- A single home insurance claim typically raises your premium by 9% to 40%, and this surcharge usually lasts for three to five years.

- Filing a claim often removes a “claim-free discount” you may not have realized you had, creating a double financial hit at your next renewal.

- Filing multiple claims within a short window drastically increases your risk of non-renewal, which can force you into the expensive non-standard insurance market.

- The math on small, cosmetic claims rarely works in your favor when you calculate the long-term rate impact against the immediate payout.

The Calculation Most Homeowners Skip

When your home is damaged, the immediate instinct is to call your insurance company. You pay your premiums every month for exactly this reason. But in my years reviewing claims and sitting across from adjusters, I have seen a recurring pattern that ends up costing policyholders thousands of dollars. Homeowners focus entirely on their deductible, asking themselves only one question: is the damage more than my deductible amount?

That is the wrong starting point. A claim that raises your premium for three to five years can easily cost you more in the long run than the claim ever paid out. The rate impact is the calculation most homeowners skip, and it is the one that most often determines whether filing the claim was actually a smart financial move.

Let us walk through exactly how insurers adjust your rates after a claim. We will look at the mechanics of surcharges, the hidden cost of losing your claim-free discount, and how to do the actual math before making that phone call to file.

How Surcharges Actually Work

When you file a claim and your insurer pays out on it, you become statistically more likely to file another claim in the future. To offset this increased risk, insurers apply a surcharge to your policy. But this does not happen immediately the day you receive your settlement check. It happens at your next policy renewal.

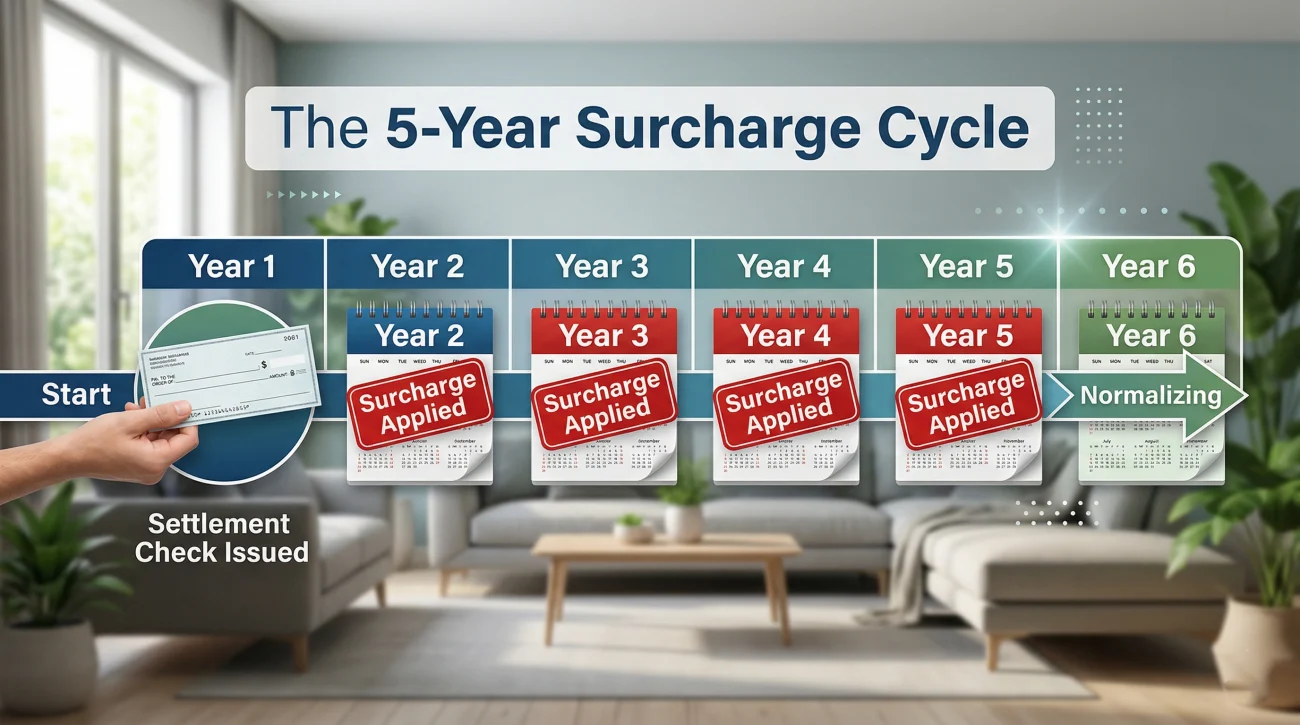

Most insurers apply a surcharge percentage to your base premium. This surcharge does not last forever, but it stays attached to your policy for a defined period, which is typically three to five years. During that entire window, every single time your policy renews, it includes that higher rate.

