- The roof is the most frequently claimed component in home insurance, but it also has the highest rate of underpayment and wear-and-tear denials.

- Initial settlement offers rarely cover the full scope of damage, often missing crucial line items like flashings, decking, gutters, and drip edges.

- If you have RCV coverage, your first check is only a partial payment based on depreciated value. You must file a supplement to recover the rest.

The Initial Offer Is Rarely the Full Picture

When a severe storm passes through and damages your roof, you expect your homeowners insurance to step in, assess the damage, and write a check that covers the repair. However, when you finally receive that first settlement document, the numbers often do not align with the estimates your local roofing contractors are giving you. I have sat down with countless homeowners who feel completely defeated by a surprisingly low initial offer or a confusing denial letter.

The roof is the most claimed single component in homeowners insurance. Because of this high volume, it is also the component scrutinized the most heavily by insurance carriers. The reality is that the first offer you receive on a homeowners insurance roof claim is almost never the full picture. It is a starting point based on a visual inspection by an adjuster who may or may not have extensive roofing experience. Knowing exactly what they are looking for is the only way to ensure your claim scope reflects the physical reality of your property.

How Roof Damage Claims Are Actually Assessed

The insurance claim process for a damaged roof begins with the adjuster’s inspection. It is important to set the right expectations for this visit. Insurance adjusters are trained professionals, but they are generalists. They are not licensed roofing contractors. Their job is to document what they can visually identify as storm-related damage and plug those findings into estimating software, usually a program called Xactimate.

When an adjuster gets on your roof, they are generally looking for specific markers depending on the peril claimed. For wind damage, they look for creased, lifted, or missing shingles. For hail, they look for impact bruising, granule displacement, and dents on soft metals. They will typically mark a “test square” (a 10-foot by 10-foot area) on different slopes of the roof to count the number of impacts or damaged shingles. This count heavily influences whether they approve a full replacement or just a partial repair.

In my experience reviewing hundreds of roof claim files, one of the biggest disconnects happens during the physical inspection. A thorough roof inspection takes time, often an hour or more depending on the size and steepness. When I see a file where the adjuster was on the property for less than 20 minutes, I almost guarantee the resulting scope will be missing critical line items.

The scope produced by the adjuster dictates what gets paid. If an item is not explicitly listed in the Xactimate estimate, it is not funded in your settlement. This is why relying solely on the adjuster’s quick visual inspection can leave you thousands of dollars short when the actual roofing work begins.

| Adjuster’s Focus | Roofer’s Focus |

|---|---|

| Verifying storm damage vs. normal aging | Ensuring the roof is watertight and up to local code |

| Counting impacts in a specific test square | Assessing the integrity of the entire roofing system |

| Writing an estimate based on visible surface issues | Identifying hidden damage requiring tear-off to fix |

| Applying depreciation to all materials | Ordering materials at current market costs |

Before the adjuster arrives, prepare your documentation baseline:

- 📷 Clear photographs of the roof and any interior leaks taken immediately after the event.

- 🌧️ Weather records or local news clippings from the specific storm date.

- 📋 A detailed, line-item inspection report from your own roofing contractor.

- ⏱️ A simple log noting the exact time the adjuster arrived and departed.

