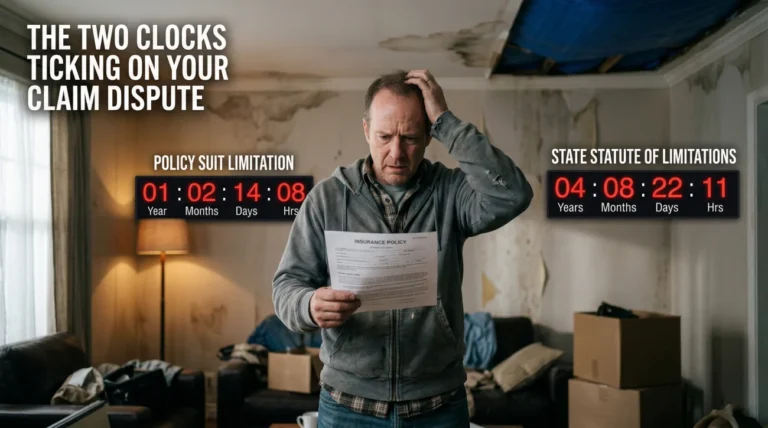

- An Examination Under Oath (EUO) is a formal, legally binding proceeding where you answer questions from the insurer’s representative while under penalty of perjury.

- It is not the same as a casual recorded phone statement. The transcript becomes official evidence in your claim file.

- Most standard homeowners policies contain a cooperation clause that requires you to attend. Refusing to participate can give the insurer legal grounds to deny your claim entirely.

- You have the absolute right to have an attorney present during the questioning to protect your rights and object to improper tactics.

The Reality of an Examination Under Oath

Receiving a formal letter scheduling a home insurance examination under oath is one of the most stressful moments in the claims process. The very phrase sounds intimidating. You immediately wonder if you are being accused of insurance fraud, if you did something wrong, or if your claim is about to be denied.

In my experience reviewing claim files and adjuster logs, I understand exactly why this notice causes panic. However, it is vital to take a breath and look at the situation objectively. If your insurer schedules this proceeding, you are not necessarily being accused of a crime. You are, however, entering a highly formal phase of the investigation.

I have seen these examinations used simply because a loss was very large and the insurer wanted to lock down the facts. I have also seen them used strategically to overwhelm homeowners with intrusive financial questions or to build a documented case for a denial. Knowing exactly what this process entails, what your obligations are, and when you need professional backup is the best way to protect your settlement.

