- Suing your insurance company is a normal legal remedy when standard negotiations and appeals fail, not a dramatic last resort.

- The discovery phase is where these lawsuits are heavily fought. Be prepared to produce years of maintenance records and sit for a formal deposition.

- Most property insurance lawsuits settle during mediation before ever reaching a courtroom, but the process still requires significant time and documentation.

The Reality of Taking Your Insurer to Court

Suing your insurance company sounds extreme. For most homeowners, the idea of walking into a courtroom against a massive financial corporation feels overwhelming. However, in the world of property claims, litigation is simply a formal mechanism for resolving a contract dispute when all other avenues have been exhausted. It is a normal legal remedy, not an unprecedented event.

I am a property claims writer, not an attorney, and I cannot give you legal advice. But having reviewed hundreds of claim files and watched them transition from standard adjuster negotiations into full legal battles, I know exactly what the mechanical steps look like from the policyholder side. Many homeowners jump to the threat of a lawsuit out of frustration, without understanding the timeline, the intense scrutiny of the discovery process, or the emotional endurance required.

Before you make the decision to escalate your claim to a courtroom, you need to understand how the actual timeline and daily realities of an insurance lawsuit unfold. Knowing what happens after the complaint is filed removes the mystery and helps you make a realistic, financially sound decision about your property.

When Suing Becomes a Realistic Option

Litigation is rarely the first step. Insurance policies contain multiple mechanisms designed to resolve disputes before legal action is necessary. A lawsuit typically becomes a realistic path only after these internal and regulatory mechanisms have failed to yield a fair result.

In a typical progression, a homeowner will first dispute an initial adjuster estimate by providing independent contractor bids. If the insurer refuses to revise the scope, the homeowner might request a reinspection or file a formal internal appeal. If your policy contains an appraisal clause, this dispute resolution mechanism should also be attempted before litigation to resolve pricing differences without courtroom costs.

Homeowners may also escalate the issue by filing a complaint with their state Department of Insurance, which acts as a regulatory path rather than a legal one. For a broader overview of the warning signs that indicate you need legal intervention, you can review our main guide on when an insurance claim crosses the line into legal territory.

Litigation enters the picture when the internal appeal is exhausted, when appraisal is denied or unhelpful, when the Department of Insurance complaint does not resolve the core financial dispute, or when the insurer’s conduct crosses into documented bad faith. Most importantly, a lawsuit becomes viable when the financial gap between your actual repair costs and the insurer’s settlement offer is large enough to justify the time and expense of the legal process.

What Type of Lawsuit Are You Filing?

When you take legal action against an insurance carrier, you are generally filing one of two types of claims, or sometimes a combination of both. Understanding the foundation of your lawsuit dictates what you have to prove and what you can potentially recover.