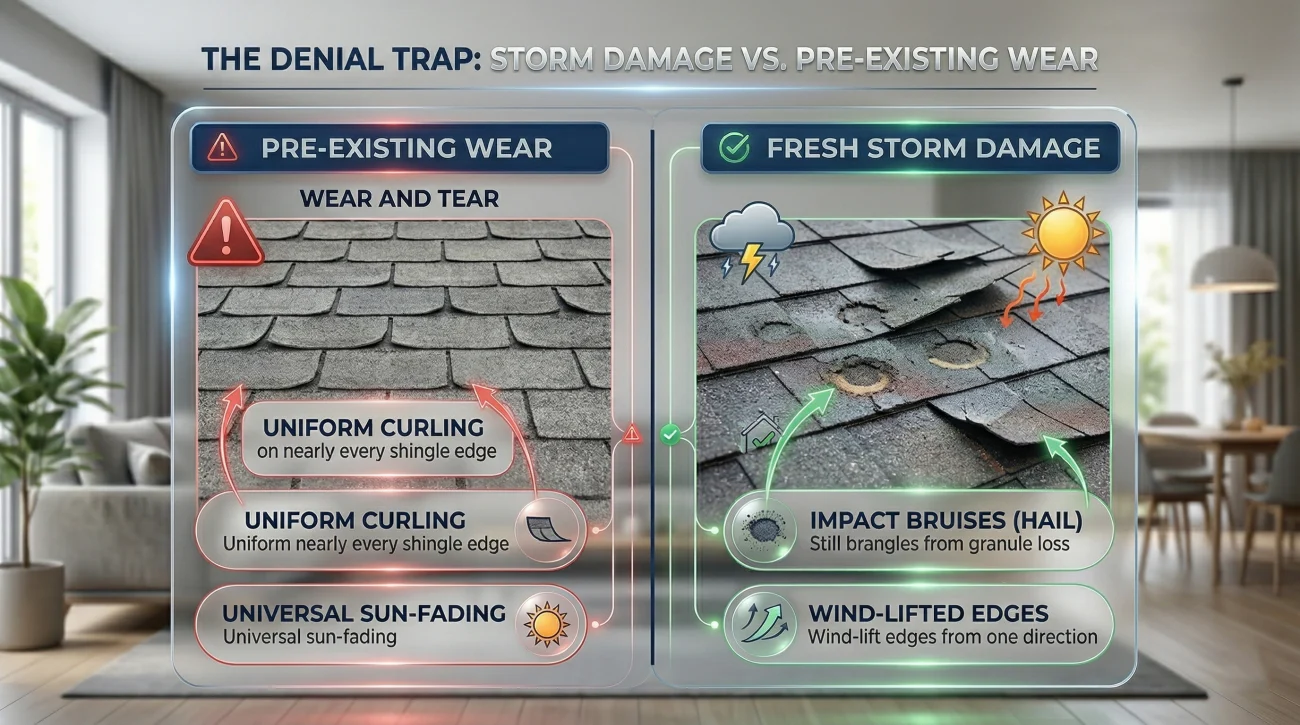

The Pre-Existing Damage Denial Trap

The most common hurdle in a roof claim is not a complete denial of the storm, but rather a denial based on the condition of the roof prior to the storm. Insurers frequently argue that the damage showing on your roof, such as granule loss, curling shingles, or minor cracking, existed long before the insured event occurred. They categorize this as wear and tear, age, or poor maintenance, which are universally excluded under standard homeowners policies.

This creates an incredibly frustrating situation. Normal aging and fresh storm damage can, and often do, coexist on the exact same roof. An older roof is actually more susceptible to wind and hail damage. The question is not whether the roof is old; the question is whether the recent storm caused damage that would not have occurred otherwise.

The distinction often comes down to how the damage pattern is documented. Adjusters use directional pattern assessments to determine cause. For example, damage that appears only on the north and west slopes of a roof is consistent with a storm moving in from that direction. Damage that appears uniformly across all slopes is more often attributed to age and sun exposure. For a deeper explanation of how these patterns are evaluated, you can review our guide on the hail damage insurance claim process.

Arguing with the adjuster that your roof never leaked before the storm, assuming that proves the storm caused all the visible damage.

Having a professional document the specific, directional impact marks and lifted shingles that correlate directly with the recorded wind speeds and hail sizes of that specific storm date.

The Most Common Roof Scope Gaps

Even when a claim is approved and a replacement is authorized, roof scopes routinely miss vital line items. This is what we call a “scope gap.” It is the difference between what the insurance company agrees to pay for and the actual physical work required to restore your property. Scope gaps are the primary reason homeowners feel they are being shortchanged.

When you review your settlement estimate, the dollar amount at the bottom is less important than the list of items above it. If the line items are missing, the final payout will never be sufficient. It is helpful to understand the home insurance claims by damage type to see how these estimating gaps happen across different parts of the home, but on a roof, the missing items follow a very predictable pattern.

Here are the components most frequently omitted from an initial roof claim scope:

- Valleys and Flashings: Adjusters often include the shingles but forget the metal flashing required in the roof valleys, around chimneys, and at wall intersections. These metals are almost always damaged when the surrounding shingles are torn off for replacement.