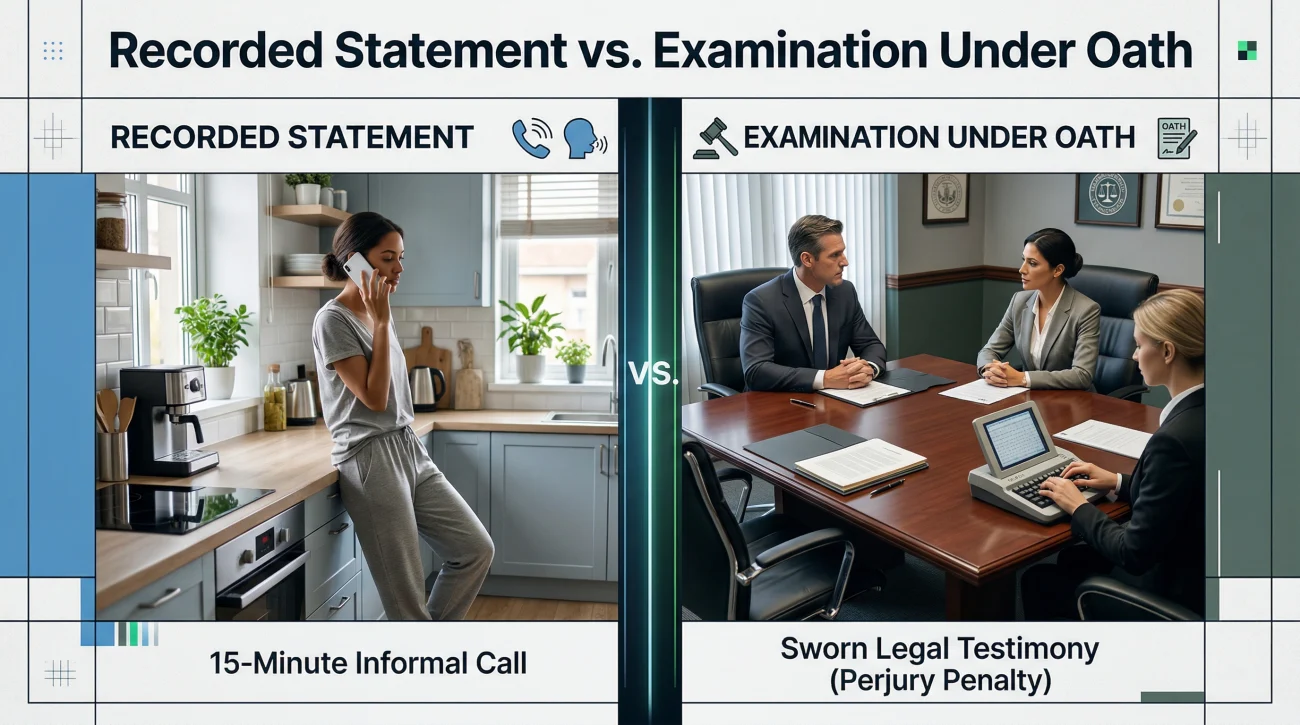

What Makes the EUO Different from a Recorded Statement?

Many homeowners confuse this process with the recorded statement they gave over the phone the day they reported the damage. They are entirely different tools.

A standard recorded statement is usually a brief phone call with an adjuster to get the basic facts of the loss. An EUO is a formal legal proceeding. It is typically conducted in person at a conference room or via an extended video call. An attorney hired by the insurance company usually asks the questions, and a certified court reporter types every single word spoken into an official transcript.

Key Point: You are placed under oath before the questioning begins. This means you are answering under penalty of perjury. The transcript becomes a permanent piece of evidence that is fully admissible in court if your claim ever escalates to a lawsuit.

A 15-minute phone call covering the basic “who, what, when, and where” of the incident shortly after it happens.

A formal session lasting several hours, led by an attorney, exploring your claim, your financial history, and your background in meticulous detail.

Why Insurers Schedule These Proceedings

Insurance companies do not request an examination under oath for a standard wind-damaged fence or a simple appliance leak. Hiring a lawyer and a court reporter costs the insurer money. They reserve this tool for specific situations where they feel the need to investigate deeper.

The most common triggers include large dollar claims. If your home suffered a massive fire or a total loss, the sheer financial exposure often prompts the insurer to verify every detail under oath. Complex facts also trigger this process. If the timeline of a water leak is unclear, or if there is a dispute about whether damage occurred in one event or multiple events, the insurer will use the questioning to clarify the narrative.

I have read transcripts where the entire proceeding was triggered simply because the homeowner gave two slightly different dates for a plumbing failure during initial phone calls. The insurer used the formal setting to lock the homeowner into a single, binding timeline.

Another major trigger is suspicion of material misrepresentation. If the insurer suspects that personal property inventories are inflated, or if they are looking for a financial motive behind a fire, they will schedule this proceeding to dig into your personal finances.

The Cooperation Clause and Your Obligations

The most frequent question I am asked is whether a homeowner can simply refuse to participate. The short answer is no, not without severe consequences.

Virtually every standard homeowners insurance policy (often called an HO3 policy) contains a section titled “Duties After Loss.” Within that section is a cooperation clause. This clause explicitly states that you must cooperate with the insurer’s investigation, show them the damaged property, provide requested documents, and submit to an examination under oath as often as they reasonably require.

⚠️ Warning: Refusing to attend, or walking out halfway through the questioning, is generally considered a material breach of the insurance contract. If you breach the contract, you hand the insurance company immediate legal grounds to deny your claim completely, regardless of how valid the physical damage might be.

The Intrusive Document Requests

Beyond your obligation to attend, the insurer will also demand something else before you even sit down in the room. You will receive a document production request, which is often where homeowners feel their privacy is being severely invaded. The insurer is permitted to ask for documents that are relevant to their investigation.

