- Standard policies are designed to cover “sudden and accidental” events, not gradual wear and tear or maintenance issues.

- Water damage coverage depends entirely on the source: sudden internal bursts are typically covered, while external flooding and slow leaks are usually excluded.

- Your policy is divided into different coverage types (Dwelling, Personal Property, Loss of Use), each with its own specific limits and rules.

- Payouts vary drastically based on whether you have Actual Cash Value (ACV) or Replacement Cost Value (RCV) coverage for your property.

- If a denial reason does not match the actual facts of how your damage occurred, the insurance company’s coverage decision may be challengeable.

The Moment Most Homeowners Actually Read Their Policy

In my years of reviewing property claims, I have noticed one universal truth: most homeowners only sit down to read their insurance policy after a disaster has happened. Even worse, many only read it after receiving a denial letter. When you are standing in a flooded living room or staring at a damaged roof, finding out that your coverage does not work the way you assumed it did is an incredibly stressful experience.

There is a massive gap between what homeowners think their policy covers and what the dense, legal language actually dictates. When you pay your premiums every month, it is easy to adopt the mindset that “damage is damage” and the insurance company will simply write a check to fix it. Unfortunately, the claims process operates on a strict set of definitions, exclusions, and characterisations.

I am writing this guide to walk you through exactly what homeowners insurance covers, without the confusing industry jargon. We are going to look at the different parts of your policy, the critical difference between sudden and gradual damage, and the specific exclusions that catch families off guard every single day. Understanding the boundaries of your policy is the very first step in protecting your financial interests if you ever need to file a claim.

“The most heartbreaking claims I review are not the ones with massive destruction. They are the claims where a homeowner suffered genuine, expensive damage, but because they misunderstood one single word in their policy exclusions, the claim is rightfully denied by the carrier. Education before the loss is your best defense.”

The Core Pillars of Standard Coverage

When you buy a standard homeowners insurance policy, you are not just buying one blanket of protection. You are actually buying a package of different coverages bundled together. Adjusters look at your property damage and immediately categorize it into these specific “buckets.”

Coverage A: Dwelling Coverage

This is the core of your policy. Dwelling coverage protects the physical structure of your home. If you were to pick up your house and shake it, whatever does not fall out is generally considered part of the dwelling. This includes the roof, the foundation, the framing, the drywall, attached garages, and built-in appliances or fixtures.

If a tree falls on your roof or a fire destroys your kitchen, Coverage A is the part of your policy that pays to rebuild or repair the structure.

Signs You May Be Underinsured

The limit on your Coverage A should reflect the total cost to rebuild your home from the ground up in today’s construction market. This is a common trap: your home’s real estate market value might be $400,000, but because of soaring material and labor costs, it might cost $550,000 to actually rebuild it after a total loss. If your Dwelling limit is tied only to your mortgage amount or an outdated market valuation, you risk being severely underinsured when a catastrophic event hits.

Coverage B: Other Structures

This bucket covers structures on your property that are not physically attached to your main dwelling. Common examples include detached garages, fences, gazebos, and sheds. In a standard policy, Other Structures coverage is usually strictly capped at 10 percent of your main Dwelling Coverage.

Because fences and detached outbuildings are incredibly vulnerable to storms, this 10% limit is frequently exhausted quickly. For a deeper breakdown of how claims are handled for these specific items, read our complete guide on Other Structures Coverage limits and exclusions.

Coverage C: Personal Property

Personal property coverage protects your “stuff”: your furniture, clothing, electronics, kitchenware, and sporting equipment. While Coverage C seems straightforward, it contains hidden traps.

Standard policies place severe “sub-limits” on high-value items. Even if you have $150,000 in general personal property coverage, your policy might cap the payout for stolen jewelry at just $1,500 total, or strictly limit payouts for firearms and electronics. Knowing these sub-limits before you claim is critical.

Coverage D: Loss of Use (Additional Living Expenses)

If a covered peril makes your home completely uninhabitable, you need a place to stay. Coverage D (Additional Living Expenses, or ALE) pays for the extra costs you incur because you cannot live in your home, such as hotel bills or temporary rental homes.

