- Not all home insurance claims are treated equally. The specific type of damage you claim directly dictates how adjusters investigate it, the likelihood of a scope dispute, and the common reasons for underpayment.

- Water damage and roof claims have the highest volume and the highest rate of scope disputes, usually revolving around hidden moisture or pre-existing wear and tear arguments.

- Fire claims have the highest average settlement value, but homeowners routinely lose thousands because non-visible smoke and HVAC soot contamination are omitted from the initial scope.

- Certain damage types like mold and burst pipes hinge entirely on how the adjuster characterizes the event, focusing on sudden versus gradual timelines, rather than the physical damage itself.

- Universal red flags cross all damage types. If your settlement offer arrives within a week of major damage, or the inspection lasted under 60 minutes, your scope is almost certainly incomplete.

The Reality Behind the Scenes: Not All Claims Are Treated Equally

I have sat across from insurance adjusters on hundreds of property claims, reviewing line items, analyzing damage reports, and looking at the exact moments where a homeowner’s settlement falls off a cliff. If there is one truth I try to impart to every homeowner navigating the claims process, it is this: your insurance company does not view all damage through the same lens. Some claims settle smoothly and quickly. Others have dispute rates far above the industry average, and homeowners rarely know which category their specific damage falls into until after they have signed a settlement release.

When you file a claim, you see a damaged home that needs fixing. The insurance carrier, however, sees a specific category of loss. The nature of your damage affects how easy it is for an adjuster to underestimate the scope, what specific exclusions they will look for, and how aggressively they will investigate causation. Understanding the unique traps associated with home insurance damage types is the first step to protecting your financial recovery.

In my field experience reviewing claim files, the gap between what a homeowner needs to rebuild and what the insurance company offers is rarely a math error. It is a categorization error. The adjuster documents the damage type in a way that limits the policy’s exposure.

This guide breaks down the most common types of property damage, what insurance adjusters are trained to look for during their inspections, and the specific, predictable ways those claims get disputed. We will not be covering how to DIY a complex claim negotiation. Instead, I am going to show you the operational reality of how these different damage types are handled on the carrier’s side, so you know exactly what to document before the adjuster even knocks on your door.

At-a-Glance: Claim Complexity and Dispute Risk

Before diving into the specifics of each damage type, it helps to understand exactly what you are up against. I developed the comparison table below based on my observations of hundreds of active claim files. It outlines the relative dispute risk (scaled as Low, Medium, or High), the primary documentation needed, and the average complexity (scaled as Low, Medium, or High) for the most common property losses.

Use this quick reference to gauge how strictly you need to document your specific loss event.

| Damage Type | Dispute Risk | Primary Scope Gap | Complexity Level |

|---|---|---|---|

| Water Damage | High | Hidden moisture inside wall cavities, truncated drying times. | Medium |

| Fire & Smoke | High | Non-visible soot, HVAC contamination, personal property. | High |

| Roof Damage | High | Pre-existing wear characterization, missing flashings. | Medium |

| Storm & Hail | Medium | Multi-system damage ignored (siding, AC condenser). | Medium |

| Mold | High | Causation mischaracterized as gradual, sub-limit tactics. | High |

| Burst Pipe | High | Negligence denials regarding failure to heat or winterize. | Medium |

Primary Damage Categories: Where Claims Break Down

The six damage types below represent the vast majority of homeowners insurance claims. While they differ physically, each has a specific, predictable point of friction where insurance adjusters consistently push back or underestimate the scope. Understanding these nuances is crucial before you file.

Water Damage Claims: High Volume, Hidden Scope

Water damage represents the highest volume of daily claims, but it is also where the largest hidden scope gaps occur. The core issue is that water travels behind walls and under subfloors, and visual inspections routinely miss this moisture if adjusters fail to use thermal imaging or moisture meters. Furthermore, insurers often cap drying equipment times well below the required industry standards (IICRC S500). If your settlement only covers surface repairs, your scope is likely incomplete. Read our full guide on navigating a water damage insurance claim to protect your rebuild.

