- A supplement is an additional request submitted to your insurance company to cover repair costs that were not included in the original settlement.

- It is completely normal and happens on almost all major claims when hidden damage is uncovered during the actual repair process.

- Your contractor should be the one to document, draft, and submit the supplement to the insurer on your behalf.

- As a homeowner, your job is to stay informed, review the scope changes, and avoid paying out of pocket for items your policy should cover while the supplement is pending.

The Mid Repair Surprise

You finally made it through the initial inspections. Your insurance company sent a check, you hired a local contractor, and the demolition work began. But just a few days into the project, your contractor stops working, calls you, and says they need to submit a “supplement” to the insurance company.

If you have never filed a major property claim before, this word can trigger immediate anxiety. Homeowners instantly wonder if this means the claim is being reopened, if they will be penalized by their insurer, or worse, if they are going to have to pay the contractor out of pocket to finish the job.

In my time reviewing property claims, I have seen homeowners completely panic when a contractor mentions a supplement. They think something has gone terribly wrong. The reality is that supplements are standard operating procedure. A home is not a simple machine, and you rarely know the full extent of the damage until you start tearing things apart.

Understanding how this step fits into the broader home insurance claim process is the key to keeping your project on track. Here is exactly what is happening behind the scenes, why your contractor submitted the request, and what your role should be while waiting for approval.

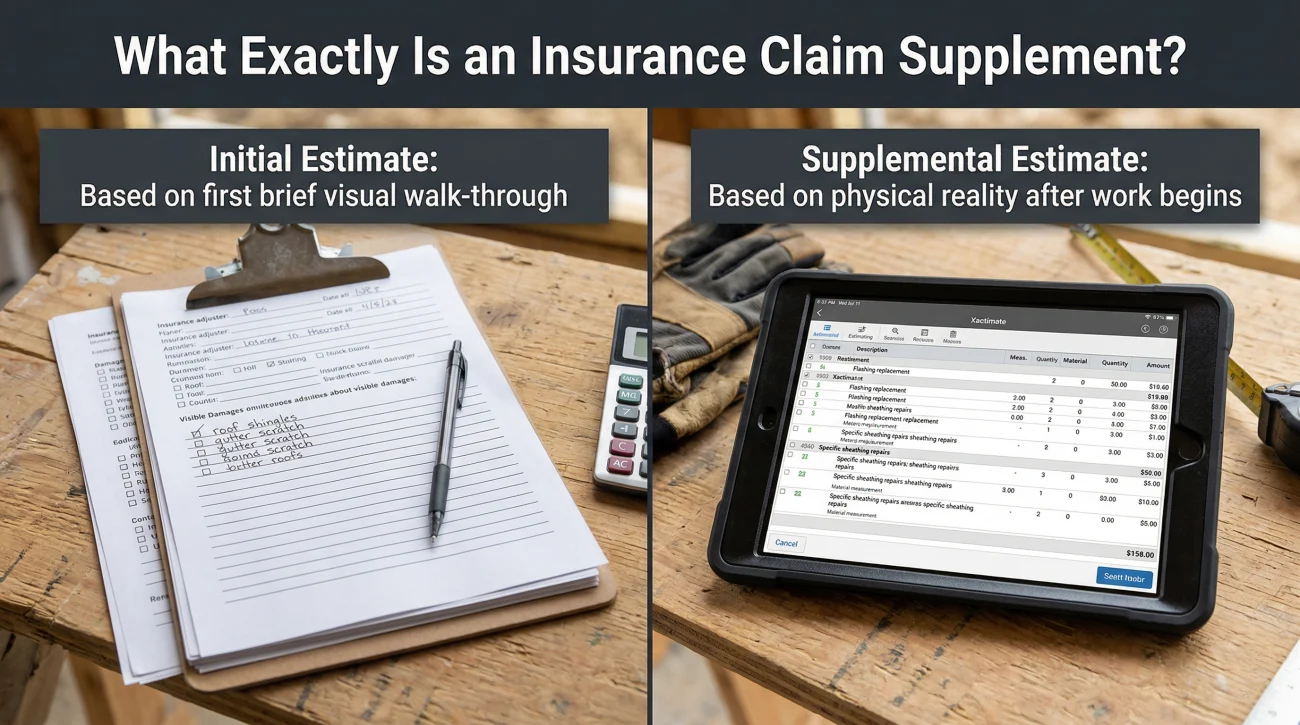

What Exactly Is an Insurance Claim Supplement?

