- Filing a police report immediately is a non negotiable requirement; missing this step is a primary reason theft claims are denied.

- Proof of ownership is the hardest hurdle. Adjusters require receipts, serial numbers, or clear photographic evidence to pay full value.

- Standard policies have strict sub limits for high value items like jewelry, cash, and electronics, meaning your payout may be capped regardless of the item’s actual worth.

The Reality of Filing a Theft Claim

When you come home to a kicked in door or a shattered window, the emotional toll is immediate. You call the police, you survey the damage, and you eventually call your insurance company. Most people assume that because theft is a covered peril on a standard policy, a homeowners insurance theft claim will be a straightforward process of listing what is missing and getting a check. Unfortunately, that is rarely how it works in practice.

Theft claims are denied or severely underpaid more often than almost any other type of property claim. This high failure rate isn’t usually a question of coverage. Rather, it comes down to documentation, because very few of us maintain perfect records of everything we own.

In my years of reviewing property claims, I have seen hundreds of legitimate theft claims stall out because the homeowner could not prove they owned the items they were claiming. An adjuster’s job is to verify the loss, and without a paper trail, their hands are tied.

As a property claims writer, I have sat on the operational side of these disputes. I know what the adjuster is looking for when they open your file, and I know exactly where the process breaks down for the average homeowner. In this guide, I will walk you through the exact steps to file your claim correctly, how to gather proof of ownership when you think you have none, and how to spot the early warning signs of an investigation.

The Police Report Requirement

The most critical rule of any theft claim is straightforward: you must file a police report, and you must do it immediately. Insurance companies treat theft with a high degree of scrutiny due to the potential for moral hazard or fraud. The police report is the foundational document that proves a crime actually took place.

A delayed police report or a missing police report is one of the fastest ways to get a home insurance claim denied outright. If you discover a burglary on a Friday but wait until Monday to visit the precinct, the adjuster will immediately question the validity of the timeline.

When you file the report, accuracy is vital. The items you list on the police report must match the items you eventually claim with your insurance company. If the police report states that a generic laptop was stolen, but you submit a claim for a brand new, maxed out MacBook Pro, the adjuster will flag the discrepancy. Take the time to be as specific as possible with the responding officer.

⚠️ Warning: Never assume the police will automatically send the report to your insurer. It is your responsibility to obtain a copy of the final report or at least the official incident number and the responding officer’s contact information to provide to your adjuster.

