- Finding the right attorney is not about picking the biggest billboard; it is about finding a specialist who exclusively represents policyholders, not insurance companies.

- A successful vetting process requires looking at trial experience and the percentage of the firm’s practice dedicated specifically to property damage disputes.

- The initial consultation is as much for you to interview them as it is for them to evaluate your claim: prepare with specific questions about fee structures and past results.

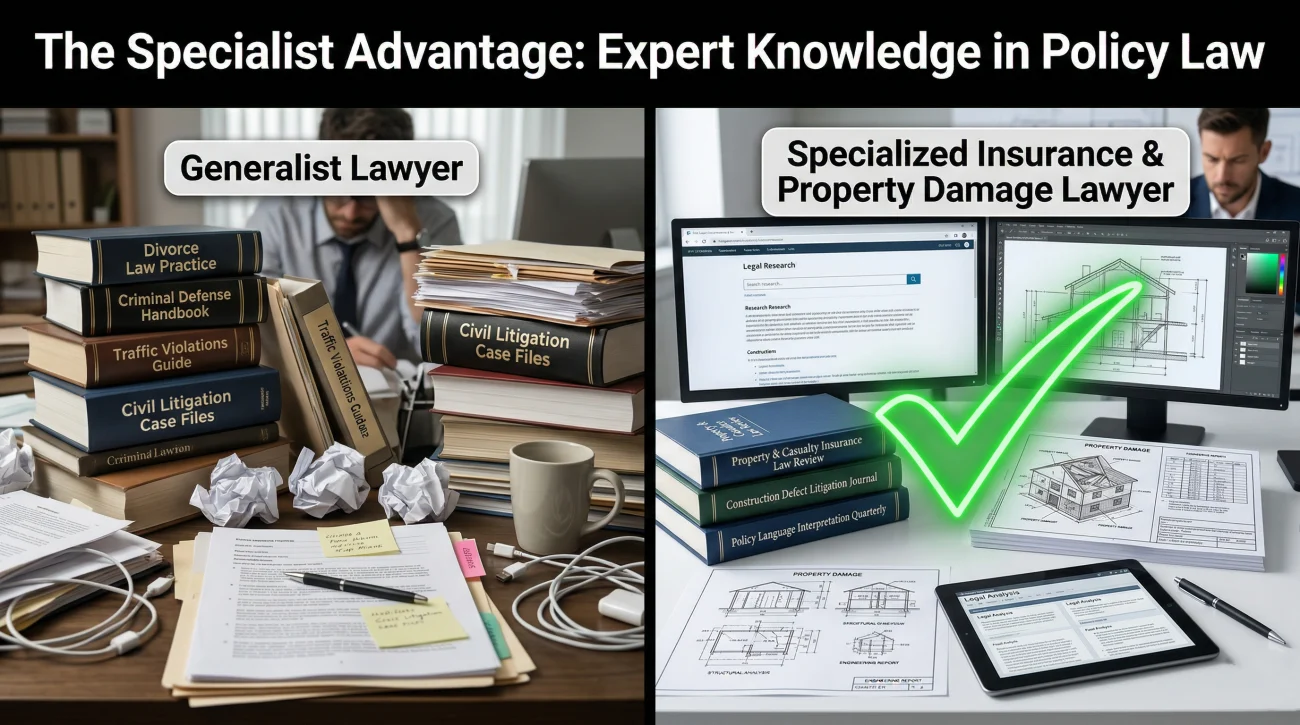

- Avoid “general practice” lawyers who handle everything from car accidents to divorces; insurance claim litigation requires deep knowledge of policy language and bad faith standards.

