- Sewer backups are classified as Category 3 “black water” events, requiring strict contamination protocols and material removal rather than just drying.

- Most standard policies do not cover backups automatically. They require a specific endorsement which often comes with strict sub-limits like $5,000 or $10,000.

- Proper documentation from a licensed plumber stating the exact origin and cause of the blockage is mandatory to trigger coverage.

- When remediation scopes are cut short due to coverage limits, secondary mold growth becomes a massive risk within 24 to 72 hours.

The Reality of a Sewage Backup Event

A sewer or drain backup is one of the most distressing events a homeowner can face. The smell, the health hazards, and the immediate need for professional cleanup create a chaotic environment. In my time working through complex property claims, I have seen homeowners panic, call the first available mitigation crew, and start tearing out carpets before taking a single photograph. That understandable urgency is exactly where the insurance claim process begins to derail.

Unlike a clean water leak from a broken supply line, a sewer backup introduces severe contaminants into your home. If you do not understand the rules of engagement before the cleanup crew arrives, you risk authorizing work that exceeds your coverage limits or accepting a settlement that leaves hidden hazards behind.

To successfully navigate this process, you have to treat the event not just as water damage, but as a severe contamination event. By documenting the source correctly, managing your endorsement limits carefully, and understanding the industry standards for cleanup, you can protect yourself from a denied or severely underpaid settlement.

Understanding Category 3 Water and Your Cleanup Scope

When an adjuster assesses a standard water damage claim process, they look at the source of the water to determine the appropriate cleanup method. A sewer backup is not just water. Under the Institute of Inspection, Cleaning and Restoration Certification (IICRC) S500 standards, sewage backup is classified as Category 3 water, commonly known as black water. This classification fundamentally changes the scope of your claim.

Category 3 water is highly contaminated and contains pathogenic, toxigenic, or other harmful agents. Because of this, the remediation scope approved by the adjuster must be far more aggressive than it would be for a clean water leak. You cannot simply extract the water, place a few fans, and call the job done. Any porous materials that have absorbed Category 3 water must be removed and discarded.

In my experience reviewing mitigation files, one of the most frequent adjuster errors is writing a ‘clean and extract’ line item for carpet and carpet pad that has been saturated by a drain backup. Under Category 3 protocols, that carpet and pad must be ripped out, bagged, and safely discarded. Accepting a scope that only pays to dry contaminated materials leaves a severe health hazard in your home.

Here is how the scope should differ when your home experiences a backup event:

| Material Affected | Standard Clean Water Protocol | Category 3 Sewer Backup Protocol |

|---|---|---|

| Carpet and Pad | Extract water, float carpet, apply heavy drying equipment. | Remove entirely, dispose of properly, treat subfloor with antimicrobials. |

| Drywall and Insulation | Remove baseboards, drill holes for airflow, dry in place if intact. | Cut away at least two feet above the highest waterline, remove and discard insulation. |

| Hardwood Flooring | Extract water through mats, utilize specialized floor drying systems. | Often requires complete removal if contaminated water has penetrated the joints and subfloor. |

⚠️ Warning: If the estimate you receive from your insurance company suggests cleaning and drying porous materials that were touched by sewage, the scope is fundamentally flawed and must be challenged.

The Endorsement Limit Problem: When Your Coverage is Capped

The endorsement limit is where most sewer backup claims fall apart. Standard homeowners insurance base policies generally exclude damage caused by water that backs up through sewers or drains. To have coverage, you must have a specific “Water Backup and Sump Overflow” endorsement added to your policy.

The problem is that these endorsements usually come with strict sub-limits. While your main dwelling coverage might be $400,000, your sewer backup endorsement might only be capped at $5,000, $10,000, or perhaps $25,000. In a severe event involving a finished basement or a main living area, a $5,000 limit might not even cover the emergency extraction and demolition, leaving absolutely zero funds for rebuilding.

What to Do When the Limit Runs Dry

When your endorsement limit is exhausted but the cleanup is only half done, you face a critical decision. You can request the mitigation contractor to itemize and separate their invoice, clearly distinguishing between emergency extraction (which falls under the endorsement) and tear-out of subsequent damage (which might fall under the base policy if a resulting peril like a burst pipe occurred). Never blindly authorize open-ended work without written confirmation of how the contractor will bill for overages.