This is a highly scrutinized area of the claims process with strict reimbursement rules. To understand exactly what qualifies as an “additional” expense and how to submit those receipts properly, see our dedicated Loss of Use Coverage Guide.

Named Perils vs. Open Perils: How the Burden of Proof Shifts

Understanding what items are covered is only half the battle. You also must understand what events (perils) those items are covered against. In the insurance world, policies are generally written in one of two ways: Named Perils or Open Perils.

| Named Perils Policy | Open Perils Policy |

|---|---|

| Only covers damage caused by a specific list of events explicitly written in the policy (e.g., fire, wind, hail, theft). | Covers damage caused by ANY event, UNLESS that specific event is explicitly excluded in the policy language. |

| Burden of Proof: The homeowner must prove the damage was caused by one of the listed perils. | Burden of Proof: The insurance company must prove the damage was caused by an excluded event to deny the claim. |

The HO3 vs. HO5 Difference

When reviewing documents, you will often see policies labeled as HO3 or HO5. The difference lies entirely in how they apply those peril rules.

| HO3 Policy (The Standard) | HO5 Policy (The Premium) |

|---|---|

| Dwelling: Open Perils Personal Property: Named Perils | Dwelling: Open Perils Personal Property: Open Perils |

| Most common policy type. Broad protection for the house itself, but stricter limits on proving damage to your belongings. | Broader overall protection. If you drop paint on your expensive sofa, an HO5 might cover it, while an HO3 likely will not. |

💡Pro Tip: Knowing which coverage bucket your damage falls into, and whether you are dealing with named or open perils, is the first step in speaking the adjuster’s language. Understanding these two factors allows you to report your claim accurately and sets the right tone for a professional negotiation.

The Most Expensive Assumption: “Damage is Damage”

