- Mold coverage is based entirely on causation. The mold itself is not a covered event, but if it resulted from a sudden, covered peril (like a burst pipe), it may be covered.

- Gradual water damage, slow leaks, and poor ventilation are the most common reasons mold claims are denied.

- Even when mold is covered, standard homeowners policies often enforce strict sub-limits, typically capping remediation payouts between $5,000 and $10,000.

- How your insurance adjuster documents the source of the water during their initial inspection will determine whether your mold claim is approved or denied.

The Reality of Finding Mold in Your Home

Finding mold spreading across your drywall or blooming under your floorboards is a terrible moment for any homeowner. The immediate panic about health and safety is quickly followed by a stressful financial question: does homeowners insurance cover mold? In my years of reviewing hundreds of property files and sitting across the table from adjusters, I have seen homeowners assume that because mold is dangerous and expensive to remove, their policy will automatically pay for the cleanup.

Unfortunately, standard property insurance does not work that way. Mold coverage is easily one of the most misunderstood areas of homeowners insurance. The confusion rarely stems from the complexity of the policy language, but rather from the fact that insurance companies do not look at how bad the mold is. They only look at what caused it.

I have reviewed hundreds of denial letters, and the pattern is remarkably consistent. Homeowners file a claim for mold, and the insurance company denies it by pointing to a maintenance exclusion. To navigate this process, you must understand how your adjuster is evaluating your property. The decision to pay or deny your claim hinges on a concept called the causation rule. Once you understand this rule, you will know exactly how to approach your situation before you even pick up the phone to call your carrier.

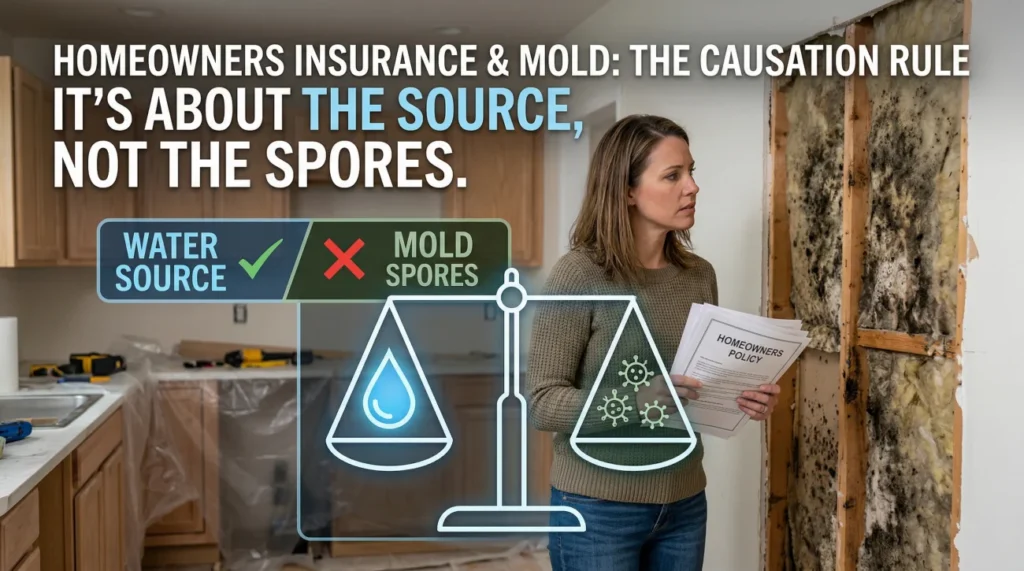

The Causation Rule: It Is About the Source, Not the Spores

When you read through understanding what standard homeowners insurance policies include, you will notice that mold is usually listed in the exclusions section. However, there is a massive exception to that exclusion. The causation rule dictates that mold is only covered if it is the direct result of a covered peril.

In the insurance world, the mold itself is never the covered event. The underlying event that allowed the water to escape and feed the mold is what matters. If that underlying event is covered, the resulting mold is generally covered as a consequence.

Key Point: Do not file a claim by simply telling your insurance company you have a mold problem. You must file a claim for the sudden water event that caused the mold to grow.

