- Filing a claim is a financial calculation, not an automatic reflex. The wrong call can cost you more in future premiums than the claim pays out.

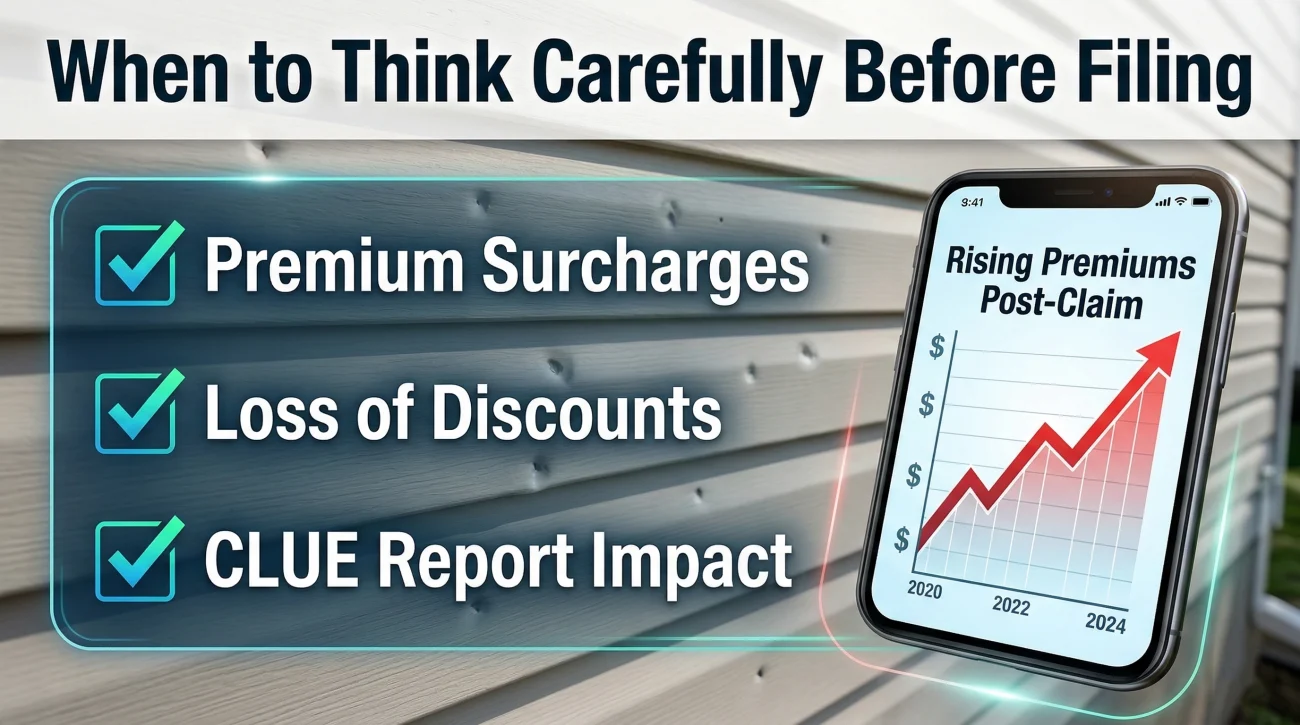

- Do not rely solely on the advice to “file if the damage is over your deductible.” You must factor in the loss of claim-free discounts and a typical three to five year rate surcharge.

- Claims and zero-pay inquiries stay on your CLUE report for typically five to seven years, following you to any new property or new insurance carrier.

- Filing for an inadequate settlement is the worst possible outcome. You take the permanent record hit and the rate increase, but still have to pay out of pocket to finish the repairs.

The Decision Homeowners Get Wrong

Filing a home insurance claim sounds straightforward. Damage happens, you have a policy, you pay your premiums, so you file a claim. Most online advice oversimplifies the next step, telling you to simply file if the repair cost is higher than your deductible.

As a property claims writer who has analyzed how the system actually operates, I can tell you that this math is fundamentally incomplete. Your deductible is just the entry fee. It does not account for the long-term financial echo of a filed claim.