Fire and Smoke Damage: The Highest Average Settlement

Fire claims are the most complex, multi-layered losses a homeowner will face. They combine structural damage, personal property loss, and temporary displacement. While the physical burn damage is obvious, the non-visible smoke and soot contamination inside HVAC systems and wall cavities is systematically underscoped by adjusters. Because the financial stakes are massive and the nuances of smoke particulate are easy to visually dismiss, you must review our detailed fire damage insurance claim process before accepting any initial offer.

Roof Damage Claims: The Pre-Existing Wear Trap

The roof is the most frequently claimed single component and carries the highest rate of denial and underpayment industry-wide. The most endemic dispute is the pre-existing damage argument, where insurers conflate normal aging with sudden storm damage to deny coverage. Even approved claims routinely omit critical line items like drip edges, pipe boots, and the depreciation supplement. You can read our full breakdown of the roof damage claim process for specific details on closing these gaps.

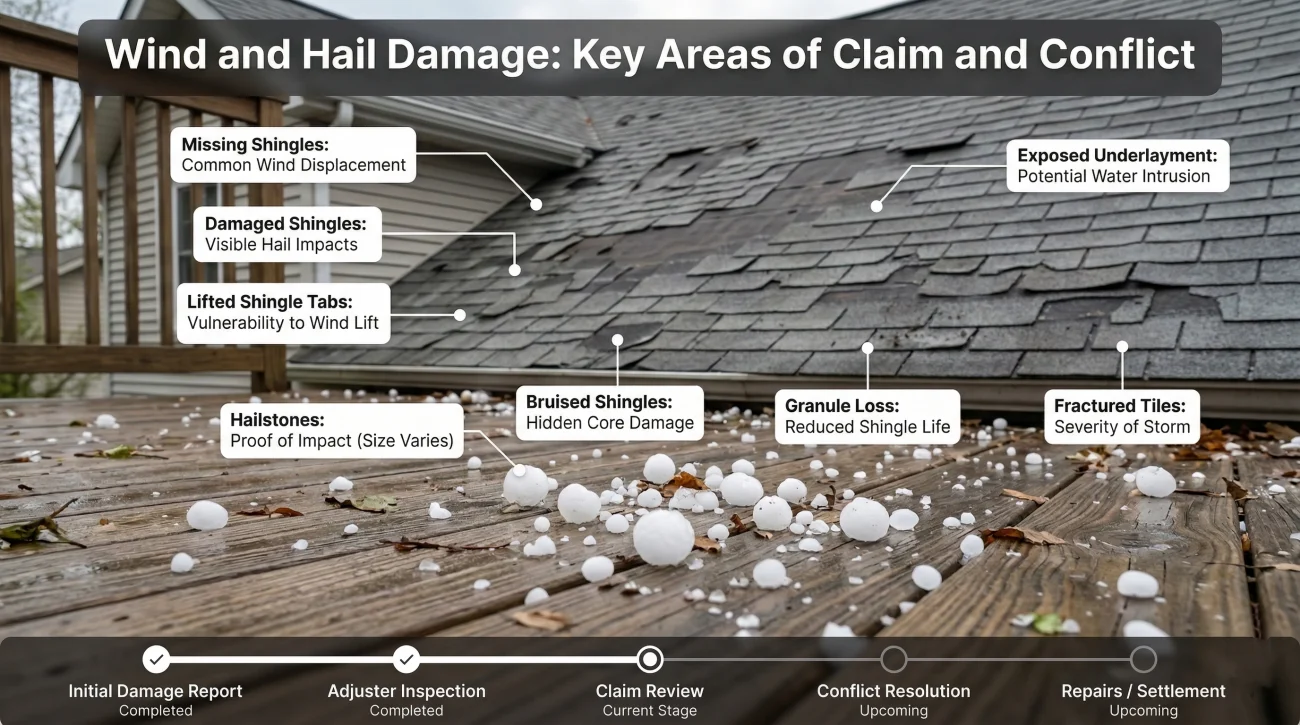

Storm and Hail Damage: The Rushed Inspection Problem

When major storms hit, insurers deploy independent adjusters who rush through multiple inspections a day, often missing multi-system damage to gutters, siding, and exterior AC units. Insurers also rely heavily on meteorological maps to verify hail size and wind direction, which can either validate or sink your claim based on your reported date of loss. For a comprehensive look at documenting these widespread events accurately, review our guide on the storm and hail damage insurance claim process.