When the actual remediation scope exceeds the endorsement limit, disputes inevitably arise. Proving where the endorsement ends and the base policy begins requires meticulous documentation to ensure the insurer is categorizing the damage correctly. You can read more about how insurers categorize different perils in our guide covering the different types of property damage claims.

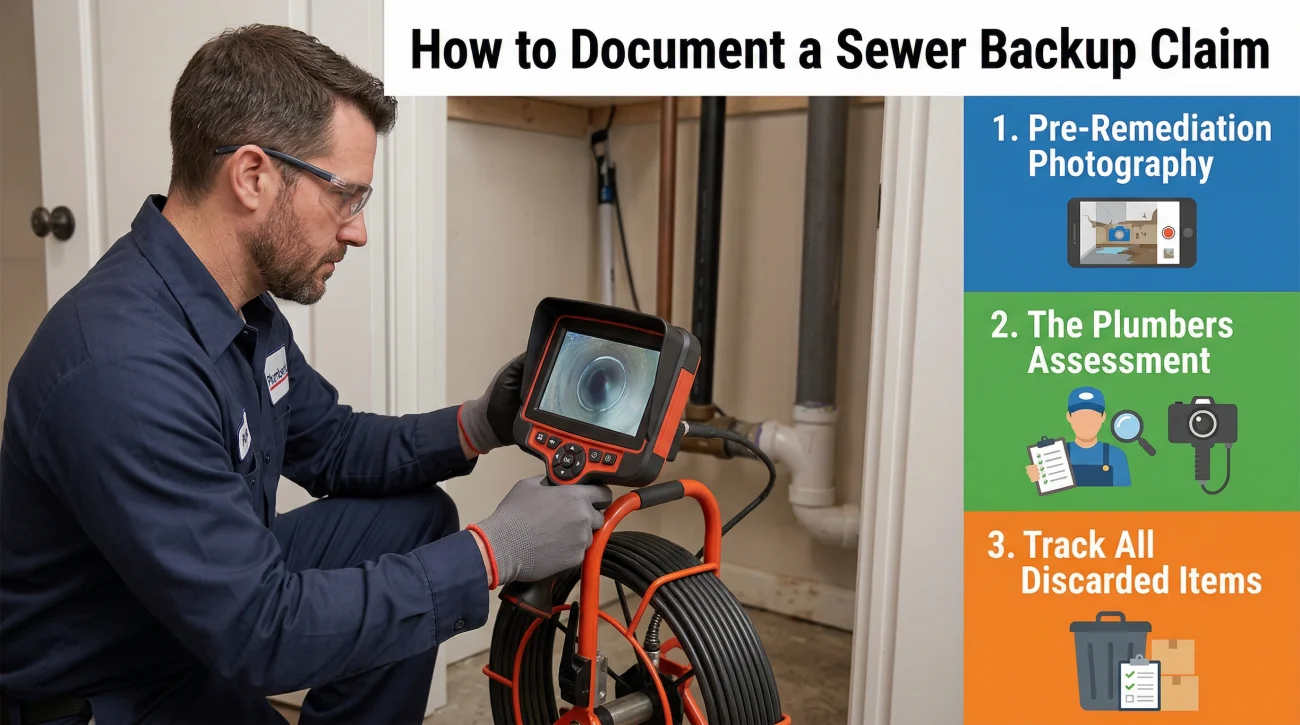

How to Document a Sewer Backup Claim Correctly

Because you are dealing with a strict policy endorsement and a severe health hazard, documentation is your only defense against a denied claim or an artificially low settlement. You must capture the evidence before the cleanup crew makes it disappear.

Step 1: Pre-Remediation Photography

Before a single piece of drywall is cut or a vacuum is turned on, photograph the entire affected area. You need to document the exact height the water reached on the walls, baseboards, and furniture. This visual evidence justifies the tear-out scope later. If you do not have photos of the water level, the adjuster may argue that the contractor cut away too much drywall and refuse to pay for the replacement materials.

Step 2: The Plumber’s Assessment

The insurance company needs to know exactly what caused the backup to determine if the endorsement applies. A vague invoice from a plumber will almost guarantee a delay. You need the plumber to write a specific, detailed report on their company letterhead.

Plumber invoice says “Cleared clogged drain in basement. $250.”

