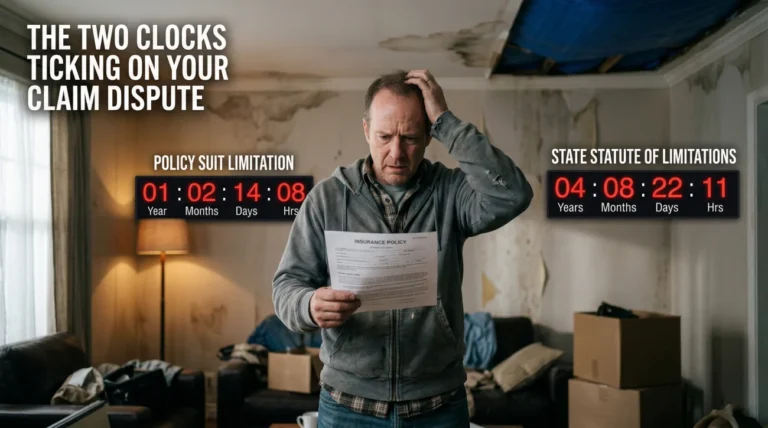

- You have the legal right to sue your homeowners insurance company without an attorney, either in small claims court or in civil court as a pro se litigant.

- Small claims court is viable for minor, straightforward underpayments, but severe policy disputes and bad faith claims do not belong there.

- In standard civil court, unrepresented homeowners face a massive structural disadvantage against experienced corporate defense teams.

- Procedural errors, the inability to afford independent expert witnesses, and lack of negotiation leverage are the primary reasons DIY lawsuits fail.

- Because most property claim attorneys work on contingency, upfront cost should not be the deciding factor when choosing to represent yourself.

The Reality of Taking on Your Insurer Alone

When a legitimate property damage claim is denied or severely underpaid, the frustration is overwhelming. I have sat across the table from countless homeowners who have reached their breaking point after months of ignored emails and confusing adjuster reports. Eventually, almost everyone asks the exact same question: Can I just take my insurance company to court myself?

The technical answer is yes. You have the absolute right to file a lawsuit without legal representation. However, the practical answer requires a much deeper look into what you are actually stepping into. In my time working through complex property claims, I have seen the operational realities of how insurers handle unrepresented policyholders. The idea of standing in front of a judge to simply tell your side of the story is a common misconception. Litigation is a rigid, rule-bound arena.

This guide is not meant to discourage you from exercising your legal rights. Instead, it is designed to give you an honest, practical look at the mechanics of a DIY lawsuit against a major insurance carrier. By understanding the structural imbalances, the procedural hurdles, and the tactics defense attorneys use, you can make a fully informed decision about whether proceeding alone is the smartest path for your specific financial recovery.

