- Not every difficult or delayed claim requires a lawyer. Many scope and pricing disputes are better handled by a public adjuster who can negotiate the valuation of your damage.

- A home insurance claim lawyer becomes the right tool when the dispute shifts from a negotiation problem (pricing) to a legal problem, such as your insurer acting in bad faith, misrepresenting your coverage, or ignoring your formal appeals.

- Cost should not stop you from seeking legal help. Most property damage attorneys work on a contingency fee basis, meaning you pay nothing upfront and they only get paid if they successfully recover money for your claim.

The Tipping Point in a Property Damage Dispute

In my time reviewing hundreds of property damage files and sitting across from insurance adjusters, I have seen claims derail for almost every reason imaginable. Sometimes, the adjuster simply misses a room during the inspection. Other times, the software they use spits out a labor rate that has not been accurate in your zip code for five years. These are frustrating situations, but they are normal hurdles in the standard process.

However, there is a distinct line where a normal delay or disagreement morphs into a fundamental breach of trust. Not every difficult insurance claim needs a lawyer, but some absolutely do. Waiting too long to get professional legal help when you are facing a hostile or unreasonable insurance company can severely limit your options and your financial recovery.

The hardest part for most homeowners is identifying exactly where that line is. When you are staring at a massive repair bill and a denial letter, it all feels like a legal problem. My goal here is to help you strip away the confusion. We are going to walk through exactly how to tell if your situation requires a public adjuster for negotiation, or if you have crossed into territory where a home insurance claim lawyer is the only logical next step.

When a Public Adjuster is the Right Tool

Before we dive into when to hire an attorney, we have to talk about the alternative. A significant portion of the homeowners who think they need a lawyer actually just need a better negotiator. This is where a public adjuster comes in. A public adjuster is an insurance professional licensed by your state to represent you, the policyholder, in evaluating and negotiating the value of your property loss.

If your insurer acknowledges that your damage is covered, but they simply refuse to pay what your contractor says the repairs will cost, you generally have a valuation dispute. Valuation disputes are negotiation problems, not legal problems. If you have not yet exhausted your negotiation options, reviewing the standard claim denial process and learning how to fight a denied claim with professional help is often the most practical first step.

Scope Disputes and Undervalued Damage

Let us say a severe windstorm damages your roof. The insurance company’s independent adjuster comes out, agrees that wind caused the damage, and writes an estimate. The problem is that their estimate only covers replacing a few shingles, while three different local roofing contractors have told you the entire roof is compromised and needs full replacement.

The insurance company is not denying coverage. They are disagreeing on the “scope” of the damage. In these scenarios, bringing in a lawyer might be premature. A public adjuster knows how to write an estimate using the same exact software (often Xactimate) that the insurance company uses. They can document the brittle test failures, photograph the unsealed shingles, and argue the construction facts directly with the desk adjuster.

“I frequently review files where a homeowner was ready to sue their insurance company over a $15,000 gap in repair costs. Once a public adjuster stepped in and submitted a hyper-detailed, line-by-line supplement request with proper photo documentation, the insurer paid the difference without a single legal threat. The issue was not bad faith; the issue was that the homeowner’s original documentation was just not strong enough to trigger the payment.”

Incomplete Documentation Problems

Another common scenario where a public adjuster shines is when you simply do not know how to prove your loss. If you suffered a massive house fire, the sheer volume of personal property you need to list, age, and value is staggering. If the insurance company is delaying your claim because your contents list is incomplete or lacks proof of ownership, a lawyer is not going to inventory your burnt living room. A public adjuster, however, will.

💡 Pro Tip: If your primary frustration is that the insurance company’s dollar amount is too low, but they agree the event itself is covered under the policy, your first call should usually be to a public adjuster, not an attorney.

When a Lawyer Becomes the Right Tool

While a public adjuster argues the facts of the damage, a homeowners insurance claim lawyer argues the law and the binding language of the insurance contract. When an insurance company decides to dig its heels in on a coverage issue, or when their behavior crosses the line from “slow” to “intentionally evasive,” negotiation is no longer effective. You cannot negotiate with a brick wall.

