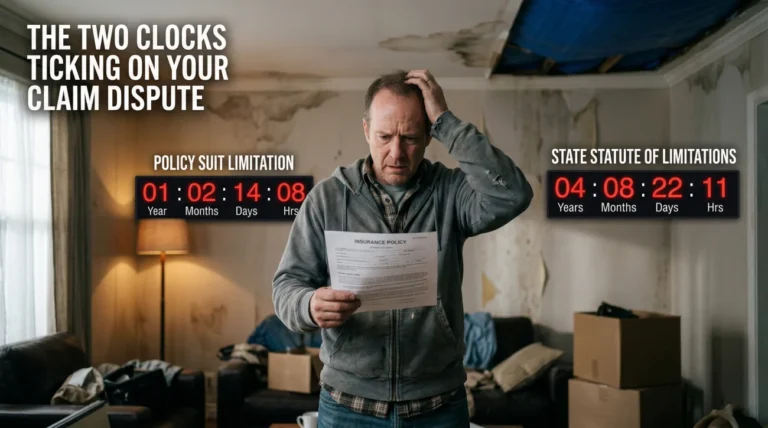

- It is not just about denials: The decision to involve an attorney isn’t only for denied claims; claim size and damage complexity often dictate the need for legal leverage early in the process.

- Large losses face friction: Adjusters handle high volumes of claims. Large dollar amounts (typically over $100k) trigger intense internal scrutiny, multiple reinspections, and routine pushback.

- Multi-system damage requires specialists: Claims involving fire, smoke, and water simultaneously are systematically undervalued by generalist adjusters.

- Early intervention sets the baseline: Bringing in an attorney for a complex claim prevents the insurer from establishing a low initial estimate as the permanent baseline for your settlement.

Beyond the Denial: Why Claim Size and Complexity Change the Rules

When homeowners ask me about escalating a claim, the conversation almost always starts with a denial letter. There is a common misconception that you only need a legal professional when your insurance company flat-out refuses to pay. But after years of reviewing claim files and watching how standard procedures break down, I can tell you that a denial is only one trigger.

In many cases, the sheer size or complexity of the damage is what makes the standard insurance process inadequate. You might have an open, approved claim where the adjuster is perfectly polite, yet you are still bleeding money and losing time because the system is simply not built to handle catastrophic, multi-system losses smoothly without external pressure.

I am not an attorney, and I don’t give legal advice. But I have sat across from insurance representatives on enough large-scale claims to know exactly when a homeowner is outgunned. The reality is that the decision to lawyer up is often a practical response to the economics of the insurance business. When the dollars at stake get high enough, or the damage becomes complex enough, the standard negotiation playbook stops working.

If you are wondering when does a home insurance claim need a lawyer outside of a standard denial, you need to evaluate the structural complexity of your loss. Waiting until a complex claim falls completely apart can limit your options. Let’s walk through the specific claim characteristics that typically indicate you need more than just a standard adjuster assigned to your file.

The Economics of Adjuster Volume on Large Claims

To understand why large claims stall, you have to understand the desk of the person handling it. A typical desk adjuster is managing anywhere from 50 to 100 claims at any given time. Their performance metrics are largely based on file closure rates and minimizing cycle time.

When a $5,000 wind damage claim crosses their desk, it is easy to approve, process, and close. But when a $150,000 major fire or structural collapse lands in their queue, the dynamic shifts entirely. High-dollar claims require management approval, internal auditing, and usually the deployment of multiple independent vendors. The adjuster cannot simply “approve” it to get it off their desk.

One of the most consistent patterns I observe in large-loss files is the ‘delay by vendor’ tactic. Instead of processing the claim, the desk adjuster will send an engineer, then a week later send a hygienist, then two weeks later request a forensic accountant. The claim doesn’t get denied – it just gets buried in operational friction because the dollar amount demands intense internal scrutiny.

Because these claims are heavily audited, adjusters are financially incentivized to scrutinize every line item. This is where you start seeing depreciation applied excessively, line items for debris removal heavily capped, and structural repair scopes arbitrarily chopped down. The complexity of the claim inherently puts you at odds with the carrier’s volume-based business model.