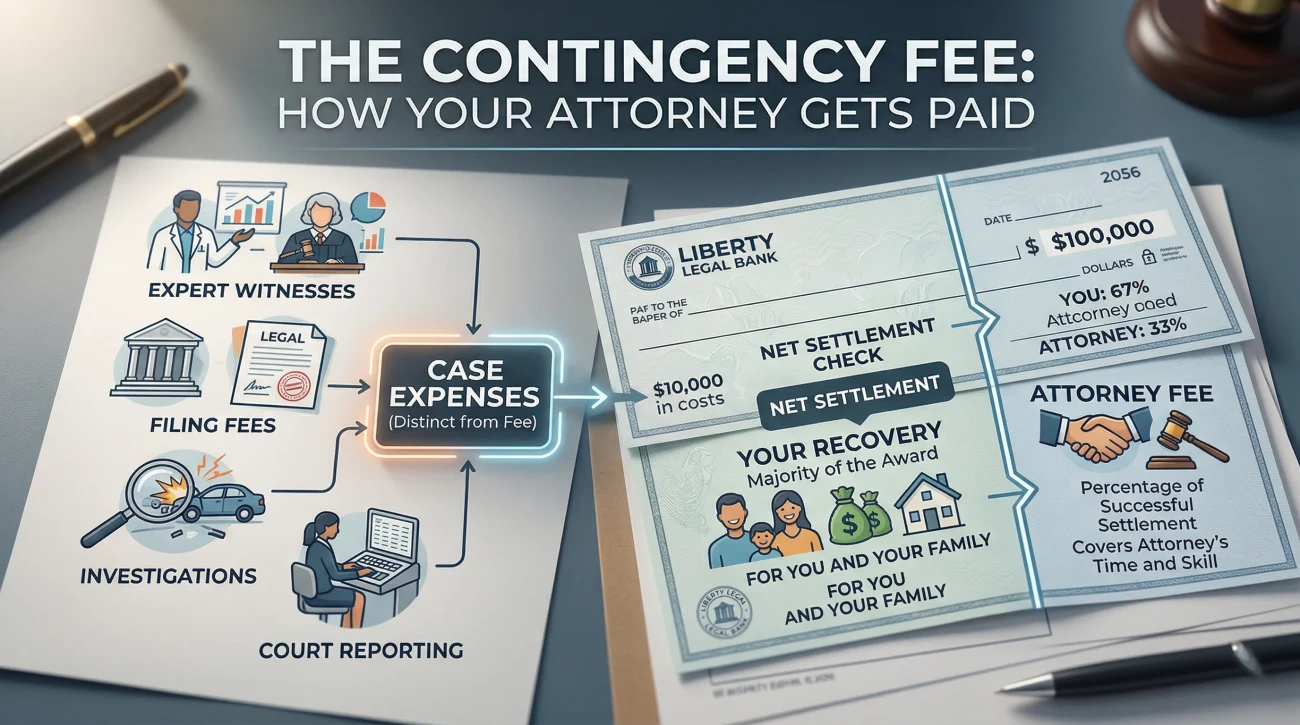

- Most reputable home insurance attorneys work on a contingency fee basis, meaning there is no upfront cost to get a professional assessment of your legal options.

Beyond the Billboards: How to Evaluate a Property Damage Attorney

When an insurance claim hits a wall, the stress can lead to hasty decisions. I have seen many homeowners reach for the first phone number they see on a highway billboard or the top sponsored result on a search engine. While those firms might have massive marketing budgets, they often operate on high-volume models where a complex property dispute can get lost in a sea of simple personal injury cases. Finding the right home insurance claim attorney is a strategic process that requires looking past the glossy ads and into the actual courtroom leverage of the firm.

In my years reviewing claim files, I have learned that the dynamic of a claim shifts the moment a qualified lawyer is involved. The insurer knows that the negotiation has moved from polite requests to legal accountability. However, this accountability only carries weight if there is a credible threat of litigation. If the insurer knows your attorney has a reputation for taking cases all the way to a verdict, their incentive to offer a fair settlement increases significantly. Without that specific leverage, you are simply trading one person who negotiates for another, which rarely moves the needle on a stubborn denial.

p>I once reviewed a claim where a homeowner hired a general litigator for a complex fire dispute. The attorney missed the specific suit limitations deadline in the policy because they were relying on the general state statute of limitations. That one mistake ended the claim permanently. This is why specialized experience is not just a preference; it is a necessity.

