- Most home insurance attorneys work on a contingency fee basis, meaning you pay no upfront hourly rates and they only get paid if you receive a settlement.

- Attorney fees are typically calculated as a percentage of your total recovery or a percentage of the “new money” they secure above the insurer’s initial offer.

- Case expenses, such as hiring independent structural engineers or court filing fees, are usually billed separately from the attorney’s percentage fee.

- The contingency model makes legal representation accessible, but the math does not always favor the homeowner on very small claims.

- Before signing a retainer, you must clearly understand how the fee is calculated and whether expenses are deducted before or after the fee is applied.

The True Cost of Legal Help in Property Claims

The biggest reason homeowners hesitate to hire an insurance attorney is the fear of the final bill. When your home is damaged, your finances are already stretched thin. The thought of paying a lawyer five hundred dollars an hour to fight your insurance company feels impossible. In my experience working around hundreds of property claims, I see homeowners walk away from thousands of dollars in legitimate coverage simply because they assume legal help is completely unaffordable.

That assumption is usually based on a misunderstanding of how property damage attorneys actually charge for their services. Unlike divorce lawyers or corporate counsel who bill by the hour, most attorneys who handle homeowners insurance disputes use a contingency fee model. This structure is designed specifically for people who are facing sudden financial hardship due to property loss.

Understanding exactly how a home insurance attorney contingency fee works is critical. It shifts the dynamic entirely. Instead of viewing legal representation as a luxury you cannot afford, you can evaluate it as a business decision based on simple math. This guide will walk you through the mechanics of attorney fees, what percentages are typical, and how to read a retainer agreement so you know exactly what your net recovery will look like.

How the Contingency Fee Model Works

A contingency fee means the attorney’s payment is contingent upon a successful outcome. This is fundamentally different from a traditional hourly retainer model, where you must pay a large upfront deposit and the attorney bills hundreds of dollars per hour against it regardless of whether you win or lose. With a contingency agreement, there are no upfront retainers to pay and no monthly invoices for hours billed.

The attorney simply takes a predetermined percentage of the settlement or court award they recover for you. If they do not recover any money from the insurance company, you typically owe them nothing for their time.

This model aligns the attorney’s financial interests directly with yours. Because they are absorbing the risk of working for free if the case fails, they are highly motivated to maximize your settlement and resolve the claim efficiently.

When I review claim files that have stalled for months, the tone of the insurer’s correspondence often changes the moment a formal letter of representation arrives. The contingency model levels the playing field, allowing a homeowner with limited cash to bring the exact same legal pressure that the insurance company brings to the table.

However, the phrase “percentage of recovery” can mean several different things depending on the contract you sign. Before you commit, you must understand exactly what pool of money that percentage is being applied to.

