- Standard homeowners insurance is designed for sudden, accidental events, which means predictable issues (like normal wear and tear) and systemic risks (like regional floods) are almost always excluded.

- Many common homeowner nightmares, such as sewer backups, slow pipe leaks, and foundation settling, fall under standard exclusions, but some can be covered by purchasing specific endorsements.

- A claim denial based on an exclusion is heavily dependent on how the insurance adjuster categorizes the damage; mischaracterizing a sudden event as “gradual damage” is one of the most common reasons valid claims are denied.

The Reality of Your Policy Language

Your homeowners insurance policy is likely much longer than you think, and it covers significantly less than you might assume. In my years reviewing property claims, I have noticed a recurring pattern: most homeowners only discover the true boundaries of their coverage after they have filed a claim and received a denial letter.

We pay our premiums expecting a safety net that catches everything. However, insurance contracts are highly specific documents. They do not cover “damage” in a broad sense; they cover specific perils under specific conditions. When you understand exactly what the common homeowners insurance exclusions are, you stop being surprised by the process and start making better decisions about how to document your property and protect your financial interests.

I am going to walk you through the standard homeowners insurance exclusions list, not just to tell you what is not covered, but to explain exactly why these lines are drawn. More importantly, I will share how these exclusions are applied in the real world when an adjuster is standing in your living room.

Why Do Standard Homeowners Insurance Exclusions Exist?

To understand what is not covered by homeowners insurance, it helps to understand how insurance companies price risk. If a policy covered absolutely everything that could possibly go wrong with a house, the annual premium would be completely unaffordable for the average family.

To keep premiums manageable, actuaries exclude risks that fall into three main categories:

- 🏠 Controllable Risks: Things you, as the homeowner, are expected to prevent through basic maintenance (like fixing a slow drip before it rots the floor).

- 🌊 Systemic Risks: Events that destroy thousands of homes at the exact same time, bankrupting an insurance pool (like regional flooding or earthquakes).

- 💣 Uninsurable Risks: Events that violate public policy or are entirely intentional (like setting fire to your own property).

When you view your policy through this lens, the standard homeowners insurance exclusions start to make logical sense, even if they are frustrating to deal with during a crisis.

The Exclusion Review Checklist (Before You Have a Claim)

Based on my experience, the best time to understand your exclusions is long before a disaster hits. I highly recommend grabbing your policy jacket tonight and checking these three specific details so you are not caught off guard later:

- Find the actual “Exclusions” header: Read the exact list of excluded perils in the main policy booklet. Do not rely on the summary Declarations page, as it only shows coverage limits, not the fine print.

- Check for “Water Backup”: Look specifically for a “water backup and sump overflow” endorsement. If you do not see it explicitly listed, you do not have it.

- Identify your vacancy timeline: Check how many consecutive days your home can be empty before coverage is automatically suspended (this is usually 30 or 60 days).

Category 1: Weather and Geological Exclusions

When severe weather strikes, the exact source of the damage determines your coverage. Standard policies exclude broad, systemic earth and water movements. If you want a complete picture of the baseline coverage before looking at these exceptions, I highly recommend reviewing exactly what standard homeowners insurance covers first.

Flood and Surface Water

This is perhaps the most misunderstood exclusion in the entire industry. Standard home insurance policy exclusions universally apply to “flood,” which the industry defines strictly as external water rising and affecting normally dry land. If a river overflows, a storm surge hits, or heavy rain causes groundwater to pool and enter your basement, it is excluded.

A common field observation: Homeowners frequently use the word ‘flood’ when reporting a burst pipe to their agent (‘My kitchen is flooded!’). I always advise against using this word for internal plumbing failures. While a good adjuster knows the difference, using the word ‘flood’ on your initial claim intake can trigger automatic delays while the carrier investigates for an excluded peril.

Earthquake, Sinkholes, and Earth Movement

In my experience reviewing catastrophic claims, homeowners are often shocked to learn that if the ground shakes, sinks, or slides, standard policies simply do not apply. Earthquakes, landslides, and mudflows are entirely excluded. Sinkholes are also excluded in most states. Coverage availability varies significantly by region (for example, Florida has specific legislative requirements), so you must proactively ask your local agent about adding this protection.