- Gutters and Downspouts: A storm severe enough to destroy an asphalt roof will almost certainly dent or pull away gutters. However, because they are a separate system attached to the fascia, they are frequently left off the roof estimate entirely.

- Roof Decking: Hidden underneath the shingles, damaged or rotten decking cannot be confirmed until tear-off begins. Initial scopes rarely include decking line items, which means major surprises once the old roof comes off. In colder climates, code-required ice-and-water shield is a separate line item that adjusters frequently omit entirely.

- Drip Edge and Starter Strips: These are critical components for a code-compliant roof installation. They seal the edges of the roof against wind-driven rain. Adjusters sometimes leave them off, assuming the old ones can be reused (they rarely can be).

- Fascia and Soffit: Wind events that lift shingles at the eaves often damage the fascia board and the vented soffit beneath it. This secondary damage is routinely overlooked during a quick ground-to-ladder inspection.

⚠️ Warning: Never agree to a final settlement or sign a release of claims before a contractor has confirmed that every single required component is listed in the adjuster’s Xactimate scope.

Partial Repair vs. Full Replacement Disputes

Another major battleground in roof claims is the dispute between a partial repair and a full replacement. Insurers prefer to pay for localized repairs, replacing only the damaged shingles on one slope. Roofing contractors will often argue that a full replacement is necessary. Both sides have financial motivations, but the physical reality of the roof usually dictates the correct answer.

The core issue here is “repairability.” If your roof is ten years old, the existing shingles have become brittle from UV exposure. If a contractor attempts to lift an old, brittle shingle to slide a new one underneath for a repair, the old shingle will crack and break. This creates a cascading effect where repairing one square foot damages the next. When a roof cannot be repaired without causing further damage, a full replacement is warranted.

The Matching Dispute: When Partial Repairs Look Like a Patchwork

One of the most endemic problems in roof claims revolves around matching. When an insurer approves a partial repair, they assume the new materials will seamlessly blend with the old. In reality, a roof that is even a few years old has faded from sun exposure. Placing brand-new shingles next to weathered ones creates a glaring, patchwork appearance.

Furthermore, shingle manufacturers frequently discontinue specific colors or product lines. If your exact shingle is no longer manufactured, the insurer cannot simply supply a substitute that is merely close enough. Most standard policies include language regarding repairing the property to a uniform appearance or providing like kind and quality materials. Depending on your specific policy language and the matching standards your insurer applies, the inability to source an exact match can trigger a full roof replacement, even if only a portion of the roof sustained direct physical damage.

