- Standard homeowners insurance covers water damage if it is sudden and accidental, such as a burst pipe or a washing machine hose rupturing.

- Gradual water damage, like a slow plumbing leak that occurs over weeks or months, is almost always excluded because insurers view it as a maintenance issue.

- The coverage decision often comes down to the adjuster’s characterization of the damage; keeping broken parts and detailed plumber reports is critical to proving your loss was sudden.

The Coverage Reality of Water Damage

Most homeowners assume that if water damages their home, their insurance policy will automatically cover the repairs. It is a logical assumption. Water destroys drywall, ruins flooring, and damages personal property regardless of where it came from. But from the perspective of an insurance carrier, the visual damage is secondary. What actually matters is exactly how the water escaped in the first place.

In my years reviewing water damage claims and reading through adjuster reports, I have seen homeowners devastated not just by the physical destruction of their property, but by the denial letter that follows. Water damage is the most common type of home insurance claim, yet it is also the most frequently misunderstood. The confusion usually stems from a single line in standard policy language regarding time and maintenance.

If you are standing in a wet kitchen right now, or if you recently filed a claim and are waiting for an adjuster’s decision, you need to understand the fundamental rule that governs water claims. It is not about the severity of the flood in your living room. It is entirely about the timeline of the leak.

Key Point: Standard homeowners insurance covers water damage, but only when the event is sudden, accidental, and originates from an internal source. Gradual deterioration is almost universally excluded.

The Core Rule: Sudden vs. Gradual Damage

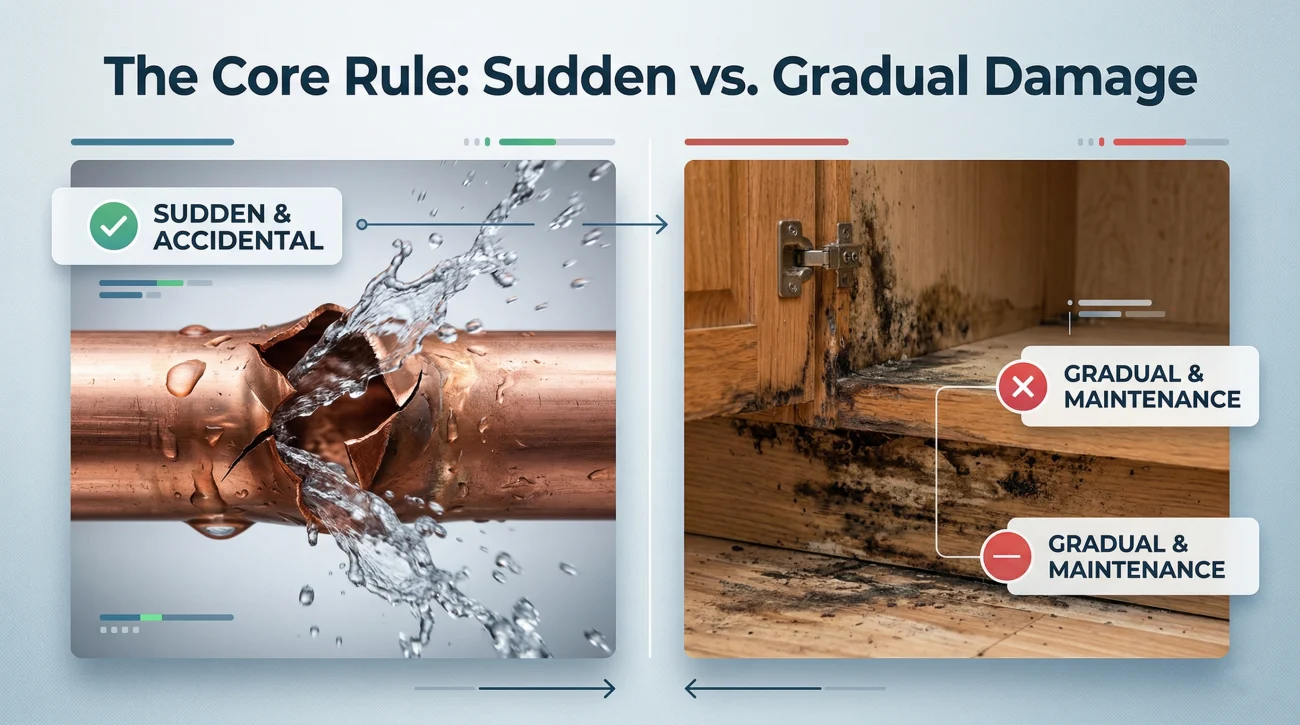

To understand whether your specific water damage is covered, we have to look at how insurance companies classify risk. Homeowners insurance is designed to protect you against unpredictable, instantaneous disasters. It is not designed to function as a home warranty or a maintenance policy.

