- Receiving a denial letter feels like the absolute end of the road, but it is usually just the insurance company’s initial negotiating position based on incomplete documentation.

- Every homeowners insurance claim denied falls into one of two distinct categories: legitimate (where coverage genuinely does not exist) or challengeable (where human error or rigid processes caused a mistake).

- Overworked field adjusters, rushed property inspections, and desk adjusters misapplying policy language are the most common reasons behind challengeable denials.

- Your next step should never be a blind, emotional argument. Your path forward depends entirely on decoding the specific reason cited in your letter.

- Even if a claim is denied and no payout is made, the incident may still appear on your property’s C.L.U.E. report and impact your future insurance rates.

The Harsh Reality of the Denial Letter

I have sat across from insurance adjusters at kitchen tables, reviewed hundreds of claim files, and read more denial letters than I can possibly count. I know exactly how it feels in your stomach when you finally open that envelope. You have suffered significant damage to your home, you paid your premiums faithfully for years, and the response you get is a dense, corporate letter telling you the company will not pay a single dime.

It feels deeply personal. It feels final. But in my experience working inside the mechanics of property claims, a denial letter is rarely the last word unless you choose to accept it as such. It is a formal statement of the insurer’s current position, based on the limited and often flawed information they gathered during their first review.

Before you pick up the phone to argue with your desk adjuster, you need to understand how the system actually operates. Insurance claim denials are not all created equal. The biggest operational mistake homeowners make is arguing that a denial is “unfair.” The insurance claims process does not care about fairness or your loyalty as a customer. It only cares about the written contract and the physical documentation in the file.

To navigate this system successfully and get what you are owed, we need to strip the emotion away. We must look at your claim file exactly the way the insurance company’s management team looks at it. We need to systematically determine if your denial is based on a rigid policy exclusion, or if it is the result of human error, an incomplete inspection, or a misinterpretation of the facts on the ground.

Field observation from my years in claims: The vast majority of homeowners read the first paragraph of a denial letter, see the bold word ‘DENIED’, and immediately panic. They gloss over the crucial middle paragraphs where the adjuster cites specific policy section numbers. That specific citation is actually the only thing that matters, because it dictates the exact counter-evidence you will need to gather next.