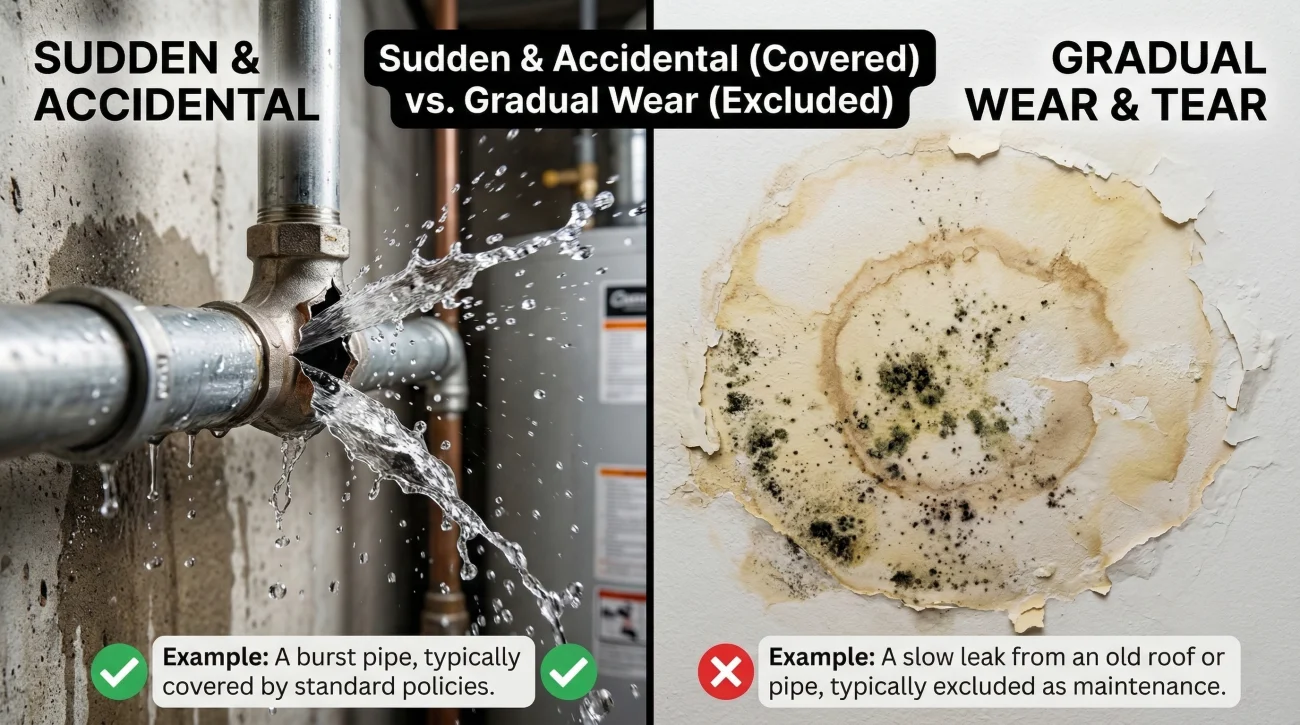

The single most destructive mindset a homeowner can have during a claim is believing that because an item is broken, the insurance company will automatically pay to fix it. Homeowners insurance is strictly designed to cover events that are sudden and accidental. It is not a home warranty, and it is certainly not a maintenance contract.

The timeline of the damage is the most important factor an adjuster evaluates.

A pipe beneath your kitchen sink has been dripping slightly for six months. Over time, it rots the cabinet floor, creates mold, and eventually causes the subfloor to warp. Because this happened slowly over time and is considered a maintenance failure, standard policies will deny this claim.

You are sitting in your living room and suddenly hear a loud pop, followed by water pouring through the ceiling. A supply line in the upstairs bathroom has completely ruptured. Because the event was sudden, unexpected, and immediate, the resulting water damage is generally covered.

The danger here lies in how the adjuster characterizes the damage. Often, a sudden event might look similar to gradual damage if it is not inspected properly. For example, a sudden roof leak caused by a storm might go unnoticed for a few days. When the adjuster arrives, they might see old water stains near the new, severe damage and attempt to label the entire event as “gradual.”

Because pipes and plumbing fail so frequently, we highly recommend reading our specific guide on how the sudden vs gradual rule applies specifically to water damage claims to avoid inadvertently sabotaging your own payout.

🗝️ Key Point: If an insurer can argue that a reasonable homeowner should have noticed and fixed a problem before it caused catastrophic damage, they will use the gradual damage exclusion to deny the claim.

When communicating with your insurer about a new claim, your terminology matters immensely. Consider the difference in these two statements when opening a claim:

“I just noticed my ceiling is leaking. I think water has been getting in up there for a while because the paint is peeling.”

“During the severe thunderstorm last night, a leak suddenly appeared in my ceiling. I need to report this sudden water damage.”

Never lie or misrepresent facts. But be incredibly precise. Do not guess about how long damage has been occurring if you do not actually know. Stick to the facts of when you discovered the sudden event.

The Water Confusion: Flood vs. Water Damage

To a homeowner with an inch of water in their basement, it feels like a flood regardless of where the water came from. But to an insurance company, the source of the water dictates the coverage.

- ✅ Covered Water Damage: Water that originates from inside the home (burst pipes, overflowing bathtubs) or rain that enters because a covered peril suddenly created an opening (like wind ripping off shingles).

- ❌ Excluded Flood Damage: Water that originates from outside the home and rises or flows over normally dry land (overflowing rivers, storm surge, or heavy surface runoff seeping under doors).

Standard homeowners policies explicitly exclude flood damage. This distinction causes massive confusion during severe weather events. If you are dealing with a complex water scenario, read our detailed breakdown of how adjusters classify Flood vs. Water Damage to understand how your specific damage will be interpreted.

The Exclusion List That Surprises Homeowners Most

Every policy has an exclusions section. Exclusions exist because insurers cannot price policies accurately if they have to cover highly predictable events, entirely uncontrollable regional disasters, or gross negligence. Here are the standard exclusions that catch homeowners by surprise:

1. Flood (External Water)

As discussed, rising external water is universally excluded from standard HO3 policies. To get coverage for this, you must purchase a separate flood insurance policy, typically through the National Flood Insurance Program (NFIP) or a private flood insurer.

2. Earth Movement and Sinkholes

Standard policies do not cover damage caused by the earth moving. This includes earthquakes, landslides, mudslides, and mine subsidence. If an earthquake cracks your foundation, a standard policy pays nothing. You need a specific earthquake endorsement.