This dynamic is exactly why understanding the general overview of when legal help makes sense is so critical. It is rarely a case of a cartoonish villain refusing to pay; it is usually a massive corporation applying standard operating procedures to a uniquely devastating loss.

Total Loss Claims: When the Math Gets Aggressive

A total loss, where the home is completely destroyed by fire, tornado, or hurricane, is perhaps the most glaring example of a claim that demands immediate, specialized attention. You would think a total loss is simple: the house is gone, so they write a check for the policy limit, right? In my experience, it is almost never that straightforward.

A total loss home insurance claim lawyer is often necessary because the math involved in these settlements is highly susceptible to manipulation. Insurers will look for ways to reduce the payout even when the structure is a pile of ash.

| Standard Claim Friction | Total Loss Claim Friction |

|---|---|

| Arguing over the cost of 5 squares of roofing shingles. | Disputing the cost of clearing massive debris and toxic material from the foundation footprint. |

| Calculating standard depreciation on a 5-year-old appliance. | Attempting to separate “land value” from structure value to artificially lower the Replacement Cost Value (RCV). |

| Matching the color of replacement siding. | Forcing you to re-create a complete inventory of every single item you owned from memory while displaced. |

One of the biggest hurdles in a total loss is the distinction between Actual Cash Value (ACV) and Replacement Cost Value (RCV). Insurers will hold back massive amounts of money as depreciation, paying you only the ACV upfront. To unlock the rest, you have to prove you are rebuilding. But if the ACV check is too small to even start construction, you are trapped. An attorney who understands large loss mechanics can intervene to challenge excessive depreciation and force the release of funds necessary to actually begin the recovery process.

⚠️ Warning: Never accept an adjuster’s verbal assurance that a total loss will simply “max out your limits.” Until you have a written settlement breakdown detailing exactly how the dwelling, other structures, personal property, and debris removal coverages are being applied, assume the numbers will be contested.

Multi-System Damage: The Danger of the Generalist Adjuster

When I review scopes of loss, the ones with the largest financial gaps are almost always multi-system damage claims. Think of a severe house fire: you don’t just have fire damage. You have smoke and soot damage throughout the HVAC system, and you have massive water damage from the fire department extinguishing the blaze, which rapidly leads to mold.

The insurance company will typically send one general field adjuster to assess this. But a general adjuster is not an industrial hygienist, they are not a structural engineer, and they are not a water mitigation specialist. Because they lack the expertise to accurately scope the interconnected damage, they systematically under-scope it.

Allowing the single field adjuster to write a combined estimate for fire, smoke, and water, assuming they captured the hidden complexities of structural drying and soot encapsulation.

Demanding separate, specialized assessments for each damage type, and heavily considering a multi-system home damage attorney to compel the insurer to accept estimates from independent, credentialed experts.

In these scenarios, the intersection between different policy coverages creates intense disputes. The insurer might try to cap the water damage payout by claiming it falls under a specific sub-limit, or they might refuse to pay for HVAC duct replacement by arguing that a simple cleaning is sufficient for the soot. A legal advocate can dissect the policy language to ensure each system is treated with the appropriate coverage limits without being unfairly capped. And ensuring these limits are maximized becomes even more critical when you cannot even live in the house during the dispute.