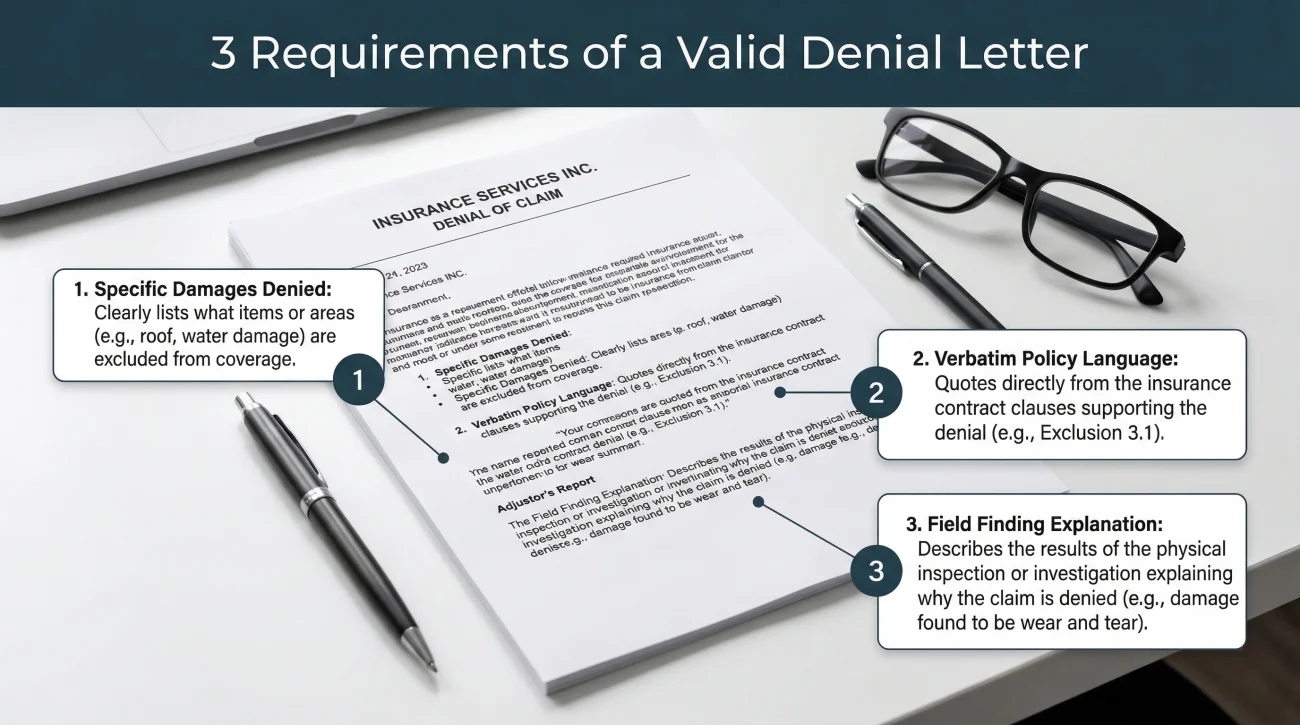

What Your Denial Letter Must Actually Contain

Before we classify your denial, we need to verify if the document you received is procedurally valid. By state regulations, an insurance carrier cannot simply send a letter that says “we are not paying this.” A formal denial letter must legally contain specific structural elements.

First, it must explicitly name the exact damages being denied. Second, and most importantly, it must quote the exact policy section and exclusion language verbatim from your contract. Finally, it should provide a brief explanation of how the adjuster’s field findings apply to that specific exclusion. If your letter lacks specific policy citations and reads like a generic template, that alone is a red flag that the investigation was improperly handled.

How the Claims Process Actually Generates Denials

To understand why your claim was denied, you have to understand who made the decision. Homeowners often assume that one highly trained expert thoroughly investigated their home and reviewed their policy. This is rarely how modern insurance operations work.

In most standard property claims, the process is split between two different people who may never actually speak to one another. First, there is the field adjuster. This is the person who shows up at your house. Especially after a major weather event, they might be an independent contractor handling eight to ten houses a day. They are rushing to meet corporate quotas, and their primary goal is to take a set of standard photos and move on.

The field adjuster does not make the final decision. They upload their photos and notes into the carrier’s software. That file is then sent to a desk adjuster, potentially three states away. They have never seen your house. They simply match the uploaded photos and notes against your policy document and approve or deny the claim.

When you understand this disconnect, you see how legitimate claims get denied by accident. A thorough investigation of a complex structural claim typically requires 30 to 45 days. If you received a flat denial within 48 hours of the adjuster’s visit, the system moved too fast to be thorough. If the field adjuster fails to take a photo of the cracked pipe behind the drywall, the desk adjuster assumes the pipe is fine. The denial is not necessarily malicious; it is a symptom of a fractured, high-volume process.

The Only Distinction That Matters: Legitimate vs. Challengeable

When I review a denied claim file, I immediately look to categorize the insurer’s decision into one of two distinct buckets: legitimate or challengeable. This mental framework is the foundation of every action that happens next.

If you try to fight a purely legitimate denial, you will waste months of your life for an outcome that will never change. Conversely, if you passively accept a challengeable denial, you are leaving the money you are contractually owed sitting in the insurance company’s bank account.

What Makes a Denial Legitimate?

A legitimate denial means your specific property damage falls cleanly into a written exclusion in your policy contract. In these scenarios, the adjuster did their job correctly, the photo documentation is accurate, and the policy language was applied appropriately to the facts of the loss.

What Makes a Denial Challengeable?

A challengeable denial occurs when coverage might actually exist, but the insurance company reached the wrong conclusion due to a flawed process. This typically stems from rushed physical inspections, missed structural evidence, or a desk adjuster misapplying the policy language to the field notes.

Diagnostic Flowchart: Categorizing Your Denial Step 1: Does your letter cite a specific, verbatim exclusion clause (e.g., "earth movement")? ➔ If NO: The letter is procedurally flawed and challengeable. ➔ If YES: Move to Step 2. Step 2: Does the adjuster's written description match the physical reality of what you actually saw happen? ➔ If YES (e.g., they cite flood, and it was indeed rising surface water): The denial is likely Legitimate. ➔ If NO (e.g., they call a suddenly burst pipe "gradual seepage"): The denial is Challengeable.