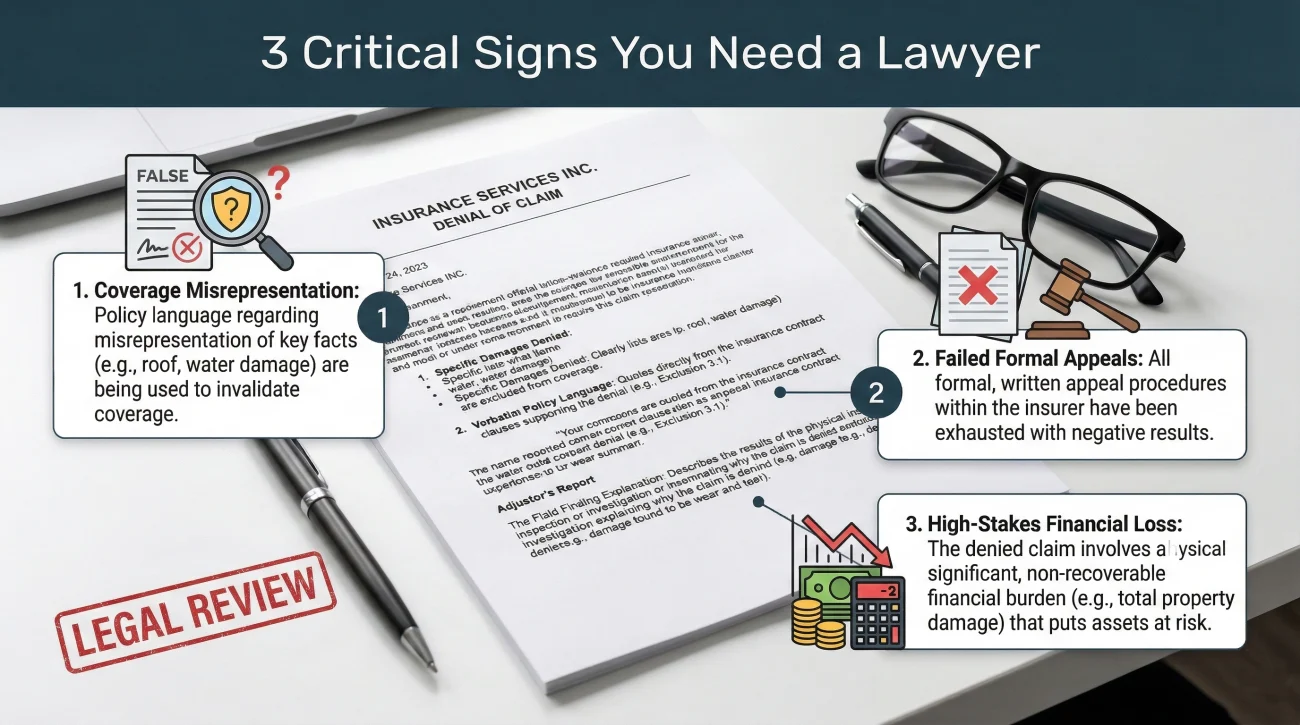

Your Coverage is Being Misrepresented

Insurance policies are incredibly dense documents. Sometimes, adjusters misinterpret them. Other times, the insurance company actively relies on confusing language to deny perfectly valid claims. If your denial letter cites a specific exclusion that you know does not apply to the facts of your loss, you are facing a legal dispute.

For example, if a pipe bursts inside your wall and floods your home, that is typically a covered event. But what if the adjuster’s letter claims the damage was due to “long term seepage and leakage” and denies the entire claim, despite your plumber providing a written report stating the pipe ruptured suddenly? The insurer is miscategorizing the factual event to fit an exclusion in their policy. An attorney steps in to legally challenge that misrepresentation.

Your Formal Appeals Have Failed

If you have already navigated the standard appeals process, submitted a well-documented appeal, provided contractor reports, and the insurance company still upholds their denial without providing any new reasoning, you have hit a dead end. At this point, sending a third or fourth letter yourself will not change their mind. The introduction of legal counsel changes the internal math for the insurance company. If you are wondering whether you can sue your insurance company, the answer often depends on how they respond to these formal appeals.