Plumber invoice says “Camera inspection revealed tree roots breached the main sewer line 30 feet from the foundation, causing municipal waste to back up through the basement floor drain. Line snaked and cleared.”

If you need to guide your plumber on what to write, use a script similar to this when requesting their final report:

Hello [Plumber Name],

Thank you for clearing the backup at my property today. Because I am filing an insurance claim, my adjuster requires a detailed description of your findings on the invoice.

Could you please update the invoice to clearly state the exact location of the blockage (e.g., main sewer line, municipal connection) and the specific cause of the backup (e.g., system overload, root intrusion)? This documentation is critical for my coverage assessment.

Thank you for your help.

Step 3: Track All Discarded Items

Because Category 3 water ruins almost everything porous it touches, you will likely have to throw away rugs, clothing, furniture, and stored boxes. Do not throw anything in the dumpster until you have taken clear photos of the items and recorded their brand, age, and estimated replacement cost. Adjusters cannot pay you for contents they cannot verify existed.

Pro Tip: Always keep a physical claim log. Write down the name of every representative you speak with, the date of the conversation, and a summary of what was promised. When disputes over coverage limits or mitigation timelines arise, a detailed log is your best tool for holding the insurer accountable.

The Liability Question: Municipal vs. Private Lines

One detail that frequently gets overlooked is exactly where the blockage occurred. If the backup originated in the municipal sewer main rather than your private lateral line, the responsibility for the damage might not rest entirely on your homeowners policy.

In cases where the city system failed, documenting the municipal origin via your plumber’s camera inspection creates a record that opens a separate avenue for recovery beyond your homeowners policy, one worth discussing with a professional.

The Hidden Health Hazard: HVAC and Wall Cavity Contamination

Visual inspections consistently underestimate the true scope of a sewage backup. Water is insidious, and black water is dangerous. While the adjuster will easily see the damaged flooring and drywall, they often miss the secondary contamination pathways that require extensive cleaning.

If your home relies on floor registers or if your HVAC ductwork runs through a crawlspace or basement that was flooded, sewage has likely entered your ventilation system. When the furnace or AC kicks on, it can distribute airborne pathogens throughout the entire house. An adjuster doing a basic walkthrough rarely inspects the interior of the ductwork.

Key Point: If Category 3 water has breached your ductwork, standard surface cleaning is insufficient. The ductwork must be professionally decontaminated or completely replaced, and the HVAC unit itself must be inspected for contamination.

This is where independent industrial hygienist testing becomes incredibly valuable. An industrial hygienist can take swab tests inside wall cavities and air quality samples throughout the home. Their written report provides undeniable, scientific documentation of contamination that a visual inspection cannot capture. When an insurer attempts to deny the replacement of ductwork or subflooring, a hygienist’s report forces them to confront the scientific reality of the contamination.

When Inadequate Cleanup Triggers a Secondary Claim

Even when the visible cleanup appears complete, the contamination window is already closing, and mold does not wait. Timing is critical in any water event, but it is especially unforgiving with sewage.

If mold appears after a remediation company has supposedly finished their work and signed off on the job, a complex liability dispute begins. The insurer will often argue that the mitigation was completed successfully and any subsequent mold is a new, excluded maintenance issue.

Pursuing a secondary mold claim in this scenario requires proving that the original contractor failed to achieve the necessary clearance standards, or that the adjuster forced a premature end to the drying process by capping the approved scope. This is exactly why you must demand post-remediation verification testing before signing any certificate of completion.

Signs Your Sewer Backup Claim is Being Underpaid

The confusion surrounding endorsement limits and contamination standards leaves homeowners highly vulnerable to underpayment. If you are experiencing any of the following scenarios, the scope of your claim is likely incomplete and requires intervention.

- 📍 The adjuster is applying your endorsement sub-limit to the entire claim, ignoring ensuing damage that should legitimately fall under your base policy limits.

- 📍 Your remediation contractor states the necessary cleanup scope is larger than what the adjuster has authorized.

- 📍 The insurance company approved drying out porous materials (like carpets or drywall) instead of removing them, ignoring Category 3 contamination protocols.

- 📍 Mold has appeared in the affected areas weeks after the cleanup was supposedly finalized.

- 📍 The adjuster did not commission hygienist testing, meaning contamination in wall cavities and ductwork may have been left entirely unquantified.