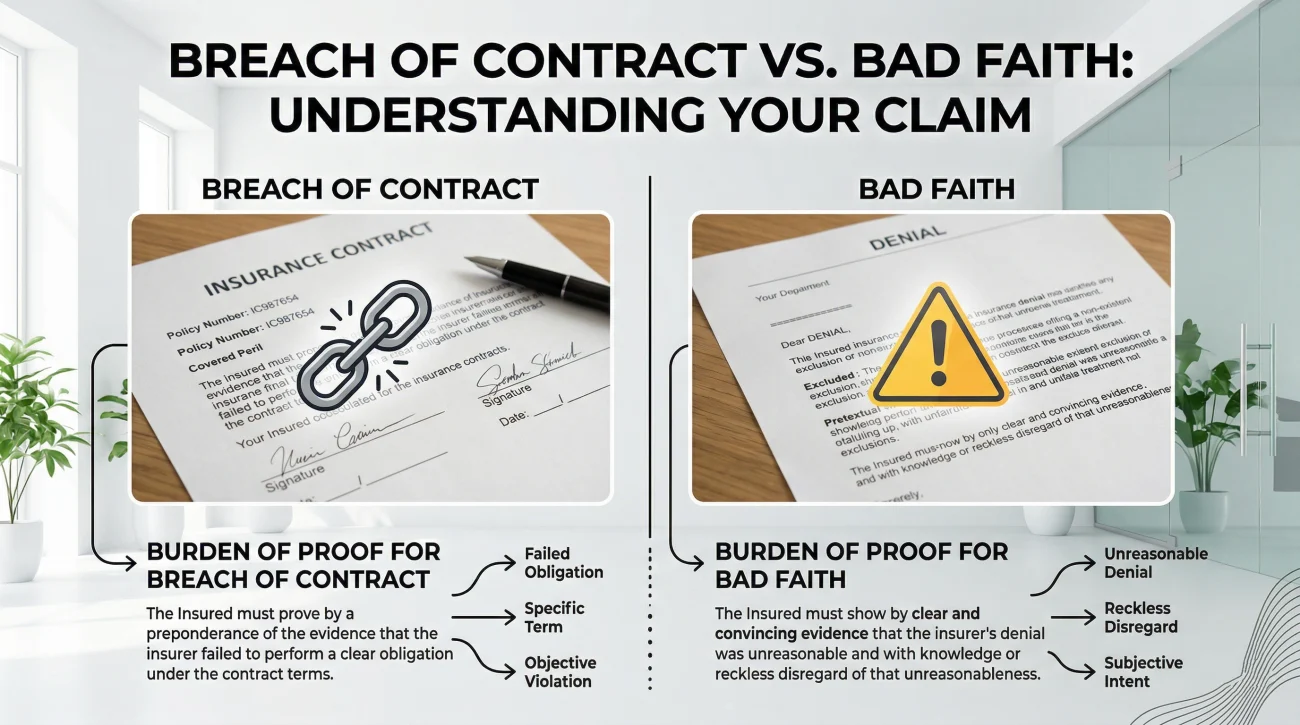

The first and most common type is a breach of contract lawsuit. Your homeowners insurance policy is a legally binding contract. If a covered peril damages your home and the insurer fails to pay the amount required by the policy language, they have breached that contract. In a breach of contract suit, you are simply asking the court to force the insurer to pay the benefits you were rightfully owed under the policy, plus standard interest.

The second type is a bad faith lawsuit. This is a heavier accusation. A bad faith claim asserts that the insurer did not just make a wrong coverage decision, but that they acted unreasonably, deceptively, or unfairly in their handling of your claim. To pursue this, you need specific evidence of improper conduct. If you believe your carrier’s actions were intentional or negligent, you should review the specific mechanics of a homeowners insurance bad faith lawsuit to understand the higher burden of proof required.

Often, attorneys will file a complaint that includes counts for both. They will argue that the insurer breached the contract by not paying, and they acted in bad faith during the process of denying it. Differentiating between these two legal theories is critical because they yield different damages. For a detailed comparison, see our explanation of the difference between breach of contract and bad faith claims.

Pre-Suit Steps: The Demand Letter and Deadlines

You do not simply wake up one morning and file a lawsuit. The litigation process begins with formal pre-suit steps that attorneys require to build the foundation of your case.

The most critical pre-suit action is the demand letter. Your attorney will draft a formal letter to the insurance company outlining the exact nature of the dispute, citing specific policy language, detailing the financial damages, and giving the insurer a final deadline to cure the breach by paying the requested amount. This letter serves as the official warning that litigation is imminent. Sometimes, a well drafted demand letter is enough to force a stubborn insurer back to the negotiation table.

* A chronological summary of the claim history.

* Identification of specific policy provisions the insurer violated.

* Enclosed independent engineering reports or contractor estimates.

* A strict deadline to respond, usually 15 to 30 days.

During this pre-suit phase, your attorney will also verify your filing deadlines. This is a critical step because missing a deadline permanently destroys your right to sue. Insurance disputes involve strict timelines, and you must understand the lawsuit filing deadlines written directly into your policy language, which often set a stricter window than you might expect.

Filing the Lawsuit: The Complaint and Response

If the deadline in the demand letter passes without a satisfactory resolution, your attorney will formally initiate the lawsuit by filing a “Complaint” in civil court. The complaint is the foundational document of your lawsuit. It introduces you as the plaintiff and the insurance company as the defendant, lays out the factual history of the property damage, and states the exact legal reasons why the insurer is liable for damages.

Once the complaint is filed with the court clerk, the insurance company must be formally served with the documents. The clock then starts ticking for the insurer to respond. In most jurisdictions, the insurance company has 20 to 30 days to file their “Answer.”