What the Percentage is Actually Applied To

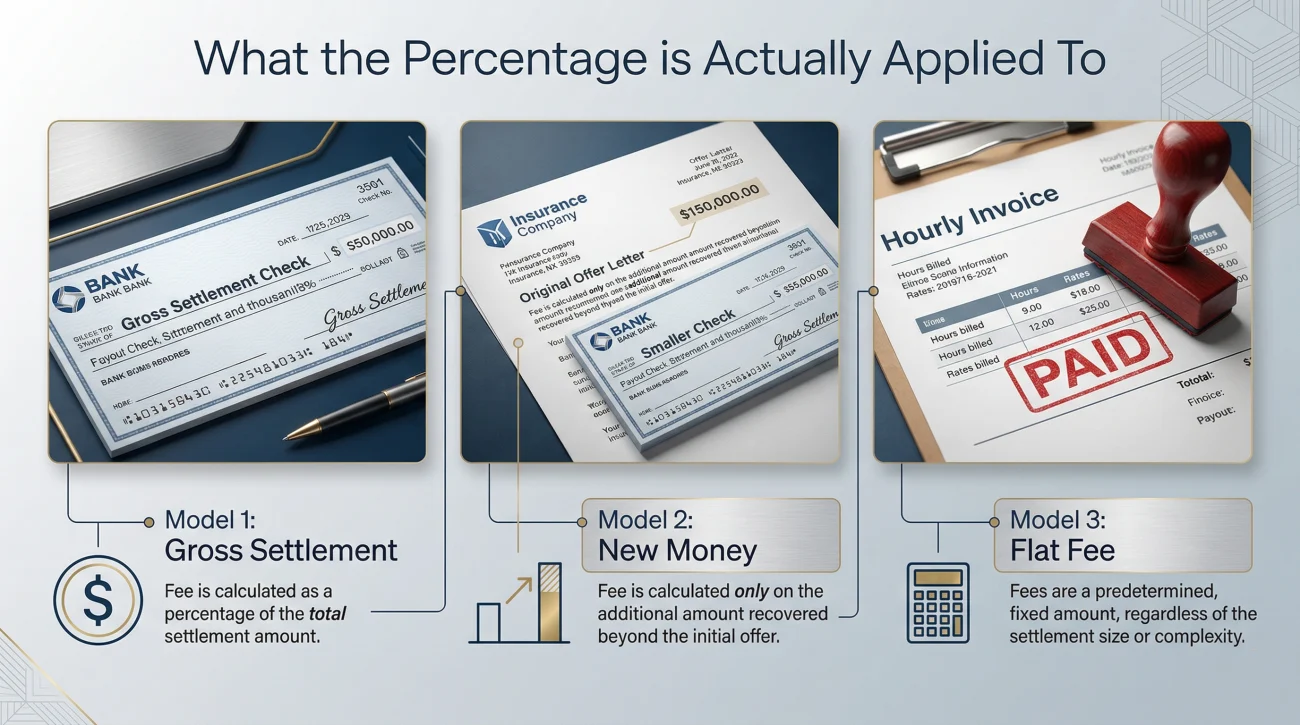

There are three common ways an insurance claim lawyer gets paid under a contingency agreement. The method your attorney uses will drastically affect your final payout.

Model 1: Percentage of the Total Gross Settlement

In this model, the attorney takes a percentage of the entire gross settlement amount. For example, if the insurance company eventually pays out a total of $100,000 for a fire claim, the attorney takes their percentage from that full $100,000. This is the most straightforward calculation, but it can be frustrating if the insurer had already offered you $60,000 before you even hired the attorney.

Model 2: Percentage of New Money Only

Many property damage attorneys prefer a “new money” structure. Here, the attorney’s percentage only applies to the funds they recover above the insurance company’s last undisputed offer. If the insurer offered you $60,000 and the attorney negotiates the final settlement up to $100,000, the attorney only takes a percentage of the $40,000 difference. Homeowners often prefer this model because it guarantees the attorney is only being compensated for the specific value they added to the claim.

Model 3: Flat Fee for Specific Services

While less common for full claim disputes, some attorneys will charge a flat fee for isolated tasks. This might include a flat rate to draft a formal demand letter, review your policy language, or attend an Examination Under Oath with you. This is usually reserved for very specific, limited-scope representation.

Assuming all contingency fees are identical and signing the retainer without asking which pool of money the percentage applies to.

Asking the attorney to clarify in writing whether their fee applies to the gross settlement or only to the new money recovered above your current offer.

Typical Percentage Ranges

There is no universal, legally mandated percentage for property damage claims. The rate typically ranges widely based on the overall size of the claim, the complexity of the dispute, and the stage at which the case resolves. State bar associations often have rules requiring fees to be “reasonable,” but that leaves room for variation.

Often, retainer agreements include a tiered percentage scale. For instance, the fee might be set at one percentage if the claim is settled through basic negotiation, a higher percentage if a formal lawsuit must be filed, and the highest percentage if the case actually goes all the way to a jury trial. The fee increases as the attorney’s time commitment and financial risk increase.

It is worth noting that bad faith claims may involve a different fee structure. Your attorney will explain what applies to your situation. For a broader view of when a home insurance claim attorney is the right tool versus when negotiation is sufficient, you have to weigh these potential fee tiers against your expected payout.