Short field observation from claims experience: I frequently speak with homeowners who are shocked by their renewal bill a full ten months after their claim was closed. They thought the settlement was the end of the transaction. In reality, the settlement is just the beginning of a multi-year rate adjustment.

It is important to understand that the surcharge period rolls off eventually. If you stay claim-free for the duration of that specific timeline, your base rate will typically normalize. However, until that window closes, you are paying a premium penalty.

How Much Will Homeowners Insurance Go Up After a Claim?

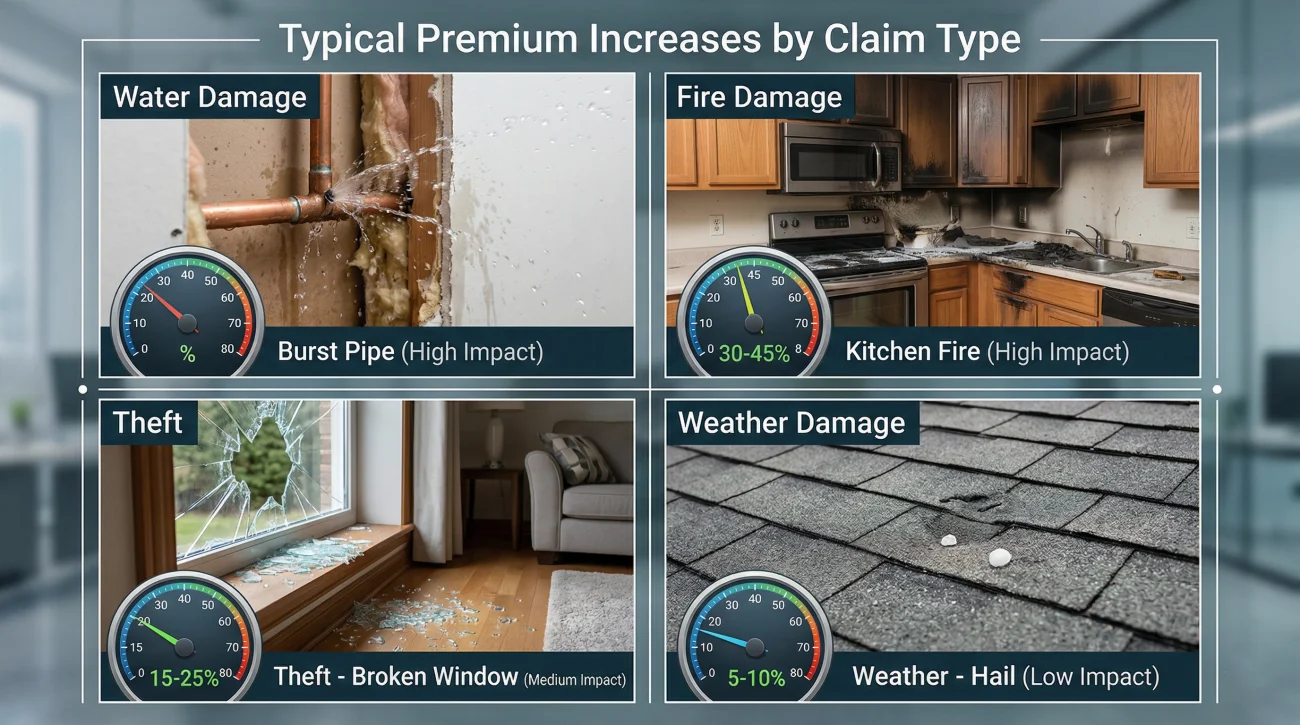

This is the most common question I get, and while I cannot give you an exact dollar figure because it varies heavily by state and carrier, I can tell you the typical ranges. A single claim typically increases premiums by 9% to 40%. Where you fall in that wide range depends heavily on the type of claim you file, the size of the payout, your location, and your specific insurance company.