This philosophy creates the “sudden and accidental” rule. If a water event happens instantly and without warning, the resulting damage is typically covered.

What Counts as Sudden and Accidental?

Sudden water damage events are usually obvious. You are sitting in your living room, you hear a loud pop from the kitchen, and suddenly water is rapidly pooling across the floor. There was no warning, and there was nothing you could have done to prevent it in that exact moment.

Common examples of sudden water damage that standard policies typically cover include:

- ✅ A frozen supply pipe that bursts inside a wall during a winter storm.

- ✅ A braided steel washing machine hose that ruptures under pressure.

- ✅ A water heater tank that suddenly splits open.

- ✅ A toilet that overflows unexpectedly, sending water through the bathroom floor.

- ✅ An ice dam on your roof that suddenly forces melting snow under the shingles and into your ceiling.

In these scenarios, the damage to your home (the floors, the drywall, the baseboards) is covered. However, it is important to note a crucial distinction: the insurance company will pay to fix the damage the water caused, but they will not pay to fix the broken item itself. You will have to pay the plumber to replace the actual burst pipe or buy a new water heater out of your own pocket.

Why Slow Leaks Lead to Denied Claims

The most common reason for a denied water claim is the gradual damage exclusion. If a pipe under your kitchen sink drips slowly for three months, quietly rotting the cabinet base and soaking into the subfloor, standard policies will almost always exclude the claim based on it being a maintenance failure.

This is not theoretical — here is exactly what adjusters are trained to look for in the field when investigating a leak:

“A common field observation I make when reviewing denied claims is the presence of heavy rust, dry rot, or established mold around a pipe fitting. Adjusters are specifically trained to look for these visual markers. If an adjuster photographs thick rust on a water valve, they will use that photo to justify a gradual damage denial, arguing the leak existed long before the homeowner reported it.”

What Counts as Gradual Damage?

Gradual damage is often insidious because you may genuinely not realize it is happening until the damage becomes severe. Excluded gradual water damage typically includes:

- ❌ A refrigerator water line that has been weeping slowly behind the appliance for weeks.

- ❌ A shower pan that has been slowly leaking into the ceiling below for several months.

- ❌ Water seeping through foundation cracks during heavy rainfalls over the years.

- ❌ A roof leak that has been slowly dripping into the attic space over multiple seasons.

- ❌ Faucet drips that eventually destroy the vanity cabinet.

⚠️Warning: The presence of mold is often used by adjusters as an indicator of gradual damage. Mold typically takes at least 24 to 48 hours to begin forming. If an adjuster arrives on day two of a claim and sees heavy, established mold growth, they will likely conclude the water has been present much longer than you realized. You can read more about how this specific issue is handled in our guide on does homeowners insurance cover mold.

The “You Should Have Known” Problem

When the line between sudden and gradual is blurred, insurers often use the “you should have known” argument. They will deny claims by arguing that even if you did not actually know about the leak, a reasonable person would have noticed the signs.

For example, if the drywall on your living room ceiling has been showing a brown water stain that slowly grew over two months before the ceiling finally collapsed, the insurer will likely deny the claim. They will argue that the visible stain was your warning to investigate and mitigate the problem.

Noticing a small drip under the sink, placing a bucket under it, emptying the bucket occasionally, and waiting until the pipe completely fails a month later to call insurance.

Shutting off the main water supply the moment you notice a leak, calling a plumber immediately to fix the source, and drying out the area to prevent secondary damage.

Your policy includes a “duty to mitigate” clause. This means you are contractually obligated to take reasonable steps to protect your property from further damage after a loss occurs. Failing to stop a known leak violates this duty, and the consequence is severe: the insurer can use this violation to completely deny the entire claim, not just the secondary damage that happened after you discovered the leak.

The Overlapping Damage Scenario

One of the most complex situations I encounter is when new, sudden damage overlaps with old, existing damage. Imagine you had a minor roof leak last year that left a small, dry yellow stain on your ceiling. You never filed a claim. Today, a pipe bursts in the ceiling directly above that exact same spot, bringing down the drywall.

