- Your deductible is not always a flat fee. Many homeowners unknowingly have percentage-based deductibles that can cost thousands of dollars out of pocket.

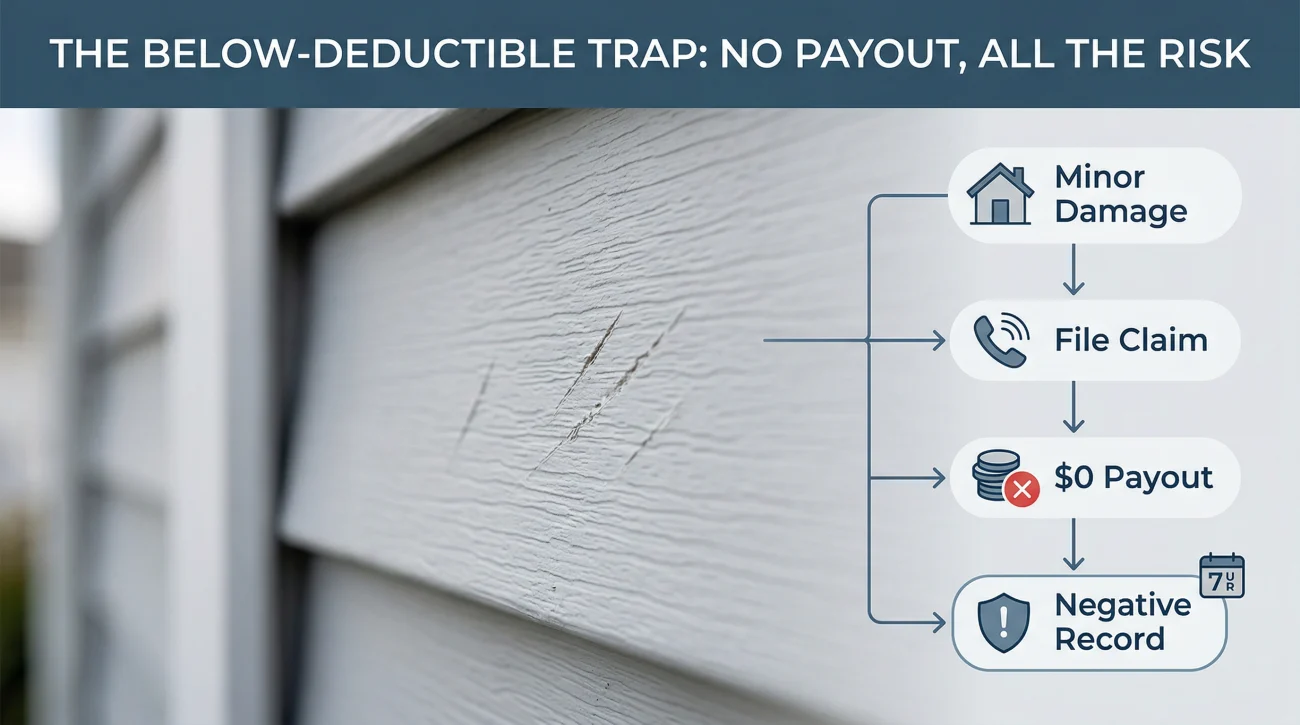

- Filing a claim for damage that costs less than your deductible will result in zero payout but can still leave a negative mark on your insurance record.

- Insurance companies often apply depreciation to your payout before they subtract the deductible, which frequently leaves homeowners with a much smaller check than expected.

The Deductible Reality Check

Most homeowners know they have a home insurance deductible. Far fewer know exactly how it works in practice. In my years reviewing claim files and settlement offers, I have seen countless homeowners find out the hard way that their actual out-of-pocket responsibility is vastly different from what they assumed when they first picked up the phone to file a claim.

Filing a home insurance claim sounds straightforward. You experience property damage, you call your insurance company, they assess the loss, you pay your deductible, and they cover the rest. However, the reality of claims processing is much more calculated. The deductible is not simply an entry fee you pay to get your house fixed. It is a strict financial threshold that dictates whether filing a claim makes any economic sense at all.