Not all claims are treated equally by underwriting algorithms. Claims that indicate a high likelihood of future issues or ongoing maintenance problems are penalized the most.

| Claim Type | Typical Rate Impact | Why Insurers Penalize It |

|---|---|---|

| Water Damage (Non-Weather) | High (20% to 40%) | Often indicates aging plumbing or maintenance issues, highly likely to recur. |

| Fire Damage | High (20% to 40%) | Extremely high severity risk, even if the first fire was small. |

| Theft or Vandalism | Medium (15% to 25%) | Indicates a location vulnerability, though less severe than fire or water. |

| Wind or Hail (Weather) | Low to Medium (0% to 15%) | Considered an “Act of God” outside your control, but frequent claims still raise rates. |

Water damage and fire claims tend to produce the highest rate increases. If a pipe bursts under your sink, the insurer worries about the pipes under your floors. Conversely, weather events like wind or hail are often treated slightly more leniently because they are outside of your control. However, if your entire zip code is reclassified as high-risk following a major storm, your base rate may increase regardless.

Let us look at a realistic calculation. Suppose your annual premium is $2,000. You file a water damage claim that results in a $10,000 payout. If your insurer applies a 20% surcharge, your premium jumps to $2,400. That extra $400 a year, multiplied by a five-year surcharge period, means you are paying $2,000 back to the insurer in increased premiums. Your $10,000 payout suddenly feels much smaller.

Assuming a $3,000 claim payout is a clear financial win just because your deductible is only $1,000.

Calculating how much a 20% premium increase will cost you over the next five years, and subtracting that from your net payout.

The Hidden Cost: Losing Your Claim-Free Discount

The surcharge is only half of the math problem. The other half is a hidden cost that catches almost everyone off guard: the loss of the claim-free discount. Many homeowners have a discount applied to their premium without realizing it, simply because they have not filed a claim in a long time.

Insurers heavily incentivize claim-free behavior. If you have gone five, ten, or fifteen years without filing a claim, your current premium likely includes a discount ranging from 5% to 20%. Filing just one claim removes that discount at your next renewal. This produces a rate increase even before the actual claim surcharge is applied.

📌 Note: The two effects together can add up to a significant first-year premium shock. This double hit (losing the credit while adding the penalty) is the actual cost of filing.

If you are unsure whether you have this discount, you need to check your declarations page or ask your agent. However, you must be careful how you ask. You do not want to trigger an inquiry on your record just by asking a hypothetical question.

Safe Script for Checking Discounts:

Hello [Agent Name],

I am doing a routine annual review of my household finances and looking over my insurance policy. Could you please send me a breakdown of all the current discounts applied to my policy? I specifically want to know if I am receiving a claim-free discount and what percentage it represents on my current premium.

Thank you.

The Non-Renewal Threshold: When Insurers Drop You

There is a scenario worse than a rate increase, and it is becoming increasingly common in high-risk markets. There is a threshold above which insurers simply decline to renew your policy rather than raising your rates. This is known as a non-renewal.

In my experience reviewing claim files, homeowners are often blindsided by a non-renewal notice. They assume paying higher rates is the worst-case scenario. But this threshold is very real. It varies significantly by insurer and state, but it is typically triggered by filing multiple claims in a short window, such as two claims within three years. It can also be triggered by a single very large claim in a market that the insurer is trying to exit.

A non-renewal is a serious problem because it forces you into the open market with a fresh, negative claims history. Standard carriers often decline applicants who have been recently dropped for claims frequency. This forces the homeowner into the non-standard market, or state-backed FAIR plans, where coverage is often much thinner and rates are significantly higher than anything in the standard market.

Do You Have Claim Forgiveness?

Before you panic about rate increases, you should check your policy for a specific feature: claim forgiveness. Much like auto insurance, some homeowners policies offer a program where your first claim does not trigger a surcharge.

You can usually find this by checking your declarations page for terms like “first claim waiver”, “accident forgiveness”, or “claim-free reward”. This is typically offered to long-term customers who have been with the carrier for several years with no prior claims. If your policy has this feature, the math of filing a claim changes dramatically because the surcharge penalty is waived.