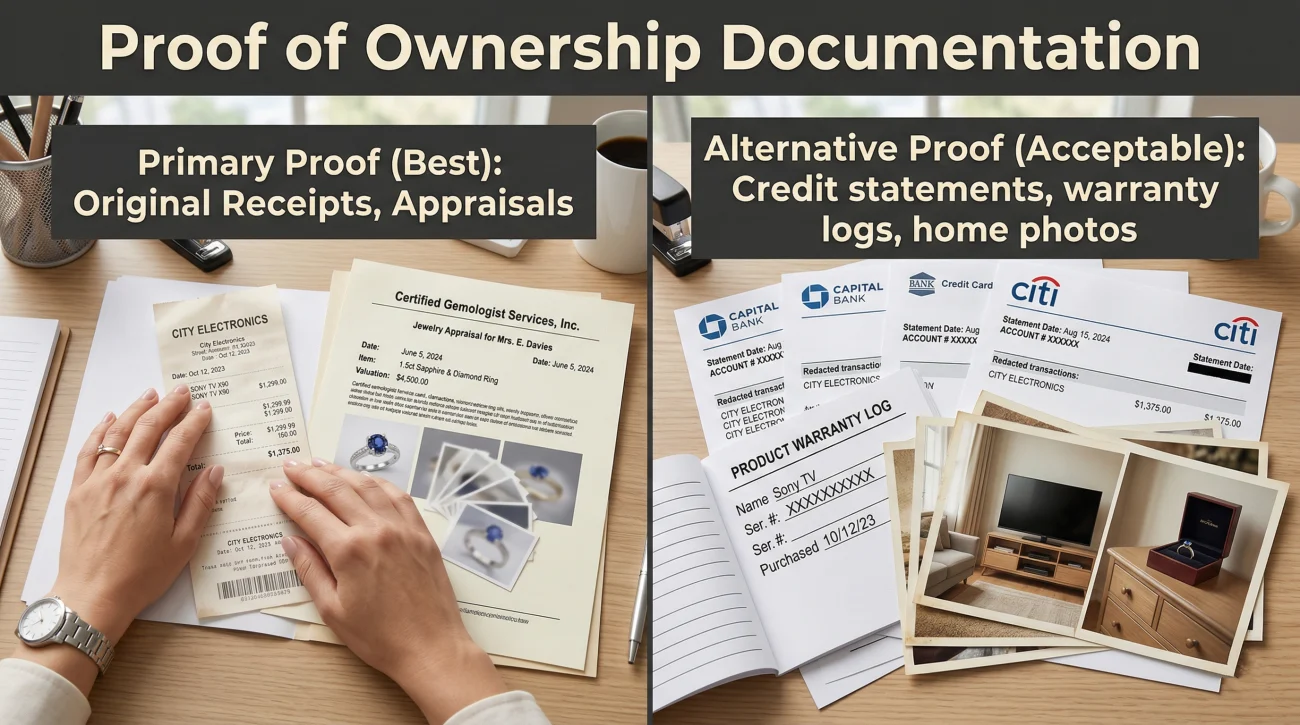

Proof of Ownership Documentation

Once the police report is filed, you face the hardest part of the process. You have to prove to the insurance company that you actually owned the items that were taken, and you have to prove what they were worth. This is where the majority of theft claims fall apart.

The gold standard for proof of ownership is a combination of a dated purchase receipt and a photograph of the item in your home. However, very few people have receipts for a television they bought four years ago or a necklace they received as a gift.

If you do not have the original receipts, you have to reconstruct your paper trail. Adjusters will accept alternative forms of proof, provided they clearly link you to the item. Here is how I advise homeowners to build their documentation file.

| Item Type | Primary Proof (Best) | Alternative Proof (Acceptable) |

|---|---|---|

| Electronics (TVs, Laptops) | Store receipt with date and price | Credit card statements, digital warranty registrations, owner manuals, photos showing the item in your living room. |

| High-End Clothing & Bags | Original designer receipt | Online order confirmation emails, credit card pull, photos of you wearing the item. |

| Jewelry | Recent professional appraisal | Certificate of authenticity, high resolution photos, jeweler cleaning records. |

| Tools and Equipment | Hardware store receipt | Home depot or Lowe’s pro account digital logs, photos of your garage setup. |

For high value items that were given to you as gifts, you may need to ask the person who gifted it to you to provide a written statement or track down their original purchase record. If you are relying on bank statements, highlight the specific transaction and match the dollar amount to the item’s known retail price.

Subject: Reconstructed Proof of Ownership for Stolen Laptop

Hello [Adjuster Name],

As requested, I am providing proof of ownership for the stolen Dell XPS 15 laptop. While I no longer have the paper receipt, I have attached three items to verify ownership:

1. A PDF of my Chase credit card statement from October 2022 showing a charge of $1,850 to Best Buy.

2. A screenshot of the digital warranty registration linked to my email address.

3. A photograph taken in my home office last year where the laptop is clearly visible on the desk.

Please let me know if this satisfies the documentation requirement for this line item.