3. Sewer and Drain Backup

If the municipal sewer line fails and pushes raw sewage into your home, standard policies do not cover the cleanup. You must purchase a specific “Water Backup and Sump Overflow” endorsement. For more details on this add-on, see our Sewer Backup Coverage guide.

4. Gradual Water Damage

Any leak, seepage, or condensation that occurs continuously or repeatedly over a period of time (usually defined as weeks or months) is explicitly excluded as a maintenance issue, regardless of the severity of the damage it eventually causes.

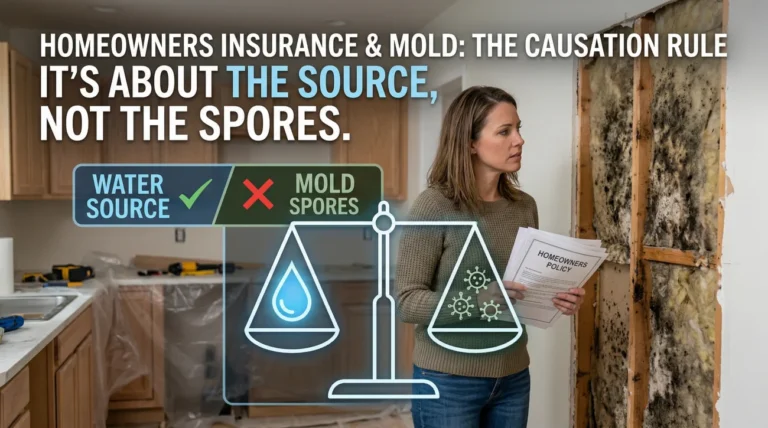

5. Mold (The Causation Rule)

Mold is based on causation. If mold grows because of chronic humidity or a slow, hidden leak (which are excluded), the mold is also excluded. However, if a sudden burst pipe ruins your drywall, and mold begins to grow a few days later, that mold is often covered because it was directly caused by a covered peril. For a deeper explanation of this specific timeline, see our breakdown of how adjusters investigate mold causation. Even when covered, most policies place strict sub-limits on mold remediation.

6. Normal Wear and Tear

If your 25-year-old shingle roof finally starts leaking simply because the shingles have deteriorated from decades of sun exposure, insurance will not pay for a new roof. Replacing aging components is the financial responsibility of the property owner. However, if severe weather caused the breach, you should verify whether your roof leak is actually covered before accepting a “wear and tear” denial.

Warning: The exclusions list is where insurance companies find their legal footing to deny claims. If your denial letter cites an exclusion, your first step is to pull your actual policy and read the exact phrasing to see if the adjuster applied it correctly.

ACV vs. RCV: The Decision You Made Years Ago

Let us say a storm destroys your 10-year-old roof, and it will cost $20,000 to replace it. Will the insurance company write you a check for $20,000? The answer depends on a choice made when you purchased the policy: Actual Cash Value (ACV) versus Replacement Cost Value (RCV).

Actual Cash Value (ACV) means the insurance company pays you the value of the damaged item today, accounting for age and condition. They apply depreciation. If your roof was expected to last 20 years, and it is 10 years old, it has lost half its value. The insurer might calculate the ACV payout as $10,000. You are left to pay the remaining $10,000 out of pocket.

Replacement Cost Value (RCV) means the insurance company pays to replace the damaged item with a new item of similar kind and quality, without deducting for depreciation. Usually, they pay the ACV amount upfront, and then reimburse you the remaining depreciation once the repairs are completed and invoiced. In this scenario, you would eventually receive the full $20,000 (minus your deductible).

What is Actually on Your Declarations Page

The “Declarations Page” (often called the Dec Page) is the summary of your coverages. Adjusters look at this page first to confirm your limits before they ever look at photographs of your damage. You should be able to identify what fields exist on it:

- 👉 Policy Period: The exact dates your coverage is active. If damage occurs outside these dates, there is no coverage.

- 👉 Coverage Limits: The maximum dollar amounts for Coverage A, B, C, D, E, and F.