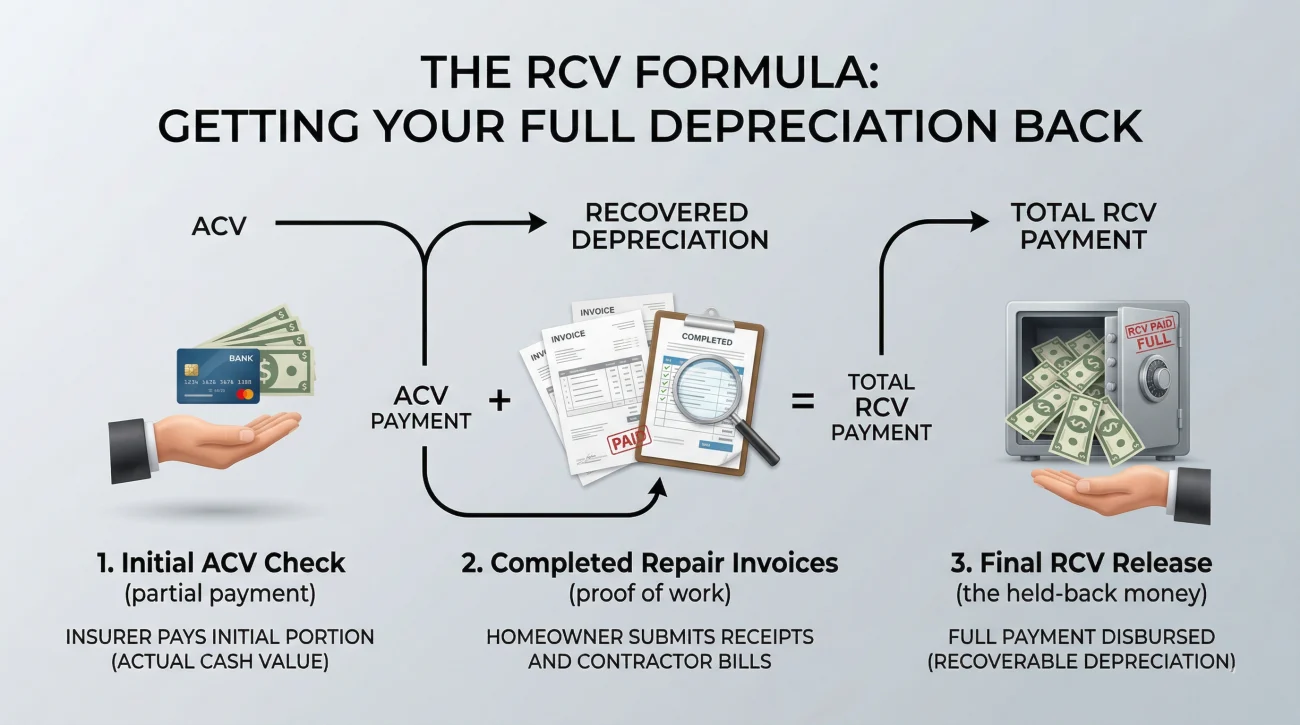

The RCV Supplement Mechanic

One of the most confusing days for a homeowner is the day the first insurance check arrives. Often, the check is for half or less of the total approved estimate. Homeowners panic, assuming the insurance company has drastically underpaid the claim. In most cases involving a Replacement Cost Value (RCV) policy, this is actually the standard mechanic of the payout process.

If you have RCV coverage, the payment happens in two stages. The initial payment you receive is the Actual Cash Value (ACV). This is the cost to replace the roof minus depreciation based on its age and condition. The insurance company holds back the depreciated amount, known as recoverable depreciation. To get the rest of your money, you must actually complete the repairs and submit the final invoices.

Many homeowners do not know this second step exists, or they get confused by the paperwork and leave thousands of dollars sitting on the table. The process requires submitting a formal supplement.

[Initial ACV Payment] + [Submit Contractor Invoices] = [Release of Recoverable Depreciation]

Furthermore, the supplement process is how you handle hidden damage. When your contractor tears off the old roof and finds rotten decking that was not visible during the adjuster’s inspection, they must stop, document it with photos, and submit a supplement request to the insurer before covering it up. Keep the supplement request and all attached photos in writing — a paper trail here is essential if the insurer delays or disputes the added scope. For a full breakdown of how depreciation is calculated and recovered, review the mechanics of ACV vs RCV home insurance policies.

Hello [Adjuster Name],

During the tear-off phase of the roof replacement, my contractor uncovered damaged decking that was not visible during the initial inspection. We have paused work in this area to allow for your review.

Attached are the photographs of the newly discovered damage, along with the contractor’s supplemental estimate for the required decking replacement and associated labor. Please review this supplement and provide written authorization so we may proceed with the repairs.

Thank you,

[Your Name]

Signs Your Roof Claim Scope Is Incomplete

You do not need to be a construction expert to spot the red flags that indicate your claim is being undervalued. If you are sitting at your kitchen table right now looking at a confusing estimate or a denial letter, look closely at the details.

Here are the clear signs you are facing an incomplete scope:

- The Wear and Tear Rejection: You are holding a denial letter citing pre-existing damage, yet you have clear weather records showing a severe storm hit your exact address just days before the leak started.

- The Partial Repair Conflict: Your estimate lists replacing only 20 shingles, but your roofer has physically demonstrated that the surrounding older shingles are too brittle to lift without snapping.

- Missing Adjacent Systems: You know your gutters were dented by the exact same hail, but scanning the Xactimate line items, you see zero mention of the gutter system or fascia.

- Unexplained Discrepancies: Your ACV check does not even cover the base cost of roofing materials, and the adjuster provided no written explanation of the pricing database used to calculate the payout.