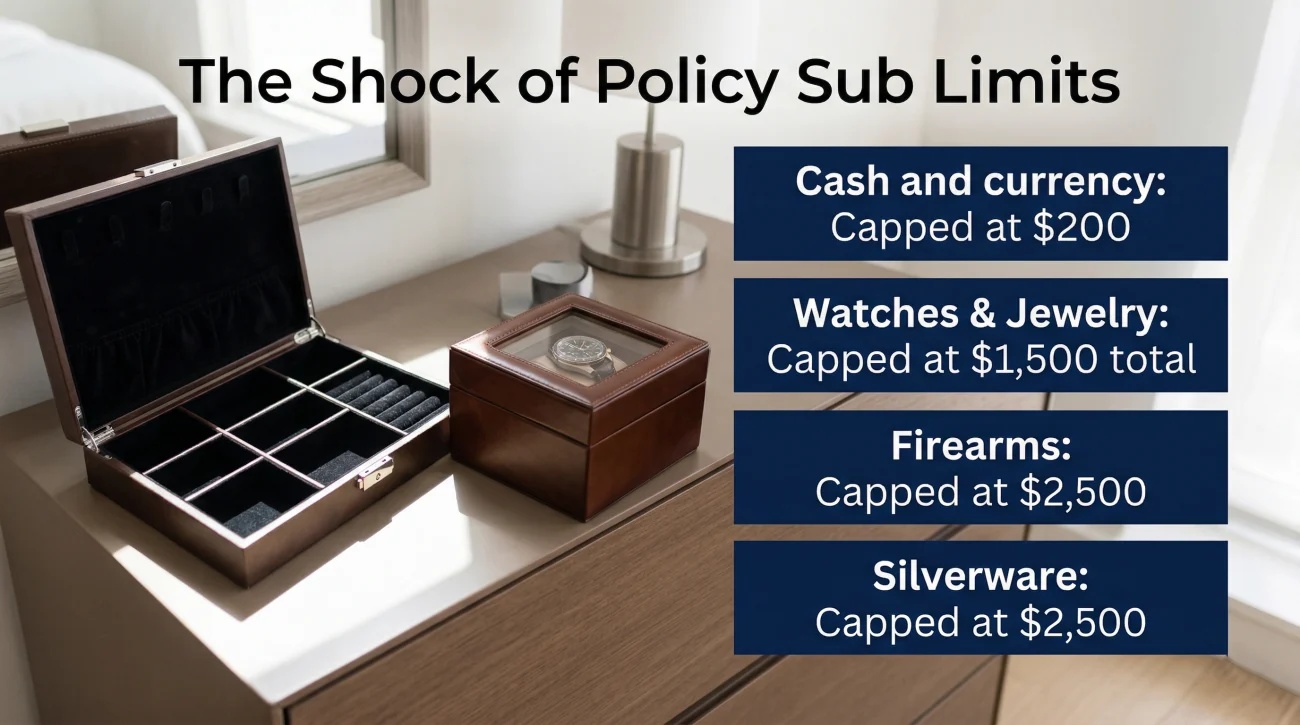

The Shock of Policy Sub Limits

One of the most painful conversations I see happen during a theft claim revolves around sub limits. Most homeowners assume that if they have $100,000 in personal property coverage, they can claim up to $100,000 for whatever was stolen. This is not true.

Standard homeowners policies contain strict limits for specific categories of high risk items. These caps apply regardless of your overall coverage limit. Common theft sub limits in a standard policy typically look like this:

- 💵 Cash and currency: Capped at $200

- 💍 Watches, jewelry, and precious stones: Capped at $1,500 total

- 🔫 Firearms: Capped at $2,500

- 🍴 Silverware and goldware: Capped at $2,500

If your stolen items exceed these limits, the only way to recover full value is if you previously added a “scheduled personal property endorsement” (often called a floater) to your policy. A floater explicitly lists and insures high value items individually. If you didn’t buy a floater before the theft, the base sub limit is all you will receive.

Assuming your $5,000 engagement ring will be fully reimbursed because your overall property limit is high enough.

Reading your declarations page immediately to understand the exact caps applied to jewelry and cash, so you can set realistic expectations before the adjuster sends the settlement letter.

If you are currently facing a massive gap between your actual loss and the adjuster’s offer due to how items were categorized, it might be worth having a professional review the file. Understanding how these limits fit into the broader picture of home insurance claims by damage type helps clarify how adjusters manage payout risks.