The Financial Loss Requires Legal Leverage

When you are dealing with a total loss fire or a massive hurricane claim, the financial exposure for the insurance company is massive. Sometimes, the sheer size of the claim makes the insurer overly defensive. They might subject you to endless requests for the same documents or demand an Examination Under Oath (EUO). In these high-stakes environments, the leverage that a property damage insurance claim lawyer brings is often the only way to level the playing field. The insurer knows that an attorney can compel them to produce their internal claim handling guidelines through the discovery process if a lawsuit is filed.

When the financial stakes reach this level, and the insurer’s tactics shift from investigation to intimidation, your response strategy must change accordingly.

Threatening to sue the adjuster over the phone because they offered you $5,000 less than your roofing quote. This makes you look emotional and harms your credibility.

Calmly requesting a detailed explanation of the denial in writing, realizing it relies on a twisted interpretation of your policy, and bringing that written denial to a specialized attorney for review.

What “Insurance Bad Faith” Means in Plain English

You will often hear the term “bad faith” thrown around in insurance forums. Homeowners get angry and immediately want to file an insurance bad faith claim. However, bad faith is a very specific legal concept. It does not just mean the insurance company made a mistake or was rude to you. It means the insurer failed to uphold their legal duty to handle your claim fairly, honestly, and reasonably. Sometimes, a simpler administrative issue can be resolved if you file a complaint with your state insurance department, but true bad faith requires stronger action.

We do not need to look at dense state statutes to understand this. We can look at the actual behaviors that courts repeatedly recognize as insurance bad faith examples.

