- Filing a claim after repairs are completed is possible if your policy filing window is still open.

- Emergency repairs to prevent further damage are expected, but destroying evidence before an adjuster visits can complicate your settlement.

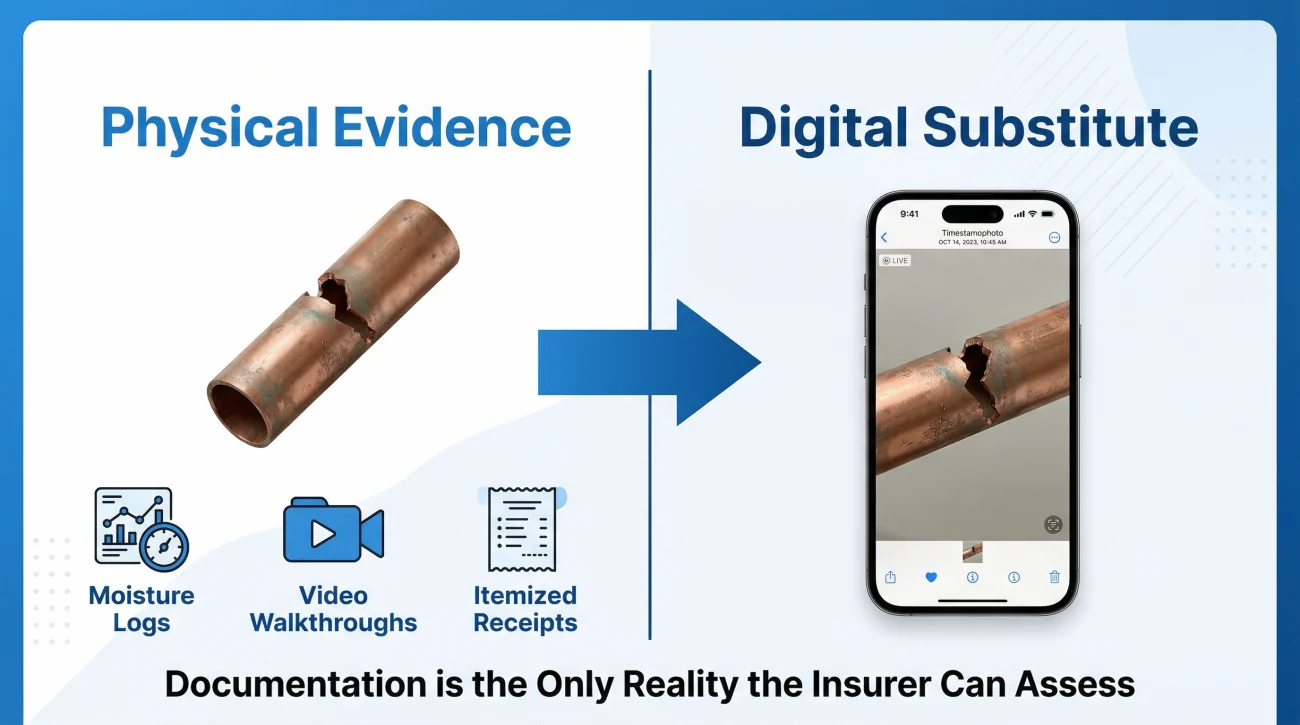

- Without physical damage to inspect, your claim relies entirely on the quality of your pre-repair documentation and contractor records.

- A detailed written assessment from your contractor is often the deciding factor when physical evidence is gone.

The Post-Repair Panic: Is It Too Late to Get Reimbursed?

You had damage, you panicked, and you fixed it. Maybe a pipe burst in the middle of the night and you called an emergency plumber. Maybe a storm blew off a section of your roof and you paid a roofer out of pocket to tarp it and replace the shingles before the next rain. Now that the dust has settled and the contractor’s bill is sitting on your kitchen table, you are probably asking yourself a very stressful question.

Can you still file a home insurance claim after the repairs are done?

I hear this question constantly. Homeowners often believe that the moment a hammer swings or a wet vac is turned on, they have voided their insurance policy. They assume that because they did not wait for an adjuster to arrive with a clipboard, the insurance company will automatically stamp “denied” on their file.