The Specialist vs. the Generalist: Why It Matters

Most people have a family lawyer or a friend who handles real estate and estate planning. While these professionals are valuable in their own right, an insurance claim is a highly technical contract dispute. I often compare it to high-end engineering: you would not ask a residential architect to design a bridge. You need a specialist who understands the complex framework and the specific, often restrictive language of a homeowners insurance policy.

A specialist attorney knows how to read the fine print of an HO-3 policy. They understand the difference between a proximate cause and a concurrent cause. More importantly, they understand the standard of care that an insurance company owes to its insured. If you are wondering when do you need a lawyer for an insurance claim, the answer usually involves a level of complexity where a generalist simply cannot match the insurer’s specialized defense team.

The Policyholder-Side Advantage

When you are looking for candidates, I always recommend finding a firm that is 100% dedicated to representing the insured (the policyholder). Many firms play both sides, representing carriers on some cases and homeowners on others. While they might argue this gives them insight, it often creates a mindset that is too sympathetic to the insurer’s internal processes. Policyholder-only firms are generally more aggressive because they have no interest in maintaining relationships with the insurance industry’s defense network.

💡 Pro Tip: To verify if a firm is truly policyholder-only, check their website for a “Defense” or “Insurance Representation” practice area. You can also search the firm’s name in your local court records: if you see them listed as the attorney for an insurance company in other lawsuits, they are playing both sides.

Key Experience Markers to Look For

Not all experience is equal. An attorney might have been practicing for thirty years, but if they have only handled five property damage claims in that time, they are not the right fit. When I vet attorneys for my own research, I look for three specific markers of expertise that indicate they can actually move a claim forward through active verification.

| Marker | What It Tells You | Vetting Action |

|---|---|---|

| Trial Experience | The actual ability to take a case to a jury. | Ask for a list of recent jury verdicts in property damage cases. |

| Practice Percentage | The level of daily focus on property law. | Ask what portion of their active files are homeowners claims. |

| Specific Damage Type | Technical knowledge of your specific loss. | Confirm they have litigated the same cause of loss (e.g., Fire, Mold). |

I also suggest looking for attorneys who are active in professional organizations like the American Association for Justice (AAJ). These lawyers are usually at the forefront of changing case law and know which new court rulings might benefit your specific situation before the insurer even acknowledges them.

Where to Start Your Search

The best attorneys rarely need to spend millions on TV commercials; their reputations usually precede them in the industry. If you are starting from scratch, I recommend using a tiered approach. However, I have found that traditional search methods often require an extra layer of skepticism.

- 🔎 State Bar Referral Services: Every state bar has a list of licensed attorneys categorized by specialty. Look for Insurance Law or Property Damage specifically.

- 🔎 Peer Ratings (Super Lawyers / Martindale-Hubbell): These sites allow other lawyers to rate their peers. While helpful, remember that high ratings in general litigation do not always translate to insurance expertise.

- 🔎 Public Adjuster Recommendations: In my experience, this is often the most reliable source. Public adjusters (PAs) deal with insurance attorneys every day. They have seen the attorney’s actual work product firsthand, not just their marketing. If a PA recommends a lawyer, it is usually because that lawyer has consistently recovered more money for their clients during the negotiation phase.

In many cases, the most efficient path is to use a vetted network that specializes in connecting homeowners with qualified legal counsel. This removes the guesswork of cold-calling random firms. If your claim has reached a point where negotiation is no longer working, connecting with an insurance claim attorney for a free review is often the fastest way to verify if your case has legal merit.

Red Flags to Watch For During the Search

Not all legal representation is beneficial. I have seen homeowners hire attorneys who actually made their situation worse by over-promising or under-delivering. Vetting is about more than just looking for wins: it is about looking for integrity and clear communication. If you feel like a number during the initial intake, that feeling will only intensify once the litigation begins.

