- A breach of contract occurs when the insurer fails to pay what the policy covers, while bad faith means they acted unreasonably or deceptively in handling your claim.

- The type of claim you file dictates your potential recovery. Breach covers exactly what you are owed, whereas bad faith can include additional damages like attorney fees and consequential losses.

- You do not always have to choose just one. In many cases, property damage attorneys will pursue both claims simultaneously, though bad faith requires a much higher burden of proof.

When a Claim Denial Becomes a Legal Dispute

When I sit down with homeowners who have just received a devastating denial letter, the first reaction is almost always anger. You pay your premiums for years, and when disaster strikes, the carrier either refuses to pay or offers a fraction of the real repair cost. When homeowners decide it is time to take legal action, they often assume there is only one type of lawsuit to file. The reality is much more nuanced.

If your carrier has denied a valid claim or severely underpaid your damages, there are two distinct legal theories you need to understand: a breach of contract vs bad faith insurance claim. Knowing the difference between the two is not just a technicality for lawyers to argue over. It fundamentally changes what you have to prove, how the discovery process works, and what you can actually recover financially.

In my experience reviewing hundreds of property damage files, the line between a simple adjuster mistake and an intentional, unreasonable denial is where the most intense battles happen. Understanding these two paths is the very first step in evaluating when an insurance claim lawyer is necessary to protect your home and your financial stability.

Breach of Contract Insurance Claim Explained

To understand the difference between the two claims, you first need to look at your insurance policy for what it truly is: a legally binding commercial contract. You agree to pay your premiums, and in exchange, the insurance company agrees to pay for covered perils according to the exact language printed in that document.

An insurance breach of contract claim is simply an assertion that the insurer broke that specific promise. It means a loss occurred, the policy provided coverage for that type of loss, and the insurer failed to pay the correct amount. The focus here is entirely on the policy language and the physical damage to your home.

When you file a lawsuit based solely on a breach of contract, the court is looking at the facts of the damage. The adjuster’s bad attitude, the annoying delays in communication, or the disorganized nature of the carrier’s claims department do not heavily factor into a pure breach case. The only question the judge or jury cares about is whether the carrier owed you the money under the terms of the agreement.

I recently reviewed a wind damage file where the carrier denied a roof replacement because they claimed the damage was standard wear and tear. Our independent engineer proved it was sheer wind uplift. The carrier’s initial decision was wrong, but their investigation process was standard. They sent out a qualified inspector promptly. That is a classic example of a breach of contract without the element of bad faith.

What a Bad Faith Claim Adds to the Equation

If a breach of contract asks whether the insurer made the wrong decision, a bad faith claim asks a much harder question: why did they make that decision, and was their conduct unreasonable? Insurers have a legal duty, often called the implied covenant of good faith and fair dealing, to handle your claim fairly, investigate thoroughly, and communicate honestly.

Bad faith does not usually look like a screaming match on the phone; it looks like administrative weaponization. It involves a documented pattern of the carrier prioritizing their financial interests over your contractual rights.

I recall a fire claim where the carrier denied $50,000 in structural repairs. The desk adjuster relied entirely on a blurry drone photograph taken from a neighbor’s yard, blatantly ignoring detailed reports from three local fire remediation experts who had actually stood inside the burned living room. Their refusal to look at valid, ground-level evidence was not an oversight. It was an intentional and unreasonable failure to investigate, which is the very definition of bad faith.

⚠️ Warning: Poor customer service is not automatically bad faith. An adjuster who is slow to return calls, seems rude, or rotates out to a new desk adjuster three times is deeply frustrating. However, bad faith requires a legal showing of unreasonable conduct that directly impacts the outcome of your claim, not just poor corporate manners.