For a standard property damage claim, they might just ask for repair estimates, receipts for damaged items, and contractor correspondence. However, if they are investigating a potential financial motive, the requests become incredibly personal. They are looking for evidence of financial distress that might suggest a reason to intentionally cause the loss.

1. Tax returns and bank statements (to check for massive debt or impending bankruptcy).

2. Credit card statements (to identify maxed-out accounts or unusual spending leading up to the loss).

3. Cell phone records and logs (to verify your physical location at the exact time a fire or leak started).

4. Mortgage statements (to see if you were facing foreclosure or default notices).

While this feels highly intrusive, courts have historically allowed insurers broad leeway in requesting financial documents if there is a valid reason to investigate the circumstances of the loss. Gathering these documents thoroughly and accurately is a critical part of the preparation process.

What Actually Happens in the Room

When the day arrives, the atmosphere is formal. The insurance company’s attorney will ask you questions while the court reporter records the dialogue. The questioning can last anywhere from two hours to an entire day, depending on the complexity of your claim.

They will walk you through the day of the loss chronologically. They will ask you to confirm details on the documents you provided. They will ask about your prior insurance history, whether you have had claims with other companies, and details about the maintenance history of your home.

| Topic Area | What They Are Looking For |

|---|---|

| The Incident Timeline | Inconsistencies in your story or timeline gaps that might trigger policy exclusions. |

| Property Value | Evidence that you inflated the value of personal items or submitted receipts that do not match the claim. |

| Financial Background | Signs of financial distress (bankruptcy, foreclosure, heavy debt) that could suggest a motive for insurance fraud. |

The key to surviving this phase is absolute honesty. It is perfectly acceptable to say “I do not know” or “I do not remember.” Guessing answers to please the attorney is the fastest way to damage your credibility and your claim.

Your Rights During the Proceeding

While the insurer holds significant leverage through the cooperation clause, you have distinct rights that you must exercise to protect yourself.

First and foremost, you have the right to have an attorney present. I always strongly suggest utilizing this right. You also have the right to take breaks during the questioning if you become fatigued or need to consult with your legal representative.

After the session is over, the court reporter will type up the transcript. You have the right to read the transcript, correct any typographical errors or clarify misstatements, and sign it before it becomes official. Always request a copy of your transcript for your own records so you know exactly what evidence the insurer is evaluating. Exercising these rights is essential, especially when the investigation starts crossing the line from fact-finding to intimidation.

Signs the Process Is Going Off Track

Not every examination under oath is a routine fact-finding mission. Sometimes, it is a tactic. In my reviews of complex claim timelines, I watch for specific patterns indicating the insurer is using the process unfairly.

- The insurer schedules the formal questioning only after completing three or four physical inspections of your property without issuing a single payment.

- The document request is impossibly broad, asking for decades of financial records that have no clear relevance to a simple roof leak.

- The insurer schedules the proceeding but gives you less than a week to gather years of complex financial documents, setting you up to fail the cooperation requirement.

- The insurance attorney attempts to dictate whether your own legal representative can speak, object, or properly advise you during the session.

- The insurer has gone completely silent for weeks, only to suddenly issue a demand right as you threaten to file a formal complaint.

When insurers use procedural tools purely to delay payment or harass a policyholder, they cross a line. Recognizing these patterns is crucial because they are often the exact behaviors that lay the groundwork for a homeowners insurance bad faith lawsuit down the road.

What If the Proceeding Is Rescheduled or Canceled?

Occasionally, an insurer will issue a formal demand and then abruptly postpone or cancel it. Homeowners are often left wondering what this shift means for their claim.

If the insurer cancels the session entirely after you have provided your requested documents, it generally means their questions were answered by your paperwork. They found the verification they needed and realized hiring an attorney for a formal session was no longer cost-effective. This is usually a positive sign.

However, if they continuously reschedule the date, pushing it back weeks or months at a time, this can be a stalling tactic. They maintain the threat of the examination to keep the claim open without actually moving toward a settlement or a formal denial. If you find yourself trapped in a cycle of rescheduling, it is a clear signal that the claim has stalled.

The Aftermath: What Happens Following the EUO?