I frequently review files where a homeowner filed a claim for $2,500 in water damage, received a $1,500 check after their deductible, and then paid $3,000 in increased premiums over the next four years. They essentially paid their insurer for the privilege of fixing their own home.

To make an informed decision, you need a multi-factor framework. You have to weigh the actual repair costs against the hidden penalties of filing: rate surcharges, the loss of discounts, the permanent tracking of your property history, and the risk of non-renewal. You also have to consider the risk of going through the entire process only to receive a settlement that does not actually cover your contractor’s estimate.

Before you pick up the phone to report damage, let us walk through the exact variables you need to calculate. By the end of this guide, you will know exactly when it makes financial sense to trigger your policy, and when it is safer to absorb the cost yourself.

The Deductible: Why It Is Only the Starting Line

The most common advice homeowners hear is that if the damage is $500 over the deductible, you should file. This is dangerous advice. To understand why, we first need to look at how deductibles actually function, because many homeowners misunderstand their own policy structure.

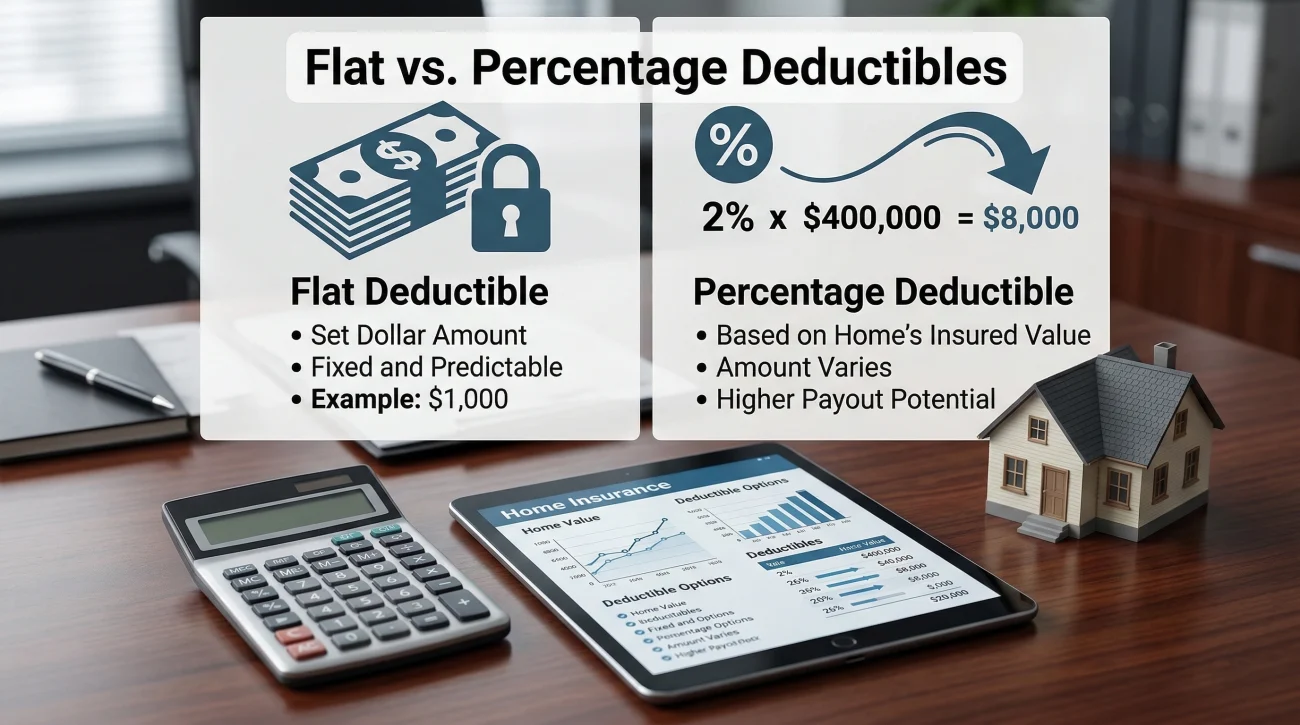

Flat Dollar vs. Percentage Deductibles

If you have a flat dollar deductible, the math is easy to see. A $1,000 deductible means you pay the first $1,000, and the insurer pays the rest up to your policy limit. However, a massive portion of policies today, especially in areas prone to storms, rely on percentage deductibles.