Theft Away From Home: Cars, Hotels, and Storage

Not all theft claims happen at the primary residence. Someone might break into your car at the gym, or your luggage might be stolen from a hotel room while you are on vacation. Your homeowners insurance still covers your personal property in these situations under an “off-premises” clause.

However, there is a catch that catches many travelers off guard. Most policies cap off-premises personal property coverage at 10% of your total property limit. If you have $100,000 in total property coverage, your maximum payout for a theft on vacation is $10,000. And yes, your standard homeowners deductible still applies to these losses, which often means minor car break ins are not worth claiming.

ACV vs RCV on Stolen Contents

Even if you prove you owned the item and it does not fall under a restrictive sub limit, you still have to navigate depreciation. How your policy values stolen property determines the size of the check you will receive.

If your policy is Actual Cash Value (ACV), the insurer will pay you what the item was worth on the day it was stolen, not what it costs to buy a new one today. Electronics, clothing, and furniture depreciate rapidly. I recently reviewed a claim where a homeowner was shocked to receive only $300 for a stolen custom PC they built three years ago for $1,500. The adjuster calculates this by assigning a lifespan to the item and deducting value for every year you owned it. The math they use generally follows this structure:

[Current Retail Price of New Item] minus [Age and Condition Depreciation] = [Your ACV Payout]

If you have Replacement Cost Value (RCV) coverage, you are entitled to the cost of buying a brand new equivalent item. However, insurers typically do not just hand you the full replacement cash upfront. They will pay you the ACV amount first. To get the remaining money, known as recoverable depreciation, you have to actually go buy the replacement item and submit the new receipt to the adjuster.

The Best Claim Strategy is Prevention

While this guide focuses on the claim process, I always tell homeowners that the best time to prepare for a theft claim is before it happens. Taking 15 minutes this weekend to walk through your house recording a video on your phone is the ultimate safety net.

Open your drawers, narrate the brand names of your electronics, and film the serial numbers on the back of your TVs and laptops. Email that video to yourself or save it to a cloud drive. If you ever face a break in, that single video file is often enough to bypass the hardest proof of ownership disputes entirely.

Immediate Action Checklist After a Theft

The actions you take in the days following a break in dictate how smooth the rest of your claim will be. To avoid giving the adjuster any reason to investigate your motives, follow this timeline-based checklist.

- ✅ First 24 Hours: Call the police. Do not touch the point of entry or disturbed areas until they arrive. Take wide angle photos of the scene, such as broken windows or ransacked drawers. Make a rough list of missing items to give to the police on the spot.

- ✅ Days 1 to 3: Call your insurance company to open the claim and provide the police incident number. Request the specific property inventory form they require (usually called a Sworn Statement in Proof of Loss).

- ✅ Days 3 to 7: Build your documentation file. Pull bank statements and find old photos.

When you submit your official inventory to the adjuster, do not just send a chaotic email. Create a “Loss Inventory Spreadsheet” with dedicated columns for: Item Description, Brand/Model, Estimated Age, Purchase Price, Current Replacement Cost, and an index number linking to your attached proof (receipts or photos). A well organized file commands respect and speeds up the review.

The SIU Investigation and Early Warning Signs

Because theft claims often lack physical evidence beyond a broken window, they are frequently routed to a Special Investigative Unit (SIU). The SIU’s job is to screen for fraud. In my experience, homeowners are often caught off guard when a standard claim suddenly feels like an interrogation. You need to know the early signs that your claim is being escalated, rather than just waiting for a lowball offer or denial letter.

The first major red flag is if the adjuster begins requesting your cell phone records, credit reports, or recent tax returns. This is a standard SIU tactic for high value claims to check if you are experiencing financial distress. Another warning sign is if you are asked to submit to an Examination Under Oath (EUO), which is a formal, recorded questioning session.

Additionally, pay attention to how items are categorized. A common tactic to lower settlements is classifying a high end camera or expensive laptop as “business property” rather than personal property, which triggers a much lower, separate policy limit.

