- Filing a small claim combines a low net payout with the full rate and record penalties of a major disaster claim.

- A minor payout can trigger a multi-year rate surcharge, often costing you more than the repair itself.

- Filing for damage that falls below your deductible results in zero payout but still places a claim inquiry on your CLUE record.

- Losing a “claim-free discount” creates an immediate premium spike even before standard surcharges are applied.

The Hidden Cost of the “Just to Be Safe” Claim

When you spot a minor water stain on the ceiling or a handful of cracked siding panels after a storm, the instinct is usually to call your insurance company immediately. After all, you pay your premiums every month for exactly this reason. But the math on a small home insurance claim almost never works in the homeowner’s favor. In fact, most homeowners only discover the true cost of a minor claim when their policy renewal arrives six months later.

In my experience writing and reviewing property claims, the question “should I file insurance claim for minor damage” is one of the most critical financial decisions you will make regarding your home. It is not just about whether the damage exceeds your deductible. It is about understanding the long-term arithmetic of premium surcharges, lost discounts, and your insurability for the next half-decade.

I frequently see homeowners who filed a claim for a $1,500 repair, received a $500 check after their deductible, and then spent the next three years paying an extra $800 annually in premium surcharges. They essentially paid the insurance company for the privilege of fixing their own house.

The goal is to protect your property without falling into a financial trap. To do that, we need to look past the repair estimate and break down exactly how insurers penalize small claims, why cosmetic damage is a dangerous trigger, and how to calculate your true break-even point before you ever pick up the phone to file.

Why Small Claims Are Uniquely Bad Financial Moves

To understand why filing for minor damage is risky, you have to look at how insurance carriers treat claims data. To an insurer, a claim is a claim. Whether your house burned to the ground or you had a minor pipe leak under the kitchen sink, the administrative process and the statistical risk marker placed on your file are largely the same.

Because of this uniform penalty system, the financial logic shifts drastically for minor repairs. A small claim combines a very small net payout (your repair cost minus your deductible) with the full rate and record consequences of a filed claim. The surcharge applied to your premium persists for a set period, typically three to five years, regardless of how small the claim check was.

The Break-Even Calculation

Let us look at a standard scenario I see often in standard policies. You have minor wind damage to your roof. The repair estimate from a local contractor is $2,000. Your policy carries a flat $1,000 deductible. You decide to file the claim.

| The Minor Claim Scenario | Financial Impact |

|---|---|

| Total Repair Cost | $2,000 |

| Your Deductible | -$1,000 |

| Net Claim Payout to You | $1,000 |

| Estimated Annual Premium Surcharge (e.g., $300/year) | $300 |

| Surcharge Duration (Typically 3 Years) | x 3 Years |

| Total Cost of Surcharge Over Time | $900 |

In this illustrative scenario, you gained $1,000 today but will pay back $900 over the penalty period. Your net benefit for going through the hassle of adjusting, documenting, and filing the claim is only $100. If that surcharge extends longer, or if the annual rate increase is higher than estimated, you are actually losing money over the life of the policy.

⚠️ Warning: These figures are illustrative and vary heavily by state and insurer. However, the mechanism remains the same. The smaller the payout, the more likely the multi-year surcharge will consume or exceed the benefit of filing.

The Claim-Free Discount Problem

There is a secondary, often hidden penalty when filing for a small amount of damage. Many homeowners have a “claim-free discount” automatically applied to their premium. Because insurance policies are notoriously dense, most people never realize this discount is active until it disappears.

Filing a single claim, no matter how small, typically strips this discount from your policy at the next renewal. This creates a compounding rate shock. You are not just getting hit with a post-claim surcharge; you are also losing a discount you have relied on for years. Let us look at how this double penalty plays out on a typical premium bill:

Base Premium: $1,500

Claim-Free Discount (10%): Saves $150

Current Bill: $1,350After a minor claim:

Discount Removed: Bill goes back to $1,500

Claim Surcharge Added (15%): Adds $225

New Bill: $1,725 (A sudden $375 annual increase for a minor payout)

This combined effect is the actual cost of filing. When you are doing the math on whether to absorb a $1,200 plumbing repair out of pocket, you must calculate both the potential surcharge and the loss of any existing discounts. If you do not know if you have a claim-free discount, check your declarations page or ask your agent before filing.