A percentage deductible is based on your home’s total insured dwelling value (Coverage A), not the amount of the damage. If your home is insured for $400,000 and you have a 2 percent wind and hail deductible, your out of pocket responsibility for a storm claim is $8,000. I have sat with homeowners who thought they had a standard $1,000 deductible, only to discover their specialized storm deductible wiped out any chance of a payout.

Assuming your standard flat deductible applies to all types of damage.

Checking your declarations page specifically for separate wind, hail, or hurricane percentage deductibles before calling a roofer.

The Actual Cash Value (ACV) Depreciation Trap

The deductible is not the only thing subtracted from your payout. The way your policy values your property matters just as much. If your policy pays Actual Cash Value (ACV) rather than Replacement Cost Value (RCV) for certain items, the insurer will deduct for age and wear and tear before they even apply your deductible.

Let us say you have a 15-year-old roof that sustains $12,000 in wind damage. The insurer determines the roof has outlived 75 percent of its useful life. They depreciate the value by $9,000. The remaining ACV is $3,000. Now, they apply your $2,000 deductible. Your final check is $1,000 for a $12,000 repair. Filing a claim to receive $1,000 is almost always a bad financial move once you factor in the rate increases that will inevitably follow.

Do Home Insurance Claims Raise Your Rates?

The short answer is typically yes. Unlike health insurance, where you are expected to use your benefits for routine care, home insurance is designed strictly for catastrophic, sudden losses. When you use it, the carrier recalculates your risk profile.

How Surcharges Work

After a paid claim, most insurers apply a surcharge percentage to your base premium at your next policy renewal. Understanding how long and how much your rates will increase is crucial, as this surcharge typically lasts for three to five years, depending on your state and the insurer’s specific underwriting guidelines. During that entire period, every renewal bill you receive will include this higher rate.

The amount your premium increases varies significantly. A single claim typically increases premiums by anywhere from 9 percent to 40 percent. The type of claim heavily influences this number. Water damage and fire claims tend to produce much higher premium surcharges than a straightforward wind or hail claim. Because data shows that a home with one water leak is statistically highly likely to have another, the decision to file for water damage requires a much stricter financial calculation.

The Hidden Cost: Losing Your Claim Free Discount

This is a variable almost no one talks about outside the industry. Many homeowners have a “claim free discount” automatically applied to their premium. They have had it so long they do not even realize it is there.

When you file a claim, two things happen at your next renewal. First, the insurer removes your claim free discount. Second, they apply the new surcharge. The combined effect of losing a 10 percent discount and gaining a 20 percent surcharge is the true cost of the claim. This is why a payout of $1,500 can easily cost you $3,000 over the next half decade.

Warning: The compounding problem is real. If you file a second claim within a short window, the surcharge multiplies rapidly. We will look closer at this specific risk later in the guide.

The Exception: Claim Forgiveness Programs

Some carriers offer “first claim forgiveness” for long-term customers with clean records. If you have this endorsement, your first claim might not trigger the standard rate surcharge. However, this does not give you a completely free pass. You will still likely lose your claim-free discount, and the incident will still be recorded on your CLUE report. Always verify your policy endorsements before assuming you are protected from a rate hike.

The CLUE Report: How Long Do Claims Stay on Record?

Your insurance history is not kept in a private file by your current carrier. It is logged into a massive national database. Understanding this database is critical when deciding whether to file.

The Comprehensive Loss Underwriting Exchange (CLUE) is a database maintained by LexisNexis. Almost all property and casualty insurers in the country report claims to this system, and they all check it when you apply for a new policy. Depending on the type of loss, an incident typically stays on your CLUE record for five to seven years.