Mold Damage Claims: The Causation Battleground

Mold claims hinge entirely on how the adjuster characterizes the initial moisture source. If they deem the leak a long-standing maintenance issue rather than a sudden event, the mold claim is denied completely. Note that determining how causation applies to your specific policy language is a coverage interpretation issue that this guide cannot dictate. Even when coverage applies, insurers frequently re-categorize standard water damage repair costs as mold remediation to artificially push the payout into a restrictive sub-limit. Learn more about fighting this tactic in our mold insurance claim guide.

Burst Pipe Claims: The Negligence Denial

Following the same mechanics as mold disputes, burst pipe claims hinge heavily on the sudden versus gradual distinction. In winter scenarios, insurers frequently issue denials arguing the homeowner was negligent by failing to maintain heat or winterize plumbing, especially if the home was temporarily vacant. How that distinction gets applied depends entirely on your specific policy language and the exact findings of the adjuster’s inspection. Our burst pipe insurance claim breakdown explains how to navigate these specific negligence disputes.

Other Critical Damage Categories You Must Document Carefully

While water, fire, and weather events make up the bulk of property losses, there are several other damage types that carry very specific, predictable pitfalls. The way you handle the first few days of these specific claims dictates your final payout.

External Smoke Damage

Smoke damage from a nearby wildfire or a neighbor’s structure fire presents a unique battle because there is no primary fire damage to your own home. Insurers frequently characterize this external smoke as a cosmetic odor issue to limit payouts to basic cleaning. They routinely ignore the need for HVAC duct replacement and porous material removal. Proving structural contamination requires independent air quality testing. See the smoke damage insurance claim guide for full documentation steps.

Sewer and Drain Backup

A sewer backup is classified as a Category 3 contamination event, requiring specialized extraction and demolition of porous materials. The primary dispute here usually involves endorsement limits. When the biohazard cleanup alone costs $12,000 but your endorsement limit is $5,000, disputes arise over what portions of the damage fall under the base policy. Read more on the sewer backup claim process.

Lightning and Electrical Surges

Lightning is a named peril, but proving causation is notoriously difficult. When a power surge destroys your HVAC compressor and appliances, insurers frequently attempt to attribute the failure to age or pre-existing electrical panel issues. Winning these claims requires highly specific documentation from independent technicians. Dive into the details in our lightning damage claim guide.

Tree Impact and Neighbor Disputes

When a tree hits your house, insurers may attempt to deny the claim based on a failure to maintain the property if the tree was visibly dead. Furthermore, if a neighbor’s tree falls on your property, the insurance liability mechanics become confusing for most homeowners very quickly. Discover how these lines are drawn in our tree damage claim breakdown.

Theft and Burglary

Theft claims are denied or underpaid heavily because of rigid documentation requirements. Insurers require a prompt police report and proof of ownership for stolen items. Categories like jewelry, electronics, and cash also have severe sub-limits that shock policyholders. See our theft claim process guide to understand the proof of loss hurdles.

Ordinance or Law (Code Upgrades)

If a severe storm damages your older home, the city may require you to upgrade the electrical or framing to current building codes during the rebuild. Standard policies only pay to replace what was there before. Unless you have Ordinance or Law coverage, you will be paying out of pocket for mandatory code upgrades. We explain how to identify this coverage in our ordinance or law coverage guide.

The First 48 Hours: Universal Checklists by Damage Type

The outcome of a property claim is often decided before the adjuster ever sets foot on your property. How you document the scene, what you throw away, and what you communicate in the first two days will either build a fortress around your claim or leave it completely vulnerable to underpayment.

