- Coverage D, known as Loss of Use or Additional Living Expenses (ALE), pays for your housing and living costs when a covered disaster forces you out of your home.

- It only covers the “additional” expenses above your normal baseline budget, not your entire cost of living.

- You are entitled to a temporary residence that reflects a comparable standard of living to your damaged home, not just a standard hotel room.

- There are strict limits on this coverage, usually calculated as a percentage of your total dwelling coverage or capped by a specific timeframe.

- Keeping meticulous receipts and understanding how to negotiate temporary housing options are critical to not burning through your limits too quickly.

The Financial Lifeline You Probably Did Not Know You Had

In my years of working on property claims, the most traumatic cases are always the ones involving displacement. Standing in the driveway while firefighters pack up their gear, or looking at a house fully gutted by category three water, homeowners inevitably ask the exact same question: “Where are we supposed to sleep tonight, and how am I going to pay for it?”

The good news is that if your home is rendered uninhabitable by a covered peril, your insurance policy provides a specific financial safety net for exactly this situation. It is called Loss of Use coverage, often referred to as Additional Living Expenses or ALE. It falls under Coverage D in standard policies.

The bad news is that most homeowners do not know this coverage exists until the day they urgently need it. Even worse, those who do know about it often use it incorrectly, burning through their limits in the first few months and leaving themselves stranded while their house is still under construction.

As a claims writer, I have seen families of five squeezed into single hotel rooms for months because they did not know they had the right to demand a comparable rental house. Understanding exactly what this section of what your homeowners insurance actually covers is the difference between a stressful but manageable displacement and a total financial nightmare.

What Loss of Use Coverage Actually Pays For

The most important word in Additional Living Expenses is “additional.” Understanding this specific definition is the key to getting your reimbursements approved.

Your insurer is not stepping in to pay for your entire life while you are out of your home. You still have to pay your mortgage, your normal car payments, and your baseline bills. Coverage D is designed strictly to cover the difference between what it normally costs you to live and what it costs you to live now that you have been displaced.

I recently reviewed a file where a homeowner thought their insurance company would cover their entire $1,500 monthly grocery bill while they were displaced. The adjuster denied it. The homeowner was furious, but the adjuster was technically correct. The policy only pays the cost above the homeowner’s normal baseline. If you normally spend $800 on groceries, and now you have to spend $1,500 because you are eating out every night, the insurance company only owes you the $700 difference.

What Qualifies as an Additional Expense

Every claim is unique, but if an expense is necessary to maintain your normal standard of living and was directly caused by the displacement, it generally qualifies for reimbursement. Common approved categories include:

- Temporary Housing: Hotel bills for the immediate aftermath, followed by rent for a temporary house or apartment during long-term repairs.

- Food and Meals: Restaurant bills or increased grocery costs, minus your normal monthly food budget.

- Pet Boarding: If your temporary hotel or rental does not allow dogs or cats, the cost to board them is typically covered.

- Increased Commuting Costs: If your temporary rental is 20 miles further from your office or your children’s school, the extra gas and mileage qualify.

- Storage Fees: The cost to rent a storage unit for belongings that survived the event but cannot stay in the damaged home. Note that damage to the items themselves falls under a different section of your policy. You can read our detailed breakdown on how personal property limits work for more context on that.

- Laundry Expenses: If your temporary housing lacks a washer and dryer, laundromat or dry cleaning fees are reimbursable.