The conclusion of the questioning does not mean you will get a check the next day. The aftermath follows a specific timeline that requires patience.

First, it typically takes a week or two for the court reporter to produce the official transcript. You and your legal representative will then have a set period to review it, submit corrections, and sign it. The insurer’s attorney will then write a summary report for the adjuster, evaluating your credibility and highlighting any policy violations discovered during your testimony.

Based on that report, the claim will move in one of three directions. The insurer may lift their reservations and proceed to pay the claim. They may issue a partial payment based on what they were able to verify. Alternatively, if they found inconsistencies or believe you breached a policy condition, they will issue a formal denial letter citing specific pages from your sworn transcript.

The Role of Legal Representation

Going into a sworn legal proceeding alone against an experienced insurance attorney is a profound mismatch. The insurance attorney knows the policy language intimately and knows exactly how to phrase questions to elicit answers that benefit the insurance company.

This is where understanding when you need a lawyer for your insurance claim becomes a practical reality rather than just an abstract concept. An attorney representing you acts as a necessary shield against this power imbalance. They will review your documents before you hand them over to ensure you are complying with the request without volunteering irrelevant personal data. During the session itself, your legal representative can object to questions that are abusive, repetitive, or completely outside the scope of the claim. They ensure the record remains clean and that the insurer’s attorney plays by the rules. Learning what a home insurance attorney actually does during these sessions helps clarify why their preparation and guidance are so valuable for complex losses.

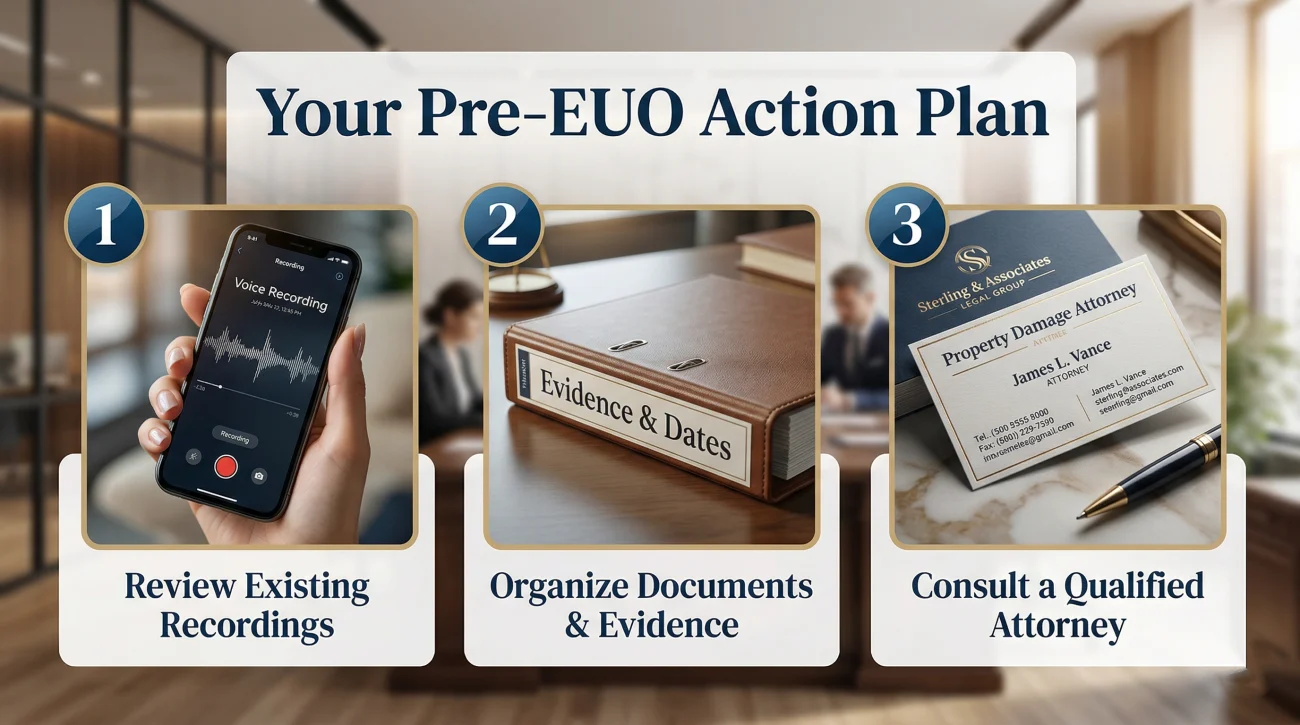

A Practical Pre-EUO Checklist

If you have received a demand letter for an examination under oath, your preparation must begin immediately. Do not treat this as a casual meeting. Use this practical checklist to protect your claim before you ever step into the room.