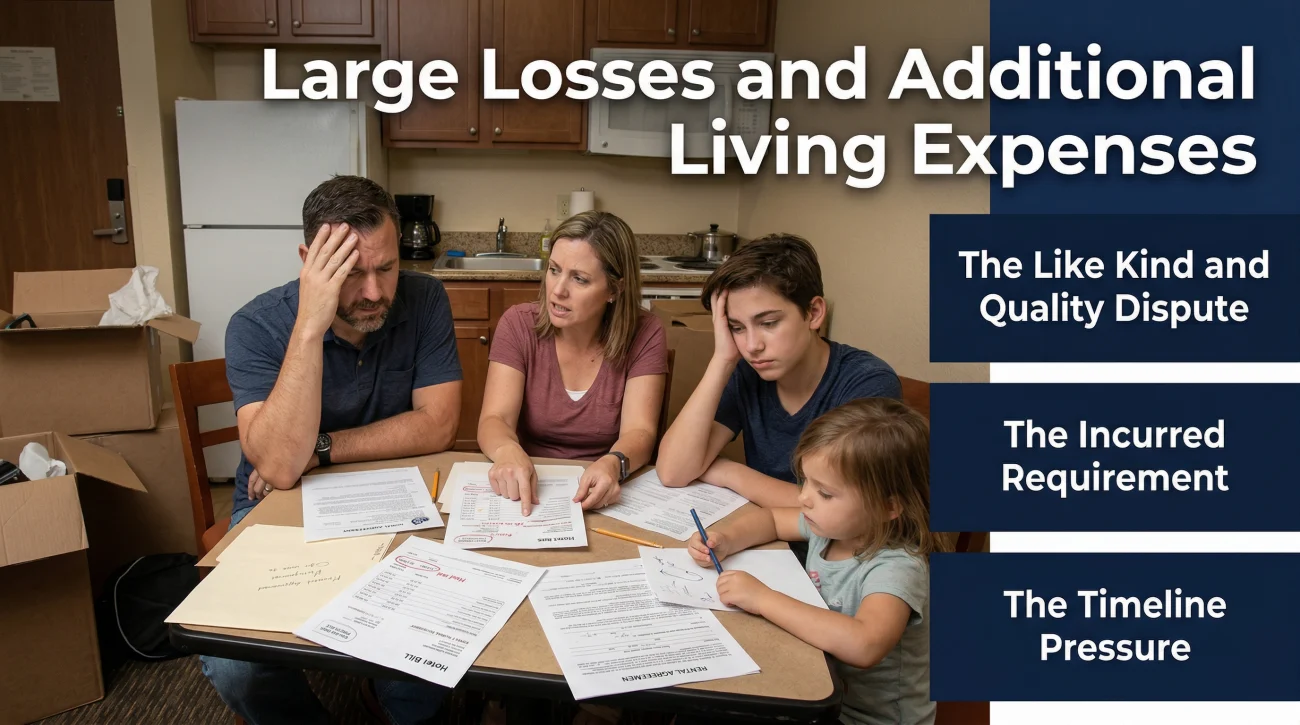

Large Losses and Additional Living Expenses (ALE)

If your home has suffered severe damage, you are not living in it. You are displaced, which brings Additional Living Expenses (ALE) or Loss of Use coverage into play. For a minor claim, staying in a hotel for a week is a non-issue. But for a large loss, you might be out of your home for 12 to 18 months.

Insurers heavily scrutinize long-term ALE claims. The policy typically states they will cover the increased cost of living to maintain your “normal standard of living.” However, what you consider normal and what the desk adjuster considers normal rarely align.

- 👉 The “Like Kind and Quality” dispute: If you lived in a four-bedroom house with a yard, the insurer might try to force you into a two-bedroom apartment for a year to save money.

- 👉 The “Incurred” requirement: Insurers often refuse to advance ALE funds, forcing you to pay out of pocket for an expensive rental and submit receipts for reimbursement, causing a massive financial strain on your family.

- 👉 The timeline pressure: As the 12-month mark approaches, adjusters frequently use the impending expiration of ALE benefits as leverage to force you into a lowball settlement on the main dwelling claim. I have seen carriers intentionally drag out structural estimates for months, knowing that once your temporary housing money runs out, you will be desperate enough to sign a release just to get repair funds flowing.

When the ALE component alone reaches tens of thousands of dollars, it becomes a major point of negotiation leverage. If you feel the insurer is using your displacement to pressure your decision-making, it is a strong indicator that the claim complexity has crossed the threshold where professional intervention is required.

Signs Your Claim Has Outgrown the DIY Approach

There is a distinct turning point in complex claims where negotiation stops being collaborative and starts becoming adversarial. I call this the friction phase. If you are handling a massive claim yourself, you need to recognize the operational signals that the insurer has moved into defensive mode.