Category 2: The Maintenance and “Gradual Damage” Trap

While natural disasters grab the headlines, the most common coverage disputes I see actually stem from everyday maintenance issues. This category causes more claim denials than any other. Insurance is designed to cover the sudden and accidental. It is not a home warranty. If damage occurs slowly over time, the carrier expects you to have noticed and fixed it before it became a major issue.

Wear and Tear / Gradual Leaks

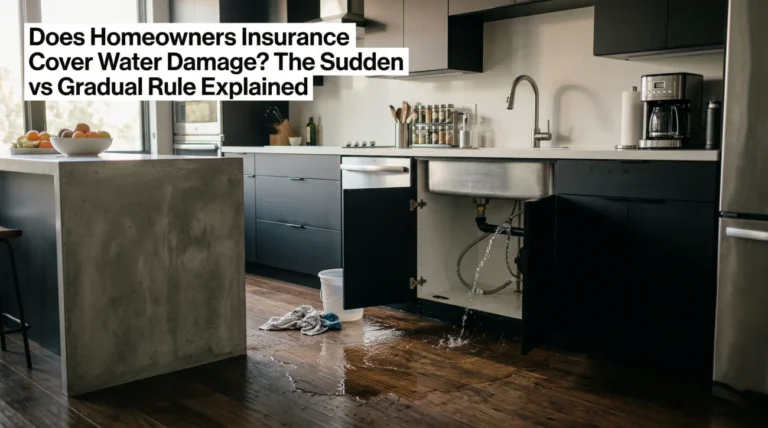

If a pipe suddenly bursts while you are sleeping, the resulting water damage is generally covered. However, if a pipe under your kitchen sink has been dripping a few ounces of water a day for six months, rotting the cabinetry and the subfloor, that is considered gradual damage. The surprising things homeowners insurance doesn’t cover almost always trace back to this “duration” timeline.

Telling the adjuster, “This pipe has been leaking for a few weeks, but it just got really bad yesterday.” You have just handed them a gradual damage exclusion on a silver platter.

Sticking strictly to the facts of when you discovered the damage: “I walked into the kitchen on Tuesday morning and found the water.” Let the physical evidence speak for itself.

Mold, Rot, and Fungus

Mold coverage is entirely dependent on causation. Standard policies exclude mold that arises from chronic humidity, lack of ventilation, or long-term seepage. It is important to note that if mold results directly from a sudden, covered event, like a pipe burst, it may be covered up to a specific sub-limit. However, the baseline rule for general mold growth is a firm exclusion.

Pest Damage (Termites, Rodents, and Insects)

I have sat at kitchen tables with homeowners devastated by termite damage, but I have never seen a standard policy that covers it. Pest damage is universally viewed as a maintenance issue. The rationale is that a homeowner should schedule regular pest inspections and interventions before the structural integrity of the home is compromised.

Category 3: Infrastructure and System Failures

Beyond everyday maintenance, your home is also connected to larger infrastructure grids. When those systems fail, the resulting damage often falls into a coverage gap that catches homeowners completely off guard.

Sewer and Drain Backup

I regularly see claims where a city’s main sewer line backs up and pushes raw sewage through basement drains. Unfortunately, standard homeowners insurance coverage exclusions apply here. Because the failure originated off your property in a municipal system, the standard policy will not cover the devastating cleanup. You must have a specific “water backup and sump overflow” endorsement for this.

Foundation Settling and Cracking

Over the years, houses settle. Soil expands and contracts. This causes foundation cracks, sticking doors, and uneven floors. Because this is a natural geological and physical process, foundation damage is almost always excluded unless it is the direct, immediate result of a covered peril (like a vehicle crashing into your house).

Power Surges from the Grid

If lightning strikes your home directly and fries your electronics, that is usually covered. However, if the local power company experiences a grid fluctuation that sends a surge into your home and destroys your HVAC system and appliances, that is typically excluded under the “power failure off-premises” clause.

Category 4: Behavioral and Contractual Clauses

Infrastructure failures are largely out of your control. However, some things not covered by homeowners insurance are based entirely on your own actions or how the home is used and left unattended.

