- The appraisal clause is a binding dispute resolution mechanism built into most standard home insurance policies to settle disagreements over the dollar value of a claim.

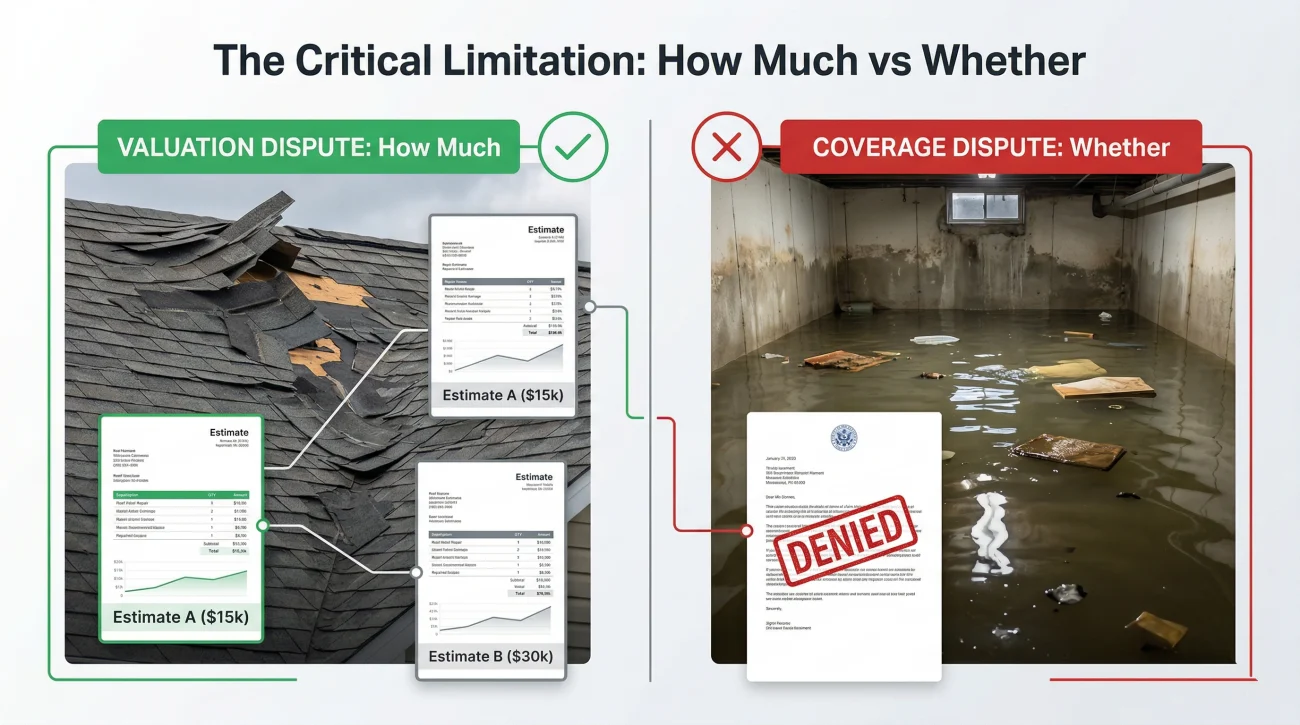

- It can only be used for valuation and scope disputes (disagreements over “how much” a repair costs), not for coverage disputes (disagreements over “whether” the policy covers the damage at all).

- The process involves you and the insurer each hiring an independent appraiser. If the two appraisers cannot agree on the repair cost, a neutral third party called an umpire makes the final, binding decision.

- Understanding the financial cost, the necessary preparation, and the strict mechanics of the process is required before anyone sends a demand letter.

What the Appraisal Clause Actually Is

At its core, the appraisal clause is a contractual agreement designed to keep valuation disputes out of the court system. It acts similarly to private, binding arbitration, but it is highly specialized for property damage.

When you invoke the appraisal clause, you are essentially telling the insurance company that negotiations have failed. You are removing the insurance adjuster from the equation and replacing them with a formal panel of three people.

The panel consists of your chosen appraiser, the insurance company’s chosen appraiser, and a neutral umpire. The goal of this panel is singular: to determine the exact, fair market dollar value of your covered property loss.

Once the panel reaches an agreement (either by the two appraisers agreeing, or one appraiser agreeing with the umpire), the dollar figure they set is binding on both you and the insurance company. The carrier must pay it, and you must accept it.