I have reviewed thousands of claim files, and the homeowners who successfully recover their full policy benefits are the ones who treat the first 48 hours like a forensic investigation. Below are the specific actions you must take based on your damage type.

Water and Plumbing Checklist

- Stop the source of the water immediately and photograph the standing water before any extraction begins.

- Do not throw away the failed supply line, valve, or appliance part. The insurance carrier has the right to inspect the broken component to confirm it was a sudden failure.

- Hire a mitigation company to stop secondary damage, but do not sign a contract that allows them to gut the house without the insurer’s approval of the scope.

- Photograph the migration path. Show how the water traveled from the upstairs bathroom down through the ceiling below.

Fire and Smoke Checklist

- Secure the property by boarding up windows and doors to prevent theft or further weather damage.

- Request an immediate cash advance against your policy for emergency living expenses, clothing, and toiletries.

- Do not run your HVAC system. Running the air conditioning or heating will pull soot into the ductwork and contaminate the entire system, complicating your remediation.

- Start your personal property inventory room by room, capturing photos of debris piles before anything is shovelled out.

Storm, Roof, and Hail Checklist

- Place tarps over exposed roof decking or broken windows to mitigate further interior water damage.

- If you have hail, photograph the hailstones next to a tape measure or a coin to document the size on the exact date of loss.

- Walk the perimeter of your home and photograph the AC condenser, window screens, and siding.

Key Point: In storm claims, adjusters are trained to look for hail impacts on soft metals first. If they do not see dents on your gutters, downspouts, or AC fins, they will frequently argue that the damage to your tough asphalt shingles is just normal wear and tear. Photographing those soft metal dents yourself is crucial.

Theft and Vandalism Checklist

- Call the police immediately and wait for them to arrive. Your claim cannot proceed without an official report detailing the date and point of entry.

- Photograph all damage to doors, windows, and locks before initiating any repairs.

- Gather receipts, credit card statements, or warranty registrations for high-value missing items immediately, as adjusters will request proof of ownership within days.

For all communication during this critical window, keep everything in writing. A simple email summarizing a phone call with your carrier creates a permanent record.

Hello [Adjuster Name],

I am writing to confirm our phone conversation today regarding my water damage claim. You stated that the field adjuster will arrive on Thursday at 10 AM, and you authorized me to proceed with emergency water extraction. Please let me know if anything above is incorrect.

Thank you,

[Your Name]

DIY vs. Professional Help: When Do You Actually Need a Public Adjuster?

A question I am asked constantly is whether a homeowner needs to hire representation for every single claim. The honest answer from inside the industry is no. Not every claim requires a professional advocate. Knowing when to handle it yourself and when to call in a public adjuster is crucial for protecting your payout without giving up unnecessary percentage fees.

When to handle the claim yourself:

If you have a clear, isolated loss with a definitive scope, you can usually navigate the process alone. For example, if a localized wind gust blew off twenty shingles, or a small kitchen fire was contained strictly to the stovetop with no smoke migration, the repair scope is straightforward. Additionally, if the total claim value is under $5,000, or if your loss involves simple theft of standard electronics with clear receipts, hiring a public adjuster may not make financial sense.

When to hire a professional:

The dynamic changes completely when a claim involves hidden damage, subjective causation, or multi-layered coverage complexities. You should strongly consider hiring a public adjuster if:

- You suffer a major fire, where structural smoke contamination and total loss inventory are at stake.

- You have extensive water damage that requires tearing out drywall, cabinetry, and subflooring.

- Your initial settlement offer is drastically lower than the repair estimates provided by your local, licensed contractors.

- The insurance company issues a partial denial based on pre-existing wear, negligence, or a sudden versus gradual timeline argument.

- Your older home requires mandatory, expensive building code upgrades to legally complete the repairs.

