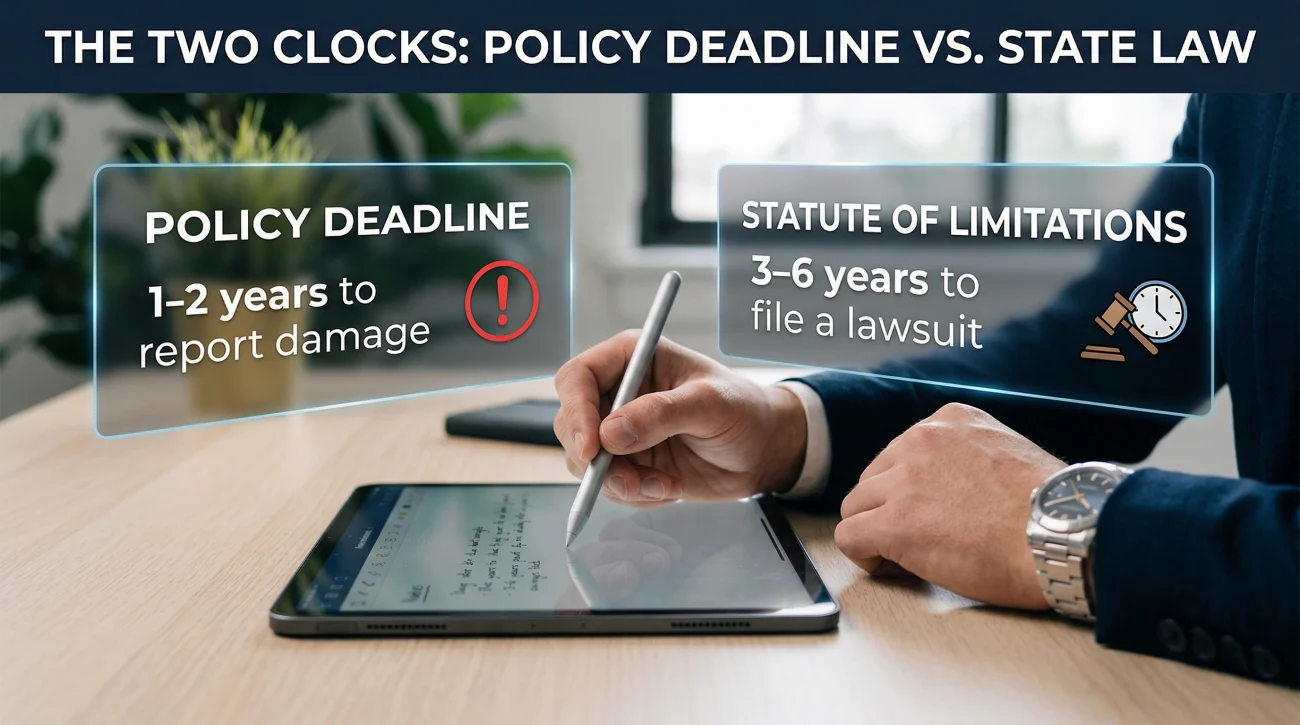

- Your policy claim filing deadline and your state’s statute of limitations are two completely different clocks. The policy deadline is usually much shorter and is the one that matters first.