The Critical Limitation: “How Much” vs “Whether”

Before we go any further into the mechanics, we must address the single biggest point of confusion I see homeowners make. The appraisal clause has a strict jurisdictional limit.

The appraisal panel can only decide how much something costs to fix. They have zero legal authority to decide whether an item is covered under your policy.

If the insurance company issued a full denial stating that your damage was caused by a flood (which is excluded from standard policies) instead of wind, you cannot use the appraisal clause. That is a coverage dispute. On the other hand, if the insurance company agrees that wind damaged your roof, but they think it can be patched for $500 while your contractor says it requires a $10,000 full replacement, you have a valuation dispute. That is exactly what the appraisal process is built for.

This line gets blurry when dealing with a partial claim denial where the insurer accepts some damage but denies other items. If you are unsure what kind of denial you are facing, you must clarify that first. If you attempt to invoke appraisal on a full coverage denial, the insurer will simply reject your demand in writing.

“We are denying your claim because the pipe leaked for six months, which falls under the gradual damage exclusion.”

“We agree the sudden pipe burst is covered, but we will only pay to replace the kitchen flooring, not the custom cabinets.”

When the Appraisal Clause is Applicable

If your dispute clears the coverage hurdle, there are several specific scenarios where invoking this clause is mechanically appropriate. Based on my experience reviewing stalled claims, these are the most common triggers for a successful appraisal demand.

The Xactimate vs Real World Pricing Gap

Adjusters use software called Xactimate to generate their estimates. This software relies on average regional pricing databases. Often, these database prices lag significantly behind the actual real world cost of labor and materials in your specific neighborhood, especially after a major storm when local demand spikes. If your local contractors simply cannot do the work for the Xactimate price, the appraisal panel can adjust the unit costs to reflect reality.

Scope of Damage Disagreements

Valuation is not just about the price of a single shingle; it is also about the scope of the repair. If the insurer’s estimate only includes replacing drywall, but your contractor insists that the local building code requires upgrading the electrical wiring inside that wall, this is a scope dispute. Appraisers can determine the correct, necessary scope of work to bring the property back to its pre-loss condition.

Actual Cash Value (ACV) Depreciation Disputes

Insurers often apply heavy depreciation based on the supposed age and condition of your property. If an adjuster arbitrarily decides your hardwood floors were in “poor” condition and depreciates them by 70 percent, reducing your upfront check to almost nothing, an appraiser can step in. The appraisal panel has the authority to review the actual condition and adjust the depreciation percentage to a fair number.

If you have a Replacement Cost Value (RCV) policy, the appraisal award will typically establish both the new ACV and the new RCV. The insurer will issue a check for the new ACV amount right away. You then complete your repairs and submit the final invoices to claim the newly established, larger RCV holdback, just like you would in a standard claim.

Who Should Serve as Your Appraiser?

Before the formal process begins in earnest, selecting who will represent your side is actually the most consequential decision you will make. You should strictly vet your appraiser against three criteria before hiring them:

- ✔️ Xactimate Fluency: Do they write and argue line items in the exact software the carrier uses?

- ✔️ Appraisal Experience: Have they successfully negotiated appraisal awards, or do they only write initial estimates?

- ✔️ Impartiality: Are they free from any direct financial conflict of interest regarding your repair work?

In the claims industry, public adjusters frequently step into this role. Because they spend their days calculating scopes of loss and disputing valuations with carriers, they possess the exact technical skill set required for the appraisal panel.

If you are facing a massive gap in repair costs and need representation, a licensed public adjuster can serve as your appraiser and knows exactly how to navigate this strict procedural mechanism. You can request a free review to see if a public adjuster is the right fit for your specific dispute.