However, you must read the fine print. Claim forgiveness usually waives the surcharge, but it might not protect your claim-free discount. Furthermore, even if the carrier forgives the claim internally, that claim still goes on your permanent record, which brings us to another critical variable.

Key Point: Claim forgiveness only applies as long as you stay with your current insurer. If you decide to shop around for a new policy, the new insurers will still see the claim on your record and will quote you accordingly.

The Connection to Your Claims Record

Surcharges are what your current insurer charges you, but how does a new insurer know about your past? The answer is a database called the Comprehensive Loss Underwriting Exchange (CLUE). Every time you file a claim, it gets recorded here.

Here is a critical operational reality that catches many homeowners off guard: simply calling your insurer to ask if a hypothetical scenario is covered can generate an “inquiry” on your CLUE report, even if no money is paid out. Some carriers treat these inquiries similarly to zero-payout claims.

The rate surcharge is a separate mechanism from this database record, but both matter immensely. If you are planning to sell your home or switch insurance carriers in the next few years, understanding what goes into this database is vital. For a deep dive into how inquiries work and how they affect your insurability, you should review our guide on how long entries stay on your CLUE record.

Detecting an Active Surcharge When Shopping

If you are buying a new home or switching carriers, you need to know how to read your new quotes to see if a past claim is currently penalizing you. An active surcharge does not always have a bright red warning label.

Look for line items labeled “claims surcharge”, “loss history debit”, or simply compare the base rate to the final premium. If you are inheriting a claim history from a prior owner of the property, you might be paying a surcharge for damage you did not even experience. Always ask the new agent explicitly if a past claim is currently elevating the quoted premium.

The Compounding Financial Penalty of Multiple Claims

If you take away nothing else from this guide, remember this rule: the second claim is always judged much more harshly than the first. I always warn clients about this reality. If you file a second claim during that same active surcharge window, the new surcharge does not just add to the old one; it compounds.

Let us say you had a minor roof leak two years ago and filed a claim. Now, you have a small pipe leak under your sink. If this was your first claim, you might consider filing it. But because it is your second claim in a short timeframe, the math is entirely different. The financial penalty multiplies aggressively.

The surcharge applied for a second claim is often exponentially higher than the first.

Signs the Rate Impact Changes Your Filing Calculation

The decision to file a claim is rarely a simple “yes” or “no.” It requires looking at the numbers and your specific situation. Here are the clear signs that the rate impact should make you pause and recalculate before you file:

- 🛑 The damage is close to your deductible: If the repair is $2,500 and your deductible is $1,500, the $1,000 payout will easily be eclipsed by the surcharge over the next few years. You also need to verify exactly how your specific deductible works, as percentage deductibles can be deceiving. You can learn more about how your specific home insurance claim deductible is calculated before doing the math.

- 🛑 This would be your second claim: If you have filed any claim recently, the compounding surcharge makes filing a small or moderate claim highly risky financially.

- 🛑 You are in a high-risk market: If you live in an area prone to wildfires, hurricanes, or severe hail, insurers are already looking for reasons to reduce their exposure.

- 🛑 You have an unchecked claim-free discount: If you have been with your carrier for a decade without a claim, your current low rate is likely heavily dependent on a discount that will vanish the moment you file.

The Break-Even Math: Visualizing the True Cost

To make the right choice, you need to map out the break-even point over a standard renewal cycle. Here is a simplified look at how the net payout compares to the long-term cost.

| Estimated Repair | Net Payout (After Deductible) | Estimated 5-Year Surcharge Cost | Financial Outcome |

|---|---|---|---|

| $2,500 | $1,500 | $2,000 | Net Loss (-$500). Do not file. |

| $6,000 | $5,000 | $2,500 | Marginal Win (+$2,500). Consider carefully. |

| $25,000 | $24,000 | $3,500 | Clear Win (+$20,500). File the claim. |

Note: This is an illustrative example assuming a $2,000 annual base premium and a flat $1,000 deductible. Your actual numbers will differ based on your specific surcharge rates, but the formula remains the same.