The Vacancy Clause

If you leave your home unoccupied for an extended period (typically 30 to 60 consecutive days depending on the policy), coverage for perils like vandalism, glass breakage, and sometimes water damage is suspended. Insurers know that an empty house is a target for thieves and that a small leak in an empty house will become a massive disaster before anyone notices.

💡 Pro Tip: If you are remodeling, traveling for months, or dealing with an estate property, you must purchase a “vacant home” endorsement or policy. Do not assume your standard coverage remains intact. For more on how policies treat different living situations, revisiting our guide on what standard policies cover is a helpful next step.

Intentional Damage and Neglect

If you intentionally set fire to your home, obviously, it is not covered. But this exclusion also extends to severe neglect. If a tree falls and puts a hole in your roof, the initial damage is covered. However, if you leave that hole uncovered for two months and rain ruins the interior of the house, the insurer will deny the interior damage under the “failure to protect property from further damage” clause.

If you discover a sudden issue, you are contractually obligated to mitigate further damage immediately to protect your coverage. We will look at exactly how to document and handle this process in the first 24 hours section below.

A Quick Note on Sub-Limits

While not outright exclusions, sub-limits function exactly like hidden exclusions for your most valuable possessions. Standard policies place severe payout caps on items like jewelry, firearms, and electronics if they are stolen. For a full breakdown of these categories, I highly recommend reviewing our complete guide to personal property coverage limits.

What to Do in the First 24 Hours to Prevent an Exclusion Denial

How you act in the immediate aftermath of a sudden event can make the difference between a paid claim and an exclusion denial. I always advise homeowners to follow a strict documentation protocol right from the start:

- Video the active source: If a pipe bursts, take a video of the water spraying before you shut the main valve off. This proves visually that the event was sudden and catastrophic, not a slow drip.

- Keep the broken part: Never throw away the ruptured hose, cracked fitting, or broken supply line. The adjuster needs to see the physical evidence to verify causation and rule out gradual wear and tear.

- Watch your words on intake: Do not guess what happened on the initial phone call with the carrier. Stick strictly to the visible facts (“I walked into water in my kitchen at 8 AM”) and avoid using loaded terms like “flood,” “seepage,” or “rot.”

Closing the Gaps: The Endorsement Landscape

The good news about the homeowners insurance exclusions list is that you can buy back coverage for many of these risks. These add-ons are called endorsements or riders.

| Common Exclusion | The Coverage Solution | Estimated Annual Cost |

|---|---|---|

| Sewer and Drain Backup | Water Backup Endorsement (Highly Recommended) | $50 – $150 |

| Flood and Surface Water | Separate NFIP or Private Flood Policy | $500 – $1,200+ |

| Earthquake | Earthquake Policy or Endorsement | $100 – $300 (Varies widely) |

| Off-Premises Power Surge | Equipment Breakdown Endorsement | $25 – $50 |

PAIN SECTION: When Exclusions Are Misapplied to Your Claim

Understanding policy exclusions is one thing; dealing with an insurance adjuster who applies them incorrectly is another entirely. This is where the claims process becomes incredibly frustrating for homeowners.

Because exclusions like “gradual damage” and “wear and tear” save insurance companies millions of dollars, adjusters are trained to look for them. In many cases, a completely valid, sudden accidental event gets mischaracterized by an overworked or aggressive adjuster to fit an exclusion profile.

Signs that an exclusion may have been misapplied to your claim include:

- Your damage resulted from a sudden, specific event (like a pipe bursting on a Tuesday), but the denial letter cites a “gradual maintenance” exclusion.

- Wind tore off your shingles, allowing rain in, but the adjuster cites the “flood” or “surface water” exclusion for the interior damage.

- The adjuster makes a determination that damage is “long-standing” without cutting into drywall or properly inspecting the hidden source of the issue.

- The exclusion cited in your denial letter does not actually appear in the specific policy language provided in your declarations package.

If you are holding a denial letter and the cited exclusion does not match the reality of how the damage occurred in your home, you have a characterization dispute. The adjuster has categorized your damage in a way that benefits the carrier. Overcoming this requires operational claims experience to push back on their specific categorizations.