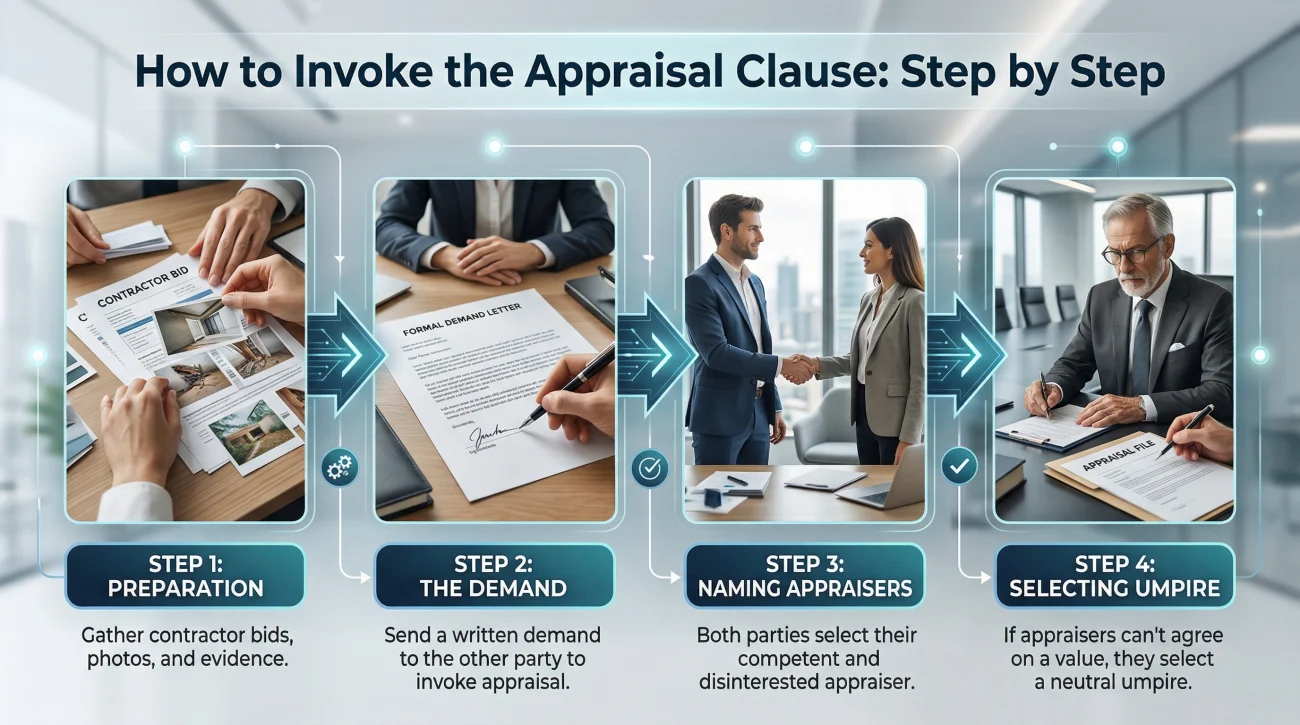

How to Invoke the Appraisal Clause: Step by Step

The appraisal process is formal. You cannot trigger it by angrily telling the adjuster over the phone that you want an independent review. It requires a specific procedural chain of events.

Step 1: Preparation (What to Hand Your Appraiser)

Before anyone sends a demand letter, you need to arm your future appraiser with ammunition. You should prepare a highly detailed contractor estimate, a comprehensive photo log of the damage, and a clear document comparing your contractor’s scope against the adjuster’s estimate. Giving your appraiser a fully documented file on day one drastically increases their leverage.

“The most successful appraisal files I see are the ones where the homeowner’s contractor has provided a highly detailed, line-by-line estimate that clearly exposes the missing items in the insurance company’s generalized scope of loss.”

Step 2: The Written Demand

The process begins when either party sends a formal, written demand for appraisal. It is important to note that the insurance company also has the right to invoke appraisal. If they trigger it first, you are contractually obligated to participate, which makes hiring a strong appraiser immediately critical.

Once the demand is received, a strict timeline begins. Most standard HO3 policies specify that the receiving party must respond and name their appraiser within 20 days (always check your specific policy language for your exact timeframe).

Sample Appraisal Demand Language:

“Pursuant to the Appraisal clause located in the Conditions section of my policy [Insert Policy Number], I am formally demanding an appraisal to resolve our disagreement over the amount of loss for the claim dated [Insert Date]. Please find the contact information for my chosen independent appraiser below. I expect your appraiser’s contact information within [Insert policy timeframe, typically 20 days].”

Step 3: Naming the Appraisers

You will hire a competent, independent appraiser to represent your side of the valuation. The insurance company will hire their own independent appraiser. These appraisers must be impartial, meaning they cannot have a direct financial interest in the final settlement amount.

Step 4: Selecting the Umpire

Before the two appraisers even look at your damage, they must agree on a neutral umpire. This is a critical safety net. If the two appraisers investigate the damage and cannot reach an agreement, the umpire will break the tie. If the two appraisers cannot agree on who the umpire should be after a set period (usually 15 days, though always check your specific policy language for your exact timeframe), either party can petition a local judge in a court of record to appoint one.