If your damage involves complex structural issues like a destroyed roof from a severe storm, you want to make sure your repair estimate is perfectly accurate before you commit to the multi-year surcharge. In those cases, consulting a public adjuster for roof damage can help ensure the initial estimate actually covers your real recovery costs.

Making the Final Financial Call

Calculating the true cost of a claim requires gathering specific pieces of data. You need to know your current premium, your likely surcharge range for the specific type of damage you have, whether you are risking a claim-free discount, and how many years remain on any prior surcharge.

Once you have those numbers, you can estimate the long-term cost of filing. You then compare that hidden cost against your expected net payout, which is your total repair cost minus your deductible.

This math is just one pillar of the decision. To see how rate impact fits into your overall filing decision, you need to weigh it alongside the deductible math, your database record, and the adequacy of the settlement you are likely to receive.

But what happens if you have already filed the claim, taken the hit to your record, and the settlement offer comes back drastically lower than your contractor’s repair estimate? This is the worst-case scenario. You are suffering the rate increase without getting the funds to fix your home.

If you have already filed and the settlement does not cover your actual repair costs, the net calculation changes entirely. You have already paid the penalty, so you need to ensure you receive the correct payout based on your policy. If the insurer’s estimate is missing significant line items, getting a free claim review from a licensed public adjuster is the most practical next step to determine if the gap is worth fighting for.

Final Thoughts on Premium Increases

When you strip away the emotion of property damage, a home insurance claim is ultimately a financial transaction. The deductible is only the entry fee. The real cost is paid over the next several renewal cycles.

Never file a claim blindly. Always assume that your rates will go up, and do the rough math to project that cost over three to five years. If the net payout from the insurance company is smaller than the projected premium increase, the smartest financial move is usually to pay for the repairs out of pocket and keep your clean record intact.

❓ FAQ

📈 Does homeowners insurance go up after a claim?

Typically, yes. Filing a paid claim usually results in a surcharge added to your base premium at your next policy renewal. The exact amount varies by state, insurer, and the type of claim filed.

🕒 How long does a claim affect homeowners insurance rates?

A claim surcharge typically stays on your policy for a period of three to five years. If you remain claim-free during this window, the surcharge usually rolls off and your rates normalize.

💸 How much does homeowners insurance go up after a claim typically?

A single claim generally increases premiums by 9% to 40%. The increase depends heavily on the cause of loss, with water and fire claims usually producing higher surcharges than wind or hail claims.

🛡️ What is a claim-free discount on homeowners insurance?

It is a premium reduction applied by insurers to reward policyholders who have not filed claims for a certain number of years. Filing a single claim removes this discount, causing a rate increase even before a surcharge is applied.

❌ How many claims before insurance drops you?

There is no universal number, but filing two claims within a three to five year window is a common threshold for non-renewal. In high-risk markets, a single very large claim can sometimes trigger a non-renewal.

💧 Will a water damage claim raise my premium more than wind?

In many cases, yes. Water damage (non-weather) often indicates ongoing maintenance or plumbing issues, making it a higher statistical risk for future claims compared to weather events like wind or hail.

🌪️ Does a weather-related claim raise my rates?

It can, though weather claims are generally treated more leniently than maintenance-related claims. Insurers may also raise base rates for your zip code following a large regional storm event.

📉 Can I avoid a rate increase if I pay out of pocket?

Yes. If you pay for the repairs entirely out of pocket and never report the damage or file a claim with your insurer, there is no claim record generated and therefore no resulting rate surcharge.

🚫 Will a denied claim still raise my premium?

It depends on the insurer and state laws. A denied claim usually does not trigger a direct payout surcharge, but the simple act of filing can sometimes remove your claim-free discount or affect your overall risk profile.

🔄 Do homeowners insurance rates go down after the surcharge period ends?

Typically, the specific surcharge tied to that claim will drop off after the three to five year period. However, your overall premium may still reflect general inflation and statewide rate adjustments implemented during that time.

Filing is just the beginning. These cover what the rest of it looks like.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

That gap is common and usually closeable. These explain how.

- 5 patterns that signal your settlement is probably short

- Who the adjuster at your door actually works for

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When a denial needs legal leverage, not just negotiation

- Four paths to fight a denial, including one most homeowners miss

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.