The answer is not an automatic no. In many cases, you can still file. However, the success of a post-repair claim depends entirely on a few specific variables, mostly surrounding how well you documented the disaster before you cleaned it up. When the physical evidence is gone, your documentation becomes the only reality the insurance company can assess.

The Key Question: Is Your Claim Filing Window Still Open?

Before we look at receipts and photographs, we have to look at the calendar. The absolute first hurdle in a post-repair claim is the deadline set by your insurance policy.

If the damage occurred within your policy’s claim filing period, you generally still have the right to file even if the repairs are complete. This window is typically one to two years from the date of the loss, though you must check your specific policy documents to confirm your exact timeframe. The deadline clock runs from the date the damage occurred, not the date you finished the repair, and certainly not the date you decided to call the insurer.

I frequently review cases where a homeowner fixed a ceiling leak out of pocket, only to find extensive mold six months later. Because they were still within their one-year filing window from the original storm date, we could still initiate the claim. The delay made it harder to prove, but the door was not legally closed.

If you are past that deadline, the quality of your repair documentation will not matter. The insurer will typically issue a denial based purely on late reporting. If you are unsure how these timelines interact with state regulations, understanding the exact timeline for filing home insurance claims is the best place to start your research.

Emergency Repairs Are Expected (And Often Required)

One of the biggest misconceptions in the property claims world is that you must leave your house actively flooding or your roof actively leaking until the adjuster arrives. This is completely false.

Most policies explicitly allow, and actually require, you to make temporary emergency repairs to prevent further damage after a covered loss. This is known in the industry as your “duty to mitigate.” If a tree falls through your living room during a storm, you are expected to board up the window and tarp the roof. If a pipe bursts, you are expected to shut off the main water valve and extract the standing water.

Performing these emergency actions does not forfeit your claim rights. In fact, failing to do them can give the insurer grounds to deny portions of your claim, arguing that the secondary damage (like mold growth or ruined hardwood) was your fault for failing to mitigate the initial problem.

Leaving standing water on your hardwood floors for four days because you are terrified that cleaning it up will void your insurance coverage.

Taking 50 photos of the standing water, recording a video of the active leak, and then immediately calling an extraction crew to pull the water out and set up drying fans.

The problem arises when homeowners cross the line from emergency mitigation into permanent reconstruction before the adjuster has a chance to inspect. Tarping a roof is mitigation. Tearing off the entire roof deck and installing brand new architectural shingles is permanent reconstruction. If you have crossed into permanent repairs, your claim relies heavily on what you preserved on paper or on camera. If the incident involved fire or severe smoke, and you already tore out the drywall, engaging a public adjuster specializing in fire damage can help you navigate how to retroactively prove the severity of soot penetration.

The Documentation Problem: Inspecting What No Longer Exists

When you file a claim before repairs happen, the insurance company sends an adjuster to evaluate the scene. They measure the moisture in the walls, take wide-angle photos of the collapsed ceiling, and inspect the cracked pipe to determine the cause of loss.

When you file after repairs are complete, the physical evidence of the original damage is completely gone. You cannot expect an adjuster to approve a $15,000 payout based on a beautifully painted, brand-new ceiling and your verbal assurance that “it looked really bad last week.” The burden of proof shifts entirely to you.

| Physical Evidence (Pre-Repair) | Documentation Substitute (Post-Repair) |

|---|---|

| Water stains and active dripping on drywall | Timestamped video of the active leak occurring |

| The split angle stop valve under the sink | The actual broken valve kept in a plastic bag |

| Saturated hardwood floors lifting at the edges | Moisture readings logged by the mitigation company |

| Hail dents on the aluminum siding | Close-up photos with a tape measure showing dent size |

What you have instead of an active loss site is whatever documentation you created before or during the repair. The quality, depth, and clarity of this documentation will absolutely dictate whether your claim is approved or denied.

What Documentation Actually Supports a Post-Repair Claim

If you are piecing together a file to submit after the contractor has already left, you need specific types of evidence. A simple credit card receipt showing you paid a plumber $2,500 will not work. The insurer needs to know the cause of loss, the extent of the damage, and the justification for the cost.