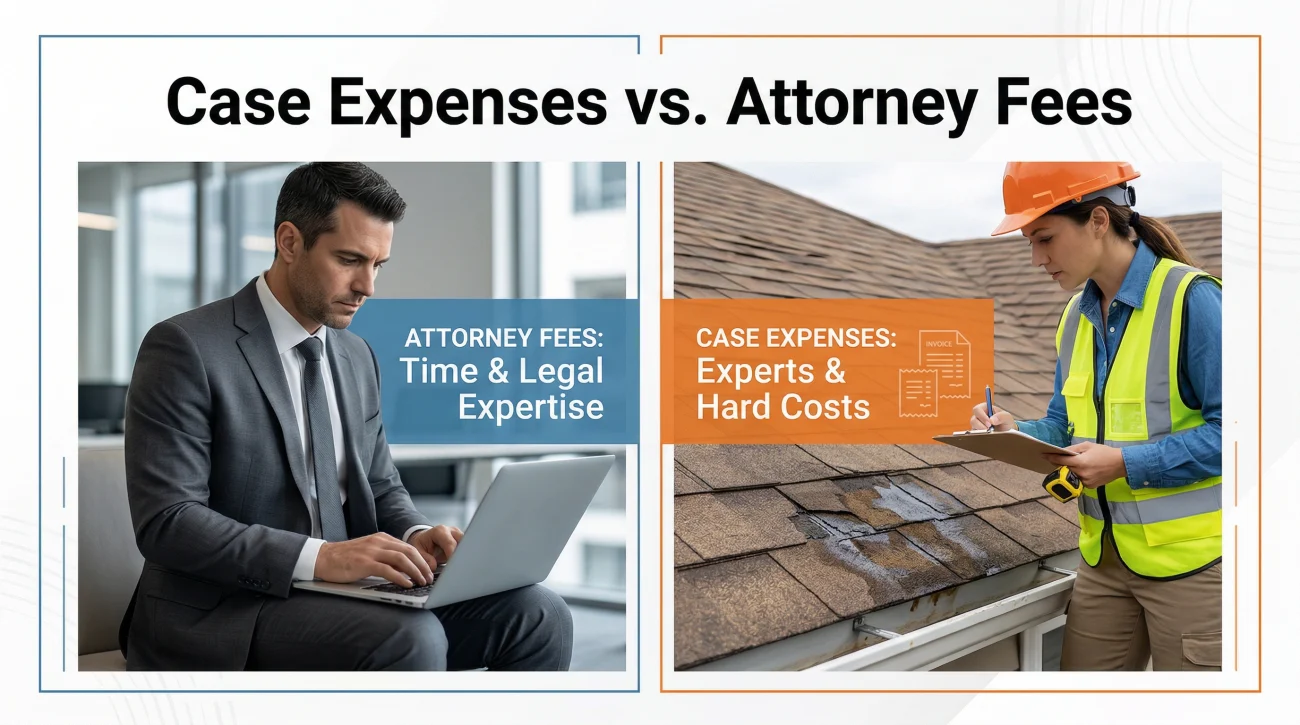

Case Expenses vs. Attorney Fees

This is the area that causes the most confusion for policyholders. Attorney fees and case expenses are two completely separate things.

The contingency fee covers the attorney’s time, legal expertise, and office overhead. However, fighting a complex property claim often requires outside resources. You may need an independent structural engineer to prove a roof cannot be repaired, a forensic meteorologist to verify wind speeds, or an industrial hygienist to test for toxic mold. There are also hard costs like court filing fees and deposition transcript costs.

Warning: Case expenses are almost always the responsibility of the homeowner. Most attorneys will front these costs during the litigation process, but they will deduct the accumulated expenses from your final settlement check.

You need to look closely at your agreement to see exactly how expenses are deducted. If your attorney deducts the case expenses from the gross settlement before calculating their percentage, you take home more money. If they calculate their percentage first and then deduct expenses from your portion, your net payout shrinks.