The Danger of Zero-Pay Claims and Inquiries

This is where the system catches many homeowners off guard. A claim does not have to be paid to appear on your CLUE report. If you file a claim, the adjuster inspects, and the damage is determined to be under your deductible, that is recorded as a “zero-pay claim.” It still counts against your record.

Worse, with some carriers, simply calling your agent or the 1-800 number to ask “would this be covered if I filed?” can trigger an inquiry record that behaves similarly to a claim on your report. Insurers view a homeowner asking about water damage as a risk, whether a check is cut or not.

Key Point: The CLUE report follows the property and the person. If you sell your house, the new buyer’s insurer will see the claims you filed. If you move to a new state and buy a new house, your new insurer will see your past claims. You cannot outrun your claim history by switching companies.

The Ultimate Risk: Policy Non-Renewal

There is a threshold above which insurers decide they no longer want to raise your rates; they simply want you off their books. This is known as non-renewal, and it is a detail most homeowners only learn about after it happens to them.

Insurers can and do non-renew policies after multiple claims. The threshold varies by carrier and state, but generally, filing two non-weather-related claims in a three year period is a massive red flag. In high risk markets like coastal states or wildfire zones, even a single significant claim can trigger a non-renewal review.

If your standard carrier drops you, you will be forced to shop in the non-standard market or rely on state backed insurers of last resort. Policies in these markets provide less coverage, have stricter exclusions, and often cost two to three times as much as standard market premiums. The fear of non-renewal is exactly why you must protect your claim history and only use your policy for events you truly cannot afford to handle yourself.

When You Should Almost Always File

There are catastrophic scenarios where the decision to file is clear and necessary. When a loss threatens your home’s structural integrity or your family’s safety, the rate impact and CLUE record consequences become secondary concerns. If your situation fits into one of the following categories, your primary focus should be securing the property and triggering your policy’s protection.

- 👉 Catastrophic large losses: If a fire destroys your kitchen, a tree falls through your living room roof, or a burst pipe floods multiple floors, you file. When repair costs run into the tens of thousands or hundreds of thousands of dollars, out of pocket repair is not feasible. This is exactly what the policy is designed to cover.

- 👉 Damage affecting habitability: If the damage forces you out of your home, you need to file. Your policy likely includes Additional Living Expenses (ALE) coverage, or Loss of Use, which pays for your hotel, temporary rental, and extra food costs while your home is uninhabitable. This is incredibly expensive to pay out of pocket.

- 👉 Damage that will aggressively worsen: If you have an active situation that requires immediate, large scale professional mitigation, such as major water extraction to prevent toxic mold, filing promptly is necessary. Failing to address worsening damage can give the insurer grounds to deny the claim later due to neglect.

- 👉 Liability claims: If someone is severely injured on your property and threatens to sue, or if your dead tree falls and destroys your neighbor’s garage, you must notify your insurer. Liability costs can bankrupt a family, and your policy provides legal defense costs in addition to paying judgments.

When to Think Carefully Before Filing

This is the gray area where most homeowners make costly mistakes. If your situation falls here, you need to sit down, do the math, and seriously consider paying for the repair yourself to protect your long term insurability.

Damage Close to Your Deductible

If your deductible is $1,000 and the repair estimate is $1,800, you are filing a claim for an $800 net payout. As we established earlier, that $800 check will likely cost you thousands in future premium surcharges. For marginal claims and minor damage, absorbing the cost is almost always the better financial strategy.

Cosmetic Damage with No Structural Risk

A severe hailstorm might cause minor denting to aluminum siding or aesthetic pockmarks on a fence. If the integrity of the material is not compromised and water cannot enter the home, the damage is purely cosmetic. Filing a claim for cosmetic issues puts a permanent mark on your record for something that does not affect the safety of the house. Treat cosmetic wear as a maintenance issue.

The Second Claim in a Short Window

If you filed a claim two years ago, the bar for filing a new claim must be extremely high. The compounding effect of multiple claims is severe. Unless this second event is a catastrophic loss that you absolutely cannot afford to fix, you should do everything in your power to avoid filing and risking policy cancellation.