Dated Photographs and Video Walkthroughs

This is your strongest substitute for a physical inspection. You need photos taken before the repairs began, and ideally, photos taken during the demolition phase. The metadata on digital photos provides the date and time, which helps establish the timeline of the sudden event.

💡 Pro Tip: Always include wide establishing shots. Close-up photos of a broken pipe are great, but the adjuster needs to see the pipe in relation to the rest of the room to understand the full scope of the resulting water spread.

Contractor Estimates and Detailed Invoices

An invoice that simply says “Fixed leak in bathroom – $1,200” is virtually useless for a post-repair claim. It does not state the cause, the materials used, or the scope of the collateral damage.

You need an itemized breakdown. If your contractor is still willing to help, ask them to provide a detailed, retroactive statement of their findings. They need to describe the damage condition they observed upon arrival.

Hello [Contractor Name],

Thank you for the emergency repair work you completed on [Date]. I am currently preparing to file an insurance claim for the incident. Because the physical damage has been repaired, my insurer requires a written statement from the professional who observed the original condition.

Could you please provide a brief written assessment on your company letterhead that includes:

1. What you observed when you first arrived on site.

2. Your professional opinion on the cause of the failure (e.g., sudden pipe burst vs long-term slow leak).

3. The specific materials that were damaged and required removal.

This will help immensely in getting the scope approved. Thank you for your help.

Emergency Service Logs

If the fire department responded to a small kitchen fire, their incident report is exceptional third-party documentation. If a water mitigation company set up drying fans, their daily moisture reading logs prove exactly how wet the structure was before it was restored.

When Post-Repair Filing is Unlikely to Succeed

I always prefer to give homeowners a realistic outlook. There are several scenarios where filing a claim after the fact is almost certainly going to end in frustration and a denial letter.

First, if no documentation of the pre-repair condition exists. If you cleaned up the water, threw away the damaged baseboards, painted the walls, and took exactly zero photos, the insurer has nothing to verify. They cannot cover an invisible loss.

Second, if the repairs were purely cosmetic and the original damage cannot be proven as a covered peril. For example, if you repainted a ceiling because of an ugly stain, but you cannot prove whether the stain came from a sudden, covered roof leak last month or a slow, uncovered condensation issue over the last ten years, the claim will struggle.

📌 Note: Throwing away the physical source of the failure is a common misstep. If a braided supply line to your toilet bursts, you must keep that broken hose. Discarding the failed component prevents the insurer from verifying whether the failure was sudden or due to long-term wear.

No Photos, No Contractor Records: Is There Any Path Forward?

If you threw away the broken pipe, took zero photos, and the emergency plumber has stopped returning your calls, you are in the worst-case scenario. However, before entirely giving up, look for alternative evidence. Did you text your spouse a photo of the flooded floor when it happened? Do you have a timestamped receipt from Home Depot for the emergency tarp? Can weather service records prove a severe hail storm hit your exact address on the date you claim?

These are not guarantees, but an experienced public adjuster can sometimes build a circumstantial case out of text logs, credit card timestamps, and weather data. What if your contractor refuses to write a formal retroactive assessment? Even a screenshot of their casual text message explaining what they found is better than arriving empty-handed.

When Post-Repair Filing is Worth Pursuing

That being said, there are plenty of scenarios where you should absolutely move forward with filing, even if the hammer has already been put away. Insurers generally prefer that you mitigated the loss rather than letting the house rot while waiting for their phone call.

A good rule of thumb for pursuing a delayed file involves this formula:

[Sudden verifiable event] + [Dated photos/video] + [Written contractor cause of loss]

If you have all three pieces of that formula, your claim rests on a solid foundation. But having proof does not automatically mean filing is a smart financial decision. You still need to confirm that the contractor invoice significantly exceeds your deductible. If you have the documentation, but your out-of-pocket repair was only $1,200 and your deductible is $1,000, submitting the file simply does not make mathematical sense given the potential rate impact.

Signs Your “Too Fast” Repair Can Still Be Reimbursed

It is incredibly frustrating to pay thousands of dollars out of pocket for an emergency, only to lie awake weeks later wondering if you left money on the table. The anxiety of “did I mess this up by fixing it too fast?” is the most common feeling at this stage. If you are sitting with a stack of receipts and second-guessing your actions, stop panicking and look for the specific lifelines that save post-repair claims.