An insurance claim supplement is a formal request for additional funds submitted to the insurance company after the original settlement estimate was issued. It is used to recover costs for necessary repair work or materials that were omitted from the initial adjuster scope.

Many homeowners confuse a supplement with filing an entirely new claim. This is a crucial distinction. A supplement does not create a new claim file on your insurance record. It is simply an extension of the exact same event.

The insurer’s opening offer based solely on what the adjuster could see with their own eyes during the first brief walk through.

A revised calculation based on the physical reality of the repair site once work begins and hidden issues are exposed.

Think of the original estimate as a baseline. The supplement is the correction applied to that baseline to ensure the property is fully restored to its pre loss condition.

Why the Initial Adjuster Estimate Is Rarely Enough

It is natural to wonder why the insurance adjuster did not just get the number right the first time. Sometimes, it is due to adjuster error or a hurried inspection. If you suspect the first offer was artificially reduced, you might want to understand why initial home insurance estimates are often too low.

However, in most standard claims, the initial shortfall is simply due to the physical limitations of a visual inspection. Adjusters write their scopes based on what is visible and accessible on the day they visit.

The Reality of Hidden Damage

An adjuster cannot see through walls, and they do not perform destructive testing. When a pipe bursts in your kitchen, the adjuster can see the warped hardwood flooring. They will write an estimate to replace the wood. What they cannot see is the soaked plywood subfloor underneath the hardwood, or the mold beginning to form behind the lower cabinets.

When your contractor arrives a month later and tears out the warped hardwood, the wet subfloor is finally exposed. At that exact moment, the scope of work changes. The contractor must replace the subfloor to do the job correctly, but they cannot do it for free. They must stop and ask the insurer to supplement the claim for the new materials and the extra labor hours.

| Damage Type | Initial Adjuster Scope (Visual) | Supplemental Contractor Scope (Actual) |

|---|---|---|

| Wind damaged roof | Replace top layer of asphalt shingles. | Replace rotted decking found beneath shingles. |

| Water damaged drywall | Cut out two feet of drywall and paint. | Remove wet insulation inside the wall cavity. |

| Kitchen fire | Clean smoke residue off cabinets. | Replace cabinets due to structural warping. |

Who Actually Submits the Supplement?

One of the biggest mistakes a homeowner can make is trying to write and submit a construction supplement themselves. That is not your job. The supplement should be submitted by the professional doing the repair work.

A contractor experienced in insurance restoration understands the strict evidentiary burden required by insurance carriers. They know that simply calling the desk adjuster and asking for another two thousand dollars will result in an immediate denial. To get a supplement approved, the contractor must provide verifiable evidence.

The Documentation Requirements

A proper supplement package prepared by your contractor typically includes several key components.

First, they must provide clear photographic evidence. This means high resolution photos of the newly discovered damage taken before it is repaired or covered up. A photo of a wet subfloor is proof. A photo of a new floor already installed with a note saying the subfloor was wet will be rejected.

Second, they provide a revised line item estimate. The insurance industry relies on specific software platforms to calculate costs. If you want to understand how contractors and insurers speak the same technical language, it helps to learn how Xactimate software generates repair prices. Your contractor will use this same coding system to justify the extra costs.

Third, they submit a written narrative explaining why the items were not on the original scope and why they are strictly necessary to restore the property.

Your Role as the Homeowner During the Supplement Process

While the contractor handles the technical documentation, you are not entirely off the hook. As the policyholder, the insurance contract is with you, not your builder. This means you must manage the relationship and oversee the process.

⚠️ Warning: Never allow a contractor to begin extensive supplemental repairs before the insurance company has formally approved the extra costs in writing. If the insurer denies the request later, you could be held personally responsible for the bill.

Your primary job is to stay informed. You need to know exactly what your contractor is asking for and how the insurer is responding. Here are the best practices to follow.

- Review the scope change: Ask your contractor to explain the newly discovered damage to you in plain English before they send it to the insurer.

- Sign off carefully: You may need to sign a document authorizing the contractor to discuss the specific supplement with the desk adjuster. Read these authorizations carefully.

- Maintain communication: If the insurer is ignoring your contractor, you have to step in. A contractor is just a vendor, but you are the customer. A call or email from the policyholder often forces a desk adjuster to take action.

Subject: Claim # [Your Claim Number] – Status update on contractor supplementHello [Adjuster Name],

I am writing to follow up on the supplemental estimate submitted by my contractor, [Contractor Company Name], on [Date]. They have halted work on my property pending your approval of the newly discovered damage to the subfloor.