- The Silent RCV Trap: Your adjuster verbally told you this check is the final payout, completely omitting any explanation of the RCV supplement process to recover your depreciation.

Roof claim underpayment is usually a scope gap. It is a matter of missing line items, incorrect pricing databases, or a pre-existing damage characterization that simply does not match the actual cause of loss. Identifying these gaps requires a trained eye that understands both roofing construction and insurance policy language.

Whether that gap exists in your claim is what a professional reinspection identifies. If you are looking at a frustrating settlement offer, having a roof-specific public adjuster review your current estimate is often the most effective way to uncover exactly what the carrier missed.

Final Steps Before You Close the File

Dealing with a roof claim comes down to who has the better documentation. If the scope of work provided by the adjuster does not match the physical reality of the damage on your property, you have options. Most policies contain a formal Appraisal clause, a dispute resolution mechanism you can invoke to challenge the scope and pricing without immediately resorting to legal action. You do not have to accept the final offer as absolute.

Before you file away your claim documents, gather your photos, contractor estimates, and weather data. A methodical review of these items against the insurance carrier’s estimate is your best defense against an underpaid roof claim.

❓ FAQ

🌩️ Does homeowners insurance cover roof replacement?

Yes, standard homeowners policies cover roof replacement if the damage was caused by a covered sudden and accidental peril, such as a windstorm, hail, or a fallen tree. They do not cover replacement if the roof simply aged out or failed due to lack of maintenance.

⏱️ How long do I have to file a roof claim?

The filing window varies by policy and state, but it is commonly one to two years from the date of the storm event. It is always recommended to file as soon as you suspect damage to prevent the insurance company from arguing that the delay worsened the damage.

📉 Why is my initial roof claim check so low?

If you have a Replacement Cost Value (RCV) policy, the first check is for the Actual Cash Value (ACV), meaning depreciation has been subtracted. You must complete the repairs and submit invoices to recover the remaining depreciated amount.

🛑 What if insurance denies my roof claim for wear and tear?

You can challenge this denial by requesting a reinspection and providing documentation from an independent contractor or public adjuster showing specific, directional storm impact marks that prove the recent weather event caused the damage.

📸 How should I document roof damage for the adjuster?

Take clear photos of all visible damage from the ground, document interior leaks immediately, save any shingles that blew into your yard, and keep a log of the exact date and time the severe weather occurred.

🌧️ Will insurance pay for interior water damage from a roof leak?

Typically, yes. If a covered storm damages the roof and allows rain to enter, the resulting interior water damage to ceilings, walls, and floors is usually covered under the same claim event.

🔨 Can I use my own roofer for an insurance claim?

Yes, you have the right to choose your own roofing contractor. You are not required to use the insurance company’s preferred vendor network, though your contractor must work within the approved scope and pricing guidelines of the policy.

💸 What is recoverable depreciation on a roof claim?

Recoverable depreciation is the amount the insurance company holds back from the initial ACV payment. It represents the loss in value due to age. Once you prove the roof has been replaced, they release this held-back money to you.

🤝 Do I need to meet the adjuster on my roof?

You do not need to physically climb the roof with them, but it is highly recommended to have your chosen roofing contractor or public adjuster present during the inspection to point out hidden damage and advocate for a complete scope.

📝 Can I reopen a closed roof claim?

Yes, in many cases you can reopen a claim by filing a supplement if new, previously hidden damage is discovered during the repair process, provided you are still within the time limits set by your policy.

Damage type affects coverage, documentation, and payout. These connect the dots.

- How the settlement process works after damage is reported

- Which parts of your policy apply when damage is involved

- How your damage type affects what the insurer is required to pay

- Whether the damage you have is actually worth filing for

- What happens when the claim you filed gets rejected

- How independent representation changes what gets documented

- When a disputed claim moves into legal territory

Each damage type has its own patterns. See what adjusters commonly miss.

- Whether your damage assessment left money on the table

- What the inspector who came to your home was actually there to do

- The parts of water damage that standard inspections routinely miss

- What fire and smoke assessments leave out of the scope

- Why the insurer's roof estimate is almost always lower than the roofer's

- When a denial crosses into bad faith and needs legal leverage

- The four options after a denial, including one most homeowners skip

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.