You are not automatically disqualified just because the drywall is painted. You have a viable path forward if you can pull together a timeline. Finding even one wide-angle photo of the damage on your phone before the crew arrived changes the conversation entirely. If the damage was from a clearly dated event, like a documented local freeze that burst pipes across the neighborhood, the insurer cannot easily dispute the cause.

The most critical sign of life for your claim is having the emergency repair crew formally document exactly what they saw before the cleanup. If you have that detailed breakdown, and your policy’s filing deadline has not yet passed, you have the legal and evidentiary breathing room to assemble a real case.

Connecting the Dots Before You Call

The insurer’s position is simple: they cannot adjust what they cannot see. Therefore, high-quality documentation serves as the only acceptable substitute for physical inspection. Whether your specific pile of receipts and smartphone photos meets their standard of proof is not something you should guess at.

Key Point: When physical evidence is gone, your documentation is no longer just supporting your claim: it becomes the entire claim.

Because the physical damage has been erased, presenting the file correctly on the very first try is critical. You only get one chance to frame the narrative. Before you submit everything, you still need to decide if the math makes sense. You can review the full framework on deciding whether to file a claim to ensure your expected payout justifies the effort. If the math works, having a professional review your evidence before you upload it to a portal can prevent an immediate denial based on “insufficient proof of loss.”

Final Thoughts on Post-Repair Claims

Your insurance policy is a contract designed to restore your property, not a trap designed to penalize you for taking swift action during an emergency. The challenge of a post-repair claim is not that you broke the rules; it is simply the heavy burden of reconstructing the evidence. Do not write off a massive repair bill just because the contractor has finished sweeping up. Gather your timestamped photos, secure a written statement from the professionals who did the work, confirm your policy deadlines, and consider getting a free claim review from a licensed public adjuster to evaluate the exact strength of your documentation before you officially open the file.

❓ FAQ

🕒 How long do I have to file a claim after fixing the damage?

The deadline depends on the filing window specified in your insurance policy, which is typically one to two years from the original date of loss, not the date the repair was completed.

📸 Can I make a claim if I do not have pictures of the broken pipe?

It is significantly harder, but possible if you have a highly detailed, written assessment from a licensed plumber explaining the exact cause of loss and what they observed upon arrival.

🛠️ What happens if I upgraded my materials during the emergency repair?

The insurer will only owe for “like kind and quality.” If you replaced standard laminate with luxury hardwood during the repair, your claim payout will still be capped at the replacement cost of the original laminate.

📝 What paperwork do I need to send for a repair I already paid for?

You need pre-repair photos, an itemized invoice detailing materials and labor, proof of payment, and ideally a written statement from the contractor outlining the cause of the damage.

💰 Can I get reimbursed for emergency water extraction?

Yes, in most standard policies, the cost of emergency mitigation, such as professional water extraction or roof tarping, is reimbursable as part of a covered claim.

🏚️ Does throwing away the damaged drywall ruin my claim?

It does not automatically ruin the claim, but throwing away physical evidence without taking comprehensive photos first makes it very difficult for the adjuster to verify the scope of the loss.

🔍 Does a text message count as written documentation for a claim?

It can. If your contractor texted you a description of the burst pipe or a photo from the site, screenshot it. While a formal letterhead is better, contemporaneous text messages establish a timeline and are valid evidence.

🛑 When is it too late to report home damage to insurance?

It is too late when the timeframe outlined in your specific policy contract expires. Reporting promptly is always advised to avoid a denial based on late notice.

📞 How do I explain to the adjuster that I had to fix it immediately?

State factually that you took immediate action to mitigate the loss and prevent secondary damage to the property, which aligns with your policy duties, and offer your documentation as proof.

❌ Is an old roof repair eligible for an insurance claim months later?

Yes, if the original storm date is verifiable via weather reports, you have documentation of the repair, and you are still within the time limit defined by your policy.

Filing is just the beginning. These cover what the rest of it looks like.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

That gap is common and usually closeable. These explain how.

- 5 patterns that signal your settlement is probably short

- Who the adjuster at your door actually works for

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When a denial needs legal leverage, not just negotiation

- Four paths to fight a denial, including one most homeowners miss

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.