- Standard property coverage pays to repair what was damaged, but it does not pay for the mandatory building code upgrades required to legally rebuild your home.

- Ordinance or law coverage is a specific policy provision that covers three hidden costs: demolishing undamaged parts of the home, bringing the structure up to current code, and the loss of value of undamaged sections.

- This coverage is rarely applied automatically. You must actively claim it by submitting written proof of the local code requirement alongside a contractor’s itemised estimate for the upgrade.

The Shock of the Code Upgrade Gap

When a severe storm, fire, or sudden plumbing failure damages your home, the initial relief of an approved insurance claim can quickly turn into financial panic. The insurance adjuster cuts a check based on replacing exactly what was there before the loss. Then, your general contractor pulls the permits and delivers bad news. The city will not let you rebuild the house exactly as it was. The building codes have changed since your home was constructed, and complying with the new laws will cost thousands of dollars out of pocket.

This gap between what your standard policy pays and what the local building department actually demands is one of the most stressful surprises in property recovery. Most homeowners assume that if their home is destroyed, their insurance will fully fund a legally compliant reconstruction. Unfortunately, standard property coverage strictly limits payouts to a like for like replacement.

In my years of reviewing property claims, the code upgrade gap is consistently the most overlooked component of a settlement. Adjusters are trained to write a scope for the damaged materials they see in front of them. They are not code enforcement officers, and they rarely volunteer to add code upgrade costs to a settlement unless the homeowner forces the issue.

As a property claims writer, I have watched homeowners drain their savings to cover new electrical panels, mandatory roof decking upgrades, and hurricane straps that their insurer refused to fund. The safety net for this exact scenario is called ordinance or law coverage. In this guide, I will explain what this hidden coverage actually does, how to find out if you have it, and the exact steps required to force your insurer to pay for mandatory upgrades.

Understanding How Ordinance or Law Coverage Works

Ordinance or law coverage, sometimes listed on declarations pages as building ordinance coverage, is not designed to pay for the primary fire or water damage. Instead, it acts as a supplemental fund that activates only when a local municipal building code forces you to alter how you rebuild.

To use this coverage effectively, look for how it applies across three specific prongs of protection. A standard property settlement will never touch these three areas unless this specific coverage is triggered.

First, it covers the cost to demolish the undamaged portions of your structure. This is often the most confusing part for homeowners. If a fire destroys half of your house, but the city code states that any home sustaining more than 50 percent damage must be entirely rebuilt to modern standards, you now have to tear down the perfectly good half of your house. Standard insurance will not pay to demolish undamaged property. Ordinance or law coverage steps in to fund that demolition.

Second, it covers the increased cost of construction. This is the most frequently used prong. If your 1980s home had basic roof decking, but the current 2024 local code requires specialized ice and water shields or thicker plywood, the materials will cost significantly more. This coverage pays the difference between the 1980s standard and the modern requirement.

Third, it covers the loss of value of the undamaged portion. When local ordinances require the demolition of structurally sound sections of your property to achieve full compliance, you lose the equity held in those materials. This provision compensates you for that forced loss of value.

| Repair Scenario | Standard Base Coverage Pays For | Ordinance or Law Coverage Pays For |

|---|---|---|

| Roof Replacement | Standard asphalt shingles and felt paper identical to what was damaged. | Mandatory drip edges, specialized underlayment, and updated ventilation required by new codes. |

| Electrical Fire | Replacing the burned wiring in the affected room only. | Upgrading the entire main electrical panel to handle modern arc fault breakers required by the city. |

| Major Structural Damage | Rebuilding the damaged load bearing walls. | Tearing down undamaged walls to install newly mandated hurricane straps or seismic retrofitting. |

Finding the Hidden Clause in Your Policy

Because it is so critical for older homes, some states require insurers to include a base level of ordinance or law coverage in all standard policies. In other regions, it is strictly an optional endorsement that you or your agent must manually add to the policy.