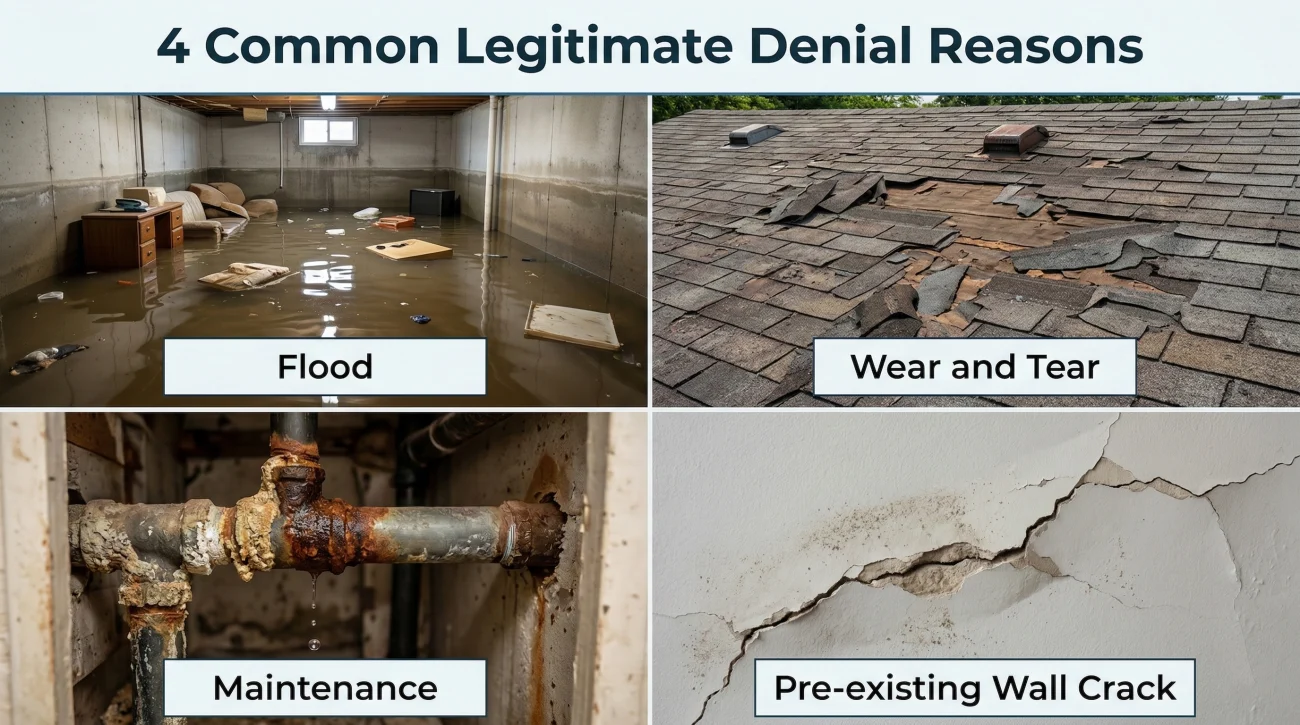

The Most Common Reasons for Legitimate Denials

If your specific situation perfectly matches one of these four categories, the denial is likely solid, because these are rigid scenarios where insurers almost always have the right to say no.

1. The Standard Flood Exclusion

In standard homeowner policies, the word “flood” has an inflexible definition. It means rising surface water that enters the home from the outside in. If a nearby river overflows, if heavy rains cause surface water to pool in your yard and seep under your doors, or if a storm surge hits, the industry considers that a flood.

Standard home policies almost universally exclude this type of flood damage. Unless you purchased a separate flood insurance policy, a home insurance claim denied for rising surface water is a legitimate, ironclad denial. The adjuster has no authority to pay it.