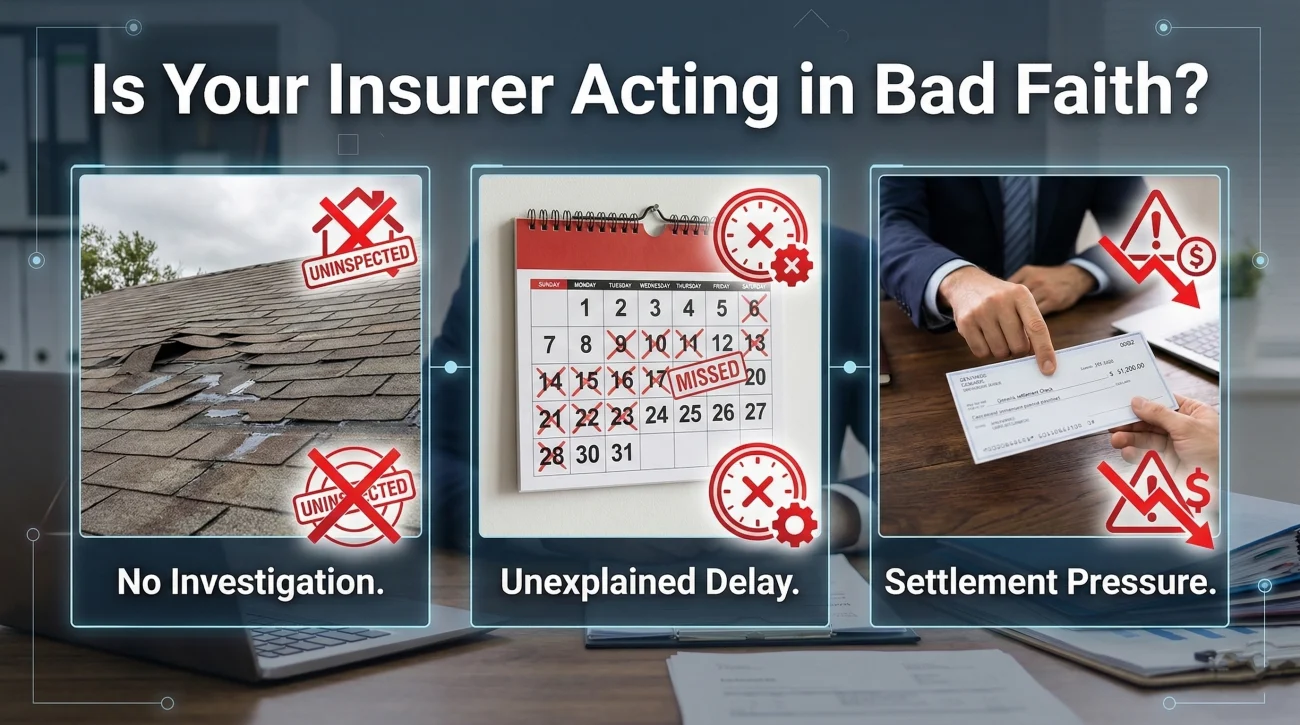

Denial Without Reasonable Investigation

Your insurance company cannot deny your claim just because they feel like it. They have a duty to investigate. If your roof collapses after a snowstorm, and the insurance company sends a denial letter citing “pre-existing structural defect” without ever sending an engineer or an adjuster to physically inspect the attic space, that is a massive red flag. They cannot reach a conclusion without doing the homework to support it.

Unreasonable and Unexplained Delay

While natural disasters can stretch timelines legitimately, insurance companies are generally expected to acknowledge claims, conduct their investigation, and issue decisions within a reasonable timeframe. An insurer cannot simply put your file in a drawer and ignore you. Insurance company bad faith delay often looks like a revolving door of adjusters where every time you call, you are told “the new adjuster is reviewing the file,” month after month, with no actual progress being made.

Key Point: Delaying a claim simply to starve the policyholder out and force them to accept a lowball settlement out of pure desperation is one of the most classic examples of bad faith behavior.

Pressure to Accept a Settlement Quickly

Conversely, sometimes bad faith looks like extreme speed. If your house burns down on a Tuesday, and on Thursday the insurance company is offering you a check for a fraction of your policy limit and aggressively pressuring you to sign a “full and final release” before you have even had time to hire a contractor to assess the ashes, they are acting improperly. They are trying to lock in a cheap settlement while you are in a state of shock.

Here is what an improper delay communication often looks like in the real world:

Subject: Status Update on Claim #8839201

Dear Homeowner,

We are writing to inform you that your claim is still under review by our management team. We require an additional time to assess the coverage parameters of your policy. We will notify you when a determination has been made.

Sincerely,

Desk Adjuster Team

If you receive a letter like that every few weeks for six months without any requests for new information or any physical inspections taking place, you are likely experiencing a bad faith delay tactic. They are not investigating; they are just stalling.

What a Property Damage Insurance Claim Lawyer Actually Does

Many people hesitate to hire legal counsel because they simply do not know what the attorney will do behind closed doors. They fear it will just lead to years of court battles. In my experience, homeowners are often surprised by how quickly the tone of a claim changes once a letter of representation is filed. While litigation is a possibility, a lawyer spends most of their time building a case so strong that the insurance company is forced to settle before a trial ever happens.