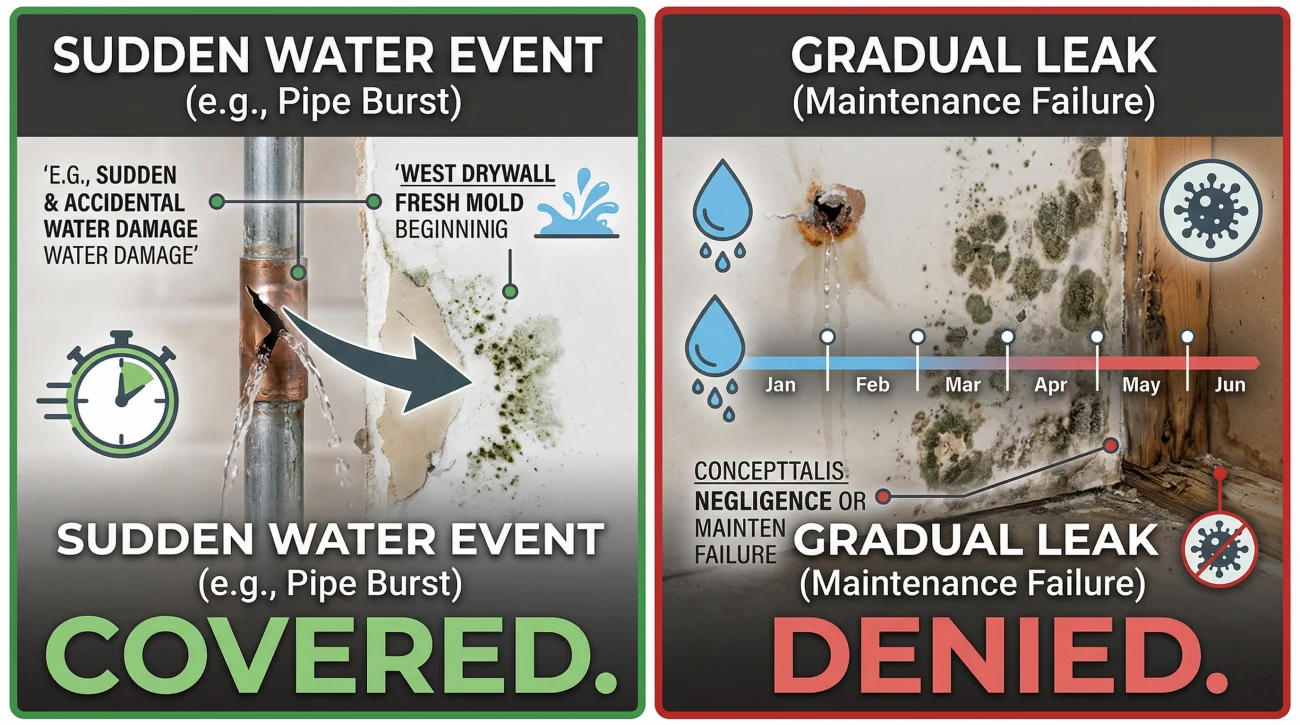

If a tree falls on your roof during a violent storm, tearing a hole that lets rainwater pour into your attic, the storm is the covered peril. If mold grows on the attic trusses three days later before the contractor can dry it out, that mold is covered because the storm is covered. On the other hand, if your attic develops mold because your bathroom exhaust fan has been venting humid air into the space for five years, there is no sudden covered peril. That claim will be denied as a maintenance failure.

“I recently reviewed a file where a homeowner reported ‘black mold under the kitchen sink’. The claim was instantly flagged for denial. If they had reported the ‘sudden rupture of the dishwasher supply line’ which happened two days prior, the resulting mold would have been viewed entirely differently by the desk adjuster.”

When Does Homeowners Insurance Actually Cover Mold?

To get a mold claim approved, you have to prove that the water source was sudden, accidental, and internal. Insurance carriers operate on the premise that sudden events are unpredictable and therefore insurable. Let us look at the most common scenarios where mold remediation is typically covered by a standard policy.

Sudden Pipe Bursts and Appliance Failures

The classic example of covered mold is a burst plumbing supply line. If a pressurized water pipe ruptures behind your drywall while you are away at work, the resulting flood is sudden. If water sits in the wall cavity and mold begins to colonize before the dry-out team can fully remove the moisture, this is generally covered. The same logic applies to sudden appliance failures, such as a washing machine hose splitting open or a water heater failing catastrophically and emptying its tank into your basement.

Sudden Roof Damage from Storms

If high winds rip shingles off your roof, or a flying branch punctures the decking, rainwater entering the home is covered. Any mold that develops from that specific intrusion, before reasonable repairs could be made, will typically fall under the coverage umbrella of the initial windstorm peril.

💡 Pro Tip: Mold can germinate extremely fast under the right conditions. If you experience a sudden water event, document the timeline aggressively to prove the mold is newly formed from this specific event, rather than a long-standing issue.