Watch for these red flags during your search and initial calls:

- The Outcome Guarantee: No ethical attorney can guarantee a specific settlement amount. If they promise you a specific check figure on the first call, they are likely just trying to get you to sign a retainer.

- Unclear Fee Structure: If they cannot or will not explain exactly how they get paid and what costs you might be responsible for, it is a sign of poor transparency.

- The Settlement Mill Pattern: If a firm has hundreds of attorneys but rarely takes a case to a jury, the insurer knows they will eventually settle for whatever is on the table. A lack of trial history is a warning signal that the insurer will use to keep their offers low.

- Communication Gaps: If you cannot get past an intake specialist to speak with the actual attorney who will handle your case, you are likely just a file number to them.

- Defense-Heavy Past: A lawyer whose firm still represents insurance companies on other cases has a permanent conflict of interest that may affect their negotiation intensity.

Key Point: A good attorney should be a reality check, not a cheerleader. You want someone who tells you the risks of your case, not just the potential rewards.

The Free Consultation: How to Prepare

Once you have filtered out the red flags, the consultation is where the real evaluation happens. Most reputable insurance attorneys offer a free initial consultation. It is a common mistake to view this as just the lawyer deciding if they want you. In reality, this is your interview of them. I tell homeowners to treat this like a business meeting where you are hiring a professional to manage a major financial asset: your claim.

To get the most value out of the consultation, you should have your documents organized. The attorney will want to see your policy declarations page, the insurer’s denial or settlement letter, and your own documentation of the damage. They are looking for the legal hook: the specific point where the insurer failed to meet their contractual obligations.

Understand that what a home insurance attorney does during this initial review is evaluate the risk. They are calculating the likelihood of a recovery that justifies the time they will invest. If they turn down your case, it doesn’t always mean your claim is invalid; it might just mean the dollar amount is too small for a contingency-fee model to work. I always suggest asking for a brief explanation if they decline the case so you can adjust your next steps.

Questions You Must Ask Every Candidate

Do not be afraid to ask tough questions. You are the client. I have found that the best attorneys appreciate a client who is informed and engaged. Use this list as a guide for your first conversation.

1. “What percentage of your practice is dedicated exclusively to property damage claims?”

2. “Have you handled a claim specifically involving [Your Damage Type] before?”

3. “When was the last time you took an insurance claim case all the way to a jury trial?”

4. “Who will be my primary point of contact? Will I be working with you or an associate?”

5. “How do you handle case expenses like expert witnesses or court filing fees?”

6. “Based on the denial letter I’ve provided, what is your initial assessment of the insurer’s position?”

The answer to the first question should be at least 50% or more. If they say they do a little bit of everything, they might not have the depth required for a complex dispute. Pay close attention to how they answer question six: a good attorney will be cautious and point out where they need more information before giving a definitive opinion.

Understanding the Fee Structure

Cost is the primary reason homeowners hesitate to hire an attorney. In most property damage cases, attorneys work on a contingency fee. This means they take a percentage of the final settlement or court award. If they do not recover money for you, you do not owe them an attorney fee. I find this model is the great equalizer: it allows a homeowner with no savings to fight a multi-billion dollar corporation.

However, you must distinguish between attorney fees and case expenses. Case expenses include things like hiring a structural engineer or paying for a court reporter during a deposition. They also include court filing fees and costs for expert testimony. Some firms advance these costs and deduct them from the final settlement, while others might ask you to pay them as they arise. You must clarify this before signing the retainer.

If you want a deeper look at the math, reviewing the home insurance attorney contingency fee mechanics will help you understand how much of the settlement will actually end up in your pocket.

Signing a retainer agreement without reading the expenses section, only to find out later you are responsible for thousands in expert fees regardless of the outcome.

Explicitly asking, “If we lose this case, do I owe anything for the expenses you’ve advanced?” and getting the answer in writing.