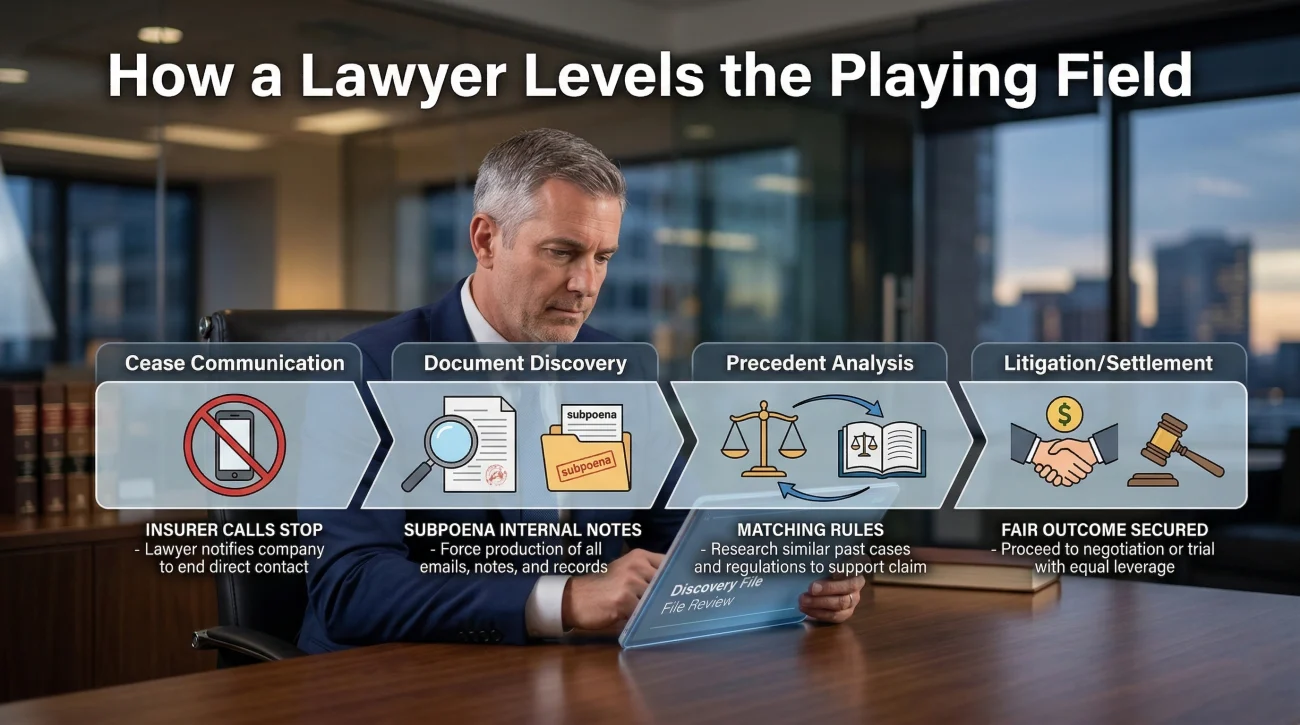

Building the Legal Case and Taking Over Communication

When you hire an attorney, they take over all communication. The insurance company is no longer allowed to call you directly; they must speak to your lawyer. This alone stops the harassment and pressure tactics. The attorney will then pull your complete policy, read the endorsements that you might not even know you have, and build a legal argument showing exactly why the denial or underpayment violates the contract.

Compelling Document Discovery (The Superpower)

This is the true superpower of legal representation. If a lawsuit is filed, your attorney can use the discovery process to legally demand internal documents from the insurance company. They can demand to see the field adjuster’s unedited notes. They can subpoena emails between the adjuster and their manager. When I look at poorly handled claims, it is common to suspect that a field adjuster originally wrote an estimate for $50,000, and a manager back at the corporate office secretly deleted line items to drop it to $15,000. Your attorney will uncover that exact digital paper trail during discovery.

Negotiating with Contractual Expertise

Adjusters negotiate differently with homeowners than they do with attorneys. An adjuster knows a homeowner usually does not understand the specific case law governing “matching rules” in their state: for instance, when an insurer is legally required to replace an entire section of siding because patching it would result in a mismatched, patchwork appearance. An attorney knows this precedent intimately. When they send a demand letter, it carries the implicit threat of a lawsuit, forcing the insurer’s legal department to re-evaluate the cost of defending a losing case.

The Realistic Timeline of Legal Action

I always tell homeowners not to expect a settlement overnight just because an attorney is involved. Here is how the timeline typically plays out:

- Week 1 to 4: The attorney reviews your policy, gathers your contractor estimates, and sends a formal demand letter or notice of intent to sue.

- Month 2 to 3: The insurance company responds. This often triggers a new round of high-level negotiations, sometimes involving the insurer’s own legal counsel.

- Month 4 and Beyond: If the insurer refuses to settle reasonably, a formal lawsuit is filed, moving the case into the discovery phase. Many cases settle during this phase before ever seeing a courtroom.

How Does an Insurance Claim Attorney Get Paid?

This is the single biggest roadblock. When I speak to homeowners whose claims are clearly being mishandled, the first thing they say is, “I am already out $40,000 on my kitchen rebuild, I cannot possibly afford to pay a lawyer $300 an hour.” The insurance industry counts on you believing that. The truth is, you almost never pay a property damage attorney an hourly rate out of your own pocket.

The Contingency Fee Model Explained

Property damage attorneys generally work on a contingency fee basis. This means exactly what it sounds like: the attorney’s payment is contingent upon them winning your case. You pay nothing upfront. If they do not recover any money from the insurance company, you do not owe them attorney fees.