Why Most Mold Claims Get Denied: The Gradual Damage Trap

The vast majority of mold claims are denied, and they almost always fail the sudden and accidental test. Insurers expect homeowners to maintain their properties. If water has been leaking slowly over a long period, the carrier will argue that a reasonable homeowner should have noticed the issue and fixed it before mold could establish a heavy presence.

Slow Leaks and Seepage

A pinhole leak in a supply line that drips one drop every ten minutes for six months will absolutely cause massive mold growth inside a wall cavity. However, because the leak was gradual, standard policies will exclude it. The insurance company classifies this as a maintenance issue. The damage to the pipe, the water damage to the drywall, and the resulting mold will all be denied.

Poor Ventilation, Ductwork, and Chronic Humidity

Mold growing on bathroom ceilings due to hot showers, or spreading through HVAC ductwork due to chronic condensation, is rarely covered. There is no sudden event to point to. This is strictly an environmental control issue, and insurance policies do not act as home maintenance warranties.

External Flooding and Groundwater

Standard homeowners insurance strictly excludes external flood water. If a river overflows, or heavy rain causes surface water to run into your basement, any resulting mold is not covered by your standard policy. You would need a separate National Flood Insurance Program (NFIP) policy or a private flood policy to have a chance at coverage for this specific event. For a deeper breakdown of this rule, see our guide on understanding the difference between flood and water damage.

Telling the adjuster, “I just found this mold behind the fridge, it looks like it has been growing back there for a really long time.”

Telling the adjuster, “The ice maker line suddenly snapped on Tuesday, water flooded under the cabinets, and now mold is blooming because we could not get it completely dry.”

The Financial Trap: Mold Coverage Limits and Sub-Limits

Even if you successfully prove that your mold was caused by a sudden, covered water event, you are not out of the woods. This is where the biggest financial shock occurs. Standard homeowners policies usually contain a mold sub-limit.

A sub-limit means that even if your overall dwelling coverage is $400,000, the amount the policy will pay specifically for mold remediation is artificially capped. In most standard policies, this limit is set at $5,000 or $10,000. Some discount policies cap it as low as $2,500.

Why is this a problem? Because professional mold remediation is incredibly expensive. Proper remediation requires building airtight containment zones, running negative air machines with HEPA filters, applying specialized antimicrobial treatments, and paying for clearance testing by an industrial hygienist.

| Remediation Phase | Typical Costs |

|---|---|

| Initial Environmental Testing | $500 – $1,500 |

| Containment and Air Scrubbing | $1,500 – $3,000 |

| Material Removal and Treatment | $3,000 – $15,000+ |

| Final Clearance Testing | $500 – $1,000 |

If you have a $5,000 sub-limit, that money will be exhausted simply by setting up the containment barriers and running the air scrubbers. You will be left paying out of pocket for the actual removal of the infected materials.

The Rebuild Difference: This is why it is absolutely critical to differentiate between three separate buckets of money: testing, remediation, and rebuilding. While the remediation (containment, treatment, removal) is capped by your sub-limit, the rebuild (putting up new drywall, painting, installing new baseboards) usually falls under your standard dwelling coverage and is not subject to the mold cap. A skilled adjuster knows how to separate these costs to maximize your coverage.

How the Adjuster Inspects Your Mold Issue

Whether you get to utilize those sub-limits—or whether your claim gets denied entirely—comes down to what the field adjuster writes in their initial report. When the insurance company sends an adjuster to your home, their primary goal during a mold claim is to establish a timeline. They are looking for physical evidence that the water has been present for a long time, which gives them the justification to deny the claim under the gradual damage exclusion.

I have observed adjusters meticulously documenting specific signs of long-term water exposure. They will look at the nails and screws in your drywall. If the screw heads are heavily rusted, they will argue the moisture has been present for months. They will look at the wood framing. If the wood is not just wet, but actively rotting and deteriorating, that is a clear signal of long-term exposure. They will pull back baseboards to see if there are multiple water rings, indicating repeated wet-and-dry cycles over time.

This is where claims go wrong. Sometimes, a sudden pipe burst happens in an area that already had a minor, unknown prior leak. The adjuster sees the old rust, blames the entire massive new mold bloom on the old leak, and denies the whole claim. You have to be prepared to defend the timeline of the primary event.