Step 5: The Evaluation and The Award

The two appraisers will separately review your policy, the initial estimates, the contractor bids, and the physical damage. They will then attempt to reconcile their differences. If they agree on the final number, they sign a binding document called an “Appraisal Award.” The process ends there.

If they remain deadlocked on certain line items, they submit their differences to the umpire. The umpire reviews the specific disputed items and makes a ruling. An Appraisal Award signed by any two of the three panel members (your appraiser and the umpire, or the insurer’s appraiser and the umpire) becomes final and binding.

What the Appraisal Process Costs

Unlike a standard internal appeal process which is free to submit, the appraisal clause requires you to spend your own money. The policy language dictates a specific breakdown of who pays for what.

You are responsible for paying 100 percent of your appraiser’s fees. The insurance company pays 100 percent of their appraiser’s fees. If the umpire is needed to break a tie, you and the insurance company split the umpire’s hourly fee equally.

Appraisers typically charge either an hourly rate or a flat fee based on the complexity of the claim. Because appraisers must be impartial, they generally cannot work on a contingency fee (a percentage of the final award) for this specific role, though state regulations on this vary.

| Expense Item | Who Pays | Typical Cost Structure |

|---|---|---|

| Your Appraiser | Homeowner (100%) | Hourly rate ($150 – $300/hr) or flat fee |

| Insurance Appraiser | Insurance Company (100%) | Hourly rate or contracted flat fee |

| The Neutral Umpire | Split 50/50 | Hourly rate (often higher, $250 – $500/hr) |

When the math makes sense: You must weigh the cost of the process against the disputed amount. If the insurance company is underpaying your claim by $2,000, spending $1,500 on an appraiser and $500 on half an umpire fee makes no financial sense. However, if your contractor’s bid is $45,000 and the insurer is offering $15,000, investing a few thousand dollars into the appraisal process yields a massive return on investment.

Diagnostic: Is Your Dispute Ready for Appraisal?

It is easy to get overwhelmed by the procedural rules, but diagnosing whether your claim belongs in appraisal is actually quite straightforward. If you are experiencing the following patterns, you have a classic valuation dispute that this clause was built to solve:

- 🚩 The coverage is acknowledged: The insurer sent you a settlement check, meaning they agree the event is covered, but the check is insultingly low.

- 🚩 The pricing is disconnected: Your local contractors physically cannot buy the materials and pay the labor rates that the insurer’s Xactimate estimate dictates.

- 🚩 The scope is artificially narrow: The insurer agrees your kitchen flooded, but their estimate stubbornly refuses to include the cost of replacing the ruined subfloor beneath the tile.

- 🚩 The negotiations are deadlocked: You have submitted supplemental estimates from your contractors, and the desk adjuster simply replies with “we stand by our initial evaluation.”

Note: Appraisal cannot be used to overturn a full claim denial.

The Risks You Must Consider

While the appraisal clause is an excellent tool, it is not a magic wand. There are inherent risks in relinquishing control of your claim to a panel.

The primary risk is the binding nature of the award. If your appraiser performs poorly, or if the umpire sides heavily with the insurance company’s pricing, you are stuck with the resulting number. You cannot reject the Appraisal Award and then decide to sue the insurance company for a higher valuation. The courts consistently uphold properly executed appraisal awards.

Furthermore, picking the wrong appraiser can severely damage your outcome. If you choose someone who lacks technical estimating experience, they will be outmatched by the insurance company’s seasoned appraiser.

Hiring your general contractor as your appraiser. Even if allowed in your state, they often lack the specialized Xactimate knowledge required to debate the carrier’s appraiser line by line.

Hiring an independent professional, such as a licensed public adjuster or dedicated insurance appraiser, who speaks the exact language of claims settlement.

Knowing Your Options Before You Commit

Because of the binding risks and the upfront costs involved, you should never send the demand letter until you have mapped out all your available options.

Sometimes, simply filing a highly documented formal appeal is enough to fix a minor scope gap without spending money on appraisers. Other times, if the insurer is acting in bad faith or actively misrepresenting your policy, you need a completely different path entirely.

If you have received a lowball offer or a partial denial and are trying to figure out your next move, you need to read the full breakdown of every option available after a claim denial and how to choose the right path for your specific dispute.

When Appraisal is Not Enough

As I have emphasized, appraisal fixes math problems. It does not fix legal problems.