If they do win, their fee is calculated as a percentage of the settlement they recover for you. This aligns your goals perfectly because the attorney is highly motivated to maximize your settlement. Because of this model, the myth that you cannot afford legal help simply does not apply here. Almost every reputable firm offers a completely free initial consultation to evaluate your denial letter. If they offer to take your case, it is a very strong signal that your insurance company is in the wrong.

Here is the formula to keep in mind:

[Zero Upfront Cost] + [Attorney Assumes the Risk] = [Percentage Taken Only From Successful Recovery]

PA vs Lawyer: A Practical Decision Framework

To make this actionable, you need a clear framework to decide who to call. Remember, picking the right professional early on saves you months of wasted time.

| Claim Situation | The Right Professional | Why This Choice Makes Sense |

|---|---|---|

| Insurer agrees to pay, but the estimate is vastly underpriced. | Public Adjuster | This is a construction pricing dispute. PAs excel at line-by-line estimating and local code documentation. |

| Insurer denies the claim citing an exclusion you believe is misapplied. | Insurance Claim Lawyer | This requires interpreting contract law and legal precedent. Only an attorney can argue legal coverage in court. |

| You have a large volume of personal property to inventory after a fire. | Public Adjuster | PAs will do the tedious, time-consuming work of sourcing and pricing thousands of individual items. |

| Insurer stops responding entirely and refuses to issue a decision letter. | Insurance Claim Lawyer | This signals potential bad faith delay. An attorney’s demand letter forces a legal response timeframe. |

When Both a PA and a Lawyer Make Sense

It is worth noting that for massive, complex claims (like a total loss fire), these two professionals are not always mutually exclusive. In my experience with high-dollar files, it is quite common to see a homeowner use both. A public adjuster handles the grueling task of pricing the materials, writing the structural estimate, and inventorying the contents. Concurrently, an insurance attorney handles the bad faith delays and legal leverage required to force the insurer to actually release the funds based on the PA’s valuation. They fight on two different fronts.

The Documentation Audit Before You Call a Lawyer

Before you request a free legal consultation, you need to gather your ammunition. Attorneys evaluate cases based on facts and paper trails, not just frustration. Having these items ready will allow an attorney to tell you almost immediately if you have a viable case:

- The Declaration Page and Full Policy: They need to see your exact coverage limits and endorsements.

- The Formal Denial Letter: Do not just summarize what the adjuster said on the phone. The attorney needs to see the specific policy language the insurer cited in writing to justify their denial.

- A Chronological Communication Log: A simple timeline showing when you filed the claim, when they inspected, and timestamps of your unanswered emails. This is critical for proving bad faith delay.

- Independent Contractor Quotes: Written proof that the actual cost to repair your home vastly exceeds the insurance company’s estimate.

Warning Signs Your Claim Has Reached Legal Territory

It is exhausting to fight a massive corporation while your house is in disrepair. To cut through the noise, look for these three specific patterns. If your claim matches any of these, your situation has almost certainly moved beyond simple negotiation and into legal territory.

- 1. The Insurer is Weaponizing “Anti-Concurrent Causation” Clauses: This happens when two events cause damage at the same time: one covered (like wind tearing off your roof) and one excluded (like subsequent surface water flooding). If the insurer uses a minor excluded peril to entirely wipe out coverage for the massive, clearly covered wind damage, they are engaging in complex legal maneuvering that requires an attorney to untangle.

- 2. The Insurer Has Ignored Your Formal Appeal for Months: You submitted a comprehensive package with engineer reports and contractor estimates. You requested a response in writing. Months have passed, and despite your follow-up emails, they offer no substantive response. Silence in the face of a documented appeal is a deliberate tactic to wear you down.

- 3. They Are Withholding Undisputed Funds to Force a Full Release: If the insurer admits they owe you $20,000 for the living room, but they refuse to cut that check unless you sign a document releasing them from liability for the kitchen and roof damage you are still disputing, this is a massive red flag. They cannot hold your undisputed ACV funds hostage to force you to drop the rest of your claim.

“The most heartbreaking files I review are the ones where a homeowner gave up after a year of delays, simply because they did not realize the insurer’s silence was a known tactic. They walked away from tens of thousands of dollars they were rightfully owed because they thought their only option was to keep sending emails the adjuster was trained to ignore.”