Here are the specific claim characteristics and insurer behaviors that indicate the carrier is building a defensive file against you, requiring an immediate professional response:

1. The estimate gap exceeds $100,000

If the insurer’s initial estimate comes in at $60,000, but your licensed general contractors are quoting $180,000 for the exact same scope of work, you do not have a minor pricing disagreement. You have a fundamental dispute over the scope of the reality of the damage. A gap this large is rarely bridged through polite phone calls.

2. Multiple reinspections by new “experts”

If the carrier sends a field adjuster, then an engineer, then a third-party consultant, they are usually building a file to justify a minimized payout or a partial denial. They are not looking for more ways to pay you; they are gathering evidence to limit their liability.

3. You are asked to submit to an Examination Under Oath (EUO)

This is a massive red flag. If an adjuster requests this, you are stepping into a formal, legally binding environment. You are contractually obligated to cooperate, but you should never submit to an examination under oath without legal representation. It means the insurer’s special investigations unit or legal department is now heavily involved.

4. The cause of loss is being subtly shifted

If a windstorm tore off your roof, but the adjuster’s notes keep referencing “long-term wear and tear” or “maintenance issues,” they are setting the stage to apply an exclusion. The moment the terminology shifts from sudden damage to gradual deterioration, the complexity of your claim has escalated dramatically.

Key Point: Recognizing the administrative signs of a troubled claim early can save months of frustration. If your adjuster is building a defensive file, you need someone building a stronger offensive file.

💡 Pro Tip regarding Public Adjusters: For large claims where the dispute is strictly about valuation and the scope of repairs (and the insurer agrees the damage is covered), a Public Adjuster can be incredibly effective. However, if the insurer is twisting policy language, threatening EUOs, or creating massive, unexplained delays, the situation has likely moved into legal territory.

When Hidden Damage Makes the Attorney Non-Negotiable

Sometimes, the damage itself is so difficult to prove or so heavily restricted by policy caps that attempting to navigate it alone is a financial risk. In my claim reviews, certain types of damage almost always benefit from someone who knows how to build a legally unassailable file.

Extensive Mold and Hidden Moisture: Mold claims are notoriously difficult. Most policies have strict, low sub-limits for mold (often capped at $10,000). However, if the mold was the direct result of a covered water peril (like a burst pipe) and the insurer delayed mitigation, a skilled representative can often argue that the mold damage should be covered under the main dwelling limit as ensuing damage, bypassing the cap. This requires sophisticated policy interpretation.

Structural Integrity and Foundation Issues: If a fire, tornado, or heavy impact damages the structural integrity of the home, insurers love to offer cosmetic fixes. They will offer to replace the drywall while ignoring the compromised framing behind it. Proving hidden structural damage requires coordinating structural engineers and ensuring their reports are formatted to meet the strict evidentiary standards of the policy.

In a recent severe wind claim I reviewed, the carrier offered $15,000 for missing roof shingles and stained ceiling drywall. They completely ignored that the roof trusses were visibly uplifted. We had to bring in an independent structural engineer to prove the entire roof system was compromised, which ultimately changed the accepted scope to an $85,000 repair. The desk adjuster simply wasn’t qualified to recognize structural failure.

The Early Advantage: What Attorney Involvement Actually Does

One of the biggest mistakes I see homeowners make on a six-figure claim is thinking, “I’ll just see what the insurance company offers first, and if it’s bad, I’ll hire a lawyer.”

Here is why that is dangerous on a complex loss: The insurer’s first estimate becomes the anchor. It establishes the baseline narrative for the claim. Once an insurer formally documents that a roof only needs patching, it takes ten times the effort to force them to admit it needs a full replacement.

Subject: Confirmation of Claim #123456 Communication Protocol

Hello [Adjuster Name],

As my claim involves severe structural and multi-system damage, please note that moving forward, all requests for information, scope modifications, and settlement offers must be provided in writing. We will be compiling independent engineering assessments before accepting any partial scope of loss.

When you involve a professional early, they control the narrative. They ensure the independent experts are brought in before the insurer locks in a lowball estimate. If you want to understand what an insurance attorney actually does behind the scenes, it largely comes down to this: they build a parallel, evidence-based file that the insurer cannot easily dismiss, preventing bad faith tactics before they start.