The Cosmetic Damage Trap

Cosmetic damage is the gray area that traps many well-meaning homeowners. We are talking about surface staining on a ceiling after a minor leak that has been fully fixed, small dents in aluminum siding from a brief hail flurry, or scratched flooring from a dropped object. The structure is sound, there is no ongoing risk, but it does not look perfect.

Filing a claim for cosmetic damage is rarely the right financial decision. Insurers view cosmetic damage with heavy scrutiny because it does not affect the home’s ability to shed water or remain structurally sound. Adjusters are trained to price these purely on aesthetics, which means estimating for sanding, sealing, or spot-painting rather than full replacement.

Furthermore, many modern policies now carry specific “Cosmetic Damage Exclusions” (especially for hail on roofs or metal surfaces), giving the insurer the explicit right to deny the payout entirely while still logging the claim inquiry on your record. Even if it is covered, the payout is usually minimal and heavily depreciated.

Key Point: Most cosmetic damage is better absorbed as a general home maintenance cost. Trading a permanent blemish on your insurance record for a few hundred dollars to paint a ceiling is a poor exchange.

Filing a claim immediately because a localized hail storm left a few shallow dents on your garage door, assuming insurance will buy you a brand new door.

Getting a contractor to estimate the repair cost first, realizing the $600 fix is well under your $1,000 deductible, and paying out of pocket to protect your claims history.

The Below-Deductible Disaster

The absolute worst scenario in the claims process is filing a claim for damage that falls below your deductible. This produces zero payout from the insurance company, but it still triggers all the negative consequences.

When you call your insurer and formally report damage, an inquiry or a “zero-pay claim” is generated on your CLUE (Comprehensive Loss Underwriting Exchange) report. This database tracks your claims history for five to seven years. Even if the insurer did not pay you a dime, the record shows that a damage event occurred at your property.

If you have a zero-pay claim on your record and then suffer a legitimate, major loss a year later, you are now filing your second claim in a short window. Insurers look very harshly at multiple claims within a tight period. That second claim, compounded with the first minor one, can push you over the threshold into non-renewal, forcing you to seek coverage in high-risk, high-cost markets.

The operational formula to remember here is simple: assess the damage privately first, calculate your true net payout above the deductible, and only file if that final number makes financial sense. You should never file for damage below your deductible. It is an all-risk, no-reward action.