The Next Step: Professional Legal Review

If those warning signs feel familiar, it is time to stop playing the insurance company’s game. Continuing to argue with an adjuster over the phone will not change their mind once a claim has been formally denied on a legal coverage issue, or when bad faith tactics are in play.

The most protective step you can take right now is to stop submitting unguided responses and have a specialized legal professional review your denial letter. A formal evaluation gives you immediate clarity on exactly where you stand legally, without committing you to a lawsuit. To explore this option and see if your claim qualifies for legal representation, you should consider getting a free legal consultation to determine your best path forward.

Final Thoughts on Protecting Your Investment

I have seen too many homeowners accept a terrible settlement simply out of exhaustion. Your insurance policy is a legally binding contract, and you upheld your end of it by paying your premiums every single month. When the insurance company refuses to do their part after a valid loss, you do not have to accept their first, second, or third ‘no’.

Document every single interaction, keep all correspondence in writing, and do not be intimidated by the legal jargon in your denial letter. By understanding your rights, recognizing bad faith tactics, and understanding the broader landscape of insurance claim lawyer representation, you take the control back. If you are facing an unreasonable denial, do not walk away from what you are owed without getting a professional second opinion.

❓ FAQ

Can I claim bad faith if the adjuster was just rude to me?

No. Being unprofessional or rude is poor customer service, but it does not meet the legal threshold for bad faith. Bad faith requires proof that the insurer unreasonably failed to uphold their contractual duties, such as denying a valid claim without investigating it.

Are there any hidden costs if my lawyer loses the case?

While you typically do not owe attorney fees for their labor if you lose, some contingency contracts require you to cover specific “hard costs” like court filing fees or expert witness fees. You must clarify how case expenses are handled during your initial consultation.

When is it too late to involve an attorney in my claim?

It is generally too late once the statute of limitations in your state has expired, or if you have already signed a full and final release document in exchange for a settlement check. Never sign a liability release without a legal review if you feel you are still owed money.

Can I hire a lawyer if I already have a public adjuster?

Yes. If your public adjuster hits a wall because the insurance company flatly denies coverage or engages in bad faith, you can bring in an attorney. The attorney will handle the legal dispute while the PA’s valuation is used as evidence, though you should review your PA contract to understand how fees will be handled.

What happens if my insurance company demands an EUO?

An Examination Under Oath (EUO) is a formal, legally binding proceeding. Most standard policies require your cooperation. However, because your answers are under oath and can be used to deny your claim, having an attorney present to prepare and protect you is highly recommended.

Will filing a lawsuit make the insurance company drop my policy?

Insurers generally cannot cancel your policy mid-term simply as retaliation for hiring a lawyer or filing a lawsuit. They can, however, choose not to renew your policy at the end of its term based on your overall claim history and the risk you present.

Can my lawyer force the adjuster to reopen a claim I already settled?

This is extremely difficult. If you signed a release of liability when you accepted the settlement, reopening the claim is usually impossible unless your attorney can prove clear fraud or extreme, documented coercion by the insurer during the settlement process.

If I hire an attorney, do I still need to talk to the adjuster?

No. Once you officially retain an attorney and a letter of representation is filed, all communication must go through their office. If the adjuster attempts to call you directly, politely inform them that you have secured legal counsel and hang up.

Does a demand letter guarantee a settlement?

No. A demand letter outlines your legal arguments and the amount you are seeking, but the insurer may still refuse to pay. If they refuse, the attorney will use the leverage of the demand letter as the foundation to file a formal lawsuit.

How long does the discovery process take in an insurance lawsuit?

The discovery phase, where both sides exchange documents and take depositions, often takes several months. This is the longest part of litigation, but it is critical because it forces the insurance company to hand over internal notes and emails regarding your claim.

Most disputes start with scope or payout. These cover the earlier stages.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

Not every disputed claim needs a lawyer. Not every denial is just a negotiation problem.

- 5 patterns that signal your settlement is probably short

- Who the adjuster at your door actually works for

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When a denial rises to the level where legal action makes sense

- The option between negotiation and a lawsuit most homeowners skip

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.