The Math: Gross Settlement vs. New Money

To understand the financial reality, let us look at a hypothetical scenario. Imagine you have a severely underpaid water damage claim. The insurance company’s initial offer was $30,000. Over the course of a year, the attorney hires a moisture mapping expert and eventually secures a final settlement of $90,000.

Here is how the two different fee models impact your actual take-home money assuming a 33 percent fee.

Scenario A: The “New Money” Model

| Item Description | Amount |

|---|---|

| Initial Insurer Offer (Already paid to you) | $30,000 |

| Final Settlement Total | $90,000 |

| New Money Secured by Attorney | $60,000 |

| Attorney Fee (33% of New Money) | -$19,800 |

| Case Expenses (Moisture expert, filing fees) | -$3,500 |

| Total Net Recovery for Homeowner | $66,700 |

Scenario B: The Gross Settlement Model

| Item Description | Amount |

|---|---|

| Final Settlement Total | $90,000 |

| Attorney Fee (33% of Entire Gross Amount) | -$29,700 |

| Case Expenses (Moisture expert, filing fees) | -$3,500 |

| Total Net Recovery for Homeowner | $56,800 |

As you can see, the New Money model puts nearly $10,000 more into your repair budget because the attorney is not taking a cut of the money the insurer already agreed to pay. Presenting the math this way helps clarify what an insurance lawyer actually does during a claim to justify their fee.

Hidden Clauses: Minimum Fees and Mid-Case Termination

Even with a standard percentage agreement, there are two specific scenarios you need to understand before you sign a retainer.

The first is the minimum fee clause. Sometimes, an insurance company will realize you are serious and immediately pay the claim just days after your attorney sends a letter of representation. To protect themselves from doing the initial case setup work for a tiny percentage of a fast settlement, some attorneys include a minimum fee clause. This ensures they receive a set dollar amount or a specific minimum percentage even if the case resolves almost instantly.

The second scenario is mid-case termination. What happens if you decide to fire your attorney before the claim is settled? You cannot simply fire a lawyer right before the final check arrives to avoid paying their fee. If you terminate the contract early, the attorney will typically place a lien on your future settlement. They will bill you for the hourly value of the work they already performed. You must be prepared to see the process through once you hire representation.

Questions to Ask Before Signing a Retainer

Before you formally hire an attorney to handle your property damage dispute, you need to conduct an interview. Do not let the stress of the situation push you into signing a contract you do not fully understand. Use this checklist during your initial consultation:

- ⚖️ Is your fee based on the total settlement amount or only the new money you recover above my current offer?

- ⚖️ Does your percentage increase if we have to file a lawsuit or go to trial?

- ⚖️ Will I be billed for case expenses out of pocket as the case progresses, or will they be deducted from the final settlement?

- ⚖️ Are case expenses deducted before or after you calculate your percentage fee?

- ⚖️ Is there a minimum fee clause if the insurance company decides to pay the claim immediately after you send a letter of representation?

An attorney who routinely handles property insurance claims will be able to answer these questions immediately and clearly. If they are evasive about their billing structure, treat that as a red flag when finding the right property damage attorney for your case.

When the Math Works For You (and When It Doesn’t)

The contingency fee model is a powerful tool, but it is not the right fit for every single claim. There are situations where the math simply will not work in your favor.

If you have a very small claim value relative to its complexity, giving up a percentage of the settlement might leave you without enough funds to actually complete the repairs. Similarly, if your dispute is purely about the price of materials and can be resolved through your policy’s standard appraisal clause, bringing in heavy legal artillery might incur unnecessary fees. The appraisal process is an alternative dispute resolution mechanism built into most policies. It involves hiring an independent appraiser to negotiate the cost of repairs directly with the insurance company’s appraiser. This route is typically much faster and less expensive than litigation if coverage is already approved and the only disagreement is the dollar amount.

💡 Pro Tip: Always secure written estimates from your own independent contractors first. You need to know the true cost of your repairs to calculate whether your net settlement after attorney fees will actually cover your reconstruction.