- 👉 Deductibles: The amount subtracted from your payout. Pay close attention here. A $1,000 “All Peril” deductible is straightforward. But a “2% Wind/Hail” deductible means 2% of your total dwelling coverage. If your home is insured for $300,000, a 2% deductible means you pay the first $6,000 out of pocket before insurance kicks in. This single field catches thousands of homeowners off guard after a major storm.

- 👉 Endorsements/Riders: A list of optional coverages you purchased, such as Water Backup, Scheduled Personal Property, or Mold enhancements.

What Happens Right After You File

Once you verify that your damage falls under a covered peril and you officially open a claim, the insurance company will assign an adjuster to your case. Their job is to inspect the damage, apply the policy rules we just discussed, and determine the settlement amount.

It is vital to understand that the adjuster works for the insurance company, not for you. The burden of documenting the extent of your loss falls squarely on your shoulders. From the moment the claim is filed, you need to save every receipt, photograph every piece of debris before it is removed, and communicate exclusively in writing.

For a complete breakdown of the timeline, the adjuster’s visit, and how to protect yourself during the evaluation phase, read our comprehensive guide on the Home Insurance Claim Process.

Signs Your Coverage May Have Been Misapplied in Your Claim

The claims process is handled by human adjusters, and humans make mistakes. Sometimes, a quick inspection leads an adjuster to characterize damage incorrectly, triggering an exclusion that should not apply. It is incredibly frustrating to know you suffered a sudden, covered event, only to receive a denial letter claiming it was a maintenance issue.

If you are currently holding a denial letter or a severely underpaid estimate, here are the signs that the insurance company’s coverage decision may be flawed and worth a second look:

- The denial letter cites an exclusion (like “earth movement” or “gradual seepage”) that simply does not match the reality of how the sudden damage occurred.

- The damage perfectly matches a covered event, but the adjuster cited a vague maintenance failure without providing engineering evidence.

- The insurer applied heavy Actual Cash Value (ACV) depreciation to your property, but your Declarations Page clearly states you purchased Replacement Cost Value (RCV) coverage.

- The adjuster characterized sudden water damage as “gradual” based purely on sight, without investigating the actual source of the rupture.

- Your claim was denied for an exclusion that does not appear anywhere in the actual policy language quoted in your letter.

When to Challenge a Coverage Decision

If your denial reason does not match your understanding of your policy or the facts of your damage, that gap is worth examining. Do not simply accept a denial because it is printed on official letterhead. Exclusions must be applied accurately, and the burden of proof often lies with the insurer depending on your policy type.

Understanding the intricacies of policy language is complex, but understanding the fundamentals of home insurance coverage is your right as a policyholder. When the line between covered damage and an exclusion becomes blurred by an adjuster’s opinion, knowing exactly who to call can change the trajectory of your claim.

If your denial is based on a pure valuation dispute, a missing scope item, or an adjuster mischaracterizing a sudden water event as a “gradual leak,” discovering whether you should hire a public adjuster to review the scope is usually your best first step. However, if the insurer is acting in bad faith, aggressively misinterpreting state law, or denying a massive total loss based on a complex legal exclusion, it is time to consult a denied claim insurance lawyer.

Final Thoughts on Protecting Your Investment

I have sat across the table from too many families who lost thousands of dollars simply because they accepted an adjuster’s first answer as the absolute truth. Your homeowners insurance policy is a legally binding contract; it outlines rules that bind both you and the insurance carrier.

By understanding the core coverages, the strict divide between sudden and gradual events, and the exclusions that dictate the rules, you level the playing field. Read your Declarations Page today, document your home’s condition before a storm hits, and if a coverage decision during a claim feels wrong, verify the exact policy language. Education is your leverage; do not wait until disaster strikes to start learning the rules of the game.