2. Wear and Tear or Gradual Deterioration

Property insurance is designed to cover sudden, accidental, and unforeseen events. A tree snapping in a windstorm and crashing through your ceiling is sudden. A twenty-year-old asphalt shingle roof slowly degrading under the sun for two decades until it leaks is gradual deterioration.

Policies explicitly exclude the natural lifecycle decay of building materials. They insure against specific perils, not the passage of time.

A small supply pipe hidden under your sink has been slowly dripping a few drops a day for months, quietly rotting the wooden cabinet base.

A main water line in the ceiling bursts overnight due to freezing, instantly flooding your kitchen.

3. Homeowner Maintenance Failures

When you sign an insurance contract, you agree to maintain your property and mitigate ongoing damages. If an insurance company can prove through prior inspection reports, satellite data, or visual evidence that a leak clearly existed for years and was ignored, they will issue a denial for homeowner negligence. They are arguing that you knew about an issue and failed to fix it, which directly led to the current damage.

Key Point: Your policy is not a maintenance contract. Ignoring small, known problems until they become catastrophic disasters will almost certainly result in a legitimate denial based on your failure to properly maintain the property.

4. Pre-Existing Conditions

A denial for pre-existing damage means the carrier has gathered evidence showing that the damage was already present before your policy began, or before the specific storm event you are claiming occurred.

How do they prove this? They often pull comprehensive home inspection reports from when you originally purchased the house. They scrape historical real estate listing photos from sites like Zillow to see the condition of your roof years ago. They even purchase high-resolution historical satellite imagery, taken weeks before the date of loss, to look for prior tarping or missing shingles. If they rely solely on blurry satellite photos while ignoring a recent, clean inspection report from your local contractor, this label can sometimes be challenged.

The Most Common Reasons for Challengeable Denials

A massive portion of the claim files I review involve denials that look official but are built on a shaky foundation of assumptions, rushed inspections, or terrible internal documentation.

1. Scope and Cause of Loss Disputes

This is the classic battleground. The insurance company agrees that damage occurred but disputes exactly what caused it. For example, the day after a severe windstorm, you file a claim for roof leaks. The adjuster visits for ten minutes and writes a report stating the leaks are entirely due to “thermal cracking” and age, calling it wear and tear rather than wind damage.

If you then hire your own licensed contractor who clearly documents wind-creased shingles and fresh hail impacts, you have a challengeable denial. The insurer’s hasty conclusion does not match the physical evidence available on the roof.

2. Coverage Misapplication by the Desk Adjuster

Sometimes the field adjuster does a near-perfect job documenting the damage, but the desk adjuster at the corporate office applies the wrong policy language. I see this constantly in complex water damage claims.

A common scenario is confusing “seepage” with a covered “sudden discharge.” The desk adjuster might read a note about a slightly corroded fitting and issue a flat denial for long-term seepage, ignoring the photos showing a massive, sudden pipe rupture that caused the immediate damage. This is a clear misapplication of facts.

3. Documentation Failure by the Field Adjuster

Catastrophe (CAT) adjusters are often exhausted and rushing. It is common to see a claim denied after an inspection simply because the adjuster physically missed the damage. They might have inspected the front slope of the roof but failed to climb into the attic where the rafters are split. When a denial is strictly based on an incomplete or lazy investigation, it is highly challengeable.

“Inspected front slope of residential roof. No visible wind damage or missing shingles observed from ladder at eaves. Claim denied for lack of storm-created openings.”

The Reality: The directional storm winds came heavily from the rear. The back slope suffered severe wind lift, but the adjuster never moved their ladder to the back of the house.

4. Problematic Insurer Conduct and Bad Faith

While less common than simple human error, there are times when a denial crosses the line into bad faith conduct. This happens when a carrier denies a claim without conducting a reasonable investigation, misrepresents policy language, or actively ignores hard evidence submitted by independent professionals.

Bridge: Knowing these common failure patterns is essential for your defense. However, in the heat of a dispute, how do you actually determine which of these patterns is playing out in your specific denial letter?

PAIN SECTION: Diagnostic Signs Your Denial May Be Challengeable

It is infuriating to read a denial letter that completely contradicts what you are standing there looking at with your own eyes inside your ruined home. You know a storm ripped through your neighborhood, you know your living room is destroyed, yet the piece of paper in your hand says the billion-dollar insurance company owes you nothing.