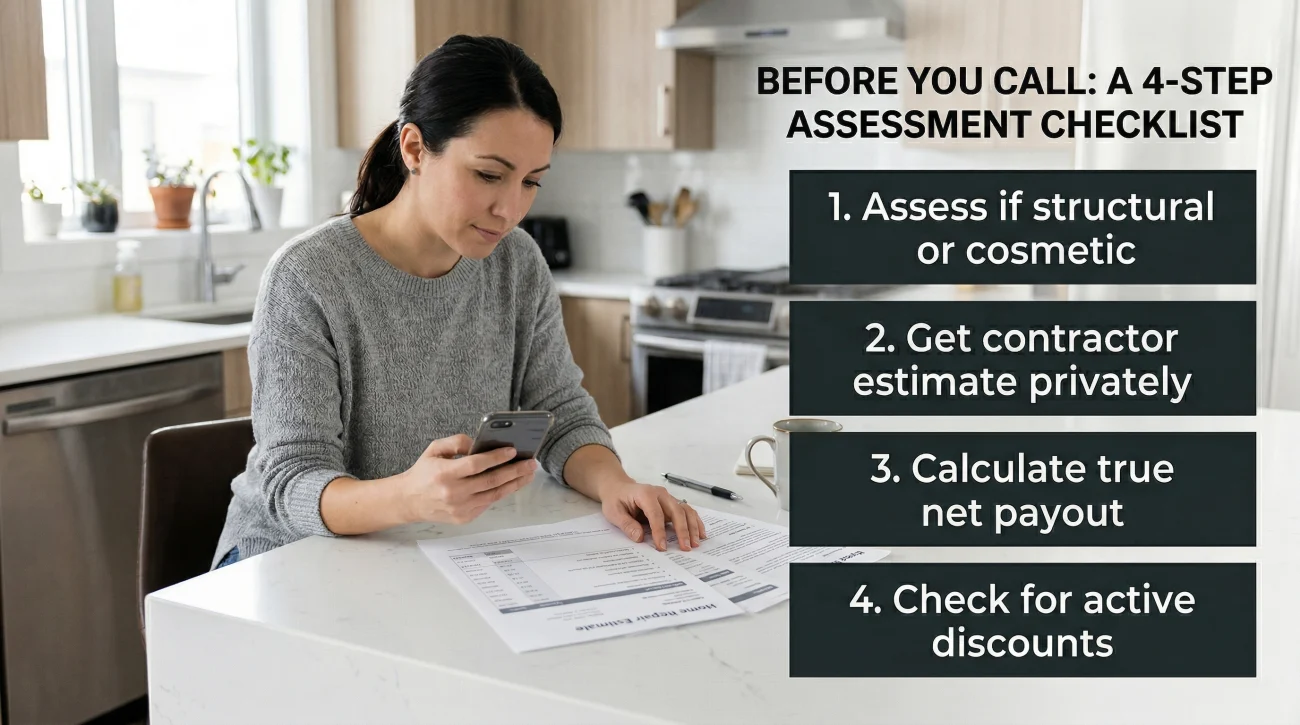

Before You Call: A 4-Step Assessment Checklist

To avoid falling into these traps, you need a clear decision flow before you pick up the phone to alert your insurance carrier. I always recommend homeowners take these four steps before opening a claim for something that appears minor:

- 1. Assess if it is structural or cosmetic: Look objectively at the damage. Does it compromise the integrity of the home, or is it just an eyesore? If it is purely cosmetic, lean heavily toward not filing.

- 2. Get a contractor estimate privately: Do not use the insurance adjuster to figure out how much the repair costs. Have a trusted local contractor inspect the damage and give you a written estimate first.

- 3. Calculate your true net payout: Take the contractor’s estimate and subtract your exact home insurance claim deductible. If your roof was damaged, make sure you are calculating the specific wind and hail percentage deductible, which is often much higher than your standard deductible.

- 4. Check your declarations page for active discounts: Review your policy declarations page to see if you have a “claim-free discount” that you will lose upon filing. Factor that lost savings into your break-even math.

When Filing a Small Claim Might Actually Make Sense

While the general rule is to avoid filing for minor issues, there are specific operational scenarios where taking the hit on your record is necessary to prevent a much larger disaster. Claims are rarely black and white, and context matters.

Here are the two scenarios where a seemingly small claim might be worth pursuing:

The damage will worsen significantly if left unrepaired

If a minor roof penetration is allowing small amounts of water into your attic, and you cannot afford the $2,500 repair out of pocket, filing the claim is necessary. Leaving it untreated will inevitably lead to rot, mold, and interior ceiling collapse. Preventing a $30,000 future claim justifies taking the immediate hit on your record today.

Hidden water damage is suspected

Water damage is notorious for being more extensive than it appears. A small puddle near a baseboard might just be a spill, or it might be a symptom of a failed supply line spraying inside the wall cavity for a week. If professional mitigation is required to open walls, run commercial dehumidifiers, and replace insulation, the cost will quickly escalate beyond a “minor” repair. What looks like a $500 fix on the surface can easily become a $5,000 mitigation project.

💡 Pro Tip: If you suspect water damage is larger than what is visible on the surface, hire a mitigation company or a plumber to provide a written assessment and moisture reading before you decide not to file based on surface appearances.

Signs a Small Claim is the Wrong Financial Decision

It is easy to panic when your home is damaged. However, treating your insurance policy like a maintenance contract for minor wear and tear will ultimately cost you. If you are sitting on the fence about whether to call your carrier, pause and look for these specific red flags.