If your insurer sends a Reservation of Rights letter shortly after you submit your inventory, or if the investigation feels like it has shifted from verifying a loss to investigating you personally, it is time to get outside eyes on your file. In these situations, getting a free review from a licensed public adjuster can help you understand your rights, format your documentation correctly, and level the playing field before the insurer makes a final decision.

Securing Your Settlement Through Discipline

A homeowners insurance theft claim is less about the damage and more about your endurance. It is deeply frustrating to feel like you have to prove your honesty to your own insurance company right after suffering a violation of your safe space. The process can feel cold and corporate when you are dealing with a personal loss.

However, understanding that the adjuster is operating under strict verification guidelines changes the dynamic. If you treat the claim process like a project focused entirely on organization, tracking down alternative receipts, and neatly presenting your loss spreadsheet, you remove the easy friction points. Stay calm, keep all communications in writing, and protect your settlement by playing by their documentation rules.

❓ FAQ

🚔 Will my claim be denied if I don’t call the police right away?

A delay doesn’t guarantee an automatic denial, but it raises a massive red flag for the adjuster. Insurance policies require prompt reporting to authorities so the event can be officially recorded while evidence is fresh.

🧾 Can I use my credit card statement instead of a store receipt?

Yes. Adjusters regularly accept credit card or bank statements as alternative proof of ownership, especially if the transaction amount matches the known retail price of the item you are claiming.

💻 Why did my $3,000 laptop only get a $1,000 settlement offer?

If you have an Actual Cash Value (ACV) policy, the insurer deducted depreciation for the laptop’s age. Alternatively, it might have been incorrectly categorized under a restrictive sub limit, such as business property.

💍 Does my home insurance cover my stolen engagement ring?

It does, but payouts are strictly capped. Unless you purchased a scheduled personal property endorsement (a floater) specifically for the ring, your standard policy will likely cap the payout at around $1,500.

🚗 Is my laptop covered if it was stolen out of my car at the gym?

Yes, personal items stolen from your vehicle fall under the off-premises coverage of your homeowners or renters policy. However, the payout is usually capped at 10% of your total property limit, and your standard deductible still applies.

📸 I have no receipts. Are photos of my living room enough?

Clear photographs showing the stolen items inside your home are excellent secondary evidence. While receipts are better, an adjuster can use high quality photos to verify that you owned the item and determine its general condition.

⏳ How quickly will I get paid for a theft claim?

If your documentation is perfect, a straightforward claim can settle in a few weeks. However, if you lack receipts or claim high value items, the file may be sent to an investigative unit (SIU), which can delay payment for months.

🔍 What does it mean if my claim is sent to SIU?

SIU stands for Special Investigative Unit. Theft claims are frequently sent here to screen for fraud. It means the insurer is looking closer at your file, and they may request additional financial documents or recorded statements.

📝 What is a Sworn Statement in Proof of Loss?

This is a formal, notarized document your insurer may require you to sign. It lists the exact items stolen and their values, legally binding you to the accuracy of your claim under penalty of perjury.

🚫 Will insurance cover the theft if I left my front door unlocked?

Generally, yes. Standard homeowners insurance covers simple negligence, such as forgetting to lock a door or close a window. However, the adjuster will document the lack of forced entry, which might trigger a slightly closer review of the claim.

Damage type affects coverage, documentation, and payout. These connect the dots.

- How the settlement process works after damage is reported

- Which parts of your policy apply when damage is involved

- How your damage type affects what the insurer is required to pay

- Whether the damage you have is actually worth filing for

- What happens when the claim you filed gets rejected

- How independent representation changes what gets documented

- When a disputed claim moves into legal territory

Each damage type has its own patterns. See what adjusters commonly miss.

- Whether your damage assessment left money on the table

- What the inspector who came to your home was actually there to do

- The parts of water damage that standard inspections routinely miss

- What fire and smoke assessments leave out of the scope

- Why the insurer's roof estimate is almost always lower than the roofer's

- When a denial crosses into bad faith and needs legal leverage

- The four options after a denial, including one most homeowners skip

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.