Planning to Sell Within Two Years

Claims stay attached to the property address in the CLUE database. If you file a claim today and attempt to sell your house next year, the buyer’s insurance company will see that history. In tight insurance markets, a recent claim on the property can cause the buyer’s insurance quotes to spike or result in outright coverage denials, which can derail your real estate transaction entirely.

The Settlement Adequacy Question Most Skip

We have discussed the math of the deductible, the rate impact, and the CLUE report. But there is one final, crucial variable that most homeowners completely skip when deciding to file: the risk of an inadequate settlement.

The standard assumption is: “If I file a claim, the insurance company will give me enough money to fix the damage.” In operational reality, this is frequently not the case. Adjusters write estimates based on standardized pricing software. They often leave out necessary line items, miscategorize materials (pricing custom cabinets as standard builder grade), or argue that certain damage was pre-existing.

This gap frequently occurs because of how insurers set the baseline for your claim. If you file before knowing the actual repair cost, the insurance company’s initial, often localized assessment becomes the official framing. Insurers use this early, incomplete picture to cap the settlement later. Once they have officially categorized the event as minor damage, fighting to prove the scope is actually much larger becomes an uphill battle.

If you file a claim and receive an inadequate settlement, you are trapped in the worst of all worlds. You have triggered the rate increase. You have placed a permanent entry on your CLUE report. But because the settlement is too low, you still do not have enough funds to pay your contractor. You are left fighting a stressful scope dispute just to get your home put back together.

The most frustrating cases I see are homeowners who filed for what they thought was $15,000 in damage, only to have the carrier assess it at $4,000. They took all the penalties of filing but received none of the financial relief. Knowing what the carrier will actually value the damage at is critical before making the decision.

This is why understanding every phase of how to file a claim properly, from initial documentation to scope negotiations, is vital to ensure you do not walk into a financial trap.