Deep Dive: Coverage Scenarios & Specifics

Because coverage nuances vary drastically depending on the specific type of damage, we have created dedicated guides addressing the most confusing policy scenarios. If you are dealing with a specific type of loss, consult the relevant guide below.

| Coverage Guide | What You Will Learn |

|---|---|

| Flood vs Water Damage Insurance | The critical distinction between rising external water and sudden internal leaks, and how adjusters classify them. |

| Does Homeowners Insurance Cover Water Damage? | A deep dive into the “sudden vs gradual” rule that determines the outcome of almost all plumbing and leak claims. |

| Does Homeowners Insurance Cover Mold? | Understanding the causation rule: why the source of the moisture matters more than the mold itself, and how sub-limits apply. |

| Does Homeowners Insurance Cover Foundation Damage? | The honest truth about why most settling and cracking is excluded, and the very narrow exceptions where coverage applies. |

| What Homeowners Insurance Does Not Cover | A comprehensive guide to the standard exclusions, why insurers mandate them, and how to spot them in your policy. |

| Does Homeowners Insurance Cover Sewer Backup? | Why this devastating event is almost always excluded from standard policies and how the water backup endorsement works. |

| Does Homeowners Insurance Cover Other Structures? | How Coverage B applies to fences, detached garages, and sheds, including the strict 10% limit. |

| Does Homeowners Insurance Cover Theft? | Navigating Coverage C for stolen items, understanding vandalism limits, and dealing with off-premises theft. |

| Homeowners Insurance Personal Property Coverage | A detailed look at sub-limits for high-value items like electronics and jewelry, and the impact of ACV vs RCV on belongings. |

| Homeowners Insurance Loss of Use Coverage | How Coverage D pays for your hotel and food when displaced, what qualifies as “additional,” and how to access the funds. |

❓ FAQ

🏠 What exactly does homeowners insurance cover?

A standard policy covers damage to your home’s structure, detached structures, personal belongings, and living expenses if you are displaced, provided the damage is caused by a covered sudden and accidental peril (like fire or wind).

🌧️ Is water damage covered by standard home insurance?

It depends on the source. Sudden, internal water damage (like a burst pipe) is typically covered. Gradual leaks over time and external flooding from nature are almost always excluded.

🛠️ Does my home insurance cover a new roof?

If your roof is damaged by a sudden covered event like a severe windstorm, hail, or a falling tree, it is covered. If it simply needs replacing due to old age and normal wear and tear, it is not covered.

🚽 Does homeowners insurance cover plumbing issues?

Insurance generally covers the collateral damage caused by a sudden plumbing failure (e.g., ruined drywall from a burst pipe), but it rarely pays to repair the actual plumbing pipe that failed due to age or corrosion.

🍄 Does home insurance cover mold removal?

Mold is typically covered only if it is the direct result of a sudden, covered water event (like a burst pipe). Mold from chronic humidity or long-term gradual leaks is excluded. Mold coverage often has strict sub-limits.

🧱 Does home insurance cover foundation cracks?

Usually no. Foundation damage is almost always categorized as gradual settling, earth movement, or hydrostatic pressure, all of which are standard policy exclusions.

🤺 Are fences covered by home insurance?

Yes, fences are covered under Coverage B (Other Structures) against covered perils like wind or fire. However, coverage is typically capped at a percentage (usually 10%) of your main dwelling coverage limit.

📑 What is the difference between HO3 and HO5?

An HO3 policy covers your dwelling for all perils unless excluded, but covers personal property only for specifically named perils. An HO5 policy provides broader protection, covering both dwelling and personal property for all perils unless explicitly excluded.

⚖️ Does homeowners insurance cover personal liability?

Yes. Although primarily for property damage, standard policies include Coverage E (Personal Liability), which protects you if someone is injured on your property and sues you, or if you accidentally damage someone else’s property.

🔎 How do I know if my specific damage is actually excluded?

Do not just rely on the adjuster’s verbal explanation. You must read your policy’s Declarations Page and the specific wording in the “Exclusions” section. If the facts of your damage do not match the exact wording of the exclusion cited in your denial letter, you should have a professional review your claim to challenge the decision.

From filing to settlement: the parts worth understanding before something goes wrong.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

These cover the situations where professional help most often changes the outcome.

- 5 patterns that signal your settlement is probably short

- Who the adjuster at your door actually works for

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When a denial needs legal leverage, not just negotiation

- Four paths to fight a denial, including one most homeowners miss

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.