When the adjuster arrives, they will see the old yellow stain around the edges of the new break. Frequently, they will use that old stain to characterize the entire new event as an ongoing, gradual issue, denying the whole claim.

This is where your documentation becomes vital. You must be able to distinctly separate the new, sudden event from any old cosmetic issues. This leads directly to why your plumber’s paperwork is so important.

The Critical Role of the Plumber’s Report

Because the coverage decision hinges entirely on the timeline, your plumber is the most important person in your claim process. The insurance adjuster will want to know exactly what failed and why.

In my experience, a generic $200 plumbing invoice can single-handedly sink a $30,000 mitigation claim. If your plumber simply hands you an invoice that says, “Fixed leak in kitchen,” you are leaving the door wide open for the adjuster to assume the worst.

💡 Pro Tip: Always instruct your plumber to save the broken parts (the ruptured hose, the split valve) and leave them on the counter for the insurance adjuster to inspect. Physical evidence of a sudden rupture is the best defense against a gradual damage denial.

When you hire a plumber for an emergency water event, ask them to write a detailed diagnostic report on their invoice. Here is an example of what you want to see.

Sample Plumber Diagnostic Note:

Responded to emergency call. Found catastrophic failure of 1/2 inch copper supply line to hall bathroom toilet. Metal pipe split longitudinally due to sudden pressure fluctuation. No evidence of prior pinhole leaks, rust, or long-term weeping. Pipe failure was instantaneous. Replaced section of pipe and restored water service. Left failed pipe section on site for homeowner.

External Water and Specific Exclusions

Up to this point, we have been discussing water that originates from inside the home. But what happens when water enters from the outside? The rules change dramatically.

Flood Water is Always Excluded

Standard homeowners policies do not cover flood damage. In insurance terms, a “flood” has a very specific definition: it is a general and temporary condition of partial or complete inundation of two or more acres of normally dry land area, or of two or more properties. This means rising groundwater, overflowing rivers, and storm surges are excluded. We explain this distinction in detail in our comparison of flood vs water damage insurance.

Sewer and Drain Backup

If water backs up into your home through the municipal sewer lines or a blocked floor drain, your standard policy will likely deny the claim. Coverage for this specific nightmare scenario requires a dedicated add-on. See our detailed guide on does homeowners insurance cover sewer backup to understand how this endorsement works.

| Source of Water | Is it Typically Covered? | Requirements |

|---|---|---|

| Burst supply pipe in wall | Yes | Must be sudden and accidental. |

| Slow drip under kitchen sink | No | Considered a maintenance failure. |

| Rain entering a sudden roof hole | Yes | Roof must have been damaged by a covered peril (like wind). |

| Rising river water | No | Requires a separate NFIP or private flood policy. |

| Sewage backing up into tub | Depends | Requires a specific water backup endorsement. |

When Your Coverage is Mischaracterized

Understanding the rules is one thing, but dealing with how those rules are applied is another. This brings us to the most frustrating phase of the process: what happens when you know the water damage was sudden, but your insurance company sends a letter denying the claim based on “gradual wear and tear”?

I frequently review cases where a homeowner reports a sudden appliance failure, but the adjuster conducts what feels like an interrogation. They will ask questions like, “Are you sure you didn’t notice a drop in water pressure last week?” or “How often do you check behind this washing machine?” They are actively building a timeline to justify a gradual exclusion.

Signs your water damage denial or low offer may reflect a coverage mischaracterization include:

- 🛑 Your damage was from a specific sudden event (like a burst pipe while you were at work) but the denial letter cites gradual damage.

- 🛑 The insurer is applying a flood exclusion to water that clearly originated from an internal plumbing source.

- 🛑 The adjuster’s report characterizes recent sudden damage as long-standing without any supporting physical evidence or plumber’s documentation.

- 🛑 Your policy explicitly has a hidden water damage endorsement, but the claim for a behind-the-wall leak was denied as gradual anyway.

If your claim is stalled because the adjuster is labeling a sudden loss as a maintenance issue, you must challenge that characterization in writing. You can use a structured request to demand evidence for their decision.

Subject: Request for Clarification of Denial Basis – Claim #[Your Claim Number]

Dear [Adjuster Name],

I am in receipt of your letter dated [Date] denying coverage for my water damage claim based on a gradual damage exclusion. I disagree with this characterization of the loss.

The damage was caused by a sudden rupture of the [specific pipe/appliance] which occurred on [Date]. I have attached the diagnostic report from my licensed plumber confirming that this was a sudden mechanical failure, not a long-term leak.

