- The core difference: Standard homeowners insurance typically covers sudden, internal water damage (like a burst pipe). It excludes external “flood” damage (like rising rivers or storm surge).

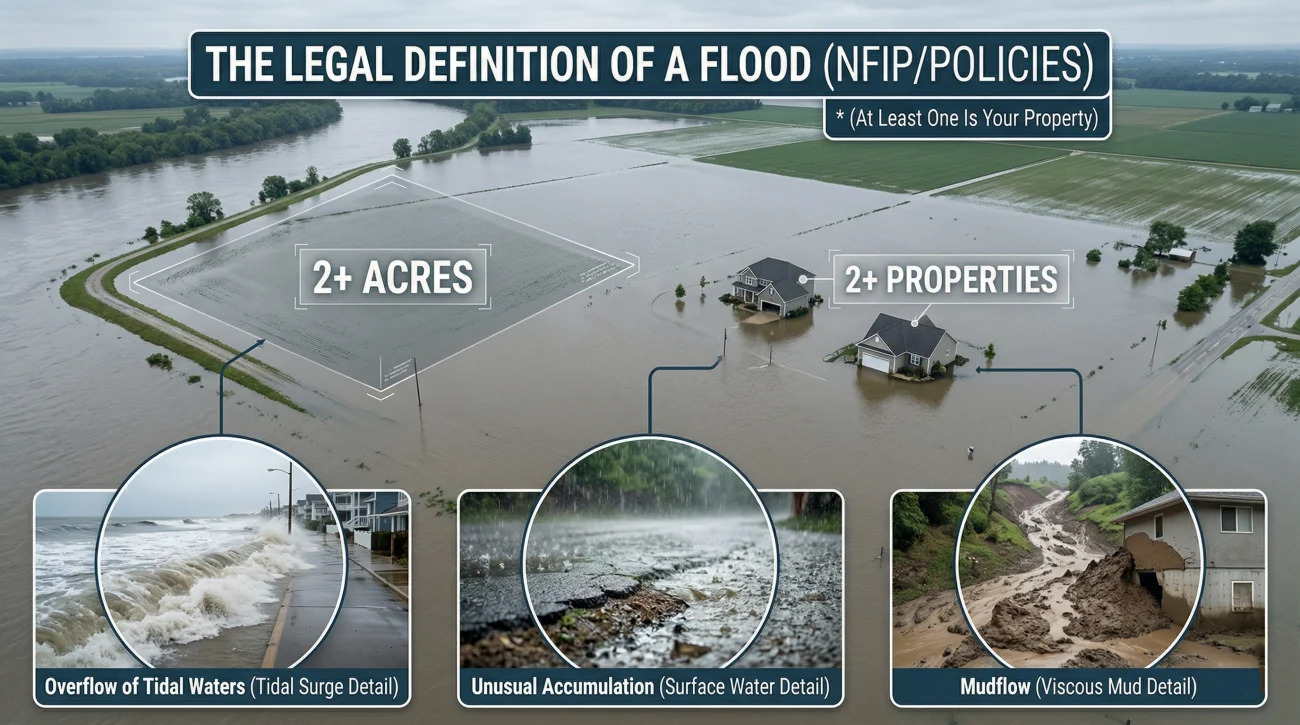

- The definition matters: According to the standard insurance definition, a flood is an excess of water on normally dry land affecting two or more properties or acres.

- The grey areas: Rainwater entering through a storm-damaged roof is usually covered water damage, not a flood. Groundwater seeping through a basement foundation is usually excluded.

- The common denial: Insurers sometimes mischaracterize covered sudden water damage as excluded flood or seepage damage. Documenting the exact source of the water is your best defense.

The Coverage Line That Changes Everything

Imagine walking into your basement to find two inches of standing water. In Scenario A, a pipe behind your washing machine burst. In Scenario B, the creek behind your house overflowed its banks. To you, the damage looks exactly the same. Ruined drywall, soaked baseboards, destroyed flooring.

But to your insurance company, the difference between these two scenarios is massive. One is likely covered. The other is almost certainly denied. Understanding the strict line between flood vs. water damage insurance is one of the most critical things a homeowner can learn.

I have reviewed hundreds of property claims, and I can tell you that a significant portion of homeowners incorrectly believe that “water is water” and their standard policy will cover any event that leaves their floors wet. This misconception is the root cause of many surprise, expensive claim denials.

In my experience, the confusion doesn’t just happen on the homeowner’s side. Sometimes, adjusters misinterpret the source of the water, labeling a covered internal leak as an excluded external flood. Today, we are going to walk through exactly how this distinction works, where the grey areas lie, and how to protect yourself if your damage is mischaracterized.