This is precisely when getting a second set of eyes on the adjuster’s scope and damage characterization from a licensed public adjuster can turn a wrongful denial into a paid claim. A professional can document the forensic evidence needed to prove the event was sudden and accidental. Furthermore, if you believe the insurer is intentionally misrepresenting policy language to avoid a large payout, it may be time to consider consulting an attorney to review the bad faith implications of the denial.

If you find yourself in this situation, here is a template you can use to demand clarity from your adjuster regarding the applied exclusion:

Hello [Adjuster Name],

I received the denial letter dated [Date] citing the “gradual damage” exclusion. Because the water event occurred suddenly on [Date of Loss] when the supply line ruptured, I do not understand how this exclusion applies to my specific loss. Please provide the exact policy language you are relying on, along with the specific physical evidence from your inspection that led you to categorize this sudden failure as gradual.

Thank you,

[Your Name]

Final Thoughts on Protecting Your Claim

Exclusions are a rigid, permanent part of every property insurance contract. You cannot negotiate them away after a loss happens. However, you absolutely can and should challenge how an adjuster attempts to squeeze your legitimate damage into an excluded category.

The best defense against a misapplied exclusion is meticulous documentation. If a pipe bursts, take video immediately. Show the sudden volume of water. Show the broken material. Keep the broken part. Do not give the carrier room to imagine a slow, gradual timeline where a sudden, catastrophic one actually exists.

❓ FAQ: Common Questions About Policy Exclusions

💧 Is water damage from rain covered by homeowners insurance?

In claims I’ve reviewed, it depends on how it enters. If rain enters through a sudden opening caused by a covered peril (like wind blowing off shingles), it is usually covered. If it seeps in gradually through an old, worn-out roof, it is excluded.

🚽 Does homeowners insurance cover plumbing issues?

In the claims I handle, standard policies generally cover the water damage caused by a sudden plumbing failure, but they do NOT cover the cost to repair or replace the actual plumbing pipe or fixture that failed. That is considered a maintenance expense.

🐶 Does homeowners insurance cover damage done by pets?

Based on my experience, damage caused by your own pets (like a dog chewing baseboards or tearing up carpet) is excluded under almost all standard policies. However, liability coverage may protect you if your dog bites someone else.

🔌 What is not covered when appliances break down?

From what I see in the field, mechanical breakdown of appliances (like a refrigerator simply stopping working due to age) is excluded. However, if the appliance suddenly leaks and ruins your floor, the resulting water damage to the floor is typically covered.

🌳 If a tree falls on my house, is it covered?

Usually, yes, if it falls due to a storm or wind. However, if the tree was dead, rotting, and you ignored it for years before it fell, the insurer might attempt to deny the claim based on negligence and maintenance exclusions.

❄️ Are frozen pipes covered?

Typically yes, but only if you maintained heat in the building. If you went on vacation in winter, turned the heat completely off, and the pipes froze and burst, the resulting damage will likely be denied due to negligence.

🧱 Does homeowners insurance cover foundation repair?

Almost never. Foundation settling, cracking, and shrinking are considered natural, gradual geological processes and are standard exclusions on home policies.

🦠 Is black mold covered by insurance?

Mold is excluded unless it is the direct result of a covered peril, like a sudden burst pipe. Even then, most policies have strict sub-limits capping mold remediation payouts at $5,000 to $10,000.

⏱️ How long does an exclusion dispute take?

In the claims I’ve managed, a dispute over an applied exclusion can add weeks or even months to your timeline. If the carrier digs in, escalating to a public adjuster or an attorney is usually the most efficient way to force a resolution.

📜 How do I find out what my specific exclusions are?

You need to read the “Exclusions” section of your actual policy jacket, not just the Declarations Page. It is usually a specifically labeled section detailing perils that are unconditionally not covered.

Knowing what is covered is step one. These explain what happens from there.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

These cover what to do when the offer does not match what your policy says.

- 5 patterns that signal your settlement is probably short

- Who the adjuster at your door actually works for

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When a denial needs legal leverage, not just negotiation

- Four paths to fight a denial, including one most homeowners miss

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.