The Cost of Waiting on a Complex Claim

Handling a minor insurance claim yourself is entirely reasonable. But when you are dealing with a total loss, multi-system damage, or a massive gap in repair estimates, the DIY approach becomes a liability. The insurance company has teams of adjusters, engineers, and corporate attorneys actively working to minimize their financial exposure to your disaster.

Every month that passes without a proper scope of loss is a month your property deteriorates and your temporary housing funds drain. The longer you wait to balance the scales, the harder it becomes to undo the carrier’s narrative.

Because property damage attorneys usually work on a contingency basis, you do not need to pay upfront hourly fees to protect your investment. If you are exhausted by the friction of a large claim, the smartest and most urgent next step is to get an evaluation from a legal professional who handles complex property damage to stop the delays and force a fair resolution.

❓ FAQ

🏠 How big does my claim need to be to hire an attorney?

While there is no strict legal minimum, attorneys generally add the most value to claims where the disputed amount exceeds $50,000 to $100,000, or in cases of a total loss. For very small disputes, the economics of hiring legal representation may not make sense.

⚖️ Do I need a lawyer if the insurance company hasn’t denied my claim yet?

You do not need to wait for a denial. If your claim is experiencing massive, unexplained delays, multiple new adjusters, or severe underpayment on a large loss, an attorney can intervene to force the process forward before a denial happens.

🔥 Does multi-system damage always require an attorney?

Not always, but claims involving fire, smoke, and water simultaneously are highly prone to being under-scoped by general adjusters. If the carrier refuses to send specialized experts (like industrial hygienists), legal leverage is often required.

📉 Can a lawyer help if the insurance estimate is just way too low?

Yes. A massive gap between your contractor’s quote and the insurer’s estimate is a scope dispute. Attorneys handle this by coordinating independent engineers and experts to legally challenge the insurer’s valuation.

🏨 What if the insurance company cuts off my temporary housing (ALE)?

If an insurer prematurely cuts off Additional Living Expenses while your home is still unlivable, this is a strong trigger for legal intervention. An attorney can challenge the termination of benefits based on the policy’s fair use requirements.

🛑 Why does the insurance company keep sending different inspectors?

In many cases, sending multiple engineers or inspectors on a large claim is a tactic to find an expert opinion that justifies a lower payout. This is a major red flag that your claim has become complex and needs professional oversight.

🕵️♂️ Should I get a lawyer if they ask for an Examination Under Oath?

Yes, absolutely. An EUO is a formal legal proceeding where you are questioned under oath by the insurance company’s attorney. You should never attend an EUO without your own legal representation.

💰 How do I pay for a lawyer if I just lost my house?

Most property insurance attorneys work on a contingency fee basis. This means they do not charge upfront hourly rates; instead, they take a percentage of the final settlement they recover for you.

⏳ Does hiring a lawyer make the claim take longer?

It can extend the timeline compared to simply accepting a lowball offer today. However, for a stalled or complex claim, an attorney’s involvement often breaks the administrative bottleneck and forces a proper resolution.

🚫 Will my insurance company drop me if I hire a lawyer?

Insurance companies typically non-renew policies based on the frequency and severity of claims, or regional risk changes, not specifically because you hired legal representation to enforce your current contract.

Most disputes start with a payout disagreement. These cover the earlier stages.

- The claim lifecycle a PA or attorney works inside

- The policy language that determines what professional help can recover

- How damage classification affects what an expert can negotiate

- Whether the situation you have justifies bringing in outside help

- When a denial is the outcome a PA could have prevented

- What a public adjuster actually does inside a claim

- When the dispute has moved past what a PA can handle

Two paths, two different situations. These clarify which one fits yours.

- How to tell if your situation actually warrants hiring one

- The difference between the adjuster you hired and the one who showed up

- When water damage scope gaps make independent review necessary

- When fire damage complexity makes independent representation worth it

- When the gap between estimates is large enough to bring in a PA

- When bad faith makes legal action the only path that works

- PA, attorney, or appraisal clause: which path fits your denial

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.