On the other hand, the contingency math clearly works in your favor when you are dealing with a large-scale claim where the gap between the insurer’s offer and your actual damage is massive. Total losses, severe structural fires, and cases where the insurer has acted unreasonably or in bad faith are prime scenarios. In certain bad faith situations, the financial recovery may go beyond the original claim amount. Your attorney can assess whether your case has that potential.

Moving Forward with Confidence

Treating a legal consultation as a business decision removes the fear from the claims process. You are not blindly handing over a blank check. By understanding the difference between new money and gross settlement percentages, and by clarifying how expenses are handled, you can project exactly what a successful legal intervention will mean for your repair budget.

The insurance company relies on homeowners assuming that lawyers are too expensive. Knowing how the math actually works takes that leverage away and allows you to evaluate your options clearly.

Final Steps

If your claim has hit a wall and the financial gap is significant, the most practical next step is to use the free consultation that most contingency attorneys offer. You can get a professional assessment of your case without spending a dime. To find out if legal intervention aligns with your financial best interests, you can request a free claim review from an insurance attorney network.

❓ FAQ

💰 Do insurance attorneys charge upfront?

In most property damage cases, no. They operate on a contingency fee basis, meaning they do not charge an upfront retainer and only collect a fee if they successfully recover money for you.

📉 What percentage does a property damage lawyer take?

The percentage typically ranges based on the complexity of the case and the stage at which it resolves. It is common to see tiered structures that increase if a formal lawsuit is filed or if the case goes to trial.

📝 How does an insurance claim lawyer get paid if we lose?

Under a standard contingency agreement, if the attorney fails to secure a settlement or court award, they do not collect an attorney fee for the hours they worked. You may still be responsible for hard case expenses, depending on your contract.

🧾 Are case expenses the same as attorney fees?

No. Attorney fees pay for the lawyer’s time and legal work. Case expenses are separate hard costs, such as hiring independent engineers, court filing fees, and paying for deposition transcripts.

⚖️ Can I negotiate the contingency fee percentage?

Yes, contingency fees are generally negotiable. Depending on the size of your claim and how straightforward the evidence is, an attorney may be willing to adjust their percentage or adopt a “new money” structure.

🛑 What is a minimum fee clause in an attorney contract?

It is a specific contract term designed to protect the attorney’s time. It ensures they receive a set dollar amount or a base percentage even if the insurance company decides to settle the claim immediately after the attorney is hired.

🔄 What happens if the insurer pays my claim right after I hire a lawyer?

If you have already signed the contingency agreement, the attorney is generally entitled to their fee for triggering the settlement. Depending on your contract, this will either be their standard percentage or a specific amount dictated by their minimum fee clause.

💸 Does my insurance company have to pay my attorney fees?

Usually, no. However, in certain bad faith situations, courts have ordered insurers to cover attorney fees. Ask your attorney whether your situation may qualify.

🤝 Can I hire an attorney just to review my policy for a flat fee?

Yes, some attorneys offer limited-scope representation for a flat hourly rate or fixed fee if you only need them to interpret a specific policy exclusion or draft a formal demand letter.

📊 How much does a home insurance attorney cost on average?

Because they work on contingency, the “cost” is directly tied to the outcome. You do not face an hourly bill, but rather a reduction in your final settlement check based on the agreed-upon percentage.

Most disputes start with a payout disagreement. These cover the earlier stages.

- The claim lifecycle a PA or attorney works inside

- The policy language that determines what professional help can recover

- How damage classification affects what an expert can negotiate

- Whether the situation you have justifies bringing in outside help

- When a denial is the outcome a PA could have prevented

- What a public adjuster actually does inside a claim

- When the dispute has moved past what a PA can handle

Two paths, two different situations. These clarify which one fits yours.

- How to tell if your situation actually warrants hiring one

- The difference between the adjuster you hired and the one who showed up

- When water damage scope gaps make independent review necessary

- When fire damage complexity makes independent representation worth it

- When the gap between estimates is large enough to bring in a PA

- When bad faith makes legal action the only path that works

- PA, attorney, or appraisal clause: which path fits your denial

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.