You will not find out if you have this coverage by looking at the settlement check. You must look directly at your policy declarations page. It is typically expressed as a percentage of your total dwelling limit (Coverage A). The most common increments are 10 percent, 25 percent, or 50 percent.

If your home is insured for $400,000 and you have a 10 percent ordinance or law endorsement, you have a maximum of $40,000 available to spend on mandatory building code upgrades. If you own a historic home or a house built before major modern code revisions, a 10 percent limit is often severely inadequate, and a 25 percent or higher limit is highly recommended.

If your declarations page is confusing or only provides a summary, contact your insurance agent directly. Request a complete copy of your policy including all endorsements, and specifically ask them to confirm your ordinance or law percentage.

📌 Note: If you review your declarations page and do not see the words “Ordinance or Law” or “Building Ordinance” listed under your coverages or endorsements, you likely do not have it. In this scenario, any code upgrades required by the city will be entirely out of pocket.

When This Coverage Comes Up the Most

While building codes apply to every inch of a house, certain types of claims trigger ordinance or law disputes almost automatically. Knowing when to look for these gaps can save you months of frustrating negotiations.

Roof claims are the most notorious trigger. Roofing codes change constantly to address wind resistance, energy efficiency, and water mitigation. During a standard roof damage process, an adjuster will often write an estimate that excludes new decking requirements or mandatory ventilation upgrades. The contractor will inevitably halt the job when the permit office rejects the outdated scope. A mandatory roof decking upgrade on an average sized home can easily add $4,000 to $7,000 to the repair bill, depending on your local market.

Fire claims are equally complex. When addressing structural fire damage claims, the building department often requires the entire home’s electrical and plumbing systems to be brought up to modern safety standards, even if the fire was contained to a single room. Upgrading an outdated electrical panel to meet new safety standards typically runs $3,000 to $5,000 out of pocket in many cases, which can consume a massive portion of an upgrade budget.

Water damage claims also present hidden code issues. If a burst pipe requires tearing out a bathroom wall, the city may require the newly exposed plumbing lines to be updated to modern materials. Rerouting plumbing to meet modern code or upgrading wall insulation to new energy efficiency standards can quickly add $2,000 to $4,000 to a bathroom restoration, though costs vary widely by region.

Identifying these mandatory upgrades is only the first step. To actually get them funded, you have to present them to the insurance company in a very specific format.