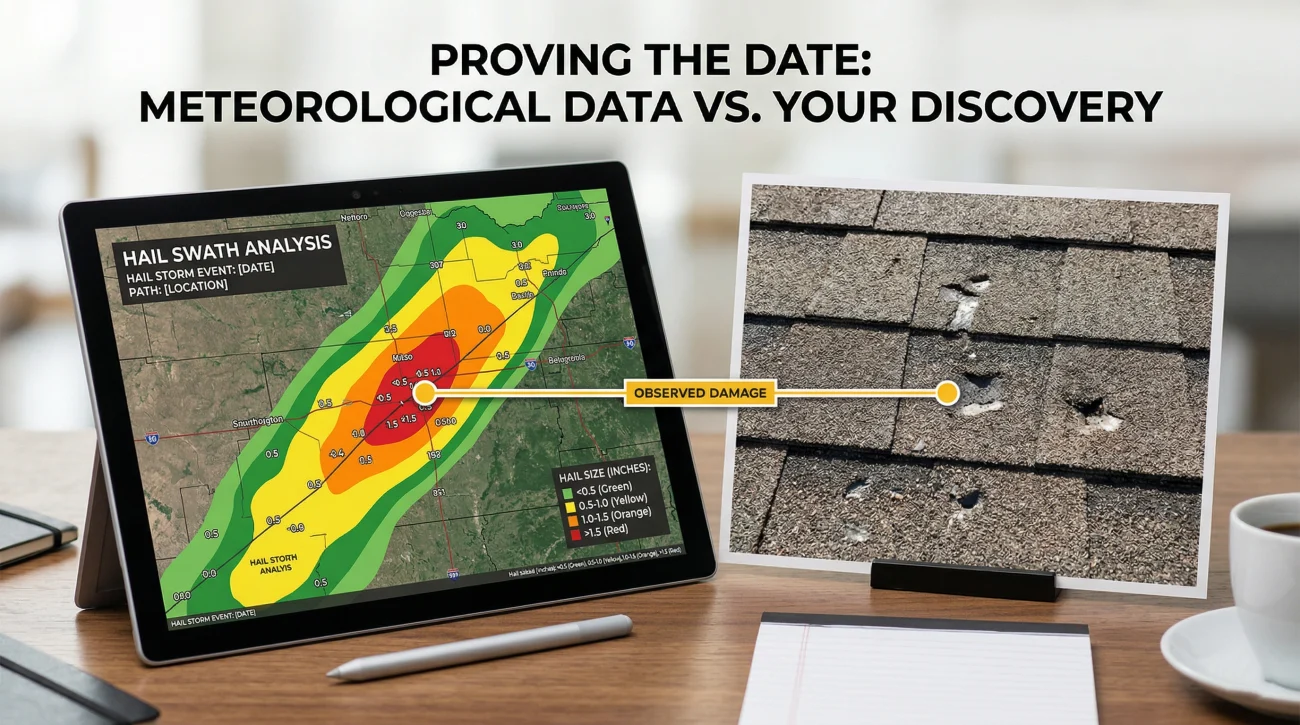

- Insurers use meteorological data and weather records to establish the exact date of storm losses. You cannot simply use the date you discovered the damage.

- If you discover hidden damage months later, some policies have a “late discovery” provision, but documenting exactly when and how it was found is critical to your success.

- Filing a late claim often results in a procedural denial that is very difficult to overturn. It is always better to file a preliminary notice of claim to stop the clock, even if your repair estimates are not completely finished.

The Reality of Discovering Home Damage Months After the Event

Finding damage to your home is stressful enough, but finding it months after a severe storm or a hidden pipe failure introduces a completely different kind of anxiety. Homeowners in this situation immediately face a ticking clock. The most common question I hear when someone uncovers a hidden roof leak or a slow-growing water stain is whether the home insurance claim time limit has already expired.

In my experience reviewing hundreds of property files, time limits are one of the most misunderstood aspects of the entire recovery process. When damage is discovered late, the immediate focus of the adjuster is often on the calendar rather than the physical destruction. You might be pointing at a collapsed ceiling, but the desk adjuster is calculating days on a spreadsheet. Insurance companies enforce deadlines strictly because as time passes, physical evidence degrades, memories fade, and distinguishing between sudden covered damage and general wear and tear becomes incredibly difficult.

Before you make a panicked phone call to your carrier, you need to understand exactly how the deadlines work, how insurers determine when an event actually happened, and what your options are if you are dangerously close to the cutoff. The rules governing how long you have to file a home insurance claim are rigid, but understanding the mechanics can mean the difference between a covered repair and an outright rejection.

The Two Different Clocks You Are Racing Against

The single biggest mistake homeowners make regarding deadlines is conflating two entirely separate legal concepts. When people search the internet for time limits, they often find the wrong answer because they do not know the difference between a policy provision and a state law. There are two different clocks running after a damage event.

The Policy Claim Filing Deadline

The first clock is set by your insurance contract. This is the policy claim filing deadline, and it is the hurdle that matters most. When you purchased your homeowners insurance, you agreed to the terms within that specific document. Most standard policies state that you must report a loss within a specific timeframe, which is typically one to two years from the date of loss.

You will typically find this language buried in the “Conditions” section of your policy packet, often under a heading like “Duties After Loss” or “Your Duties After Loss.” If you fail to notify the insurer within this contractual window, they have the right to deny the submission based solely on late reporting. This means they do not even have to debate whether the damage itself is covered. They can simply point to the missed deadline.

⚠️ Warning on the word “Promptly”: Many policies use the vague word “promptly” instead of a hard number. This ambiguity is frequently weaponized against homeowners. If your reporting delay was caused by severe weather preventing property access, or a sudden hospitalization, document that context immediately to defend your interpretation of “prompt.”

The Statute of Limitations

The second clock is the statute of limitations. This is a deadline set by your state’s laws, not your insurance company. The statute of limitations governs how long you have to file a lawsuit against your insurer if a dispute arises, such as a bad faith denial or a severe underpayment.