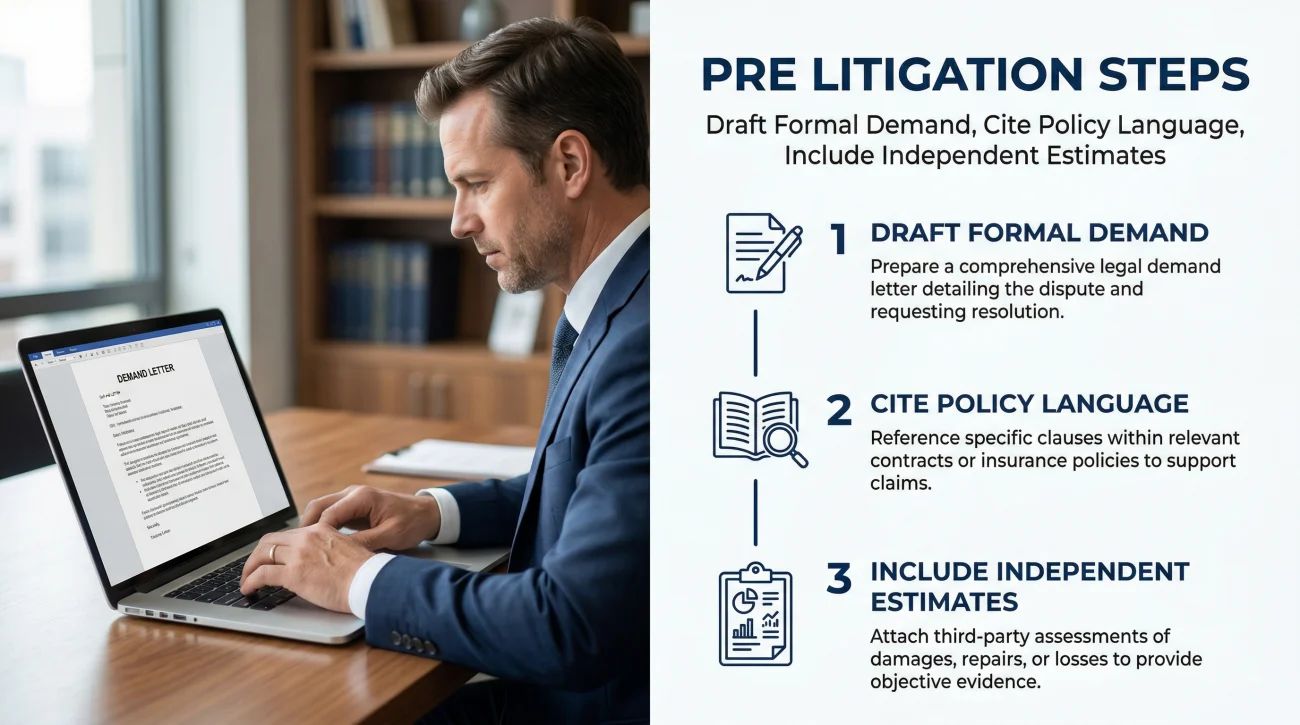

The Step Before the Lawsuit: Pre-Litigation Demands

Homeowners often think the process jumps immediately from a denial letter to a courtroom. In reality, there is a crucial middle ground. Before any formal lawsuit is filed, whether for breach or bad faith, the dispute usually goes through a pre-litigation phase.

If you hire legal representation, they will typically draft a formal demand letter. This document lays out exactly how the carrier breached the contract, cites the relevant policy language, includes all independent estimates, and gives the insurer a final deadline to pay the undisputed amounts. In many states, sending a specific type of demand letter is actually a legal prerequisite before you can file a bad faith lawsuit.

This is also the phase where alternative dispute resolutions, like the appraisal clause, might be invoked if the disagreement is purely about the cost of repairs rather than coverage. It is a calculated step to force the carrier’s legal department to review what the field adjuster did wrong. In fact, many property damage disputes are successfully resolved during this pre-litigation phase, securing a fair settlement without you ever having to step foot inside a courtroom.

Red Flags in Your Denial Letter

When you feel like you are fighting a massive corporation that is intentionally burying you in paperwork, the proof is usually sitting right in your hands. Attorneys look very closely at the specific language used to deny a claim to see if it leaves a paper trail of deceptive practices.

Watch out for these specific red flags in your carrier’s correspondence:

- 🚩 Vague Citations: The letter quotes three pages of general policy exclusions but never explains how those exclusions apply to the specific facts of your home’s damage.

- 🚩 The “Wear and Tear” Default: Denying a sudden, accidental water pipe burst by classifying it as “long-term seepage” without performing any moisture mapping or material testing.

- 🚩 Moving the Goalposts: You submit the exact document they requested, and they immediately respond by asking for a completely different, previously unmentioned set of records.

Assuming that every low settlement offer automatically gives you grounds for a multi-million dollar bad faith lawsuit.

Documenting the specific instances where the insurer failed to follow their own investigative duties or ignored concrete evidence you provided.

Financial Recovery and Realistic Outcomes

The reason the distinction between these two claims matters so much comes down to damages. The type of lawsuit you file dictates the financial remedy the court can award you.

In a pure breach of contract case, the law simply aims to make you whole based on the contract. If your kitchen cost $40,000 to rebuild and they wrongfully denied it, your damages are $40,000 plus standard statutory interest. You generally cannot recover the money you spent paying a lawyer out of that amount unless your state has a specific fee-shifting statute.