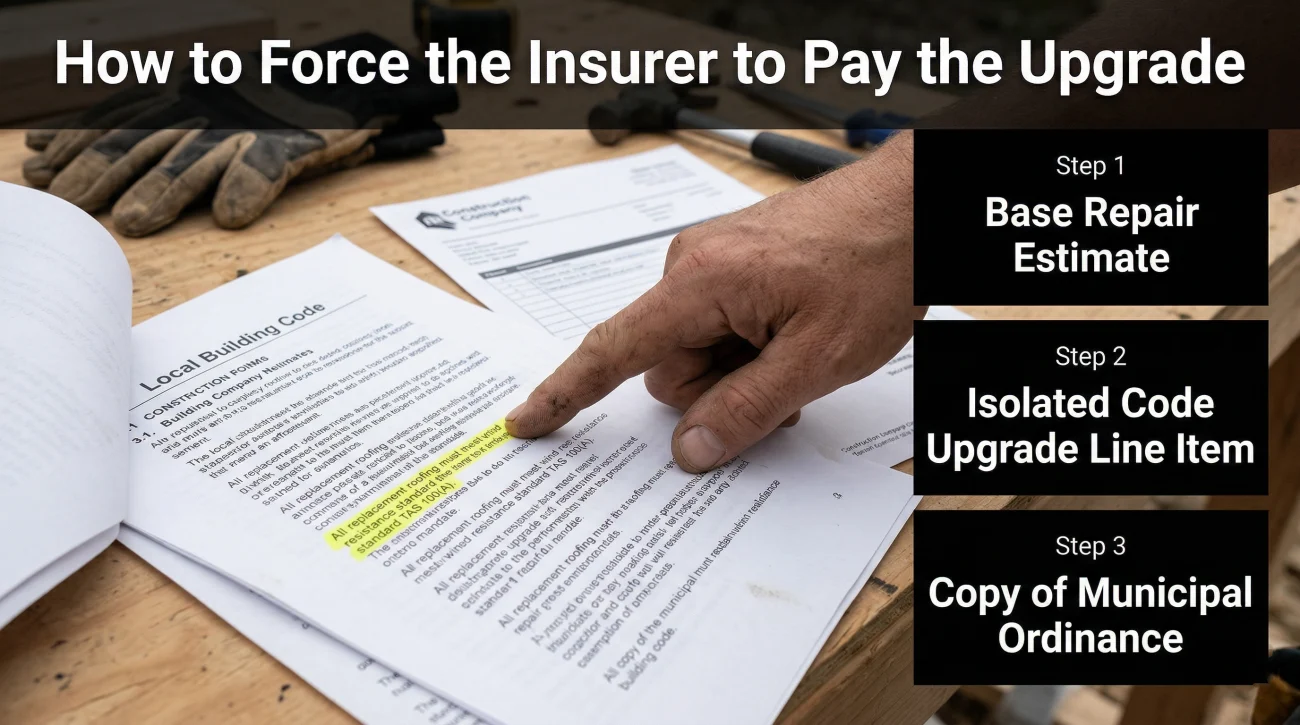

How to Force the Insurer to Pay the Upgrade

Insurance adjusters operate on a very strict rule of documentation. They will never approve a code upgrade payment just because your contractor says it is a good idea. To tap into your ordinance or law coverage, you must prove that the upgrade is a legal mandate, not a suggestion.

The documentation process requires three specific pieces of evidence. First, you need the written estimate from your contractor. Second, your contractor must separate the code upgrade costs into a completely different line item from the base repair costs. Third, and most importantly, you must provide a copy of the specific municipal code, statute, or written letter from the local building inspector proving that the upgrade is strictly required to secure the permit.

A valid ordinance claim relies on three combined documents: Your contractor’s base estimate + an isolated code upgrade line item + a copy of the local municipal ordinance.

When you have these three elements, you do not just mention it over the phone. You submit a formal request for a supplemental payment based specifically on your ordinance or law endorsement.

Subject: Invocation of Ordinance or Law Coverage – Claim #12345

Hello [Adjuster Name],

During the permitting process for the approved repairs, our contractor was informed by the municipal building department that the current electrical code requires an upgraded 200-amp panel to pass inspection.

Attached, please find three documents:

1. The revised contractor estimate with the panel upgrade isolated as a separate line item.

2. A copy of the municipal code section mandating this specific upgrade for reconstruction.

3. The written permit rejection notice from the city inspector.

Please review this documentation and apply these required costs under the Ordinance or Law provision of my policy. I look forward to your updated settlement.