If the insurance company has issued a full coverage denial, or if their conduct during the claims process crosses the line into unreasonable delay, intimidation, or intentional misrepresentation of your policy, the appraisal panel has no authority to intervene or punish the carrier.

Furthermore, what happens if you win the appraisal, the panel signs the award, and the carrier simply refuses to pay it? The appraisal panel cannot force the carrier to write the check. At that point, the carrier’s refusal crosses into bad faith territory.

For cases involving bad faith conduct, complete coverage disputes, or a refusal to honor a signed appraisal award, the appropriate escalation path involves legal representation. A licensed attorney can evaluate the carrier’s actions and force compliance through the legal system. If your dispute requires legal intervention, you can explore your options with an insurance claim attorney.

Final Thoughts on Resolving the Gap

The insurance adjuster’s initial estimate is simply their opening position. You do not have to accept a number that fails to reflect the reality of rebuilding your home.

Appraisal is a highly technical mechanism that forces a carrier to defend their math against an equal expert. By arming yourself with independent estimates and understanding the procedural rules, you stop being a passive participant. When used correctly on a true valuation dispute, the appraisal panel is often the most effective way to force a fair outcome without stepping into a courtroom.

❓ FAQ

⚖️ How does the home insurance appraisal clause work?

It acts like private arbitration for pricing disputes. You hire an appraiser, the insurer hires one, and together they agree on a neutral umpire. If the two appraisers cannot agree on the cost of repairs, the umpire breaks the tie, and the final dollar amount is binding.

🚫 Can I use the appraisal clause if my claim was completely denied?

No. The appraisal clause strictly resolves valuation disputes (how much things cost). It does not grant authority to determine coverage (whether the policy covers the event). Full denials cannot be resolved through this process.

⏱️ How long does the insurance appraisal process take?

Timelines vary greatly depending on the complexity of the damage and the schedules of the appraisers. A simple dispute might resolve in 30 to 60 days, while large, complex losses requiring heavy umpire involvement can take several months.

💰 Who pays for the appraisal process in a home insurance claim?

You pay your appraiser’s fee, and the insurance company pays their appraiser’s fee. If the neutral umpire is required to step in and review the file, you and the insurance company split the umpire’s total cost 50/50.

🤝 What is the difference between appraisal and arbitration?

Arbitration is a formal legal proceeding that resembles a court case, where an arbitrator can rule on legal interpretations and liability. Appraisal is a much narrower, informal panel restricted solely to setting the dollar value of physical damage.

🔨 Can my contractor be my appraiser?

In most states, your appraiser must be impartial and disinterested. This means your contractor usually cannot serve as your appraiser if they have a financial interest in the final outcome (like a signed contract to do the repair work).

📝 Is an appraisal clause decision legally binding?

Yes. Once an Appraisal Award is signed by at least two of the three panel members (for example, your appraiser and the umpire), the dollar amount is legally binding on both the homeowner and the insurance company.

🧑⚖️ Who chooses the insurance appraisal umpire?

The two independent appraisers must agree on a neutral umpire before they begin evaluating the loss. If they cannot agree on someone within a specified timeframe (usually 15 days), either party can ask a judge in a local court to appoint one.

📅 When is it too late to invoke the appraisal clause?

You must generally invoke appraisal before you file a lawsuit against the insurer, and before you accept a final settlement that includes a release of all claims. Check your specific policy language for exact deadlines.

📩 How do I demand an appraisal from my insurance company?

You must send a formal, written demand letter referencing the appraisal clause in your policy conditions. The letter should clearly state that you are disputing the amount of loss and provide the contact information for the independent appraiser you have hired.

A denial sits inside a larger picture. These explain the parts around it.

- How the settlement process works after damage is reported

- Which parts of your policy apply when damage is involved

- How your damage type affects what the insurer is required to pay

- Whether the damage you have is actually worth filing for

- What happens when the claim you filed gets rejected

- How independent representation changes what gets documented

- When a disputed claim moves into legal territory

Not all denials are final. The path forward depends on why it happened.

- Whether your damage assessment left money on the table

- What the inspector who came to your home was actually there to do

- The parts of water damage that standard inspections routinely miss

- What fire and smoke assessments leave out of the scope

- Why the insurer's roof estimate is almost always lower than the roofer's

- When the denial crosses from a dispute into something that needs legal leverage

- Four options to fight back, including one most homeowners never use

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.