What Is Strictly Excluded

Understanding what gets denied is just as important as knowing what gets approved. Adjusters scrutinize ALE receipts closely. You will face immediate pushback if you submit costs for things that do not fit the strict definition of an additional burden.

| Excluded Item | Why It Gets Denied |

|---|---|

| Your Standard Mortgage | You would have to pay your mortgage even if the house was perfectly fine. It is not a new cost caused by the fire or flood. |

| Normal Utility Bills | If your temporary rental includes utilities, the insurer will subtract your home’s historical average utility cost from your ALE payout to prevent double-dipping. |

| Entertainment and Upgrades | Renting a luxury condo on the beach when your damaged home is a standard inland ranch house will be flagged as an unnecessary upgrade. Movie tickets or premium cable packages at the hotel are also excluded. |

Edge Cases: Partial Displacement

A common scenario I encounter is when a home is damaged but remains partially livable. For example, if a kitchen fire destroys your ability to cook, but your bedrooms are untouched and safe from smoke, your insurer will likely not approve a hotel stay. However, your Loss of Use coverage should still trigger to cover the increased cost of eating out for every meal until your kitchen is fully restored.

The Battle for “Comparable” Housing

The single biggest mistake displaced families make is accepting whatever temporary housing the insurance company’s vendor offers them without pushing back. Insurance companies contract with third-party relocation services to find you a place to stay. These vendors are incentivized to keep costs low.

Your policy states that you are entitled to maintain your “normal standard of living.” If you live in a four-bedroom home with a fenced yard for two large dogs, a two-bedroom apartment on the third floor of a complex is not comparable. You have the right to request a single-family home rental that allows pets and provides adequate space for your family.

It is incredibly common for adjusters to initially place families in extended-stay hotels and leave them there for months. This is exhausting and burns out your coverage limits fast. You must be proactive in requesting appropriate long-term housing.

Subject: Request for Comparable Temporary Housing – Claim #12345678

Dear [Adjuster Name],

While we appreciate the initial hotel placement, the current accommodation is not sustainable for the projected six-month repair timeline. Our damaged home is a 3-bedroom, 2-bathroom house. The current single hotel room does not represent a comparable standard of living for our family of four.

Please instruct the relocation vendor to source a comparable 3-bedroom single-family rental property within our current school district. We look forward to reviewing the available rental options by [Date].

Thank you,

[Your Name]

Understanding Your Limits and Timeframes

Loss of Use coverage is not a blank check, and it does not last forever. It is tightly constrained by two factors: a financial cap and a time limit. Hitting either one will immediately cut off your temporary housing funds.

The Financial Cap: In standard policies, Coverage D is typically calculated as a percentage of your dwelling coverage (Coverage A). It usually ranges from 20% to 30%. If your home is insured for $400,000, your ALE limit is likely between $80,000 and $120,000. While that sounds like a massive amount of money, a $5,000 monthly rental plus furniture rental, increased food costs, and boarding fees can drain a $80,000 limit in less than a year.

The Time Limit: Most modern policies also include a strict timeframe limit, typically 12 or 24 months. The policy will state that it covers additional living expenses for “the shortest time required to repair or replace the damage,” subject to that hard monthly cap. If a contractor delay pushes your rebuild to month 14, but your policy has a 12-month cap, you will be paying rent out of your own pocket for those final two months.

⚠️ Warning: The clock starts ticking on the date of the loss, not the date you move into a temporary rental. Delays in the early stages of a claim are incredibly dangerous because they eat into your ALE timeframe. If your insurer is dragging their feet on approving the initial scope of work, your housing funds are quietly burning away.