- Review your initial recorded statement: Request a copy or a transcript of the very first call you made to report the claim. The opposing attorney will have it memorized, and they will look for any deviations in your current story.

- Cross-reference all dates: Ensure the timeline on your contractor estimates, your receipts, and your personal memory all align perfectly. Conflicting dates are the easiest way for an insurer to build a misrepresentation case.

- Do not contact the adjuster unilaterally: Once the demand is issued, do not call your adjuster trying to explain things off the record to make the proceeding go away. Anything you say can be used against you, and it bypasses the formal legal process that has now started.

- Consult an attorney early: Do not wait until the day before the session. If your insurer has escalated the claim to this level, getting a free consultation with a property damage attorney at least a week in advance is the smartest move. They can review your notice and assess the insurer’s motives.

Given the legal weight of a sworn transcript, facing this alone puts your settlement at severe risk. Let a professional ensure you do not inadvertently jeopardize your coverage while sitting across the table from the insurance company’s lawyer.

❓ FAQ

⚖️ What is examination under oath insurance?

It is a formal legal proceeding where a homeowner answers questions from the insurance company’s attorney under penalty of perjury to verify the facts of a claim.

📝 How is an EUO home insurance claim different from a recorded statement?

A recorded statement is usually a short phone call with an adjuster. An EUO is a formal, in-person session recorded by a court reporter and carries the legal weight of sworn testimony.

🛑 Can I refuse examination under oath insurance?

While you physically can refuse, your policy requires your cooperation. Opting out gives the insurer a direct contractual reason to close your file without paying.

❌ What happens if you refuse EUO insurance?

The insurer will likely issue a formal denial letter stating that you failed to comply with the “Duties After Loss” section of your policy, effectively ending your claim.

🛡️ What are my examination under oath rights homeowners should know?

You have the right to have your own attorney present, the right to take breaks during questioning, and the right to review and correct the written transcript afterward.

💼 Do I need an attorney for examination under oath insurance?

While not legally required, it is highly recommended. The insurer will have an experienced attorney asking the questions, and having your own legal representation protects your rights.

🕵️ Why would my insurance company request an EUO?

Insurers request them for large dollar claims, when facts are highly complex, when timelines conflict, or if they suspect material misrepresentation or fraud.

📄 Do I have to provide tax returns for an insurance EUO process homeowners?

If the insurer is investigating a potential financial motive for the loss, courts generally allow them to request tax returns and bank statements as part of the document production.

⏳ How long does an examination under oath take?

It depends entirely on the complexity of the claim. It can last anywhere from a couple of hours for a straightforward issue to a full day for massive total loss events.

🗣️ What if I don’t know the answer during the questioning?

The best and safest response is to simply state that you do not know or do not remember. You should never guess or speculate while under oath.

Most disputes start with a payout disagreement. These cover the earlier stages.

- The claim lifecycle a PA or attorney works inside

- The policy language that determines what professional help can recover

- How damage classification affects what an expert can negotiate

- Whether the situation you have justifies bringing in outside help

- When a denial is the outcome a PA could have prevented

- What a public adjuster actually does inside a claim

- When the dispute has moved past what a PA can handle

Two paths, two different situations. These clarify which one fits yours.

- How to tell if your situation actually warrants hiring one

- The difference between the adjuster you hired and the one who showed up

- When water damage scope gaps make independent review necessary

- When fire damage complexity makes independent representation worth it

- When the gap between estimates is large enough to bring in a PA

- When bad faith makes legal action the only path that works

- PA, attorney, or appraisal clause: which path fits your denial

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.