Please let me know if you have received the photos and documentation, and when we can expect the revised estimate to be approved so we can resume repairs.

Sincerely,

[Your Name]

The Timeline and What Happens Next

Once the contractor hits send on the email containing the photos and estimates, the waiting game begins. The time it takes to process a supplement varies wildly depending on the insurer, the complexity of the damage, and whether there has been a recent catastrophic weather event in your state.

For minor additions, such as a few extra bundles of shingles or an additional drywall patch, an inside desk adjuster can often review the photos and approve the cost within a few days. They simply update the file and issue a supplemental check.

When a Reinspection Is Required

If the supplement asks for a substantial amount of money or involves complex structural issues, the insurance company will likely refuse to approve it based on photos alone. They will invoke their right to inspect the property again.

This means a field adjuster will be dispatched back to your home. This process can stall your repairs for weeks. Your contractor will have to pause the project, leave the damage exposed, and wait to meet the new adjuster on site to argue their case in person.

Following this reinspection, the insurer will issue a formal decision. They might approve the new scope entirely, issue a partial approval for certain items while denying others, or completely reject the supplemental request. If an agreement is reached and documented, a supplemental check is issued so your contractor can finally resume work.

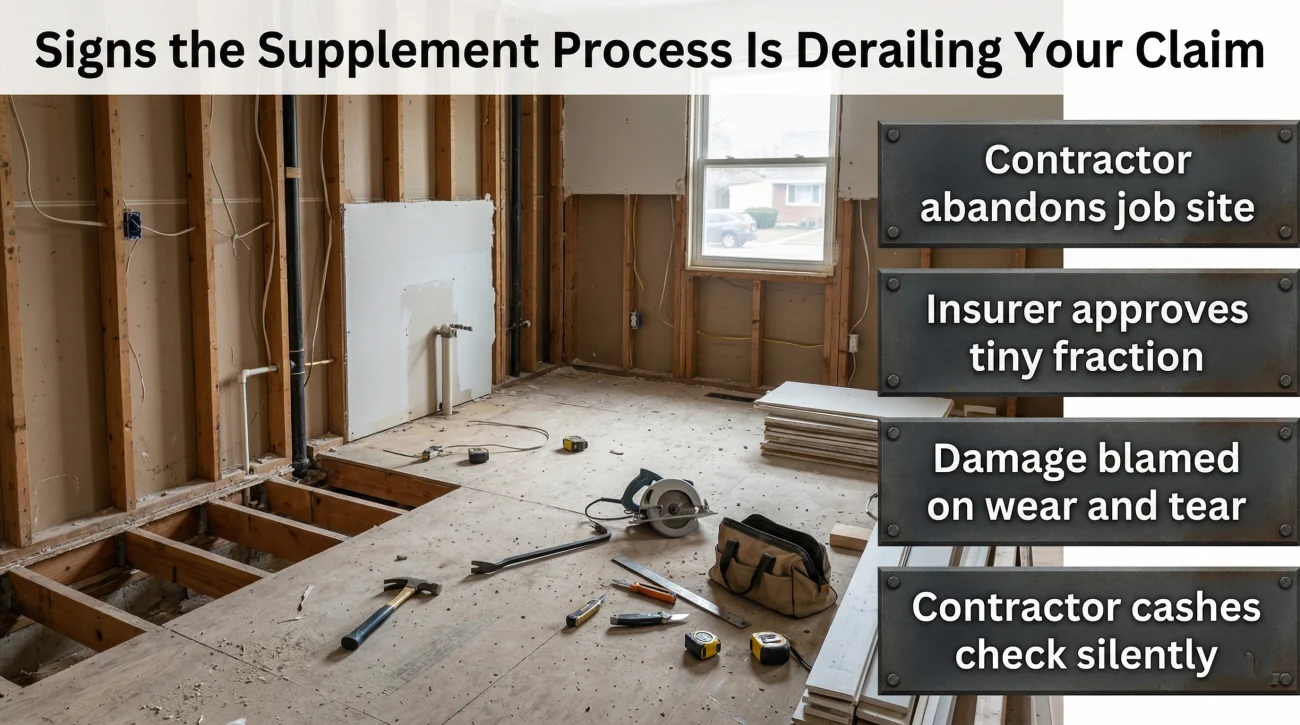

Signs the Supplement Process Is Derailing Your Claim

In a perfect world, a contractor finds hidden damage, submits a photo, and the insurer pays for it. In reality, the supplement phase is where the vast majority of severe claim disputes are born. The insurance company wants to protect its bottom line, and the contractor wants to get paid for their work. You are stuck in the middle with a torn up house.