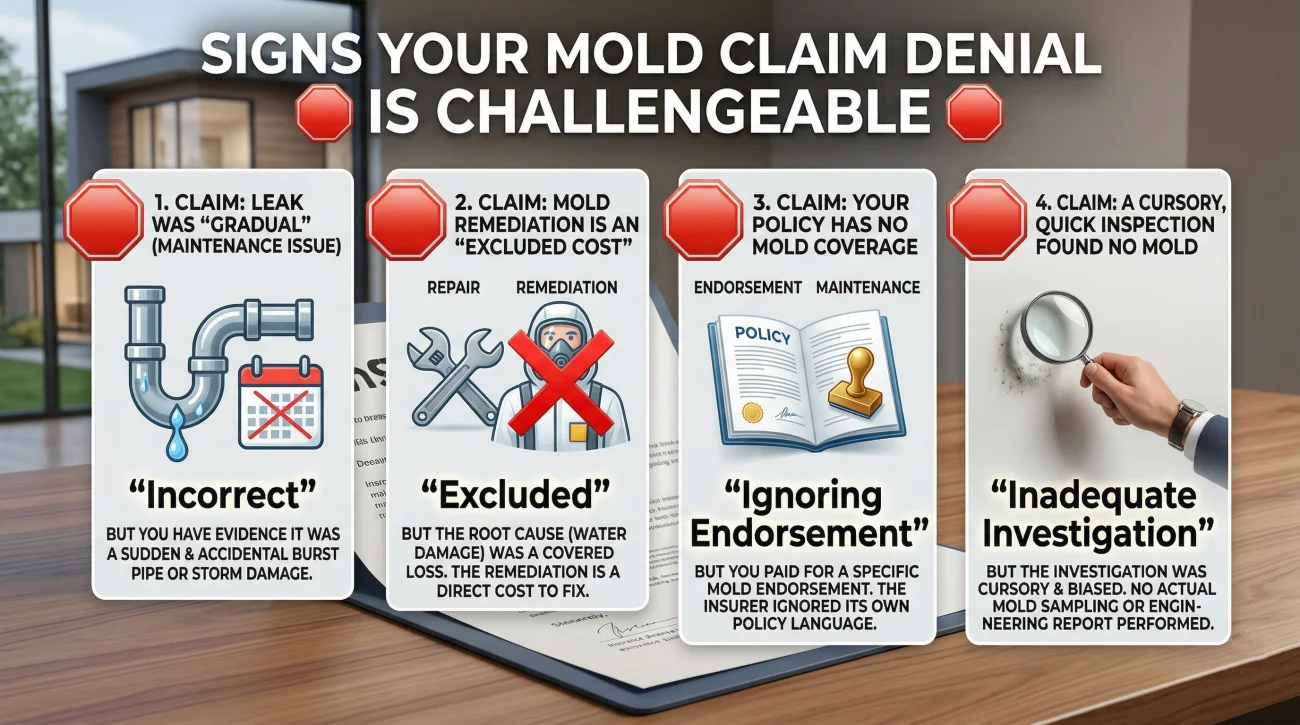

Signs Your Mold Claim Denial Needs a Second Look

It is incredibly frustrating to suffer a major plumbing failure, do everything right, and still receive a denial letter claiming your damage is due to “wear and tear.” Insurance companies rely heavily on the gradual damage exclusion, and in my experience, they often apply it incorrectly to save money. If you are sitting at your kitchen table looking at a denial letter, you need to know when to push back.

Here are the clearest signals that your mold claim denial or low settlement offer is challengeable:

- 🛑 The mold grew after a verified, sudden pipe burst, but the adjuster’s report lists the cause as a “gradual leak.”

- 🛑 The insurance company paid for the water damage drywall repairs but completely excluded the mold remediation on the exact same wall.

- 🛑 You purchased a specific mold endorsement or hidden water damage endorsement, but the carrier still denied the claim based on maintenance.

- 🛑 The adjuster barely spent ten minutes looking at the damage before declaring it “long-term wear and tear” without cutting into the wall to investigate.

Mold coverage turns entirely on how the underlying water event is characterized. If the adjuster’s characterization of the leak does not match the actual facts of what happened in your home, you do not have to simply accept their decision. Getting a professional review from a licensed public adjuster who specializes in complex water events can help you identify exactly where the carrier’s logic failed.

In cases where the insurance company is acting in bad faith or ignoring clear evidence of a sudden event, it may also be worth getting a free denial review from an insurance claim attorney. Do not let an incorrect “gradual” label cost you thousands of dollars.