Do not expect the insurer to surrender in their Answer. The standard practice for insurance defense attorneys is to deny almost every allegation in your complaint. They will also list “affirmative defenses,” which are legal reasons why they believe they owe you nothing, such as alleging you failed to mitigate the damage or failed to report the claim promptly. Seeing this aggressive response on paper can be alarming for a homeowner, but it is standard procedural posturing.

The Discovery Phase: Where Lawsuits Are Won or Lost

That aggressive posturing, however, is just the opening move. The real battle begins in discovery. Once the initial pleadings are filed, the lawsuit enters the discovery phase. This is the longest, most invasive, and most expensive part of the litigation process. Discovery is the formal exchange of information between your attorney and the insurance company’s defense team. There are no secrets in civil litigation, and both sides are entitled to review the evidence the other side plans to use.

From the homeowner’s perspective, discovery feels like an intense audit of your personal life and property maintenance habits. You must be prepared to participate actively in this phase.

Document Requests

The defense attorneys will send a “Request for Production of Documents.” They will ask for everything remotely related to your home. You may be required to produce years of tax returns, mortgage statements, receipts for every remodeling project you have ever done, past plumbing or roofing repair invoices, and every email or text message you exchanged with contractors. Their goal is to find evidence of pre-existing damage, lack of maintenance, or financial distress that might give them leverage.

Conversely, your attorney will demand the insurer’s entire claim file. This is where cases are often won. Your attorney will seek the adjuster’s internal log notes, emails between the field adjuster and the desk adjuster, drafts of estimates that were mysteriously reduced before being sent to you, and the carrier’s internal guidelines for handling claims.

Interrogatories

Interrogatories are written questions sent by the opposing side that you must answer under oath. These questions ask for detailed chronologies of the damage event, the names of every person who has inspected the property, and itemized breakdowns of your alleged damages. Your attorney will help you draft these answers carefully to ensure they are accurate and do not inadvertently harm your case.

The Deposition Experience

The most stressful part of discovery for a homeowner is the deposition. A deposition is an in-person, formal interview where the insurance company’s defense attorney asks you questions under oath, while a court reporter records every word. Your own attorney will be sitting next to you to object to improper questions, but you must answer the valid ones.

Homeowners are often shocked by how aggressive defense attorneys can be during a deposition. They will question your memory of the storm date, challenge your maintenance history, and parse every word you said in your initial claim report. Preparation with your attorney is the only way to survive a deposition without giving the defense the soundbite they are looking for./p>

Settlement Negotiations and Mediation

As discovery progresses and both sides see the strengths and weaknesses of the evidence, the financial risk becomes clearer. If those internal emails uncovered during document production contradict the denial letter, the insurer will likely want to settle. If your contractor’s estimate has major flaws exposed during deposition, your attorney may advise you to settle.

Before proceeding to a trial, many courts mandate a formal mediation session. During mediation, you, your attorney, the defense attorney, and an insurance representative with settlement authority will meet with a neutral third-party mediator. You will typically sit in one room while the defense sits in another, and the mediator shuttles between the rooms carrying offers and counteroffers in an attempt to find a middle ground.

To prepare for mediation, you need to work with your attorney to define your absolute bottom-line number and understand the tax implications of different settlement structures. For example, property damage settlements are typically non-taxable, while punitive damages from a bad faith claim might be treated differently. Mediation is highly effective, which is why it is a statistical reality that the vast majority of property insurance lawsuits never see the inside of a courtroom.

If an agreement is reached, you will sign a binding settlement agreement and a release of claims, the insurer will issue the check, and the lawsuit will be dismissed.

| Phase | What the Homeowner Does | What the Attorney Does |

|---|---|---|

| Pre-Suit | Gathers initial documents, photos, and contractor estimates. | Drafts the formal demand letter and verifies filing deadlines. |

| Pleadings | Reviews the complaint for factual accuracy. | Files the lawsuit and reviews the insurer’s legal answer. |

| Discovery | Gathers historical home records and testifies at deposition. | Demands internal claim files, deposes adjusters, defends client. |

| Resolution | Approves or rejects settlement offers based on counsel. | Negotiates at mediation or presents the case before a jury. |

What a Lawsuit Does NOT Guarantee

Filing a lawsuit is a powerful tool, but it is not a magic wand. You must enter the process with realistic expectations. A lawsuit does not guarantee speed. The civil court system is heavily backlogged, and a standard property insurance lawsuit can easily take twelve to twenty-four months from filing to resolution.