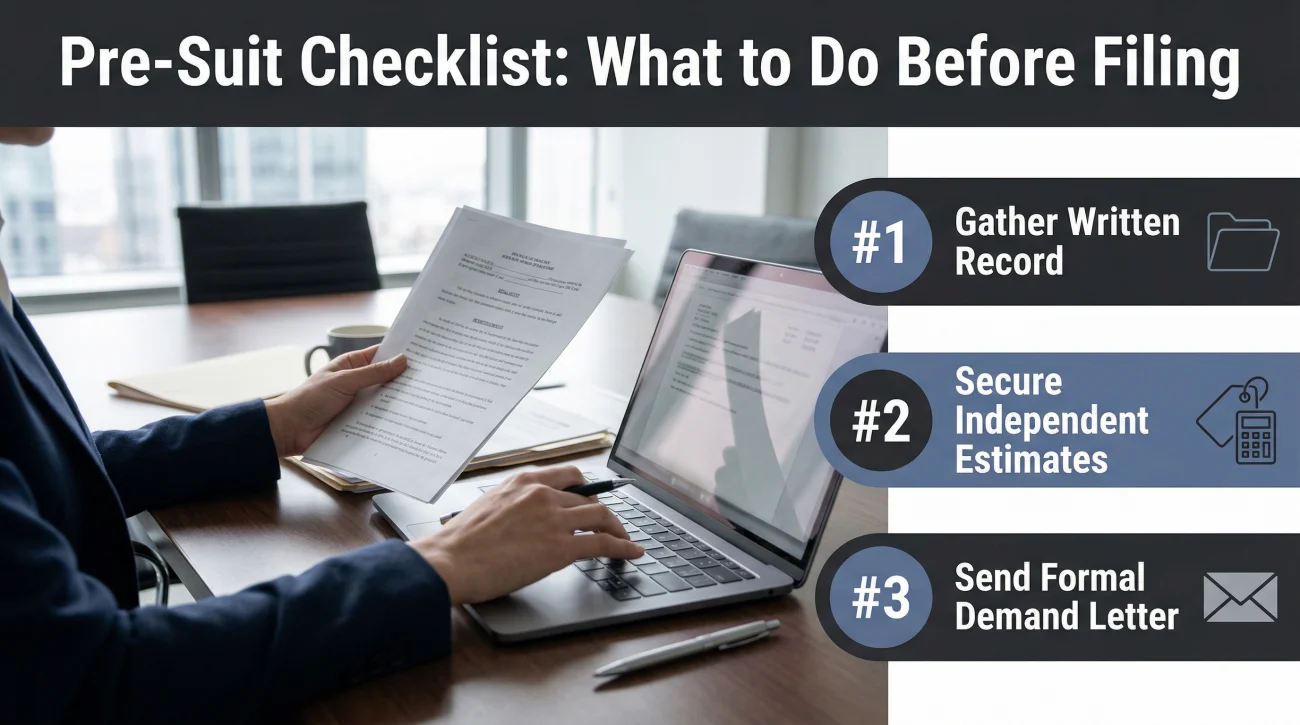

Pre-Suit Checklist: What to Do Before Filing Anything

Before you even research court filing fees, you must ensure you have exhausted the negotiation phase. A lawsuit should never be your first escalation step. Taking a few foundational steps can often force a resolution without requiring courtroom intervention.

- 📍 Gather the written record: Courts rely on paper trails. Ensure every phone call with your adjuster is backed up by an email summary confirming what was discussed.

- 📍 Secure independent estimates: You cannot sue simply because you feel the offer is low. You need a detailed, line-by-line estimate from an independent contractor to prove the financial gap.

- 📍 Send a formal demand letter: This is a factual, unemotional letter sent to the insurer stating the exact dollar amount owed, attaching your independent proof, and providing a strict deadline to pay before legal action is taken.

If the demand letter produces no result, the next decision point is choosing the right legal venue.

Filing a Complaint vs. Filing a Lawsuit

Before looking at the court system, we need to clear up a very common point of confusion. Many homeowners use the terms “filing a complaint” and “filing a lawsuit” interchangeably. In the insurance world, these are two entirely different actions.

If you want to escalate a dispute without going to court, your first option is submitting a regulatory grievance. You can explore how to file a formal complaint with your state insurance department to force the insurer to formally answer for their actions. This is a free administrative process. The state regulator acts as a mediator of sorts, though they cannot force the insurer to pay a disputed factual claim.

A lawsuit is a formal legal action filed in the judicial system. It requires paying filing fees, adhering to strict rules of civil procedure, and eventually proving your case before a judge or jury. If the regulatory route has failed and you are determined to litigate, you generally have two paths: small claims court or standard civil court.

Small Claims Court: The Most Common DIY Path

For homeowners who want to represent themselves, small claims court is usually the most accessible venue. It is designed specifically for everyday people to resolve disputes without needing a law degree. The filing fees are low, the rules of evidence are relaxed, and the process moves relatively quickly.

However, small claims courts cap the amount you can sue for, and in many states, that ceiling is low enough to exclude most serious property damage disputes. Small claims court is generally strictly for simple breach of contract disputes. It is not the place to argue complex legal theories like bad faith or deceptive practices.

I frequently see homeowners assume that small claims court will be an informal conversation between them and their claims adjuster. It never is. The insurer will not send your adjuster. They will send a licensed, experienced corporate attorney whose sole job is to protect the company’s bottom line. You must be prepared to argue against legal counsel, even in a small claims setting.

Civil Court and Pro Se Representation

If your loss exceeds those strict financial caps, small claims court is no longer an option. You must file in standard civil court. When your disputed amount forces you into this venue, proceeding without an attorney is known as “pro se” representation. This is where the difficulty level multiplies exponentially.