State statutes of limitation are typically much longer than policy filing deadlines, sometimes extending up to three, five, or even six years depending on your jurisdiction. The trap that catches many people is reading about their state’s five-year statute of limitations and assuming they have five years to simply notify their insurer of a missing roof shingle. By the time they pick up the phone, their one-year policy deadline has long passed.

I have seen countless homeowners forfeit their right to recovery because they relied on a general internet search for state laws rather than reading the specific reporting requirements printed in their own policy packet. The policy deadline is always the first gate you must pass.

Understanding which clock you are fighting is just the first step. Before you commit to opening a file, it is vital to assess all the variables involved, including your deductibles and premium risks. If you are still weighing the full framework of whether submitting a loss history record makes sense, verifying your exact deadline is the prerequisite to that entire decision.

How Insurers Establish the True Date of Loss

I often see this play out during spring roof inspections: a contractor climbs up, finds significant hail damage, and the homeowner immediately tries to file a claim using the date the contractor discovered the damage. This almost never works.

For weather-related events, insurers do not rely on your discovery date. They rely on meteorological weather records. Insurance carriers subscribe to sophisticated weather tracking databases and hail maps that pinpoint exactly when and where severe weather occurred down to the specific neighborhood block. This is how they establish the official “date of loss.”

This reality creates two immediate implications for your timeline:

- 📍 The clock starts on the weather date:

If the only hail storm capable of causing your specific roof damage happened 14 months ago, and your policy has a one-year filing deadline, you are already outside your window. - 📍 You cannot guess the date:

If you file and claim the damage happened during a minor rainstorm last week, the adjuster will pull the weather report for that date. If the report shows no hail or high winds, your submission will hit a massive roadblock regarding the cause of loss.

Telling the representative that the storm damage must have happened “sometime last month” because that is when you noticed the leak on the ceiling.

Working with a professional to pull localized weather reports to match the physical damage to a specific, verified storm event that falls within your policy’s allowed timeframe.

The Late Discovery Exception for Hidden Damage

What happens if the damage was genuinely impossible to see? Consider a slow, continuous water leak from a pipe hidden behind a kitchen cabinet. The pipe may have failed six months ago, but the damage only became visible when the floorboards started to warp today.

In some states and under certain policy language, there is an exception known as the “late discovery rule.” This rule recognizes that a reasonable homeowner cannot be expected to report damage they could not possibly have known about. If this rule applies, the filing clock may begin ticking from the date the damage was discovered, or the date it reasonably should have been discovered, rather than the date the pipe initially cracked.

⚠️ Warning: The late discovery exception is highly contested. Insurers will often argue that while the water was behind a wall, there were secondary signs like musty odors or an unusually high water bill that should have prompted an earlier investigation. Proving late discovery requires meticulous documentation.

If you are relying on a late discovery argument, the immediate preservation of evidence is mandatory. The adjuster needs to see exactly why the damage was hidden from plain view. Before tearing out drywall or completing repairs, you must create a concrete record:

- 📸 As-found photographs: Clear, well-lit shots of the hidden area before any material is moved or cleaned up.

- 📸 Surrounding context: Photos showing that there was no visible access point or exterior sign of the leak prior to the discovery.

- 📄 Utility history: Copies of your water bills showing no unexplained spikes that should have alerted you earlier.

- 📄 Contractor notes: A written statement from the emergency plumber or mitigation crew confirming the damage was structurally concealed.

How well you build this record before making the call will largely determine whether a late discovery argument holds up during adjustment.

What Actually Happens If You Miss the Deadline

Filing after your contractual window has closed triggers a specific sequence of events. First, the insurer will likely send you a “Reservation of Rights” letter. This document essentially states that while they will send an adjuster to investigate the property, they are reserving their right to deny the settlement later based on the late reporting.

Following the investigation, the most likely outcome is a procedural denial. The rejection letter will state that because you failed to report the loss within the required timeframe, the insurer’s ability to investigate the cause of the damage was “prejudiced.” This means the delay prevented them from determining if the damage was caused by a covered sudden event or an uncovered maintenance issue.

Overcoming this specific type of rejection requires a completely different strategy. A procedural timing denial is generally much harder to challenge than a simple disagreement over repair costs. If you are challenging an outright rejection based on procedural timing, you usually have to prove that your delay did not actually harm the insurance company’s ability to investigate the physical evidence. This is a high burden of proof.

💡 Pro Tip: In very rare cases, the clock can be temporarily paused—a concept known as “tolling”—if the insurer acknowledges the damage but delays their own investigation. However, proving tolling requires complex legal maneuvering and is not a DIY task; it requires professional advocacy.