The distinction between a properly investigated denial and an error-filled one is almost never obvious from the corporate jargon in the letter itself. Insurers use highly standardized templates. A rushed, sloppy denial looks exactly the same on paper as a thorough, legitimate one.

However, through years of experience, distinct behavioral patterns emerge. If your situation aligns with any of the following diagnostic indicators, your denial is worth a professional second look:

- 🛑 The cited policy section makes no sense. The letter quotes an exclusion for “earth movement”, but your actual claim was for a kitchen grease fire. This indicates a massive templated error by the desk adjuster.

- 🛑 The timeline of the denial is unusually fast. You suffered a complex, high-dollar loss. The field adjuster visited on a Tuesday afternoon, and you received a final denial by email on Thursday morning. Complex losses require time, experts, and thorough review. A lightning-fast denial on a major claim is a red flag.

- 🛑 The adjuster’s physical visit felt rushed. The adjuster spent less than fifteen minutes for a claim involving three rooms of severe water damage. They didn’t use thermal imaging or moisture meters and refused to go into the crawlspace.

- 🛑 The company ignored your documentation. You provided detailed invoices from a licensed plumber stating a pipe suddenly burst. Yet, the denial letter states the damage was caused by a long-term, gradual leak.

- 🛑 No additional information was ever requested. Before issuing a final denial, a thorough adjuster will almost always ask the homeowner for maintenance records or contractor reports to clarify gray areas. If they denied you outright without a single clarifying question, their investigation is likely biased.

Does a Denied Home Insurance Claim Count Against You?

If you are deciding whether to fight back or walk away, you need to understand the long-term consequences of leaving a flawed denial unchallenged. One of the most frequent questions I hear from homeowners is whether this rejected claim will haunt them in the future. The unfortunate answer is: in some cases, yes.

The industry uses a centralized database called the Comprehensive Loss Underwriting Exchange (C.L.U.E.) report. This database tracks claims history for properties and individuals, usually for five to seven years. The moment you officially file a claim, a permanent file is opened in this system.

Depending on your carrier’s reporting practices and state regulations, a claim that results in zero payout can still be reported to the C.L.U.E. database. Future insurers will see that an incident was reported at your address, even if the current carrier decided they did not owe you money for it.

This matters because insurance underwriting is based on risk frequency. If your record shows multiple filed claims in a short period, even if all were denied, a future underwriter might view your property as high-risk. This is why ensuring the official record is factually accurate is so critical for your financial future.

Warning: Never assume that just because you did not receive a settlement check, the claim “never happened” in the eyes of the global insurance industry. The record usually exists.

What Happens Next Depends Entirely on Your Denial Type

If you have read this far, you should be looking at the letter sitting on your desk with a completely different perspective. Your next move is not a generic, angry phone call. Your next move must be a strategic, calculated response to the exact reason the insurer gave you in writing.

Different types of insurance denials require entirely different mechanisms to fight them. If you have a partial scope and valuation dispute, invoking the appraisal clause is a powerful, binding tool. But if you try to use that same appraisal clause to fight a full coverage misapplication, your request will be rejected, wasting weeks of your time. Conversely, if you file a formal Department of Insurance complaint over a simple pricing disagreement, the state regulatory body will not help you.

You have a narrow window to get this right. You need to look at your specific denial type, understand the tools at your disposal, and apply the exact right pressure point to the carrier. The bridge from a denied claim to a fair outcome requires matching the right procedural tool to the exact problem.

To ensure you do not make a procedural mistake and waste your limited appeal window, evaluating your complete strategic options landscape is the single most critical action you can take right now.

Finding the Confidence to Push Back

There is a unique type of stress that comes from having your home damaged, only to be told by a professional at a billion-dollar company that the damage isn’t their problem. It can make you question your own memory of the event and leave you feeling small in the face of a massive corporate machine. I want you to know that feeling this way is part of the process they have built, but it doesn’t have to be the end of your story.