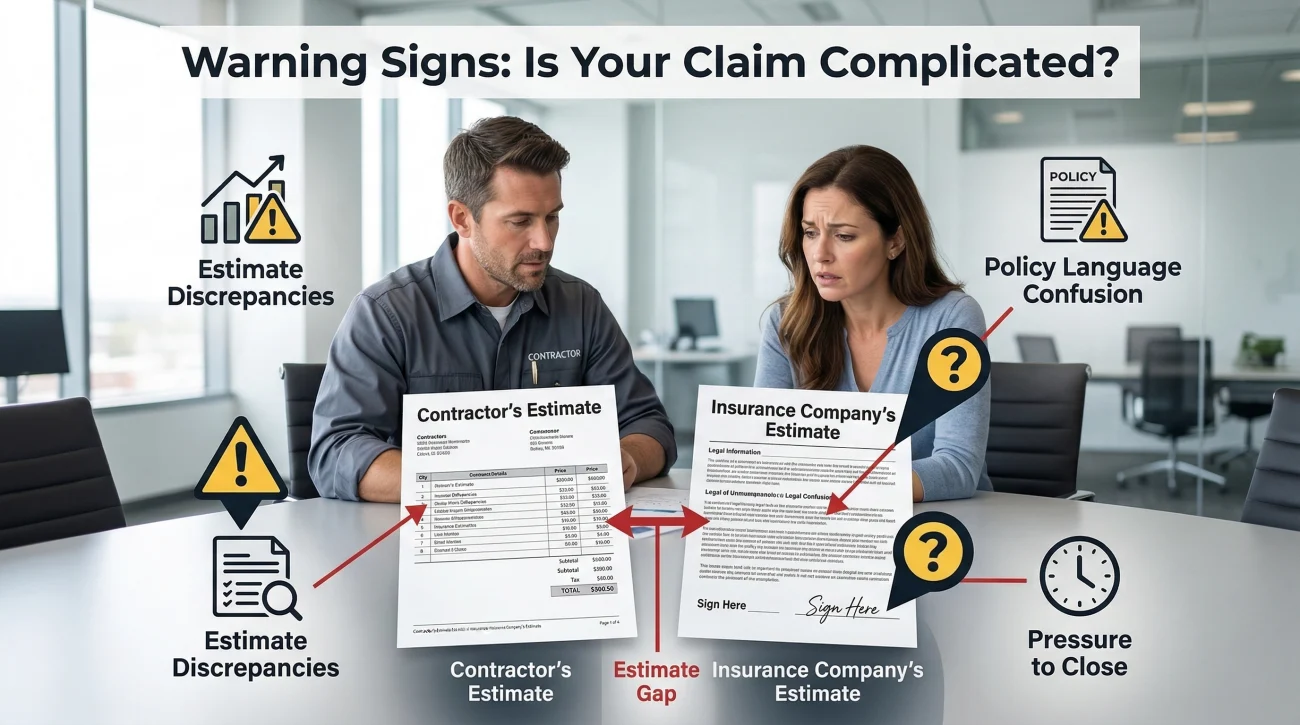

Signs the Filing Decision Is More Complicated Than It Appears

If you have already started the process, or if you are staring at a piece of damage wondering what to do, you might be feeling the pressure. The system is complex, and the frustration usually sets in when the reality of the claim process does not match your expectations. If you are experiencing any of the following, the simple “file and forget it” approach will not work for you.

Note these warning signs:

- 👉 The estimate gap: You filed, but the settlement offer from the adjuster does not even come close to covering the repair estimate your independent contractor provided. The insurer is claiming your contractor is too expensive, while your contractor says the insurer’s software is leaving off required construction steps.

- 👉 The policy language confusion: You were told verbally by a representative that the damage is likely not covered due to a maintenance exclusion, but the actual description of the event matches your sudden and accidental policy language perfectly.

- 👉 The pressure to close: Your insurer is actively pushing you to sign a settlement document or accept a direct deposit very quickly after a significant loss. (Note: This is different from a settlement that simply arrived efficiently. Look for signs of pressure, such as telling you the offer will expire, or discouraging you from getting your own estimates).

- 👉 The hidden discount loss: You just realized you have had a “claim-free discount” on your policy for years, and filing this marginal claim will strip that discount away, causing an immediate rate spike even before the official surcharge hits.

Bridging the Gap: Getting a Second Set of Eyes

The deductible math is easy. Anyone can subtract one number from another. But predicting whether the settlement will actually cover your real world repairs, and ensuring that the claim process goes correctly without jeopardizing your future coverage, is incredibly difficult for a homeowner going through it for the first time.

If you are looking at significant damage and are unsure if the payout will justify the long term cost, or if you have already filed and the insurer is lowballing the scope of work, you do not have to accept their initial framing. The adjuster works for the insurance company’s bottom line. You have the right to bring in an expert who works for yours.

Before you sign a release, cash a settlement check that seems too low, or even make that initial filing call for a complex loss, consider having a licensed professional review your scope before you commit. A free claim review can confirm if the offer matches the actual damage, or identify exactly what the insurance company left off their estimate. Whether you need a general scope review or an expert to evaluate a complex water damage claim, getting an independent assessment protects your financial interests.

Final Thoughts on the Filing Calculation

Your homeowner’s insurance policy is a safety net for catastrophic loss, not a maintenance contract. Treating it like a home warranty is the fastest way to price yourself out of the standard insurance market.

Run the real calculation: subtract your deductible and depreciation from the estimated repair cost, then subtract the three to five years of incoming surcharges and lost discounts. If that final net payout is not life-changing, you are usually better off handling the repair yourself. Protecting your CLUE report is just as important as protecting the physical structure of your house.

Explore More on Filing a Claim

To dive deeper into the specific variables of the filing decision, explore our detailed guides below.