When you file a pro se lawsuit, the judge expects you to know and follow the exact same rules of civil procedure that licensed attorneys follow. There is no leniency for being a homeowner who does not know the law. I have watched unrepresented policyholders get their cases dismissed completely, not because their damage was fake, but because they missed a civil filing deadline by one day or failed to format a complaint according to local court rules.

To understand exactly what this timeline entails, you should familiarize yourself with the step by step process of filing a lawsuit against your insurer. It is heavily front-loaded with paperwork and procedural maneuvering.

What You Are Up Against: The Insurer’s Arsenal

To evaluate whether you can win without a lawyer, you must objectively look at what the other side brings to the table. Insurance companies handle litigation every single day. It is built into their business model. When you file a lawsuit, you trigger a massive, well-funded defense mechanism.

Experienced Defense Counsel

The insurer will assign the case to either their in-house litigation department or an external defense firm specializing in insurance law. These attorneys know every procedural loophole, every precedent, and every tactic to exhaust an unrepresented plaintiff. They will routinely file motions to dismiss your case based on technicalities before you ever get a chance to present your evidence.

Beyond their legal personnel, the insurer also holds all the documentary cards.

The Claim File Advantage

The insurer owns the complete history of your claim. They have the internal adjuster notes, the recorded statements, the metadata from their estimating software, and the exact policy language. Unless you know exactly how to legally compel them to hand over these documents during the discovery phase, you will be fighting blind.

Even if you overcome the procedural hurdles and obtain the claim file, you still have to prove your physical case.

The Expert Witness Roster

This is arguably the biggest hurdle. In property damage litigation, you cannot just tell the judge that wind damaged your roof. You must prove it using causation experts. The insurer has a deep roster of credentialed specialists on retainer: structural engineers to assess load failures, industrial hygienists to prove hidden mold contamination, and forensic meteorologists to pinpoint exact wind speeds during a specific storm window. If their engineer testifies that your damage is from long-term wear and tear, and you do not have your own credentialed expert to counter that testimony, the court will almost always side with the insurer’s expert.

Where Unrepresented Homeowners Typically Lose Ground

When pro se lawsuits fail, it is rarely because the homeowner was lying about their damage. It is almost always because the homeowner was outmaneuvered structurally. Here are the specific areas where unrepresented policyholders lose their cases.

| Litigation Phase | What The Homeowner Typically Does | How The Insurer Capitalizes On It |

|---|---|---|

| Pleadings | Drafts an emotional narrative about how unfair the adjuster was. | Files a motion to dismiss because the complaint failed to cite specific breach of contract elements. |

| Discovery | Fails to send formal legal requests for the insurer’s internal guidelines and unedited adjuster logs. | Withholds crucial internal documents because the homeowner did not formally request them according to civil rules. |

| Depositions | Answers questions casually, not realizing it is a formal, sworn legal proceeding. Volunteers too much irrelevant information about property maintenance history. | Treats seemingly polite conversation as sworn testimony. Uses the transcript to lock the homeowner into statements that inadvertently validate a wear and tear exclusion, effectively destroying the case before trial. |

| Negotiation | Demands the full policy limit without legal leverage or expert backing. | Refuses to settle, knowing the homeowner does not know how to successfully navigate a jury trial. |

When Self-Representation Actually Makes Sense

Despite the overwhelming challenges, there are specific, narrow scenarios where pursuing a claim without a lawyer is realistic. You should only consider self-representation if your situation meets very strict criteria.

First, the financial gap must be small enough to fit comfortably within your state’s small claims court limits. Second, the dispute must be factual and simple, not based on complex policy interpretations. For example, if your policy clearly covers a specific structural repair, you have the completed contractor invoice, and the insurer simply refuses to release the final depreciation check due to administrative delays, a small claims filing is a highly effective tool to force their hand.

Even in this specific scenario, sending a formal demand letter before filing your case is a mandatory first step that should never be skipped.