If you miscalculate how your specific policy applies the deductible, you risk filing a claim that produces a tiny payout, or worse, no payout at all. Even without a payout, the simple act of filing goes on your claims history. This is why understanding the exact mechanics of your policy’s deductible is the mandatory first step before you allow any contractor to convince you to open a claim.

The Two Types of Deductibles You Must Identify

The first major hurdle in the claim process is identifying exactly how your deductible is structured. Do not rely on your memory from when you bought the policy. You need to pull out your declarations page and look at the numbers. Insurance policies generally use one of two deductible formats, and mixing them up is a very common mistake.

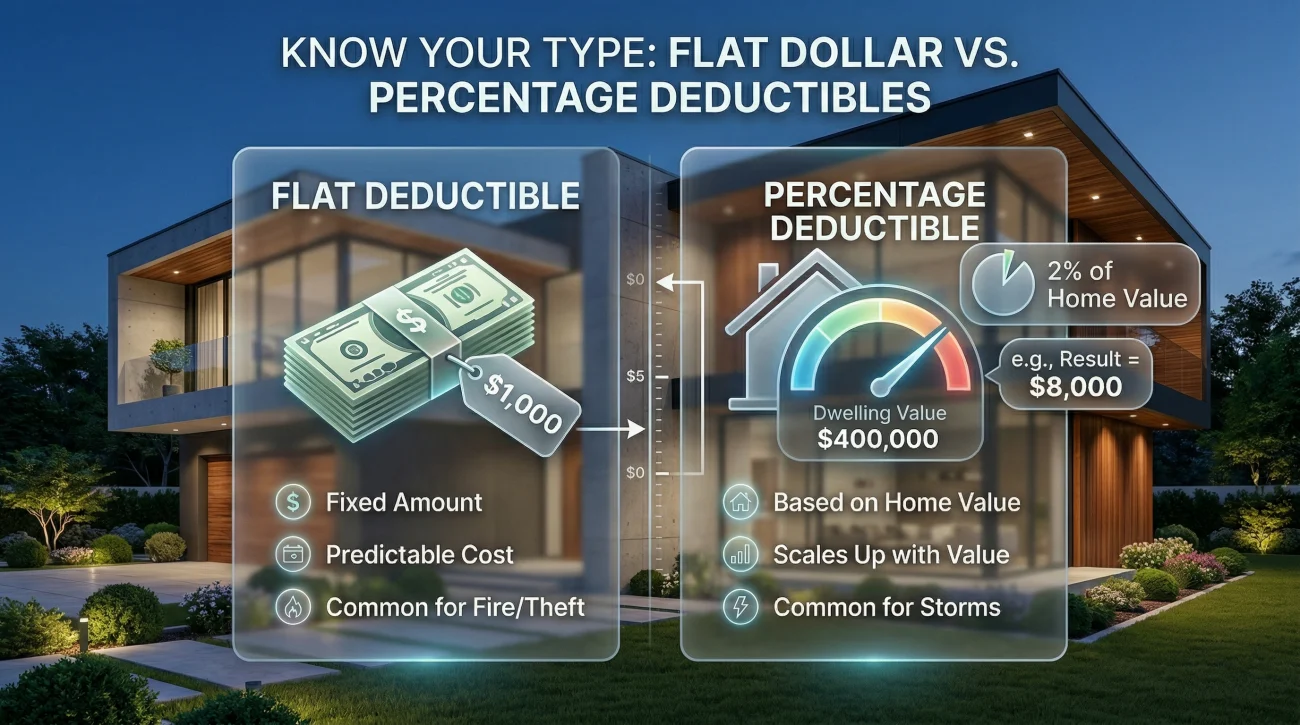

The Flat Dollar Deductible

This is the structure most people are familiar with because it functions exactly like a typical auto insurance deductible. It is a specific, fixed dollar amount written into your policy. Common flat deductibles are $500, $1,000, or $2,500.

If you have a flat $1,000 deductible and suffer $15,000 in covered water damage, the math is simple. The insurance company assesses the damage, subtracts your $1,000 responsibility, and pays you the remaining $14,000. It is predictable and easy to calculate when you are standing in a flooded living room trying to decide what to do next.