Why the Distinction Exists: The Risk Pool

It is natural to feel frustrated when an insurance company says, “We cover water, but not that water.” To understand how to navigate a claim, you first have to understand why standard homeowners policies exclude flood damage entirely.

It comes down to how insurers price risk. A burst pipe is an isolated event. Your pipe bursts, but your neighbor’s house is fine. The insurer can easily absorb that cost because only a tiny fraction of homes suffer burst pipes on any given day. But a flood is a systemic event. When a river overflows or a hurricane pushes storm surge inland, it damages entire neighborhoods or zip codes simultaneously.

If standard homeowners policies covered floods, a single major hurricane could bankrupt the insurance company, leaving them unable to pay anyone’s claims. For a broader look at how standard coverages are structured, you can review our standard coverage guide.

External flooding affects thousands of homes at once. Private insurers cannot easily model or absorb this catastrophic, localized financial hit without a separate program.

A water heater rupturing only affects one home. This is the exact type of sudden, accidental risk your standard policy is built and priced to cover.

The Strict Definition of a Flood

Because the exclusion is so absolute, the definition of what constitutes a “flood” must be very specific. Most standard policies use a definition consistent with the National Flood Insurance Program (NFIP) to draw the line.

Key Point: A flood is defined as a general and temporary condition of partial or complete inundation of two or more acres of normally dry land area, or of two or more properties (at least one of which is your property).

The source of this inundation must be from:

- Overflow of inland or tidal waters (rivers, lakes, oceans).

- Unusual and rapid accumulation or runoff of surface waters from any source.

- Mudflow.

If the water that entered your home meets this definition, your standard homeowners policy will almost certainly exclude it.

💡 Pro Tip on Flood Policies: While the NFIP is the most common provider for separate flood coverage, the private flood insurance market has grown significantly. Private policies often offer better coverage terms than the NFIP, such as Replacement Cost Value (RCV) rather than depreciated payouts, and far broader protection for basements.

What Counts as Water Damage (Potentially Covered)

So, if that is what an excluded flood looks like, what does covered water damage actually look like? The golden rule for standard homeowners insurance is that the water must come from a sudden, accidental, and internal source.

Common examples of water damage that are typically covered include:

- A frozen pipe that bursts behind your drywall.

- A supply line to your washing machine or toilet that suddenly snaps.

- A water heater that unexpectedly ruptures.

- An overflowing tub or sink.

- Sudden roof damage (like wind blowing off shingles) that allows a heavy rainstorm to pour directly into your living room.

Notice the theme here: the source is internal (or rain entered through a sudden opening), and the event happened quickly. However, it is vital to remember that even internal water damage can be denied if it is deemed a maintenance issue. We explore this specific nuance deeply in our breakdown of sudden versus gradual water damage.