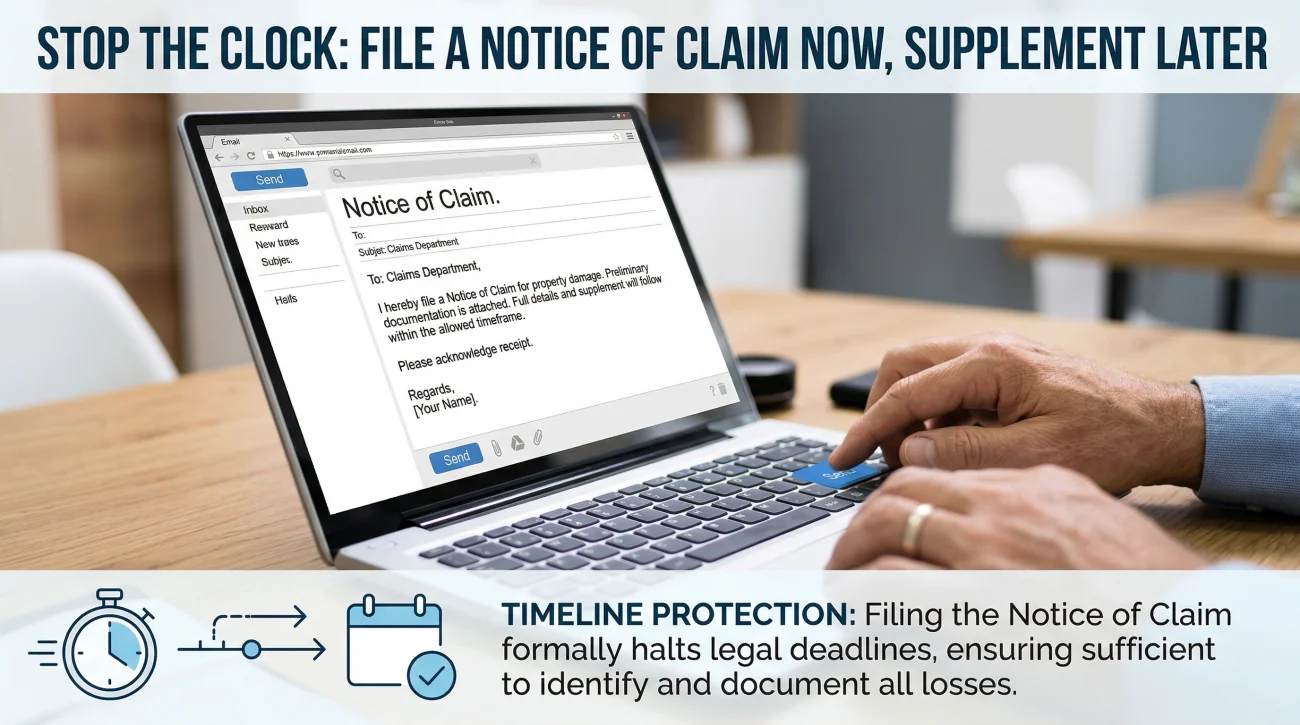

Filing Promptly Without Full Documentation

One of the most frequent errors I observe is a homeowner waiting to notify their insurer because they are waiting on a contractor to provide a final, itemized repair estimate. They watch the deadline approach, believing they need a perfect file before they can make the call.

You do not need a contractor’s estimate to notify your carrier. If you know a covered event occurred and you are nearing the end of your allowed time, you must file a “notice of claim” promptly to stop the clock. Filing the initial notice secures your place within the timeline. You can always supplement the file with contractor estimates, engineering reports, and detailed photographs later during the adjustment phase.

When you send that initial notification, keep it strictly factual. You simply need to state what happened, when it occurred (or was discovered), and confirm that your detailed estimates will follow shortly.

Subject: Notice of Claim for Property Damage

Hello,

I am writing to formally report property damage at [Property Address]. On [Date], we experienced [factual description, e.g., a sudden pipe failure in the downstairs bathroom / severe wind damage to the roof structure].

We are currently mitigating the damage and arranging for contractors to assess the full scope of the required repairs. I will forward the itemized repair estimates and detailed photographic documentation as soon as they are completed. Please assign an adjuster and provide my claim number.

Thank you.

Pro Tip: Always secure written confirmation from the representative stating the date your initial notification was received. A paper trail is your only defense if a timeline dispute arises months down the line.