The Percentage Deductible

This is where I see the most shock from homeowners. A percentage deductible is not a fixed dollar amount. Instead, it is a percentage of your home’s total dwelling coverage limit (often listed as Coverage A on your policy). Common percentage deductibles range from 1% to 5%.

The confusion happens because people assume the percentage is based on the cost of the damage. It is not. It is based on the total insured value of the house itself. This means your out-of-pocket cost scales up with the value of your property.

Your home is insured for a total dwelling value of $400,000.

Your policy shows a 2% deductible.

Your actual out-of-pocket deductible is $8,000 (2% of $400,000).

If you have $6,000 worth of damage, you will receive no money because the damage does not exceed your $8,000 deductible.

In my experience, percentage deductibles are the number one reason homeowners abandon claims halfway through the process. They file the paperwork, wait weeks for an adjuster, and then realize their 2% deductible on a half-million-dollar home completely consumes the repair estimate.

How to Find Your Deductible Type Right Now

Before moving forward, take three minutes to locate your exact deductible. Pull out your policy’s declarations page (usually the first few pages of your insurance packet) and follow these steps:

- Step 1: Locate “Coverage A” or “Dwelling Coverage” to find your home’s total insured value.

- Step 2: Look for the “Deductible” section. Note whether it lists a flat dollar amount (e.g., $1,000) or a percentage (e.g., 2%).

- Step 3: Scan for weather-specific riders. Look for terms like “Windstorm,” “Hail,” or “Hurricane” deductibles, which are often listed separately.

| Feature | Flat Dollar Deductible | Percentage Deductible |

|---|---|---|

| Structure | Fixed amount ($500, $1,000) | Based on a % of your home’s insured value |

| Example Calculation | Damage is $10,000. Deductible is $1,000. You pay $1,000. | Home insured for $300,000. Deductible is 2%. You pay $6,000. |

| Primary Risk | Easier to plan for; out-of-pocket cost is predictable. | Massive out-of-pocket surprise when large damage occurs. |

The Wind and Hail Deductible Surprise

If you live in a region prone to severe weather, such as coastal areas, tornado alleys, or zones with frequent hail, your policy likely contains a critical variation. Many insurance carriers impose a separate, specialized deductible specifically for damage caused by windstorms or hail.

You might have a standard flat deductible of $1,000 for perils like fire, theft, or a burst pipe. However, if a severe storm blows through and tears off your shingles, your policy might dictate that a separate wind and hail deductible applies to that specific event. In almost all cases, these weather-specific deductibles are percentage-based. Because they scale with your home’s insured value, they are usually much higher than your standard flat deductible.

⚠️ Warning: The wind and hail deductible overrides your standard deductible when storm damage occurs. You cannot choose which one to apply.

This creates a massive financial gap for the most common type of property damage. Roofs take the brunt of severe weather. When a storm hits, roofing contractors often canvas neighborhoods offering free inspections and urging homeowners to file a claim. If you have not checked your declarations page for a wind and hail clause, you might be walking into a trap.

For example, you might think you are paying a $1,000 standard deductible for a new roof. But if your dwelling coverage is $350,000 and you have a 3% wind and hail deductible, your actual responsibility is $10,500. Before signing any roofing contract, a licensed public adjuster can tell you the exact dollar amount your deductible will consume based on your specific policy language.

The Below-Deductible Trap

What happens if you file a claim and the adjuster determines the cost of repairs is actually less than your deductible? In short, the insurance company pays you nothing. You are entirely responsible for the repair costs out of your own pocket. However, the financial damage does not stop there.

Even though the insurance company did not pay a single dollar, you still filed a formal claim. That claim is recorded in your loss history. The database that tracks this information is shared among insurance carriers, and it has a long memory. You need to understand what goes into your CLUE report, because an entry showing a claim was filed, even a zero-dollar payout claim, stays on your record for up to seven years.

When it comes time for policy renewal, or if you try to shop around for a new insurance carrier, that zero-payout claim counts against you. Multiple claims in a short window, regardless of whether they were paid or denied due to the deductible threshold, label you as a high-risk homeowner. This can lead to increased premiums, loss of claim-free discounts, or even a non-renewal notice from your current carrier.