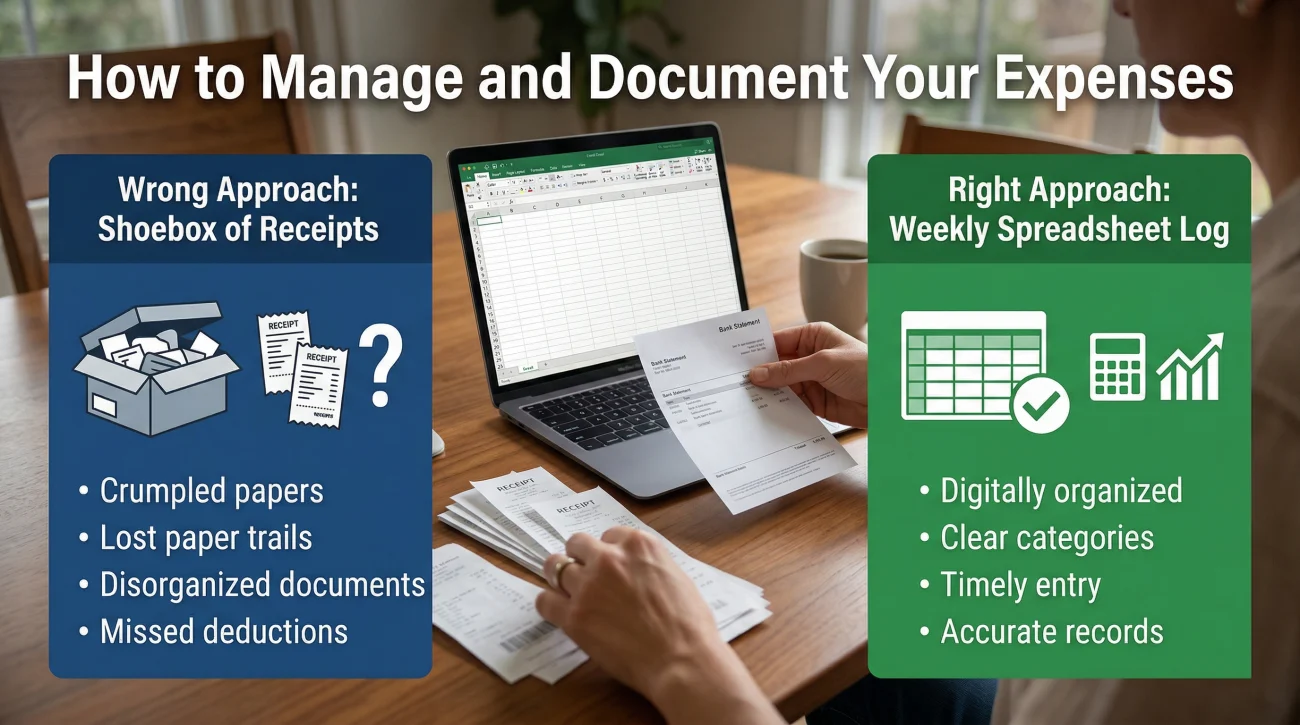

How to Manage and Document Your Expenses

Insurance companies do not just hand you a lump sum for living expenses. ALE operates on an incurred-cost basis. This means you have to spend the money, prove that you spent it, prove that it was an additional expense, and then ask for reimbursement.

Throwing all your restaurant receipts, gas station slips, and hotel invoices into a shoebox and mailing them to the adjuster three months later with no explanation.

Establishing a solid baseline budget immediately by pulling your last three months of bank statements to calculate your exact monthly average for groceries and utilities. Then, log every new expense in a spreadsheet weekly, attach the corresponding receipt, and submit organized batches to your adjuster every 30 days.

One of the most practical steps you can take is dedicating a single credit card solely for displacement expenses. Use it to pay for the hotel, the rental furniture, the laundromat, and the restaurant meals. This creates an automatic, clean paper trail that separates your claim expenses from your normal life expenses.

The Emergency Advance

It is important to note that while ALE requires you to submit receipts for reimbursement, you do not always have to front all the cash on day one. After a severe total loss, many insurers can issue an emergency cash advance, often ranging from $1,500 to $5,000, within the first 48 hours to help you secure a hotel and buy emergency clothing. Though the exact amount varies by insurer and policy, adjusters rarely offer this proactively. You must explicitly request an “emergency displacement advance” during your initial claim report to trigger these funds.

Signs Your Loss of Use Coverage Is Failing You

Because ALE is tied to the timeline of your home repairs, problems with this coverage rarely happen in isolation. When you struggle to get your housing costs approved, it is usually a symptom of a larger bottleneck in your claim. Watch out for specific warning signs that your process has crossed over from a temporary inconvenience into a serious financial risk.