Sewer backup claims involve severe contamination that a standard visual inspection consistently underestimates. When your health and the structural integrity of your home are at risk, relying solely on the insurance company’s initial assessment is a dangerous gamble. Whether the adjuster’s scope matches the actual contamination level is a question that requires independent verification.

If your settlement offer is drastically below your remediation costs, or if your cleanup was halted due to limit disputes, you need to escalate the situation. Getting a free scope review from a licensed public adjuster to assess your water damage is the most effective way to identify what was missed in the estimate before you sign any final releases.

Final Action Steps Before You Sign

A sewer backup claim requires strict discipline. Before you accept a settlement or sign a contractor’s certificate of completion, you must be certain that the Category 3 contamination has been fully addressed, not just visually hidden.

Demand independent testing, scrutinize how your endorsement limits are being applied, and never assume that a clean-smelling room means the health hazard is gone. Protect your property by verifying the science behind the cleanup and holding the insurer to the correct industry standards.

❓ FAQ

🚽 How do I know if my insurance covers a sewer backup?

You must check your policy’s declarations page for a specific endorsement usually labeled “Water Backup and Sump Discharge.” Standard base policies almost always exclude this peril. If the endorsement is listed, check the dollar limit attached to it.

📸 What should I photograph before the cleanup crew arrives?

Photograph the source of the backup, the exact high-water line on walls and furniture, all damaged personal belongings in their original place, and the overall spread of the water across the floors. This proves the scope of the inundation.

📝 What exactly does the adjuster look for in a sewage claim?

The adjuster looks for the exact origin of the water to confirm coverage, verifies the endorsement limit, and assesses the visible damage to determine the mitigation scope. They also look for any signs of pre-existing maintenance issues.

💰 What happens if the cleanup costs more than my coverage limit?

If your mitigation and repair bills exceed your endorsement limit (e.g., a $15,000 bill on a $5,000 limit), you are generally responsible for the out-of-pocket difference. However, a professional review can sometimes find ensuing damage covered under the base policy.

⏳ How long do I have to file a drain backup claim?

You must file the claim promptly, typically within a few days of discovery. Delaying the claim gives the insurer grounds to deny it based on failure to mitigate damage, as sewage causes rapid secondary deterioration and mold.

🦠 Can I claim mold damage if the sewage backup caused it?

If the mold is a direct result of the covered backup event and developed despite your prompt efforts to mitigate the damage, it may be covered. However, it is often subject to its own strict sub-limits and requires clear causation proof.

😷 Do I have to stay in the house during a Category 3 backup?

No. Category 3 water poses severe health risks. If the home is uninhabitable, you should ask your adjuster if your policy’s Additional Living Expenses (ALE) or Loss of Use coverage applies while the contamination is remediated.

🛠️ Should I let the insurance company pick the cleanup crew?

You have the right to hire your own licensed and certified mitigation contractor. While insurers offer preferred vendors, hiring your own independent crew ensures they are working strictly for your best interest, not trying to save the insurer money.

📄 What documents should I send to prove the backup wasn’t my fault?

Provide a detailed, written invoice from a licensed plumber stating the exact location of the blockage (e.g., municipal line or tree roots) and clearly stating it was a sudden backup, not a long-term maintenance failure on your part.

⚖️ Can I reopen my claim if I find more contamination later?

Yes, as long as you have not signed a final release of liability and your policy’s claim period has not expired. You can submit a supplemental claim with new evidence, such as a hygienist’s report proving hidden contamination.

Damage type affects coverage, documentation, and payout. These connect the dots.

- How the settlement process works after damage is reported

- Which parts of your policy apply when damage is involved

- How your damage type affects what the insurer is required to pay

- Whether the damage you have is actually worth filing for

- What happens when the claim you filed gets rejected

- How independent representation changes what gets documented

- When a disputed claim moves into legal territory

Each damage type has its own patterns. See what adjusters commonly miss.

- Whether your damage assessment left money on the table

- What the inspector who came to your home was actually there to do

- The parts of water damage that standard inspections routinely miss

- What fire and smoke assessments leave out of the scope

- Why the insurer's roof estimate is almost always lower than the roofer's

- When a denial crosses into bad faith and needs legal leverage

- The four options after a denial, including one most homeowners skip

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.