A denial letter is a position, not an absolute truth. When the facts on the ground and the photos on your phone tell a different story than the template-driven letter in your hand, you have every right to stand your ground. You are not being “difficult” or “aggressive” by insisting on an accurate investigation; you are simply holding the insurer to the contract you both signed. Take that deep breath, organize your photos, and approach the next phase with the quiet confidence of someone who knows the truth of what happened to their home.

Claim Denied Resource Directory

Now that you understand the critical difference between a legitimate policy exclusion and a challengeable adjuster error, your next step is mastering the specific mechanics of your dispute path. Depending on exactly why your claim was rejected, you will need to utilize entirely different administrative tools.

Below is our complete library of deep-dive guides covering every aspect of denied claims. Find the specific resource that matches your denial type to understand the exact procedural steps required to protect your property and fight back effectively.

| Claim Denied Resource List | What This Guide Covers |

|---|---|

| How To Appeal A Homeowners Insurance Claim Denial | The mechanics of the formal internal appeal process, expected timelines, and required documentation. |

| How To File Complaint Against Home Insurance Company | How to properly report procedural violations to your state’s Department of Insurance. |

| Homeowners Insurance Bad Faith Claim | How to recognize when an insurer’s poor conduct crosses from standard human error into legal bad faith. |

| Home Insurance Denial Letter What It Means | A detailed breakdown of how to decode the specific policy citations and deadlines buried in your letter. |

| Does Denied Home Insurance Claim Affect Future Coverage | How denied claims appear on your property’s C.L.U.E. report and impact your future insurability. |

| Home Insurance Claim Denied Wear And Tear | How adjusters determine gradual deterioration versus sudden, covered storm damage. |

| Insurance Denied Claim For Pre-existing Property Damage | Understanding exactly how insurers use past inspection records to deny your current property claims. |

| Home Insurance Claim Denied Negligence | The strict legal difference between passive wear and tear and your active failure to maintain your home. |

| Partial Home Insurance Claim Denial | Why this critical operational distinction determines exactly which dispute paths are available to you. |

| Homeowners Insurance Underpaid Claim | What to do when the final settlement check arrives but does not even come close to covering repairs. |

❓ FAQ

🤷♂️ Why was my home insurance claim denied so incredibly fast?

An unusually fast denial often means the desk adjuster categorized the damage as a hard policy exclusion immediately upon opening the file. In some cases, a rapid denial on a complex loss simply indicates a rushed, severely incomplete investigation.

🕵️♀️ How do insurance companies actually investigate before denying?

Insurers typically dispatch a field adjuster to take photos and measurements. They also review local weather data, past C.L.U.E. reports, satellite imagery, and your policy language. An internal desk adjuster then reviews this combined file to make the determination.

📸 Can I submit new photos if my property claim was denied?

Absolutely. If your denial is challengeable, submitting new, close-up photographic evidence that directly contradicts the adjuster’s flawed findings is a necessary part of requesting a formal claim review.

☔️ What does a wear and tear exclusion actually mean in practice?

It means the insurance company has concluded that the physical damage is strictly the result of natural aging or the end of a building material’s lifespan, rather than a sudden and accidental covered event like a storm.

⏳ Is there a hard time limit to respond to a denial letter?

Yes. The denial letter itself and your specific state department of insurance regulations outline strict deadlines for appealing. Missing these deadlines can permanently and legally close your file.

📞 Should I call my local insurance agent if my claim is denied?

Your agent can explain what the letter says, but they typically do not have the authority to overturn a claims department decision. You must address your dispute formally and directly with the claims department.

🚫 What happens if I have two denied claims on my record?

Multiple denied claims in a short period can signal to underwriters that your property is high-risk. For a full breakdown of how this impacts your insurability, see our guide on how denied claims affect your future coverage.

📄 Can an insurance company deny a claim without sending an adjuster out?

Yes. If you report damage that is explicitly excluded across the board (like surface flooding) or if your policy was completely inactive on the date of loss, the insurer can deny the claim administratively without a physical inspection.

A denial means different things depending on your coverage and claim type.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

One handles scope disputes. One handles bad faith. They are not the same problem.

- 5 patterns that signal your settlement is probably short

- Who the adjuster at your door actually works for

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When the denial involves bad faith and not just a disagreement

- Four options after a denial, including one most homeowners never hear about

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.