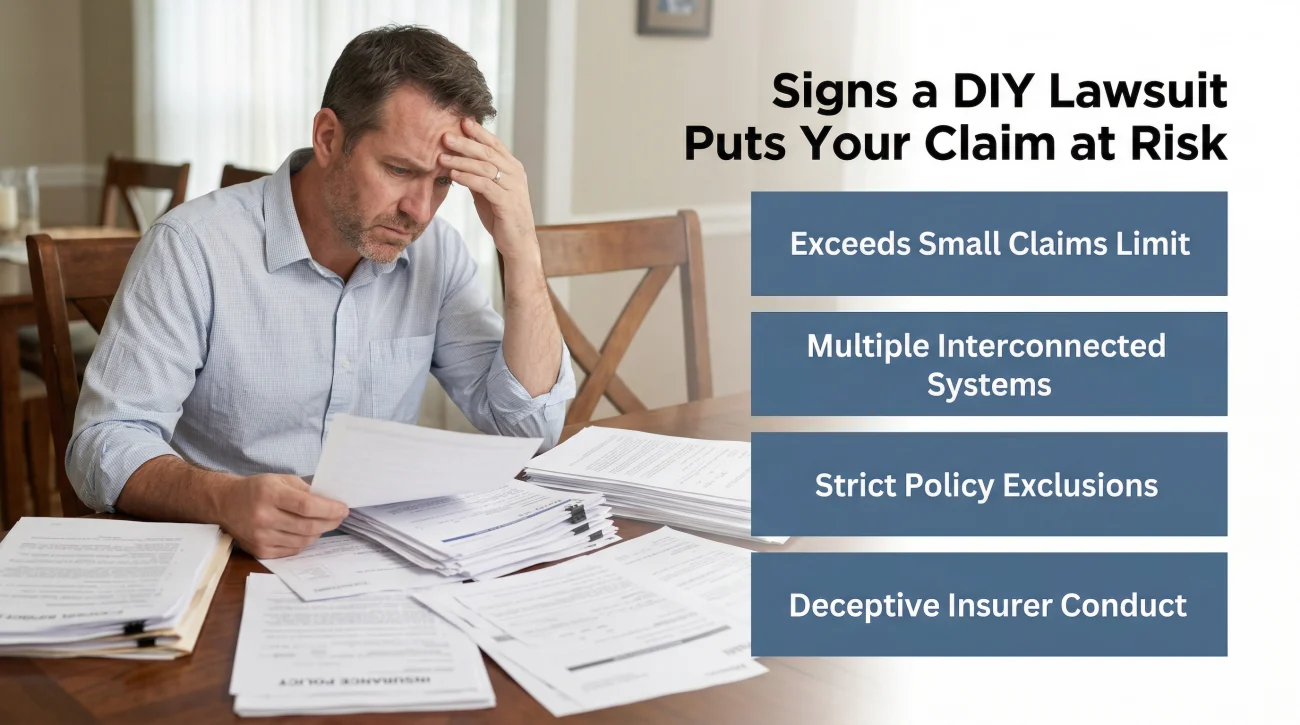

Signs a DIY Lawsuit Will Put Your Claim at Risk

If you are trying to decide whether to push forward alone, you must evaluate the complexity of your loss. Proceeding pro se is highly dangerous if any of the following warning signs apply to your situation.

- 📍 The financial gap between your repair estimate and the insurer’s offer exceeds your state’s small claims court limit.

- 📍 Your claim involves multiple interconnected systems, such as structural fire damage combined with widespread HVAC smoke contamination.

- 📍 The insurer is asserting a specific policy exclusion, such as long-term wear and tear or earth movement, which requires expert testimony to defeat.

- 📍 You have clear evidence that the insurer intentionally altered documents, lied about policy limits, or engaged in other deceptive conduct.

- 📍 You are dealing with a total loss scenario where the valuation of your entire property and land is being contested.

If these patterns match your experience, the insurer is already treating your file as a high-risk legal liability. Attempting to navigate these specific complexities alone simply gives the insurer’s defense team the structural advantage they need to deny your recovery.

The Danger of Hiring an Attorney Mid-Case

Some homeowners attempt to start the pro se process with the intention of hiring a lawyer only if things get too complicated. This is almost always a costly mistake. If you make critical procedural errors, botch the discovery phase, or provide damaging sworn testimony during a deposition, many attorneys will refuse to take over your case later. The structural damage to your lawsuit often cannot be undone once it is entered into the court record.

The Contingency Fee Alternative

Many homeowners assume that pursuing litigation means paying hundreds of dollars an hour out of pocket. This is a fundamental misunderstanding of how property damage litigation actually works.