This is why you should never file a claim just to see what the insurance company will say. If there is a high probability that the damage will not significantly exceed your deductible, it is almost always better to absorb the cost privately and protect your claims record.

ACV vs The Deductible: Why Your Payout is Smaller Than You Think

Even if you are confident that the damage far exceeds your deductible limit, the way the insurance company applies it to your settlement can drastically alter your net payout. This comes down to the difference between Replacement Cost Value (RCV) and Actual Cash Value (ACV).

If your policy, or a specific section of your policy like your roof coverage, pays out at Actual Cash Value, it means the insurance company will deduct depreciation based on the age and condition of the damaged items before they issue a check. The critical detail is the order of the mathematical operations. The insurance company applies the depreciation penalty first, and then they subtract your deductible.

Believing the insurer subtracts the deductible from the total repair cost and pays you the rest.

Understanding that the insurer calculates the depreciated value of the damaged items, subtracts your deductible from that lowered amount, and pays you whatever is left.

Let us walk through a practical scenario. Imagine a severe storm damages your 15-year-old roof. The contractor estimates the replacement cost at $12,000. You have a flat $2,000 deductible. You might assume you will get a check for $10,000. Here is what actually happens if your roof is covered at ACV:

- Step 1: Total replacement cost is $12,000.

- Step 2: The adjuster determines the 15-year-old roof has depreciated by 50%. The Actual Cash Value is now $6,000.

- Step 3: The insurer subtracts your $2,000 deductible from the $6,000 ACV.

- Step 4: Your actual net payout check is $4,000.

This calculation is the single most common reason settlement amounts surprise homeowners. The combination of heavy depreciation and a high deductible can turn a five-figure repair job into a tiny settlement check that barely covers the cost of materials.

If your policy covers replacement cost rather than actual cash value, the depreciation story changes slightly. Some of this depreciation may be recoverable. The insurer will still hold back the depreciated amount initially, paying you the ACV minus your deductible. However, once repairs are completed and invoiced, you can typically claim that withheld depreciation back. In virtually all standard policies, the deductible remains your responsibility and cannot be reclaimed.

The Marginal Claim Problem

The most difficult decision homeowners face is the marginal claim. This happens when the damage exceeds your deductible, but only by a small amount. If you have $2,500 in damage and a $1,000 deductible, the insurance company will pay you $1,500. Should you file?

In most operational claim reviews, the answer is no. A marginal claim produces a small net payout but triggers the full consequences of a filed claim. The moment you accept that $1,500 check, you expose yourself to premium surcharges. You must calculate how surcharges impact your future premiums, because a rate increase can easily wipe out the value of a small settlement.

The Filing Formula:

Assess Repair Cost + Calculate Net Payout + Estimate Rate Increase = The Real Cost of Filing

If your premium goes up by $400 a year for the next three to five years because you filed a claim, you have paid back $1,200 to $2,000 to the insurance company. When you factor in the loss of your claim-free discount, you actually lost money by accepting the $1,500 settlement. For most marginal events, the break-even calculation over the surcharge period makes filing the worse financial outcome.

This marginal math is exactly why the old advice of “file if it is over your deductible” is dangerous. You must look at the long-term impact. If you need help weighing all these factors, reviewing the complete decision framework for filing a claim will help you align the deductible math with your long-term insurability risks.

Signs Your Deductible Situation is More Complicated Than Expected

The rules of insurance are rarely clear until you are already deep into the process. The realization that the deductible math is not working in your favor usually hits at the worst possible time. If you are experiencing any of the following frustrations, your filing calculation has likely been derailed by complex policy language.

- You have a percentage deductible listed on your policy, and you have never calculated the actual dollar amount it represents.

- Your home is in a storm-prone area, and you have not checked your declarations page for a separate, higher wind and hail deductible.

- Your settlement offer arrived, and it was significantly lower than expected because you are not sure if ACV depreciation or your deductible type explains the massive gap.

- A contractor is pressuring you to file a claim immediately without explaining how your specific policy deductible will impact your out-of-pocket costs.