Common Adjuster Pushbacks and How to Counter Them

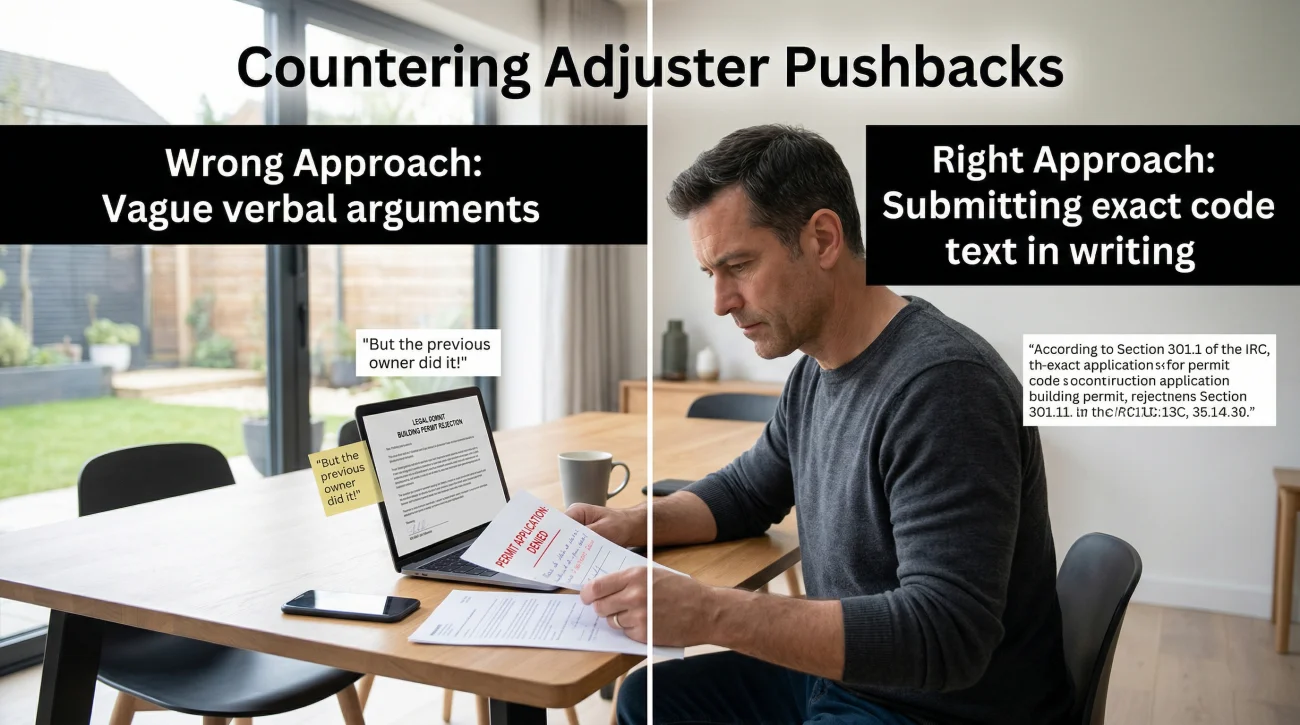

Even with perfect documentation, you may face resistance. Insurers are highly protective of ordinance or law funds. One of the most common pushbacks is the adjuster claiming that the city is only “recommending” the upgrade, not requiring it. This happens frequently with energy efficiency upgrades. Your counter strategy is simple: demand that the local building inspector put in writing that the permit will be denied without the upgrade. A denial of permit ends the debate.

Another common tactic is the adjuster arguing that the code upgrade was triggered by a pre-existing condition, not the covered loss. For example, they might say your roof decking was already rotting, which is why the city wants it replaced. You must firmly redirect the conversation back to the loss event. If the covered storm had not occurred, the roof would not be open, and the code upgrade would not have been triggered. The covered peril is the catalyst.

Letting your contractor argue vaguely with the adjuster over the phone about what the city “usually wants” done on repair jobs.

Submitting the exact municipal code text via email and forcing the adjuster to put their refusal to pay in writing.

Signs Your Settlement Is Missing Code Upgrade Costs

Because ordinance or law coverage is rarely discussed upfront, many homeowners accept inadequate settlements without realizing a massive portion of their repair budget is missing. You are in the danger zone if you are experiencing any of these specific patterns during your claim.

The clearest red flag is when your general contractor tells you they cannot pull a permit based on the insurance adjuster’s current estimate. If the contractor says the scope is outdated, you immediately have a code upgrade issue. Another major warning sign is receiving a settlement that strictly covers the replacement of old materials in an older home. If your house was built forty years ago and the adjuster’s scope reflects a simple like for like replacement, it is almost mathematically impossible that no building codes have changed in that time.

Additionally, listen carefully to the language the adjuster uses. If they repeatedly state, “We only owe you for what was there before the storm,” they are strictly applying base coverage limits, knowing that supplemental code upgrades must be formally requested by the policyholder.