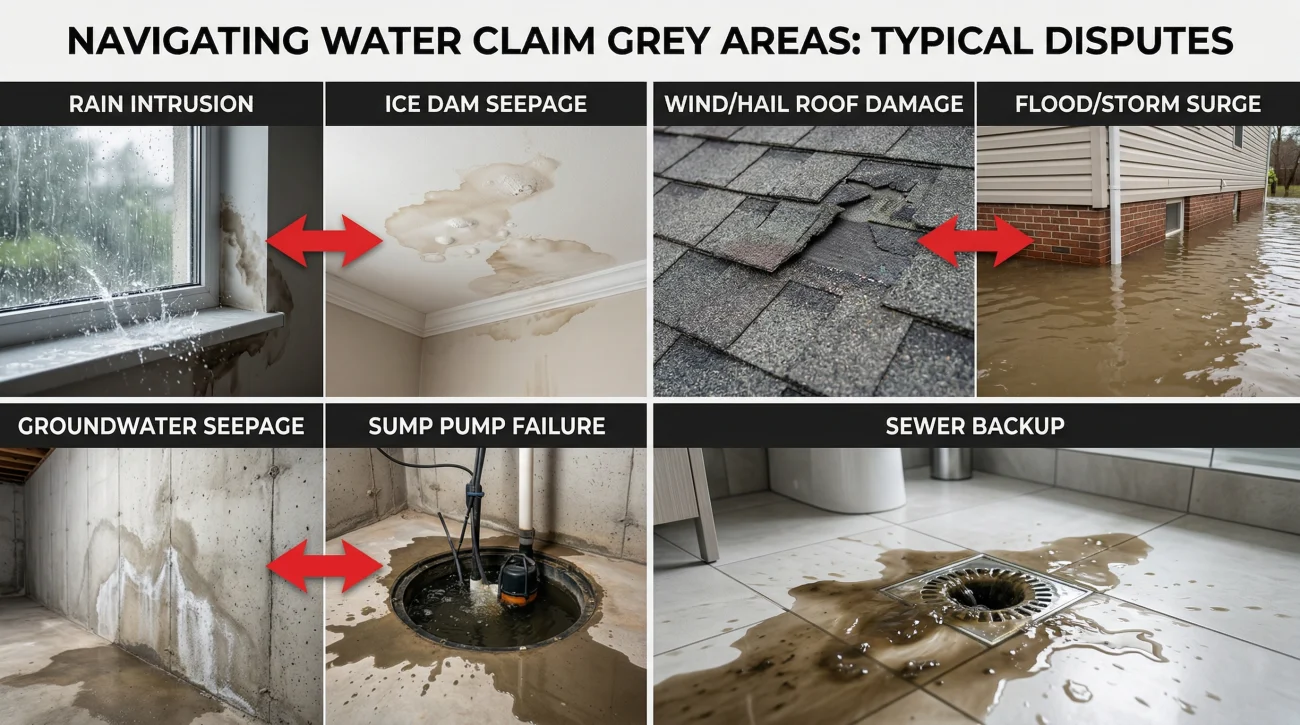

The Grey Areas That Cause the Most Disputes

In a perfect world, water damage would clearly fall into the “burst pipe” bucket or the “river overflowed” bucket. In reality, claims often sit in a messy grey area. This is where I see the most friction between homeowners and adjusters.

Rainwater Entering Through the Roof vs Ice Dams

If a severe storm damages your roof and rain pours in, ruining your ceilings, this is typically covered as water damage because the proximate cause was the windstorm creating an opening.

Similarly, water seeping in from an ice dam on your roof is a classic grey area. Adjusters sometimes try to deny this as a gradual maintenance issue, but if the ice dam formed rapidly and forced water under the shingles, it can often be successfully claimed as a sudden, covered event.

I recently reviewed a file where an adjuster initially cited a ‘surface water exclusion’ for rain that pooled on a flat roof and seeped down. Because the homeowner had photos showing a tree branch had struck the roof during the storm, creating a sudden tear in the membrane, we were able to firmly establish it as a covered sudden water event.

Simultaneous Events: Wind and Flood

What happens if a hurricane blows off your roof (covered water damage from rain) and also pushes storm surge into your living room (excluded flood)? This is one of the most complex disputes I handle. Insurers will often attempt to apply an “anti-concurrent causation” clause to deny the entire claim if the two events happened simultaneously. Documenting exactly which water caused which damage (and the precise timeline of what failed first) is crucial.

Groundwater and Foundation Seepage

If it rains heavily for three days and water slowly seeps through microscopic cracks in your basement foundation, insurers generally classify this as groundwater seepage or hydrostatic pressure. It is excluded from standard policies because it is considered a gradual maintenance issue, and it does not meet the NFIP definition of a flood. For a full understanding of what else is left out of your policy, you should review common homeowners insurance exclusions.

Sewer and Drain Backup

If heavy rain overwhelms the municipal sewer system and raw sewage backs up into your basement, it feels like a flood. However, standard policies explicitly exclude sewer backup, and standard flood policies often will not cover it unless it was directly caused by a wider area flood. To be protected here, you usually need a specific “water backup” endorsement added to your standard policy. We have a full breakdown of sewer backup coverage if you are facing this specific nightmare.

How Adjusters Investigate the Source

When an adjuster walks into your home, their primary job is to determine the exact source of the water. Their characterization of the source in their report will dictate whether your claim is approved or denied.

They look for specific evidence:

- Water lines: Is there a uniform dirt/water line on the exterior of the house? That suggests rising surface water (flood).

- Direction of flow: Are the water stains originating from the ceiling down (roof leak), from the baseboards up (groundwater), or spraying from a specific point in the wall (pipe burst)?

- State of materials: Is the broken pipe cleanly snapped, or does it show signs of heavy, long-term corrosion?

When I walk a loss site with a homeowner, the very first thing I look for is what the emergency mitigation crew might have accidentally thrown away in their rush to dry the house.

Note: A common mistake homeowners make is throwing away the broken plumbing component (like a ruptured washing machine hose) during the initial panic of cleaning up. Never throw away the source of the leak. Without it, the adjuster may default to an assumption that the water came from an excluded external source or a gradual maintenance failure.

Communicating the Source Effectively

How you report the claim on day one matters immensely. If you call the claims hotline in a panic and say, “My basement is flooded!”, the representative will likely type the word “Flood” into the initial claim notes. This can trigger an immediate flag for a flood exclusion investigation, even if a pipe burst.

The Documentation Formula: Identify the specific source + Use precise, factual language + Document with immediate photos.