Deductible type and ACV calculation are the two variables most homeowners miscalculate in the filing decision. If you have already filed a claim and the net payout feels entirely wrong, do not assume the insurance company’s math is the final word. The combination of heavy depreciation and a high percentage deductible can sometimes mask errors in the underlying damage scope. Check your settlement against what a professional assessment would show to confirm nothing was missed.

Final Thoughts Before You File

Your deductible is the financial gatekeeper of your insurance policy. Understanding how it operates is the only way to protect yourself from filing claims that harm your long-term financial health without providing any immediate relief. Before you pick up the phone to report a loss, take the time to read your declarations page.

Identify whether your deductible is a flat dollar amount or a percentage of your dwelling limit. Check for specific weather-related clauses. Most importantly, do the math. Compare the honest, depreciated value of your damage against your deductible responsibility. If the remaining net payout is not large enough to justify the inevitable rate increases and the mark on your CLUE record, absorbing the cost privately is often the smartest move a homeowner can make.

If your situation involves severe damage, complicated depreciation math, or a settlement offer that barely clears your deductible, do not make the final call based on guesswork. Having an expert look at your policy and the damage can clarify whether proceeding is truly in your financial interest. You can start by getting a free claim review from a licensed public adjuster to understand your real net payout before you commit.

❓ FAQ

🏠 How does a home insurance deductible actually work?

A deductible is the portion of a covered loss you are responsible for paying before your insurance company starts contributing. They will subtract this amount from your total approved settlement before issuing you a check.

💸 Do I have to pay my deductible upfront to the contractor?

You typically do not pay the deductible to your insurance company. Instead, the insurer deducts it from your payout. You then pay your chosen contractor your deductible amount plus the insurance funds to cover the total repair invoice.

📉 What happens if my claim is less than my deductible?

If the approved repair cost is lower than your deductible, the insurance company will not pay anything. However, the claim will still be recorded on your insurance history, which could potentially raise your future premiums.

⛈️ Why is my wind and hail deductible so high?

In areas prone to severe weather, insurers often use a separate percentage-based deductible for wind and hail to limit their risk. This is calculated as a percentage of your total home value, making it significantly higher than a standard flat deductible.

🧮 How is a percentage deductible calculated?

A percentage deductible is calculated based on your home’s total insured dwelling limit (Coverage A), not the cost of the damage. If your home is insured for $300,000 and you have a 2% deductible, your out-of-pocket cost is $6,000.

⏳ Can I waive my home insurance deductible?

You generally cannot waive a deductible. It is a contractual obligation. Beware of contractors offering to “waive” or “eat” your deductible by inflating repair estimates, as this is considered insurance fraud in most states.

📝 Does filing a claim under my deductible still go on my record?

Yes. Any time you formally file a claim, it is reported to the CLUE database, regardless of whether a payout was issued. This zero-pay claim stays on your record for up to seven years.

🗓️ Does my deductible apply per claim or per year?

Unlike health insurance, home insurance deductibles typically apply per claim or per occurrence, not per year. If you have two separate covered events in one year, you will be responsible for paying the deductible twice.

🛠️ Should I file a claim for $500 over my deductible?

Usually, no. While you would receive a $500 check, the resulting premium surcharges and the loss of any claim-free discounts over the next three to five years will almost certainly cost you more than $500.

🔍 Does the insurance company deduct depreciation before or after the deductible?

If your policy pays Actual Cash Value (ACV), the insurance company will deduct the depreciation from the total replacement cost first, and then subtract your deductible from that lowered amount.

🚫 Can my insurance company drop me if I file a small claim?

Filing a single small claim rarely leads to immediate cancellation. However, multiple claims within a short timeframe, even small or zero-payout claims, can trigger a non-renewal notice because you are flagged as a high-risk policyholder.

Filing is just the beginning. These cover what the rest of it looks like.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

That gap is common and usually closeable. These explain how.

- 5 patterns that signal your settlement is probably short

- Who the adjuster at your door actually works for

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When a denial needs legal leverage, not just negotiation

- Four paths to fight a denial, including one most homeowners miss

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.