These patterns indicate that a significant amount of money is being left on the table. If you are dealing with an older home and a complex settlement, it is highly advisable to get a free review from a licensed public adjuster. A professional can audit your policy to confirm your endorsement limits and cross reference the adjuster’s estimate against current local building requirements.

Securing Your Full Entitlement

Securing code upgrade costs requires strict administrative discipline. Relying entirely on verbal negotiations with an adjuster rarely produces results when dealing with municipal requirements. It is incredibly frustrating to feel penalized for owning an older home or to be caught in a tug of war between an insurance carrier and a city building inspector.

However, understanding what your standard policy covers versus what your endorsements provide is the key to protecting your finances. By securing the exact code documentation, isolating the upgrade costs, and formally invoking the coverage in writing, you remove the adjuster’s ability to dismiss the expense. If the process becomes too overwhelming or the insurer refuses to honor the municipal code requirements, bringing in a licensed public adjuster to review your structural scope can level the playing field and ensure your home is rebuilt safely, legally, and fully funded.

❓ FAQ

📜 What exactly does ordinance or law coverage pay for?

It pays for the increased costs associated with enforcing local building codes during a repair. This includes upgrading materials to meet new laws, demolishing undamaged parts of the home if required by code, and covering the lost value of those demolished sections.

🔍 Is code upgrade coverage included in a standard policy?

Not always. While some states require a minimum percentage to be included, in many cases, it is an optional endorsement that must be specifically added to your homeowners insurance policy.

💰 How much ordinance or law coverage do I need?

Coverage is usually sold as a percentage of your total dwelling limit, typically 10%, 25%, or 50%. Older homes require much higher percentages because they are further out of compliance with modern building codes.

🏚️ Will insurance pay to demolish undamaged parts of my house?

Standard coverage will not. However, if a local ordinance requires the undamaged portion to be torn down (often due to the 50 percent substantial damage rule), the demolition prong of your ordinance or law coverage will fund it.

📝 How do I prove a code upgrade is required?

You must provide the insurance adjuster with a copy of the specific municipal building code or a written letter from the local building inspector stating that the permit will be denied without the specific upgrade.

⚡ Does this coverage apply to electrical panel upgrades after a fire?

Yes. If your home had an older electrical system and a fire repair triggers a municipal requirement to bring the entire home’s electrical panel up to modern safety standards, this coverage applies.

🚫 Can the adjuster deny a code upgrade if the city only “recommends” it?

Yes. Ordinance or law coverage only pays for mandatory, legally enforced upgrades. If a building inspector merely suggests an upgrade for better energy efficiency, the insurer is not obligated to pay for it.

🏠 Will this coverage pay for new roof decking?

Yes, if the local building code has changed to require thicker plywood, specialized underlayment, or specific nailing patterns that were not present on your original roof before the storm damage occurred.

⏳ When should I tell my adjuster about a code upgrade?

You should notify the adjuster as soon as your contractor or the city permit office identifies a mandatory code change. Provide the code documentation and the contractor’s itemized estimate before the work begins.

🤝 Can a public adjuster help with ordinance or law claims?

Absolutely. Public adjusters are highly experienced in identifying missed code upgrades, gathering the necessary municipal documentation, and forcing the insurance company to honor the endorsement limits in your policy.

Damage type affects coverage, documentation, and payout. These connect the dots.

- How the settlement process works after damage is reported

- Which parts of your policy apply when damage is involved

- How your damage type affects what the insurer is required to pay

- Whether the damage you have is actually worth filing for

- What happens when the claim you filed gets rejected

- How independent representation changes what gets documented

- When a disputed claim moves into legal territory

Each damage type has its own patterns. See what adjusters commonly miss.

- Whether your damage assessment left money on the table

- What the inspector who came to your home was actually there to do

- The parts of water damage that standard inspections routinely miss

- What fire and smoke assessments leave out of the scope

- Why the insurer's roof estimate is almost always lower than the roofer's

- When a denial crosses into bad faith and needs legal leverage

- The four options after a denial, including one most homeowners skip

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.