The first sign of trouble often happens right at placement, when your insurer offers temporary housing that is drastically smaller or lower quality than your damaged home and refuses to approve anything else. Later in the process, you might notice that reimbursement checks for your submitted food and hotel receipts are taking weeks or months to arrive, forcing you to carry thousands of dollars in debt on your personal credit cards. You may also see the insurance company deducting large, unexplained amounts from your food reimbursements under the guise that your costs are not “additional.”

The most dangerous scenario, however, is a stalled rebuild. If you realize you are going to hit your 12-month ALE time limit before the house is finished because of an ongoing repair estimate dispute, your temporary housing security is in jeopardy.

Protecting Your Rebuild Timeline

Loss of Use coverage is designed to keep a roof over your head, but it is ultimately just a bridge. The goal is to get back into your restored home before that bridge collapses. Because ALE limits are strictly capped, your temporary housing security is deeply tied to the speed and accuracy of your main dwelling claim. If your adjuster refuses to approve a realistic repair scope, the construction will stall, and your house will not be rebuilt before your temporary housing funds run dry.

Managing a major property loss while simultaneously tracking every meal and hotel receipt is a full-time job. If you are facing a long-term displacement and feel the insurer is dragging their feet on approvals, you need to intervene early.

Bringing in professional help can take the heavy lifting of documenting property damage and negotiating repair scopes off your plate, freeing you to focus on your family’s immediate living situation. If your temporary housing is at risk due to a stalled claim, arranging a free initial review of your claim file with a licensed public adjuster is the safest next step to get your rebuild back on track.

❓ FAQ

🏠 Does homeowners insurance pay for a hotel?

Yes, if your home is uninhabitable due to a covered peril like a fire or severe water damage, your Loss of Use coverage will pay for a hotel or temporary rental.

🍔 Will insurance pay for all my food while I am displaced?

No. They will only pay the difference between your normal monthly grocery budget and the increased cost of having to eat at restaurants or buy prepared meals.

⏳ How long will insurance pay for my temporary housing?

It depends on your specific policy, but most standard policies cap the duration at 12 to 24 months, or until your financial limit runs out, whichever comes first.

🐶 Does loss of use cover pet boarding?

Yes. If your temporary accommodation does not allow pets, the cost of boarding your dogs or cats is generally considered a reimbursable additional living expense.

🚗 Are extra commuting costs covered if I have to move further away?

Yes, if your temporary rental forces you or your children to commute further to work or school, the additional mileage and gas costs are typically covered.

💰 Do I get to keep the loss of use money if I stay with family?

Usually, no. This coverage operates on an incurred-cost basis. If you do not spend the money on rent or hotels, there is no expense for the insurance company to reimburse.

💳 How do I actually get the money for my living expenses?

You generally have to pay out of pocket first, save all your receipts, and submit them to your adjuster in batches for reimbursement, though direct billing for hotels is sometimes possible.

📦 Does my policy cover the cost of a storage unit?

Yes, if you need to move surviving furniture or personal items out of the house to facilitate repairs, the monthly fee for a storage unit is a valid ALE expense.

🏢 Can the insurance company force me into a tiny apartment?

No. Your policy requires them to provide temporary accommodations that match the size, utility, and location of your damaged property as closely as possible, so you have every right to push back on inadequate offers.

🧾 What happens if I hit my financial limit before the house is finished?

Once you exhaust your Coverage D limits, the insurance company will stop paying for your temporary housing, leaving you to cover the rent out of your own pocket until repairs are done.

Knowing what is covered is step one. These explain what happens from there.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

These cover what to do when the offer does not match what your policy says.

- 5 patterns that signal your settlement is probably short

- Who the adjuster at your door actually works for

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When a denial needs legal leverage, not just negotiation

- Four paths to fight a denial, including one most homeowners miss

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.