The math is likely against you if:

- Your estimated net payout is under $1,000. After the deductible is applied, any check smaller than this is rarely worth the long-term premium penalties.

- The damage is purely cosmetic. An insurer will not pay handsomely for aesthetic blemishes like surface dents or paint scratches, but they will still penalize your claims history for reporting them.

- You have filed another claim recently. Compounding claims are the fastest route to a policy non-renewal. You must protect your standing with your carrier for truly catastrophic events.

- You are planning to switch insurers or sell the property within two years. A fresh entry on your insurance claims history report for a minor issue will make finding competitive new coverage difficult, and it can raise unnecessary red flags for potential home buyers.

Final Thoughts on the Filing Threshold

Navigating these red flags requires stepping back and looking at the situation from the insurer’s perspective. Most small claim decisions become remarkably clear once the surcharge math is done on paper. The deductible is only the entry fee, the rate impact is the true cost. Understanding how to weigh the immediate payout against your long-term record is the key to managing your policy effectively. For a deeper understanding of how these factors work together, I highly recommend reviewing the full filing decision framework to see the complete picture.

However, the biggest risk in deciding not to file is underestimating the actual scope of the damage. What looks like an $800 minor ceiling repair to a homeowner might actually involve thousands of dollars of unseen structural drying and insulation replacement. If your damage is larger than it initially appeared, or if you are unsure whether you are looking at cosmetic issues versus structural failure, an independent scope assessment can tell you the real number before you make a binding decision.

❓ FAQ

🧐 Is it worth filing a home insurance claim for small damage?

Usually, no. Once you factor in your deductible, the potential loss of a claim-free discount, and rate surcharges that last three to five years, a small claim often costs you more in premium increases than the insurer pays out.

💸 Should I file a home insurance claim for $500 damage?

No. Standard deductibles typically start at $500 or $1,000. If the total damage is only $500, you will likely receive zero dollars from the insurer, but the claim inquiry will still go on your permanent CLUE record.

📉 Do I lose my claim-free discount if I file for a minor repair?

In most cases, yes. Filing any claim, regardless of the payout size, usually triggers the removal of your claim-free discount at your next policy renewal, leading to an immediate rate increase.

📝 What happens if I file a claim that is less than my deductible?

The insurer will close the claim without issuing a payment. However, it will be recorded as a “zero-pay claim” on your history, which can still be used against you if you file another claim or attempt to switch carriers.

🏠 Should I use my insurance for minor roof damage?

You should calculate your specific wind/hail deductible first. Many policies have a percentage deductible for roofs that is much higher than standard deductibles. If the net payout is minimal, paying out of pocket is safer for your record.

💧 Is it smart to file a claim for minor water damage?

It depends on whether the damage is truly minor. Water damage often hides behind walls. If a professional confirms it is localized and cheap to fix, pay out of pocket. If hidden structural drying is needed, filing is usually necessary.

🎨 Should I file a home insurance claim for cosmetic damage?

Generally, no. Insurers pay very little for aesthetic issues like surface stains or minor dents. Taking a rate surcharge for damage that does not threaten the structure of your home is a poor financial trade.

⏱️ How long does a small claim stay on my insurance record?

Claims, including minor or zero-pay claims, typically remain on your CLUE (Comprehensive Loss Underwriting Exchange) report for five to seven years, following you even if you switch insurance companies.

🤔 Do temporary repairs affect my small insurance claim?

Emergency temporary repairs (like tarping a leak) are required to mitigate damage and usually will not hurt your claim if documented properly. However, doing permanent repairs before an adjuster visits can complicate coverage.

📞 Does calling my insurance company to ask about small damage count as a claim?

It can. Many insurers record calls discussing specific damage events as “inquiries” on your CLUE report, which can act as a negative mark even if you ultimately decide not to officially file.

Filing is just the beginning. These cover what the rest of it looks like.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

That gap is common and usually closeable. These explain how.

- 5 patterns that signal your settlement is probably short

- Who the adjuster at your door actually works for

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When a denial needs legal leverage, not just negotiation

- Four paths to fight a denial, including one most homeowners miss

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.