The Final Decision: Trust Your Documentation and the Data

At the end of the day, hiring an attorney is a partnership. You are trusting this person to represent your interests in a high-stakes environment. While credentials and trial history are the foundation, your feeling about their communication style matters too. Litigation can take twelve to twenty-four months: you need to be able to work with this person for the long haul.

Once you have vetted two or three candidates, the choice often becomes clear. The attorney who was the most transparent about the risks, the clearest about their fees, and the most knowledgeable about your specific damage type is usually the one who will fight the hardest. Do not feel pressured to sign anything on the spot. A reputable lawyer will give you the time to review the retainer and make an informed decision.

If you have already received a lowball offer or a denial, the clock is ticking on your policy’s suit limitations clause. Vetting an attorney now, even if you are not ready to file a lawsuit today, protects your rights for the future. Take the first step by organizing your claim file and scheduling that first conversation: it is the only way to move from being a victim of the process to a participant in the solution.

❓ FAQ

🏠 How much does it cost to consult with a home insurance attorney?

In almost all cases, the initial consultation is free. You should never have to pay an upfront “consultation fee” for a property damage claim review.

📞 Can I hire a lawyer if I’ve already accepted a partial payment?

Yes. Accepting an undisputed payment for part of your claim does not waive your right to sue for the remainder, provided you did not sign a full release of claims or a waiver. An attorney can review the documents you’ve already signed to confirm your rights are still intact.

🔎 Where can I find reviews for property damage lawyers?

You can check Martindale-Hubbell, Super Lawyers, and Avvo for peer ratings. Additionally, your state’s bar association website will list any disciplinary history. Always look for reviews specifically related to insurance claims.

⚖️ What is the difference between a public adjuster and an attorney?

A public adjuster handles damage estimation and negotiation. An attorney is a licensed legal professional who can file lawsuits and argue cases in court. PAs are for negotiation; attorneys are for legal leverage and litigation.

⏳ How long does it take an attorney to resolve a claim?

There is no universal timeline. Some claims settle within months, while others that go to full litigation can take 12 to 24 months. The complexity of the damage and the insurer’s willingness to negotiate drive the timeline.

💼 Do I need a lawyer near me, or can I hire a firm from another city?

As long as the attorney is licensed in the state where the property is located, they can represent you. It is far more important to have a high-quality insurance specialist than a nearby generalist.

📜 What documents should I bring to an attorney consultation?

Bring your full insurance policy, any correspondence from the insurer (denial letters, estimates), photos of the damage, and any contractor estimates you have received. The more info they have, the more accurate their assessment will be.

🚫 Can my insurance company drop me if I hire a lawyer?

Insurers generally cannot cancel your policy specifically because you hired an attorney. However, they can choose not to renew your policy at the end of the term for other reasons, such as your claim history.

👨⚖️ Will my case actually go to court?

The vast majority of insurance lawsuits settle before ever reaching a trial. Hiring a lawyer with a strong trial reputation actually makes a settlement more likely because the insurer wants to avoid the risk of a jury verdict.

💰 Is it worth hiring a lawyer for a small claim?

It depends on the “gap.” For a full breakdown of when the math makes sense, see our section on attorney contingency fees. Most attorneys will tell you honestly if your claim is too small for their services.

Most disputes start with a payout disagreement. These cover the earlier stages.

- The claim lifecycle a PA or attorney works inside

- The policy language that determines what professional help can recover

- How damage classification affects what an expert can negotiate

- Whether the situation you have justifies bringing in outside help

- When a denial is the outcome a PA could have prevented

- What a public adjuster actually does inside a claim

- When the dispute has moved past what a PA can handle

Two paths, two different situations. These clarify which one fits yours.

- How to tell if your situation actually warrants hiring one

- The difference between the adjuster you hired and the one who showed up

- When water damage scope gaps make independent review necessary

- When fire damage complexity makes independent representation worth it

- When the gap between estimates is large enough to bring in a PA

- When bad faith makes legal action the only path that works

- PA, attorney, or appraisal clause: which path fits your denial

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.