| Topic | Summary |

|---|---|

| Will Homeowners Insurance Go Up After a Claim? The Rate Impact Explained | Deep dive into rate surcharge mechanics, duration, the loss of claim-free discounts, and how multiple claims compound your premium increases. |

| Home Insurance Claims History and the CLUE Report | Understand what the LexisNexis CLUE report is, how long entries stay, how zero-pay claims affect you, and how it impacts new policy shopping. |

| Home Insurance Claim Deductible: When to File and When to Absorb the Cost | Detailed breakdown of flat vs. percentage deductibles, wind/hail specifics, and how ACV depreciation reduces your net payout. |

| Home Insurance Claim Time Limit: How Long You Have to File | Explains the difference between policy deadlines and statute of limitations, and how insurers use weather records to date a loss. |

| Can You File a Home Insurance Claim After Repairs Are Done? | Guidance on filing after emergency repairs, what documentation is strictly required, and when post-repair recovery is possible. |

| Should I File a Home Insurance Claim for Water Damage? | Water claims have higher rate impacts and CLUE flagging. Learn the specific math for hidden water scope and settlement adequacy. |

| How to Document Home Damage for an Insurance Claim | Pre-filing documentation strategies, including what to photograph, written logs, and preserving evidence before the adjuster arrives. |

| Should I File a Home Insurance Claim for Roof Damage? | Roof-specific filing variables including the roofer incentive problem, ACV depreciation on aging shingles, and wind deductibles. |

| Emergency Home Repairs Before Your Insurance Claim | Learn your duty to mitigate, what emergency costs are reimbursable, and the critical danger of destroying evidence through over-repair. |

| How to File a Home Insurance Claim: Step-by-Step | The exact mechanics of the filing act: phone vs. portal, what to say (and what not to say) during the call, and proof of loss forms. |

| The Small Home Insurance Claim Math | Why filing for minor or cosmetic damage is the worst financial decision, calculating the break-even point against long-term surcharges. |

❓ FAQ

📞 Does calling my insurance agent to ask a question count as a claim?

In many cases, yes. Some insurers record a conversation about potential damage as an “inquiry” on your CLUE report, which can negatively impact your record even if no money is paid out. Always frame hypothetical questions carefully, or consult an independent professional first.

📈 How long will a claim affect my homeowners insurance premium?

Typically, a claim surcharge will affect your premium for three to five years. The exact duration depends on your insurance carrier’s internal guidelines and the state regulations where your property is located.

🚫 Can my insurance company drop me for filing one claim?

While a single claim usually results in a rate increase rather than a cancellation, insurers can non-renew your policy for a single large claim if you live in a highly volatile, high-risk market (like a severe wildfire or hurricane zone).

💸 Should I file a claim if the repair is just slightly over my deductible?

Usually, no. If your repair is $1,500 and your deductible is $1,000, your net payout is $500. The rate surcharges and loss of claim-free discounts over the next three to five years will almost certainly cost you far more than the $500 you received.

⏳ How long do I have to file a claim after damage occurs?

This timeline is set by your policy, not state law. Most standard policies require you to file within one to two years from the date of the loss. Check your specific policy declarations page to confirm your exact filing window.

🗂️ Are denied claims shown on my record?

Yes. A claim that is filed, investigated, and denied is recorded as a “zero-pay claim” on your CLUE report. It will stay on your record for five to seven years and can be viewed by future insurers.

🛑 Is it bad to file multiple claims for different things?

Yes. Filing multiple claims within a short window (typically three to five years) severely compounds your rate surcharges and significantly increases the risk that your carrier will refuse to renew your policy.

🔨 Can I do emergency repairs before the adjuster arrives?

You are actually required to perform emergency mitigation (like tarping a roof or extracting standing water) to prevent further damage. However, do not complete permanent repairs until the adjuster has documented the original damage.

📉 Does a water damage claim affect rates more than a wind claim?

Often, yes. Insurers view water claims very strictly because data indicates a property with one plumbing or water leak is highly likely to experience another. This usually results in higher surcharges and stricter underwriting.

❌ Can I cancel a claim if I realize the payout isn’t worth it?

You can withdraw a claim before a payout is issued, but the record of you filing it may still remain on your CLUE report as an inquiry or a zero-pay event. It is better to calculate the math before you make the initial call.

From filing to settlement: the parts worth understanding before something goes wrong.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

These cover the situations where professional help most often changes the outcome.

- 5 patterns that signal your settlement is probably short

- Who the adjuster at your door actually works for

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When a denial needs legal leverage, not just negotiation

- Four paths to fight a denial, including one most homeowners miss

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.