Furthermore, a lawsuit does not guarantee a specific financial outcome. You are putting the final decision in the hands of a mediator, a judge, or a jury. There is always a risk involved in litigation, which is why having an experienced property insurance attorney carefully evaluate your evidence before filing is absolutely critical.

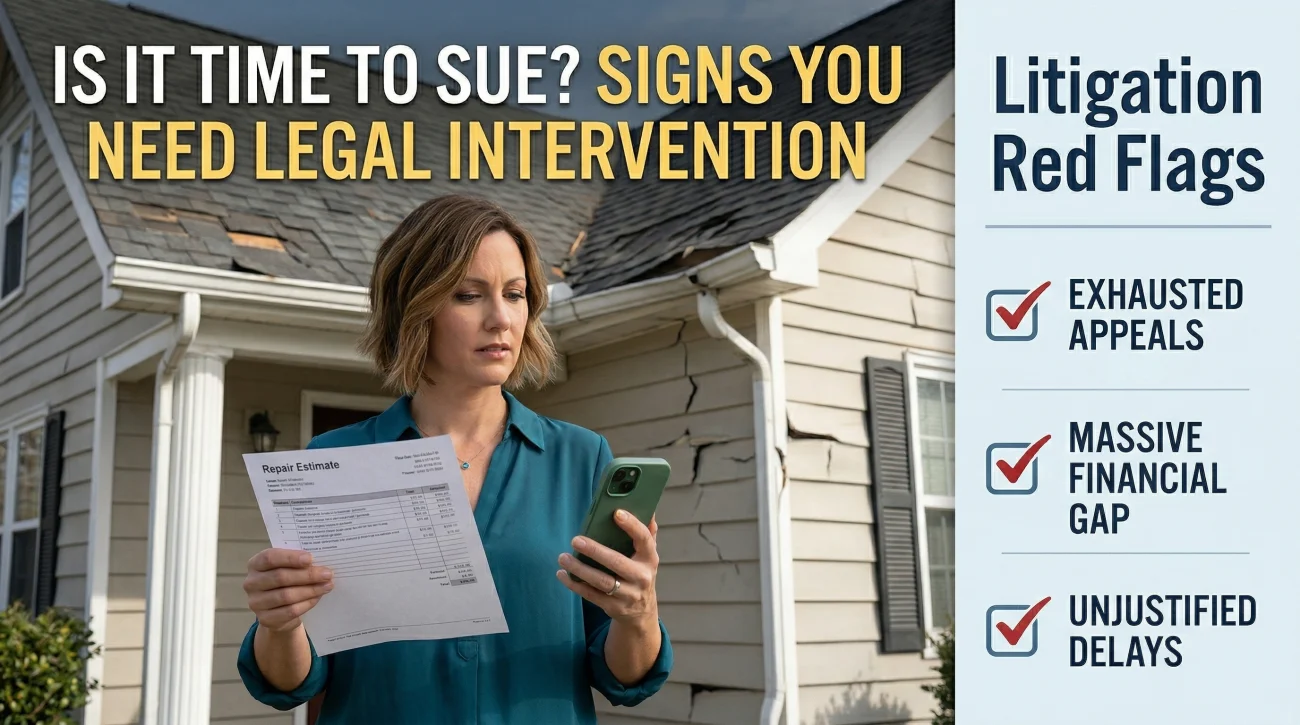

Signs Litigation May Be Your Appropriate Path

The decision to sue should never be taken lightly, but there are specific scenarios where continuing to negotiate without legal leverage is a waste of time. If you are exhausted from fighting your carrier, you must evaluate whether your claim has hit a hard wall.

Here are the clear signs you are in a situation where litigation may be the appropriate path:

- Exhausted Appeals: You have submitted multiple rounds of supplemental estimates and formal appeals, yet the insurer has made no substantive change to their position for months.

- Documented Bad Faith: You have written proof that the insurer ignored evidence, fabricated reasons for denial, or violated the claim handling timelines stated in your policy or outlined by your insurer.

- Massive Financial Gap: The discrepancy between your actual contractor repair costs and the insurer’s settlement offer is tens of thousands of dollars, making it impossible to restore your home without a full recovery.