Public adjusters speak the language of Xactimate, understand policy endorsements, and know how to document hidden line items that carrier adjusters routinely omit. If your claim falls into these complex categories, understanding exactly what a public adjuster does can be the difference between a fully funded repair and thousands of dollars out of pocket.

PAIN SECTION: Universal Signs Your Claim May Be Underpaid

Regardless of whether you handle the claim yourself or hire a professional, the operational tactics used by insurance companies leave recognizable footprints. After reviewing countless settlement letters and adjuster scopes, I look for specific patterns that indicate a homeowner is not receiving the full financial recovery they are entitled to under their policy.

These patterns are universal. They cross all damage types and all major insurance carriers. If you are experiencing the frustration of a confusing settlement, compare your situation against these universal signs that a claim is being undervalued:

- The settlement offer arrived within a week of significant damage. Speed in a major claim is rarely a sign of thoroughness. If you suffered a multi-room water event or a severe fire, and the carrier issues a binding settlement check within days, it almost certainly means they rushed the scope and omitted complex, hidden line items.

- Your contractor’s repair estimate is more than 20% above the settlement offer. A minor pricing discrepancy is normal in construction. A 20% or 30% gap is not a pricing debate; it is a scope gap. It means the adjuster entirely left out necessary materials, labor hours, or code-required upgrades.

- The adjuster visit was under 60 minutes for complex or multi-area damage. An adjuster cannot properly document moisture readings in four rooms, inspect a roof, check the HVAC system, and take 100+ photographs in 45 minutes. Short inspections yield short estimates.

- Secondary damage is not mentioned in the settlement letter. If you had a fire, but the scope does not mention smoke odor or HVAC cleaning. If you had a water leak, but the scope does not mention baseboards or subfloor. Missing secondary damage is the hallmark of an incomplete claim.

- Only visible surface damage was documented. No investigation of adjacent areas, no thermal imaging used, no lifting of carpets, and no checking behind cabinets. If they only paid for what they could see from the center of the room, you are being underpaid.

Final Thoughts on Managing Your Claim Type

Understanding the specific category of your property damage is your first line of defense. An adjuster approaches a flooded basement very differently than they approach a wind-damaged roof. By knowing the typical dispute patterns, you can anticipate the carrier’s objections and prepare your documentation accordingly.

Always communicate in writing, never assume a fast check is a complete check, and remember that you have the right to question the scope of the repairs. Your insurance policy is a contract designed to make you whole after a covered loss, but achieving that outcome requires active, informed participation on your part.

Bridging the Gap: What to Do Before You Sign

These underpayment patterns appear across all damage types. They are not the exception; in my experience, they are the operational norm for standard property claims. If your situation matches the signs outlined above, the pressing question is whether your specific repair scope was complete and accurate.

You do not have to accept the first offer the insurance company puts on the table, and you should not assume that the adjuster’s software caught every necessary line item. The burden of documenting the full extent of the loss ultimately falls on you, the policyholder. Because identifying missing line items requires a deep understanding of construction estimating, getting a professional second opinion is often the safest path forward.

A free review can answer the crucial question of what was missed before you sign any final releases or accept a check as payment in full.

Take action: If your claim feels rushed, incomplete, or undervalued, getting a second set of eyes on the scope before signing off can level the playing field. Whether you need a water damage review, a fire claim assessment, or a roof damage reinspection, professional guidance ensures you have the funds required to restore your home correctly.

| Damage Type Guide | What It Covers |

|---|---|

| Water Damage Claim | How adjusters miss hidden moisture behind walls and subfloors, and why drying scopes often fall short of industry standards. |

| Fire Damage Claim | The scope gaps that cost homeowners the most, focusing on HVAC contamination, non-visible soot, and personal property inventory. |

| Roof Damage Claim | Why the first offer is rarely full, pre-existing wear denials, matching disputes, and the ACV vs. RCV supplement mechanic. |

| Storm and Hail Damage Claim | Navigating rushed inspections, multi-system damage (siding, gutters, AC), and how meteorological data affects claim approval. |