Documentation Discipline: Proving the Sudden Event

If you discover mold following a water event, the way you document the scene will make or break your claim. You have to preserve evidence that the source was sudden to ensure the adjuster has no room to assume otherwise.

- 📷 Photograph the broken part: Do not throw away the broken plumbing fitting, the split hose, or the failed valve. That piece of metal or plastic is the physical proof of your sudden peril.

- 📏 Document the surrounding dry areas: Take wide-angle photos showing the extent of the immediate flooding to prove this was a large, singular event.

- 📝 Request written determination: If you hire a water mitigation company to set up fans, make sure their daily moisture logs are meticulous and shared with your carrier.

⚠️ Warning: Never use bleach on mold before the adjuster arrives. Not only is bleach ineffective on porous surfaces like drywall, but altering the scene can give the adjuster grounds to claim you destroyed evidence of the water source.

If your claim is taking too long or the adjuster is making verbal comments about the damage looking old, you need to force them to put their findings in writing. Use a simple, polite message to ensure everyone is on the same page regarding the facts of the loss before memories fade.

Hello [Adjuster Name],

Following your inspection on Tuesday, could you please provide a written copy of your preliminary findings regarding the exact source of the water intrusion? I want to ensure my mitigation contractor is focusing their efforts on the correct area.

Thank you,

[Your Name]

Final Thoughts on Navigating Mold Claims

Dealing with mold is terrifying, and having your insurance company treat you with suspicion only makes it worse. But remember, you have rights under your policy. If your home suffered a sudden, covered water event, do not let an adjuster summarily dismiss your damage as a “maintenance issue” without pushing back.

Document your timeline immediately, keep all physical evidence of the broken plumbing or roof damage, and do not hesitate to get a professional second opinion if the carrier’s story simply does not match the reality of what happened in your home.

❓ FAQ

💧 Does home insurance cover mold remediation if a pipe bursts?

Yes, in most cases. A burst pipe is a sudden and accidental covered peril. The resulting mold remediation is typically covered, subject to the mold sub-limits listed in your specific policy.

🏚️ Does homeowners insurance cover black mold?

Insurance companies do not care about the color or species of the mold. They only care about what caused the water damage. If the black mold was caused by a covered sudden event, it may be covered. If it was caused by a slow leak, it will be denied.

🛁 What happens if mold grew from a slow leak I didn’t know about?

Standard policies generally exclude damage from slow, gradual leaks. The insurer views this as a maintenance issue, even if the leak was hidden behind a wall. Some policies offer a specific “hidden water damage” endorsement you can purchase to cover this scenario.

📜 How do I know my homeowners insurance mold coverage limits?

You can find this on your policy’s Declarations Page. Look for a line item that says “Fungi, Wet or Dry Rot, or Bacteria Coverage.” It will usually display a specific dollar limit, most commonly between $5,000 and $10,000.

🔄 What if mold appears after my water damage claim is already closed?

You can usually file a supplemental claim. If the original water event was covered, and the mold grew because the initial dry-out by contractors was insufficient, it should still tie back to the original date of loss. Act quickly to notify your adjuster.

🌧️ Is mold from rain coming through the roof covered?

If the roof was suddenly damaged by a covered event like a windstorm or a fallen tree, the resulting rain intrusion and subsequent mold are typically covered. If the rain came in because the roof is simply old and failing, the claim will be denied.

🌬️ Will my policy pay for mold caused by poor ventilation?

No. Mold caused by chronic humidity, lack of bathroom exhaust fans, or poor attic ventilation is considered an environmental and maintenance issue. It is never covered by standard homeowners insurance.

⏱️ How long does it take for mold to grow after water damage?

Under optimal conditions (warm temperatures and high moisture), mold spores can germinate and begin growing within 24 to 48 hours. This is why immediate water mitigation after a sudden leak is crucial to prevent claims complications.

🚫 Why did my insurance company deny my mold claim?

The most common reasons for denial are that the adjuster classified the water source as a gradual leak, a maintenance failure, external flooding, or chronic humidity. They determined there was no sudden, accidental covered peril.

📑 Can I buy extra coverage for mold?

Yes. Many insurance carriers allow you to purchase a mold endorsement or rider to increase your sub-limits from the standard $5,000 up to $25,000 or more. You must request this before a loss occurs.

Knowing what is covered is step one. These explain what happens from there.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

These cover what to do when the offer does not match what your policy says.

- 5 patterns that signal your settlement is probably short

- Who the adjuster at your door actually works for

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When a denial needs legal leverage, not just negotiation

- Four paths to fight a denial, including one most homeowners miss

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.