If you need to follow up with an adjuster to clarify the source of the water, keep it factual and directly tied to the sudden, internal event.

Subject: Claim #[Your Claim Number] – Confirmation of Water Source

Hello [Adjuster Name],

I am writing to confirm the details of the water damage discovered on [Date]. As shown in the attached photos and the plumber’s initial invoice, the damage originated from a sudden rupture in the braided steel supply line leading to the guest bathroom toilet.

The water spread rapidly from this internal source into the hallway and living room. Please let me know if you need the physical supply line, as I have retained it for your inspection.

Thank you,

[Your Name]

Warning on Secondary Damage: Covered water damage claims often become complicated weeks later if mold develops. Your coverage for the mold will depend entirely on how the adjuster characterized the initial leak. Read our guide on mold coverage to understand this connection.

Signs Your Claim Was Mischaracterized (And When to Fight Back)

There is nothing more frustrating than knowing your damage was caused by a sudden, covered event inside your home, only to receive a letter from the insurance company denying the claim based on a “flood” or “surface water” exclusion.

I have seen countless valid claims initially denied because an adjuster walked into a wet basement and lazily assumed the water seeped in from outside, without properly investigating the internal plumbing. You should closely examine your denial letter if you notice any of these red flags:

- Your damage originated from a specific internal source (like a burst pipe), but the denial letter cites an external flood exclusion.

- Water entered directly through the roof or a blown-out window during a severe storm, but the insurer is improperly applying a surface water exclusion.

- Your damage occurred entirely inside the home, but the adjuster is blaming groundwater seepage without conclusive evidence.

- The adjuster’s written report describes the cause of the loss completely differently than how you, your plumber, or your mitigation company reported it.

If the insurer’s characterization of your damage does not match the actual facts of the event, you do not have to simply accept the denial. The distinction between flood and water damage is often a matter of interpretation – and adjusters make mistakes.

If you find yourself stuck in this exact dispute, getting a professional scope review, or consulting with a claim attorney, can clarify whether the exclusion was accurately applied or if you have grounds to push back and demand coverage.

Final Thoughts

Your insurance company has a team of adjusters whose job is to protect their bottom line, and that often means looking for reasons to apply a policy exclusion. You need to be just as vigilant. Don’t let an incorrect assumption about where the water came from cost you tens of thousands of dollars in out-of-pocket repairs. Document the evidence before it is thrown away, watch the language you use when reporting the loss, and if the facts of your damage don’t match their denial letter, don’t be afraid to push back.

❓ FAQ

What do I do if my insurance denies my pipe burst as a flood?

Challenge the denial by providing the physical broken pipe and your plumber’s official invoice that explicitly notes the failure was a sudden, internal rupture.

Is water damage from rain covered by homeowners insurance?

Yes, but typically only if a covered peril (like wind or hail) physically tore off shingles or broke a window first, creating an immediate opening for the rain to enter.

Does homeowners insurance cover groundwater seepage?

No, standard policies treat this as a maintenance issue. However, if the seepage occurred because a sump pump suddenly failed during the storm, a specific “water backup endorsement” might provide coverage.

Does home insurance cover sewer backup from heavy rain?

No, neither standard homeowners insurance nor basic flood insurance generally covers this. You must have proactively added a specific water backup endorsement to your policy.

How do I know if I have flood damage or water damage?

Look at the “proximate cause.” If the water touched the ground outside before entering your home, adjusters classify it as a flood. If it originated entirely inside from plumbing or appliances, it is water damage.

What does the adjuster look for to prove it was a flood?

Adjusters specifically look for uniform “bathtub ring” water lines on your exterior siding and debris or mud pushed into exterior window wells or door frames.

How do I document water damage correctly?

Beyond taking a video of the active leak, ask your emergency mitigation crew or plumber to write the exact cause (e.g., “sudden supply line snap”) on their work order before you submit it to the insurer.

What counts as flood damage insurance?

It is a completely separate policy from your homeowners insurance. Keep in mind that new NFIP flood policies usually require a 30-day waiting period before they take effect.

When does water become a flood for insurance purposes?

Depth does not matter. Under standard policy definitions, it becomes a flood when it covers normally dry land affecting at least two acres or two separate properties.

Why is my payout so low for a covered water damage claim?

Adjusters often miss “hidden” moisture. A low payout usually means they did not include the cost of removing baseboards to dry behind the drywall or replacing the subfloor beneath your ruined carpet.

Knowing what is covered is step one. These explain what happens from there.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

These cover what to do when the offer does not match what your policy says.

- 5 patterns that signal your settlement is probably short

- Who the adjuster at your door actually works for

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When a denial needs legal leverage, not just negotiation

- Four paths to fight a denial, including one most homeowners miss

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.