- Unjustified Delays: The claim has been dragged out for months or years with endless requests for identical documents and no clear path to resolution.

- Unreasonable Exclusions: The denial cites an exclusion (like earth movement or wear and tear) that your independent engineering reports explicitly refute.

If your situation matches these patterns, a free legal consultation can clarify whether filing a lawsuit is the right mechanical step for your specific dispute. You can connect with an insurance claim attorney for a case evaluation to review the merits of your file.

How Do You Pay for an Insurance Lawsuit?

A major reason homeowners hesitate to sue is the fear of crippling legal fees. However, most property insurance attorneys operate on a contingency fee basis. This means there are no upfront hourly rates. The attorney takes a percentage of the final recovery, typically after the case resolves. If they do not win or settle your case, you generally do not pay their attorney fees. This structure allows homeowners to leverage professional legal representation against large corporate defense teams without taking on upfront financial risk.

The Final Decision to File

Suing your home insurance company is a complex procedural journey that requires patience, flawless documentation, and professional guidance. The insurance company has a team of defense lawyers whose sole job is to protect the carrier’s financial interests. Attempting to navigate the pleadings, discovery, and mediation phases on your own puts you at a massive structural disadvantage.

The ultimate question you must ask yourself is this: does your current settlement offer allow you to actually restore your home safely and correctly? If the answer is no, and you have reached the end of the negotiation road, seeking legal counsel is the definitive next step.

❓ FAQ

⚖️ Can I sue my home insurance company for denying my claim?

Yes, you can sue your insurance company for breach of contract if they wrongfully denied a valid claim covered by your policy, provided you file within the filing deadlines set by your policy.

📝 What is the first step to sue an insurance company?

The first formal step is typically having an attorney draft and send a pre-suit demand letter detailing the dispute and giving the insurer a final deadline to pay before a lawsuit is filed.

⏳ How long does a lawsuit against an insurance company take?

A property insurance lawsuit usually takes anywhere from 12 to 24 months to resolve, depending on court backlogs and whether the case settles during mediation or goes to trial.

💰 Do I have to pay a lawyer upfront to sue my insurance company?

Usually no. Most property insurance attorneys work on a contingency fee basis, meaning they do not charge upfront hourly rates and only get paid a percentage if they win or settle your case.

🔍 What happens during the discovery phase of an insurance lawsuit?

During discovery, both sides exchange evidence. You will be required to provide home maintenance documents, repair receipts, and answer written questions, and you will likely have to sit for a deposition.

🗣️ What is a deposition in a home insurance lawsuit?

A deposition is a formal question-and-answer session where the insurance company’s defense attorney asks you questions under oath about your property and the damage, recorded by a court reporter.

🤝 Do most home insurance lawsuits go to trial?

No, the vast majority of homeowners insurance lawsuits settle out of court, often during a formal mediation session after the discovery phase is largely complete.

🛑 Can I sue my insurance company in small claims court?

Yes, if the disputed amount falls within the small claims court limit in your area, you can file there, but this is generally only useful for very small underpayment disputes.

📜 What is the difference between a breach of contract and bad faith?

Breach of contract means the insurer simply failed to pay what they owed. Bad faith means their conduct in denying or delaying the claim was unreasonable, deceptive, or unfair.

📅 How long do I have to file a lawsuit against my insurance company?

You must check the “suit against us” clause in your actual policy, which often sets a strict deadline of one to two years from the date of loss, regardless of what you might expect from general contract principles.

Most disputes start with a payout disagreement. These cover the earlier stages.

- The claim lifecycle a PA or attorney works inside

- The policy language that determines what professional help can recover

- How damage classification affects what an expert can negotiate

- Whether the situation you have justifies bringing in outside help

- When a denial is the outcome a PA could have prevented

- What a public adjuster actually does inside a claim

- When the dispute has moved past what a PA can handle

Two paths, two different situations. These clarify which one fits yours.

- How to tell if your situation actually warrants hiring one

- The difference between the adjuster you hired and the one who showed up

- When water damage scope gaps make independent review necessary

- When fire damage complexity makes independent representation worth it

- When the gap between estimates is large enough to bring in a PA

- When bad faith makes legal action the only path that works

- PA, attorney, or appraisal clause: which path fits your denial

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.