When Timing Complicates Your Recovery

The anxiety surrounding deadlines usually peaks when a homeowner realizes their situation does not fit neatly into a standard timeline. Time limits become the weapon used against your recovery in several highly stressful scenarios.

You may find yourself facing these exact frustrations right now:

- 📍 The Contractor Discovery: A roofer inspecting your home for an unrelated issue informs you that you have massive hail damage from a storm that happened over a year ago. You have no idea if your policy allows you to act on this information.

- 📍 The Cosmetic Misjudgment: You noticed a few missing shingles months ago but assumed it was minor cosmetic wear. Only now, after heavy rains caused major interior ceiling leaks, do you realize the roof structure was compromised long ago.

- 📍 The Repair Regret: You suffered a burst pipe, paid a mitigation crew out of pocket to dry the house immediately, and rebuilt the walls. Six months later, you realize the financial hit was devastating and you want to ask your carrier for reimbursement, but the physical evidence is completely gone.

If you fall into that last category, your situation requires a completely different documentation strategy. The insurer cannot send an adjuster to inspect damage that no longer exists. For guidance on that specific hurdle, you must focus heavily on understanding how to prove your case if you have already completed the physical restoration.

Final Thoughts on Protecting Your Window

The difference between a timely submission and a late one is frequently determined by how the loss date is established and documented, not just when you happened to notice a stain on the wall. Whether your specific situation still falls within the safe filing window depends entirely on the exact language printed in your policy and the physical evidence proving when the damage actually occurred.

If you are standing on the edge of your deadline, or if your insurer is already attempting to deny your payout based on late reporting, you should not try to navigate the appeals process alone. Procedural disputes require expert handling of the policy language.

If you need to know whether your late-discovered damage is still viable, consider having a licensed professional review your loss timeline and scope documentation to protect your interests. If you have already received a formal denial letter citing a missed deadline, it may be time to look into discussing your situation with a legal advocate who understands bad faith and timeline disputes in your specific state.

❓ FAQ

⏳ Is there a strict time limit on home insurance claims?

Yes. Your specific insurance policy contains a mandatory timeframe in which you must report damage. This window is typically one to two years from the exact date the damage occurred, but you must check your policy declarations for your exact limit.

📅 How long do I have to file a home insurance claim after a storm?

Most standard policies require you to file within 365 days or 730 days of the specific storm event. Insurers will verify the exact date of the storm using meteorological records, so the clock starts on the day the weather hit, not the day you noticed the damage.

🕰️ Can you file a home insurance claim years later?

Generally, no. Filing years later usually results in an automatic denial for late reporting. The only exception is if your state and policy allow for a “late discovery” rule, which applies only if the damage was completely hidden and impossible to detect earlier.

📝 What happens if I miss the deadline to file an insurance claim?

If you miss the deadline stipulated in your contract, the insurance company will typically issue a procedural denial. They will argue that your delay prejudiced their ability to properly investigate the physical evidence, voiding your right to a settlement.

⚖️ What is the statute of limitations for a homeowners insurance claim?

The statute of limitations is a state law determining how long you have to file a lawsuit against your insurer for a dispute, sometimes extending up to three, five, or even six years. This is different from, and almost always longer than, the policy deadline to simply report the damage.

🌧️ Should I wait for contractor estimates before filing my claim?

No. If you are approaching your policy deadline, you should file a formal notice of claim immediately to stop the clock. You can always provide the detailed contractor estimates and photographs to the adjuster later.

🔎 How do insurance companies know when the damage happened?

Adjusters use advanced weather tracking software, historical hail maps, and material wear-and-tear analysis to date the loss. They do not just take your word for it; the physical evidence and public data must match the date you report.

🏚️ Does my deadline change if my contractor just found the damage?

Usually not. For weather events, the clock still starts on the date the storm occurred, regardless of when your roofer or contractor inspected the property. Prompt post-storm inspections are highly recommended for this reason.

💧 What if the water damage was hidden behind a wall?

If the damage was genuinely hidden, you may be able to utilize a late discovery provision, meaning the clock starts when you found the leak. However, you must meticulously document the scene to prove the damage was not visible beforehand.

🛑 Can an insurance company deny a claim just for being late?

Yes. If you breach the prompt reporting conditions outlined in your contract, the insurer has the legal right to reject the submission based entirely on the delay, without ever evaluating the cost of your repairs.

Filing is just the beginning. These cover what the rest of it looks like.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

That gap is common and usually closeable. These explain how.

- 5 patterns that signal your settlement is probably short

- Who the adjuster at your door actually works for

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When a denial needs legal leverage, not just negotiation

- Four paths to fight a denial, including one most homeowners miss

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.