You do not need a massive legal fund to hire an attorney for an insurance dispute. The vast majority of attorneys who represent policyholders work on a contingency fee basis. This means they do not charge you any upfront retainer fees. Instead, they take a percentage of the final settlement or court award they recover for you. If they fail to recover any additional funds, you typically owe them nothing for their time.

Because the upfront cost is removed, financial constraints should never force you into representing yourself in a complex case. You can learn exactly how attorney contingency fees work in property claims to understand the math behind these agreements.

Making Your Final Decision

After reviewing the procedural hurdles and the sheer resources the insurer brings to the table, the decision to litigate alone comes down to risk. The insurance company relies on unrepresented homeowners making critical mistakes during the discovery phase or failing to secure the right expert witnesses. Before you file a complaint in civil court, you must be honest with yourself about whether you have the time, energy, and legal comprehension to fight a corporate defense team.

If your claim is complex, the smartest action you can take is understanding when a home insurance claim attorney is truly necessary. Taking the time for a free professional evaluation costs you nothing and provides immediate clarity on whether you have a viable legal case.

If you are ready to explore your options without financial risk, the most practical next step is getting a free case review from a property claim attorney to see if your situation warrants legal representation.

❓ FAQ

⚖️ Can I take my insurance company to small claims court?

Yes, as long as the disputed amount falls under your state’s small claims limit. In many states, that limit is lower than most homeowners expect, which is why serious property damage disputes rarely qualify. It is a viable option for simple, straightforward underpayments.

🧑⚖️ Do I need a lawyer to sue my homeowners insurance?

No, the law allows you to represent yourself pro se. However, due to the complexity of insurance law and the tactics used by corporate defense teams, doing so in standard civil court is highly risky.

💸 How much does it cost to sue an insurance company yourself?

Your direct costs include court filing fees, process server fees, and potentially thousands of dollars if you need to hire independent experts like engineers or hygienists to testify on your behalf.

📄 What happens if I make a mistake in my lawsuit paperwork?

The judge holds pro se litigants to the same standards as licensed attorneys. A procedural mistake or failing to respond to a discovery request correctly can result in your case being permanently dismissed.

🏢 Will the insurance company send a lawyer to small claims court?

Yes. Even in small claims court, insurance companies almost always send their own corporate defense counsel or local retained attorneys to argue against your claim.

🚫 Can I claim bad faith in small claims court?

Generally, no. Bad faith claims involve complex legal standards and requests for additional damages that fall outside the jurisdiction of a standard small claims court.

⏱️ How long does a DIY lawsuit against an insurance company take?

A small claims case can be resolved in a few months. A pro se lawsuit in standard civil court can easily drag on for years due to procedural motions, discovery delays, and crowded court dockets.

🏛️ Does filing a complaint with the state help avoid a lawsuit?

It can. A formal complaint forces the insurer’s regulatory compliance team to review the file. If they discover an obvious administrative error, they may resolve the claim without the need for litigation.

🔄 Can I hire a lawyer later if I start the lawsuit myself?

You can, but many attorneys will refuse to take over a pro se case if you have already made critical procedural errors, missed deadlines, or botched the discovery phase.

📉 Do I have to pay the insurance company’s legal fees if I lose?

Depending on your state’s laws and how the judge rules, if the court determines your DIY lawsuit was frivolous or without legal merit, you could be ordered to pay the insurer’s legal costs.

Most disputes start with a payout disagreement. These cover the earlier stages.

- The claim lifecycle a PA or attorney works inside

- The policy language that determines what professional help can recover

- How damage classification affects what an expert can negotiate

- Whether the situation you have justifies bringing in outside help

- When a denial is the outcome a PA could have prevented

- What a public adjuster actually does inside a claim

- When the dispute has moved past what a PA can handle

Two paths, two different situations. These clarify which one fits yours.

- How to tell if your situation actually warrants hiring one

- The difference between the adjuster you hired and the one who showed up

- When water damage scope gaps make independent review necessary

- When fire damage complexity makes independent representation worth it

- When the gap between estimates is large enough to bring in a PA

- When bad faith makes legal action the only path that works

- PA, attorney, or appraisal clause: which path fits your denial

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.