

- 🛑 There is no rescission or cancellation period stated anywhere in the document.

- 🛑 You want to cancel the agreement due to poor performance, but the termination clause is missing or demands an unreasonable cancellation penalty.

- 🛑 Your insurance check arrived with the public adjuster’s name on it, and you do not understand why you cannot cash it yourself.

A clearly written contract protects you, and a professional who will not provide clear written terms is a massive warning signal. If you are dealing with a vague contract or an unresponsive representative, you need to assess your options carefully. If you have not signed yet and are trying to decide if bringing in professional help is actually the right move for your specific damage, getting a free, no-obligation claim review is the best first step to take before any fee commitment is made.

Documentation Discipline: How to Cancel Properly

If you have read the contract, realized it is predatory, and you are still within your state’s legal rescission period, you must act with precise documentation. A phone call saying “I changed my mind” will not hold up if the adjuster decides to fight you for fees later.

Check the contract for the exact address where cancellation notices must be sent. Draft a formal email and follow it up with a certified letter through the postal service so you have a timestamped receipt proving you met the deadline. Keep the message completely devoid of emotion or accusations. Stick to the contractual facts.

Subject: Formal Notice of Contract Cancellation – [Your Name] / [Property Address]

Dear [Adjuster Name or Firm],

Pursuant to the rescission clause in our contract signed on [Date], I am submitting this formal written notice to cancel and terminate our public adjuster agreement for the property located at [Address].

Please confirm receipt of this cancellation notice and confirm that no Letter of Representation will be forwarded to my insurance carrier.

Thank you,

[Your Name]

⚠️ Warning: If you are outside the rescission window, do not send this cancellation letter without first reviewing your contract’s termination clause.

Final Thoughts on Protecting Your Claim

Navigating an insurance claim is difficult enough without having to fight the very professional you hired to help you. The contract you sign dictates the entire power dynamic of the relationship. Take the time to read the document in a quiet room, away from the damage and the high-pressure sales pitch.

Verify that the fee structure is fair, that your state’s required rescission period is included, and that you are not accidentally assigning your policy rights away through an AOB clause. A reputable, licensed public adjuster will gladly walk you through every single line of their agreement and will never pressure you to sign until you are completely comfortable with the terms.

❓ FAQ

📝 What happens after signing a public adjuster contract?

The adjuster will send a Letter of Representation to your insurance company. From that moment on, the insurer is legally required to route all communications, emails, and settlement discussions directly through your public adjuster, rather than calling you.

🛑 Can you fire a public adjuster after signing?

Yes, you can always terminate representation. However, if you fire them after the rescission period has ended and they have already performed work on your file, you will likely owe them compensation for their time and expenses as outlined in the termination clause.

⏳ What is a public adjuster rescission period?

It is a legally mandated “cooling-off” window, usually lasting 3 to 5 business days after signing, during which a homeowner can cancel the contract without any penalty or fee obligations. This protects people who signed under extreme duress after a disaster.

🌴 How long is the public adjuster contract cancellation period in Florida?

Florida law typically allows consumers to cancel a public adjuster contract within 3 business days of signing without penalty. During a declared state of emergency, this period is often extended. Always verify current rules with the Florida Department of Financial Services.

💰 Do I have to pay my public adjuster if I cancel?

If you cancel within the legal rescission timeframe, you owe nothing. If you cancel later, you generally have to pay for the reasonable value of the services they have already provided, such as inspections and estimating, as specified in the contract.

✍️ What are standard public adjuster agreement terms?

Standard terms include the specific property address, the exact date of loss, the contingency fee percentage, whether the fee applies to the new money or the total settlement, and a clear explanation of how the contract can be terminated by either party.

🚩 What are the biggest public adjuster contract red flags?

The most severe red flags include demands for upfront cash retainers, missing cancellation clauses, Assignment of Benefits (AOB) language that takes away your policy rights, and contracts that attempt to claim fees on future unrelated property damage.

❌ How to cancel a public adjuster contract legally?

You must follow the exact termination instructions printed in your agreement. This almost always requires sending a formal, written notice of cancellation via certified mail with a return receipt requested. Verbal cancellations are not legally binding.

📑 Can a public adjuster sign my insurance check?

No, a public adjuster cannot sign your name or forge your signature on a settlement check. However, because they have a contractual right to their fee, the insurance company will typically list both your name and the public adjuster’s name on the check, requiring both parties to endorse it.

🛠️ Is a public adjuster contract the same as a contractor’s AOB?

No. A public adjuster contract hires a licensed professional to negotiate your claim. A contractor’s Assignment of Benefits (AOB) transfers your actual policy rights to the builder who fixes your home. Never confuse the two, as an AOB legally surrenders your control over the claim funds entirely.

PAs are most useful in specific situations. These explain the ones that matter.

- The claim lifecycle a PA or attorney works inside

- The policy language that determines what professional help can recover

- How damage classification affects what an expert can negotiate

- Whether the situation you have justifies bringing in outside help

- When a denial is the outcome a PA could have prevented

- What a public adjuster actually does inside a claim

- When the dispute has moved past what a PA can handle

Each of these covers a real situation where the decision is not clear-cut.

- The 5 patterns that make hiring a PA worth it

- What the adjuster who came to your house was actually there to do

- When water damage scope gaps make independent review necessary

- When fire damage complexity makes independent representation worth it

- When the gap between estimates is large enough to bring in a PA

- When bad faith makes legal action the only path that works

- PA, attorney, or appraisal clause: which path fits your denial

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.