| Mold Insurance Claim | Why the causation question (sudden vs. gradual) drives disputes, and how sub-limits severely restrict remediation payouts. |

| Burst Pipe Claim | Fighting the negligence denial (failure to heat or winterize), the vacancy problem, and proving the event was sudden and accidental. |

| Tree Damage Claim | What happens when a tree hits your house, neighbor liability mechanics, dead-tree negligence denials, and removal sub-limits. |

| External Smoke Damage Claim | Proving structural contamination from wildfires or neighbor fires when the insurer characterizes the damage as merely “cosmetic odor.” |

| Sewer Backup Claim | Handling Category 3 contamination, health hazard documentation, and navigating restrictive endorsement sub-limits versus the base policy. |

| Lightning Damage Claim | Proving causation when the insurer attributes blown HVAC units and fried electronics to age or pre-existing electrical failure. |

| Theft and Burglary Claim | Filing correctly to avoid denial, the strict requirement for police reports, proof of ownership hurdles, and severe item sub-limits. |

| Ordinance or Law Claim | The hidden coverage that pays for mandatory building code upgrades (electrical, framing, roofing) during a major repair rebuild. |

❓ FAQ

🕵️♂️ What is the most common home insurance claim?

Wind and hail damage are historically the most frequent claims due to severe weather patterns, closely followed by water damage claims from internal sources like plumbing failures and appliance leaks.

⏳ How long does an insurance company have to investigate a claim?

Timelines vary strictly by state regulations, but most standard guidelines require the insurer to acknowledge the claim within 15 days, begin investigation promptly, and issue a decision within 30 to 45 days of receiving all requested proof of loss documentation.

🏚️ Why do roof damage claims get denied so often?

Roof claims are frequently denied because adjusters attribute the damage to long-term wear and tear, age, or poor maintenance rather than a sudden, covered storm event. Separating normal aging from fresh storm damage is the primary area of dispute.

💧 Does homeowners insurance cover hidden water damage?

It generally covers hidden water damage only if the source of the leak was sudden and accidental. If the hidden damage was caused by a slow, gradual leak that went unnoticed for months, it is typically excluded under maintenance clauses.

🦠 How does an adjuster determine if mold is covered?

An adjuster determines mold coverage by investigating the source of the moisture. In most policies, mold is only covered if it is the direct, resulting consequence of a covered peril like a sudden pipe burst.

🔥 Why is smoke damage hard to get covered after a fire?

Smoke damage disputes arise because insurers often treat lingering odor as a cosmetic issue requiring simple cleaning. In reality, smoke particulate embeds into porous materials and HVAC systems, requiring expensive structural remediation.

❄️ Will my insurance pay if a pipe freezes and bursts?

Yes, standard policies generally cover sudden burst pipes, but they often include a strict negligence exclusion. If the insurer determines you failed to maintain adequate heat in the home or failed to winterize the plumbing, they can deny the claim.

🌩️ Do I need to prove a lightning strike caused my electrical damage?

While the burden is technically on the insurer to prove an exclusion, homeowners often must provide independent documentation, such as weather reports confirming a strike and a licensed electrician’s report stating the damage is consistent with a surge.

🌳 What happens if a neighbor’s tree falls on my house?

If a neighbor’s tree damages your house, you typically file the claim through your own homeowners insurance. Your neighbor is generally only liable if you can prove they were negligent and ignored prior warnings to remove a visibly dead tree.

📝 What should I do if my settlement estimate is too low?

Do not sign a final release. Document the discrepancies by getting a detailed, line-item estimate from a licensed contractor. If the gap is significant, consider hiring a public adjuster to independently evaluate the scope and negotiate with the carrier.

From filing to settlement: the parts worth understanding before something goes wrong.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

These cover the situations where professional help most often changes the outcome.

- 5 patterns that signal your settlement is probably short

- Who the adjuster at your door actually works for

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When a denial needs legal leverage, not just negotiation

- Four paths to fight a denial, including one most homeowners miss

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.