Please provide the specific evidence, photographs, and policy language your team relied upon to determine this was a gradual event. I request that my claim file remain open while this documentation is reviewed.

Sincerely,

[Your Name]

Whether your damage qualifies as sudden vs. gradual is not always a clear-cut factual question. It is often a professional interpretation made by the insurance company’s representative. If that characterization does not match the actual events that took place in your home, the denial may be entirely challengeable.

If you are trapped in a dispute over how the leak is being classified, or if the settlement offered is suspiciously low due to these disputes, exploring your options for getting a second set of eyes on the scope and coverage determination from a licensed public adjuster can clarify whether the exclusion was applied fairly.

From Coverage to Payout: Your Next Steps

Dealing with water damage requires fast action. The first 48 hours dictate how smoothly the rest of the insurance process will go. If you have just discovered water, your immediate priorities are to stop the source, photograph the standing water, save the broken parts, and get a written plumber diagnostic.

Note: Just because a water claim is “covered” does not mean your insurer will pay the full amount you need to rebuild. Coverage is only the first step. The settlement amount will depend heavily on whether your policy pays Actual Cash Value (ACV) or Replacement Cost Value (RCV) for damaged materials.

Once you clear the coverage hurdle, the battle shifts to scope and pricing. The adjuster may agree to replace your drywall but refuse to replace the continuous flooring that runs into the next room, or they may apply heavy depreciation to your damaged property. Winning the coverage argument is just the beginning of the claim journey. Understanding how these specific repair disputes are processed, how adjusters calculate depreciation, and when to push back will help set your expectations and protect your final payout. You can learn exactly how to navigate the next phase and maximize your settlement in our complete guide to home insurance claims by damage type.

❓ FAQ

🗑️ What if my plumber already threw away the broken pipe?

If the physical evidence is gone, rely heavily on the plumber’s written invoice. Ask them to rewrite it if necessary to explicitly state that the failure was sudden and not due to long-term wear or rust.

🧳 Is water damage covered if my home was vacant or I was on vacation?

This is tricky. Most standard policies have a “vacancy clause” that denies water damage if the home was unoccupied for more than 30 to 60 consecutive days, or if you failed to maintain heat in the building to prevent freezing pipes.

💧 Will insurance pay the water mitigation company directly?

If you sign an “Assignment of Benefits” (AOB) or a “Direction to Pay,” the insurer can pay the mitigation company directly. Be cautious with AOBs, as you may lose control over your claim funds.

💰 Does ACV or RCV apply to my water-damaged floors?

It depends on your policy. If you have an RCV policy, they will eventually pay the full cost of new floors, but they will likely issue the first check at ACV (depreciated value) and pay the rest after repairs are complete.

🛠️ If water ruins half my kitchen flooring, will they replace the whole floor?

This is known as a “matching issue.” Depending on your specific policy language, the insurer may be required to replace the continuous flooring to ensure a uniform appearance, but they will often try to patch it first.

🔍 Should I tear open the wet drywall myself to find the leak?

Only do the minimum necessary to stop the leak. Document everything before you cut. Insurers refer to finding the leak as “tear out to access,” and they typically cover the cost of opening and repairing the wall to get to the burst pipe.

⏳ How long do I have to file a water damage claim?

Most policies require you to report the loss “promptly” or “as soon as practical.” In the case of water damage, waiting even a few days can lead to a denial based on failure to mitigate or mold growth.

📉 How does the deductible work in a water claim?

You do not pay the deductible upfront to the insurance company. Instead, they subtract your deductible amount from your final settlement check. You then use that check, plus your own deductible money, to pay your contractors.

🏚️ If I have an old leak stain, will it void a new claim in the same spot?

It shouldn’t void the new claim, but adjusters will often try to blend the two events to deny it as gradual. You must provide strong proof (like plumber notes) separating the new, sudden burst from the old, unrelated stain.

📝 Does it matter if the insurance company sends an independent adjuster?

Independent adjusters are contractors hired by the insurance company during busy times. While they don’t work directly for the carrier, they still represent the carrier’s interests and guidelines, not yours. Document everything they say and do.

Knowing what is covered is step one. These explain what happens from there.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

These cover what to do when the offer does not match what your policy says.

- 5 patterns that signal your settlement is probably short

- Who the adjuster at your door actually works for

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When a denial needs legal leverage, not just negotiation

- Four paths to fight a denial, including one most homeowners miss

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.