Because bad faith involves unreasonable conduct, the law allows for additional damages to penalize the insurer. This can include attorney fees, court costs, and consequential damages (such as the cost of a rental home if their delay forced you to live elsewhere).

| Claim Theory | Primary Focus | Potential Financial Recovery |

|---|---|---|

| Breach of Contract | The language of the policy and the physical damage. | Policy benefits owed + standard interest. |

| Bad Faith | The carrier’s conduct, delays, and investigation quality. | Policy benefits, attorney fees, consequential damages. |

A note on Punitive Damages: You often hear about massive jury verdicts against insurance companies. These involve punitive damages, which are designed purely to punish egregious corporate behavior. While they make headlines, they are exceedingly rare in real-world property claims. Most bad faith claims result in a negotiated settlement that covers the repair costs, attorney fees, and immediate out-of-pocket losses, rather than a lottery-sized courtroom verdict.

The Claim File: Proving What Happened Behind Closed Doors

Knowing that punitive damages or attorney fees are theoretically possible does not mean the carrier will simply hand them over. Proving you are entitled to that financial recovery is a completely different hurdle. While a breach of contract relies on physical evidence, proving unreasonable conduct in court requires a look behind the curtain.

To prove bad faith, the focus shifts entirely to the insurer’s internal behavior. The most critical piece of evidence is the insurer’s internal claim file. This file contains the adjuster’s private notes, emails between supervisors, directions given to independent experts, and the timeline of internal decisions.

If an attorney uncovers an internal note where a desk adjuster tells a field inspector to rewrite a report to remove the mention of wind damage, that is the foundation of a bad faith case. You do not have to wait for a lawsuit to ask for your file. Requesting it in writing is a strong operational move that signals to the carrier you are documenting their process.

Hello [Adjuster Name],

As we remain in disagreement regarding the coverage decision on my claim, I am formally requesting a complete copy of my claim file.

Please include all adjuster activity logs, internal notes, third-party vendor reports (including drafts), and communications related to the investigation of my claim. Please let me know when I can expect this documentation.

Thank you,

[Your Name]

Can You Sue for Both Breach of Contract and Bad Faith?

One of the most frequent questions homeowners ask is whether they have to choose between the two paths. The short answer is no. In fact, it is standard practice for attorneys to file both claims in the same lawsuit.

In legal terms, these are filed as separate “counts” within the same complaint. Count one alleges the insurer breached the contract by failing to pay. Count two alleges they acted in bad faith during the process. The mechanics of a bad faith lawsuit build directly on top of the underlying breach.

However, there is a practical reality to how these cases play out in negotiations. Because bad faith is much harder to prove and exposes the carrier to higher damages, insurers fight those counts aggressively. In many instances, during mediation or settlement talks, an attorney might leverage the threat of the bad faith count to force the carrier to pay the full breach of contract amount plus attorney fees. Sometimes, the bad faith claim is dropped in exchange for a swift, full-value settlement on the property damage.

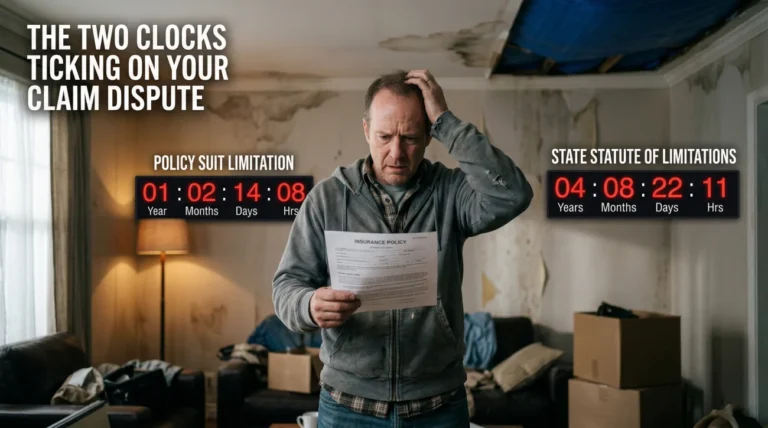

Statute of Limitations: The Clock is Ticking

If you are debating which legal theory applies to your situation, you need to be highly aware of the calendar. Property insurance claims have strict filing deadlines, known as the statute of limitations, and waiting too long can forfeit your right to sue entirely.