Here are the concrete red flags that indicate the normal supplement process has broken down and is now actively harming your recovery:

- Your contractor has completely abandoned the job site for weeks because the insurance company is refusing to return their phone calls regarding the supplement.

- The insurer approved a tiny fraction of the supplement and denied the rest, prompting your contractor to hand you an invoice for the difference.

- The desk adjuster claims the new damage is due to “wear and tear” or “maintenance issues” rather than the covered event, effectively denying that portion of the claim.

- You realize your contractor submitted a supplement and cashed a check without ever showing you the revised scope of work.

When these situations occur, you are no longer dealing with a simple administrative delay. You are dealing with a fundamental disagreement over coverage and scope.

Bridging the Gap Professionally

A stalled or partially denied supplement is often just a scope dispute disguised as a paperwork issue. The contractor documented damage that they believe is necessary to fix, but the insurer is actively resisting paying for it.

When a contractor hits a wall with the desk adjuster, they are limited in what they can do. They cannot negotiate your insurance policy terms, and they cannot force the carrier to pay. If the insurer refuses the supplement, the contractor will simply ask you to cover the cost to finish the job.

This is where professional claim representation becomes vital. A licensed public adjuster does not work for the contractor, and they do not work for the insurance company. They work exclusively for you. Because they are licensed insurance professionals, they can read the technical language of your policy, identify exactly where the desk adjuster is misinterpreting coverage, and present formal arguments using industry standards.

A public adjuster can take over the derailed supplement, evaluate whether the requested items are actually covered under your specific policy, and handle the high level negotiations with the insurance carrier directly. If your home is sitting in disrepair while your builder and your insurer argue over line items, consider getting a free claim review from a licensed public adjuster to determine why the supplement is failing and how to get your project moving again.

Final Thoughts on Mid Repair Negotiations

A successful property restoration relies heavily on the accuracy of the final scope of work. The initial document you receive from the insurance company is almost never the finish line.

💡 Pro Tip: Document everything during the supplement phase. Keep a written log of when the contractor submitted the paperwork and when you followed up with the adjuster. A clear timeline is your best defense against unnecessary delays.

Remember that the goal is a complete and proper restoration of your home. Stay engaged, demand clear explanations from both your contractor and your adjuster, and recognize that you have the right to seek professional representation if the process stalls.

❓ FAQ

📄 What is a supplement on an insurance claim?

It is a formal request for additional money submitted to the insurance company after the initial payout, used to cover hidden damage or required repairs that were left off the first estimate.

🏗️ Does my contractor file the supplement for me?

Yes, your contractor is typically responsible for documenting the extra damage with photos and writing the revised line item estimate to submit to the desk adjuster.

💰 Do I have to pay my deductible again for a supplement?

No. Because a supplement is simply an extension of the exact same incident, your deductible only applies once to the overall claim total.

⏱️ How long does the approval process take?

It can range from a few days for minor corrections to several weeks if the insurer decides to send an adjuster out for a second field inspection.

🛑 Can the insurance company deny a supplement?

Yes. An insurer can deny a supplement if they believe the damage is unrelated to the claim, is due to poor maintenance, or if the contractor failed to provide sufficient photographic proof.

🏠 Will filing a supplement make my premiums go up more?

Generally, a rate increase is tied to the fact that a claim was filed at all, rather than the specific number of supplements added to that single claim file.

🔨 Can the contractor keep working while we wait for approval?

They can, but it is highly risky. If the contractor finishes the work and the insurer subsequently denies the supplement, you will be personally responsible for paying the contractor’s bill.

📸 What kind of proof does the insurance company need?

The insurer requires clear, high resolution photographs of the newly discovered damage in its raw state, along with a written narrative explaining why it must be fixed.

🤷♂️ What if my contractor asks me to pay the difference?

Do not immediately pay out of pocket. A denied supplement is usually a scope dispute, making it the right time to have a public adjuster review the file.

📝 Is a supplemental claim the same thing as a new claim?

No. A new claim is for a separate incident happening on a different date. A supplement just adds required funds to an existing, open claim file.

Understanding the whole process changes how you handle each stage.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

Low offers and scope disputes are common. These explain what to do.

- 5 patterns that signal your settlement is probably short

- Who the adjuster at your door actually works for

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When a denial needs legal leverage, not just negotiation

- Four paths to fight a denial, including one most homeowners miss

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.