What catches many homeowners off guard is that bad faith standards and deadlines vary significantly by state. In some jurisdictions, you have several years to file a breach of contract lawsuit, but a much shorter window to file a bad faith claim. Furthermore, your specific insurance policy likely contains a “suit against us” clause that mandates legal action be taken within one or two years from the date of the damage, regardless of what the state law says.

If you are exploring how to sue your home insurance company, confirming your exact legal deadline is the most urgent administrative task you have.

What an Attorney Evaluates During a File Review

When you take your disputed claim to a legal professional, they do not just look at the final denial letter. They look at the entire history of the correspondence to determine which theory holds weight. Attorneys look for specific triggers that indicate the carrier’s internal process broke down.

Here is what a professional file review is actively hunting for:

- 🔍 Citing non-existent policy language: When an adjuster cites an exclusion that does not exist in your specific policy endorsement, it is not just sloppy reading. Legally, this demonstrates a failure of the carrier’s fundamental duty to evaluate the actual contract they sold you, crossing from error into intentional misrepresentation.

- 🔍 Endless documentation loops: Demanding the same exact paperwork four different times is rarely an accident. Legally, courts recognize this as an exhaustion tactic, a bad faith strategy designed to artificially delay payment until the homeowner gives up.

- 🔍 Expert shopping: If the carrier sends out an engineer who confirms wind damage, and the carrier buries that report to hire a second engineer to say it was wear and tear, that is a massive indicator of bad faith intent.

Having a clear timeline of events, all written correspondence, and your own independent estimates organized in chronological order makes this evaluation process significantly faster.

The First Step in Evaluating Your Options

Remember that devastating denial letter you are holding right now? It does not have to be the final word. Navigating a disputed claim is about stopping the administrative delays and holding a massive corporation accountable to the exact promises they made. The legal standards vary wildly from state to state, and insurers have teams of defense lawyers whose sole job is to protect the company from bad faith exposure.

If you have hit a wall in your negotiations, have provided all requested proof, and suspect the carrier is intentionally suppressing your settlement, the next logical step is having a professional review the file. Most property damage attorneys offer free initial case evaluations specifically to determine which legal theory applies to your facts. Taking the time to schedule a free consultation with a property damage attorney can clarify your rights, identify your exact deadlines, and outline the path forward without upfront financial risk.

❓ FAQ

⚖️ What is the main difference between breach of contract and bad faith?

A breach of contract means the insurer failed to pay what the policy covers based on the facts. Bad faith means they acted unreasonably, deceptively, or unfairly in how they investigated and handled the claim.

📝 How do I prove my insurance company breached the contract?

You must prove that a loss occurred, the specific damage is covered under your policy language, and the insurance company failed to pay the amount required to repair it.

💰 Can you sue for both claims at the same time?

Yes. It is standard practice to include both counts in a single lawsuit. You sue them for failing to pay the claim, and separately for acting unreasonably while processing it.

⏳ Is there a deadline to file a lawsuit against my insurance company?

Yes. You are bound by the statute of limitations in your state and the specific “suit against us” clause in your policy, which is often much shorter (typically one to two years from the date of loss).

📑 What is a pre-litigation demand letter?

It is a formal letter sent by your attorney to the insurer before filing a lawsuit. It outlines the breach, provides evidence, and gives the carrier one final deadline to pay the undisputed amount.

🚫 Is it harder to win a bad faith lawsuit than a simple denial?

Yes. Proving bad faith requires a much higher burden of proof. You must show evidence of the insurer’s unreasonable intent or gross negligence, not just a mathematical error.

🧑⚖️ Do I need to hire a lawyer for an insurance dispute?

While technically possible to represent yourself in small claims court for minor amounts, suing an insurer in civil court involves complex procedures and obtaining internal documents that almost always require a licensed attorney.

Most disputes start with a payout disagreement. These cover the earlier stages.

- The claim lifecycle a PA or attorney works inside

- The policy language that determines what professional help can recover

- How damage classification affects what an expert can negotiate

- Whether the situation you have justifies bringing in outside help

- When a denial is the outcome a PA could have prevented

- What a public adjuster actually does inside a claim

- When the dispute has moved past what a PA can handle

Two paths, two different situations. These clarify which one fits yours.

- How to tell if your situation actually warrants hiring one

- The difference between the adjuster you hired and the one who showed up

- When water damage scope gaps make independent review necessary

- When fire damage complexity makes independent representation worth it

- When the gap between estimates is large enough to bring in a PA

- When bad faith makes legal action the only path that works

- PA, attorney, or appraisal clause: which path fits your denial

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.