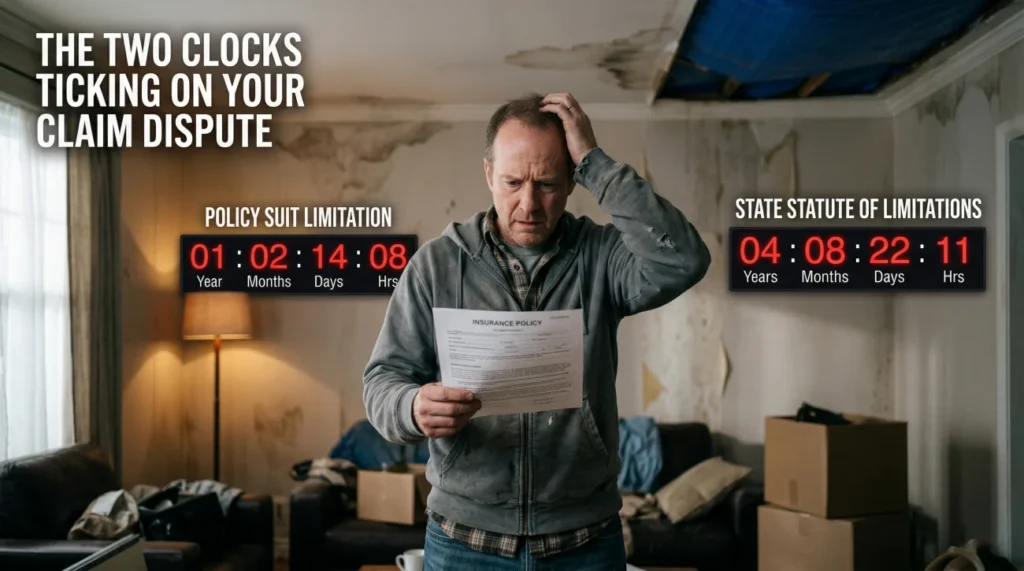

- There are two different deadlines you must track if you want to sue your insurer: the policy’s suit limitations clause and the state statute of limitations.

- The policy suit limitations clause is almost always shorter (typically one to two years) and usually overrides the state’s default timeline.

- Policy deadlines start ticking from the exact date the damage occurred.

- An ongoing investigation by your insurer does not automatically pause the legal clock. Many homeowners lose their right to sue while waiting for a final decision.

The Two Clocks Ticking on Your Claim Dispute

In my time reviewing property claim files, I have seen claims fall apart for dozens of reasons. But the most devastating losses do not come from bad coverage or tough adjusters. They come from homeowners missing a deadline they never knew existed. When you are trapped in an endless cycle of inspections, appeals, and requests for more documents, it is incredibly easy to lose track of time.

Note: If you are looking for the deadline to simply report your initial damage to your insurer, that is a completely different timeframe. You can find those details in our guide on the deadline to file a home insurance claim. This guide is specifically about the deadline to file a lawsuit after your claim has been disputed, delayed, or denied.

If you are considering legal action against your insurance company, you must understand that there are two separate clocks ticking in the background. Most homeowners assume state law gives them plenty of time to sue. The reality is that your insurance contract contains its own hidden deadline. Missing the shorter of the two clocks can permanently end your legal options.

Field Note: I routinely see files where a homeowner receives a final denial letter 14 months after a major hurricane, only to discover their policy required any lawsuit to be filed within 12 months of the storm. The insurer effectively ran out the clock during the ‘investigation’ phase, leaving the homeowner with zero legal recourse.

The Policy Suit Limitations Clause (The Hidden Deadline)

When you purchase a homeowners insurance policy, you agree to a massive contract. Buried within the “Conditions” section of that contract is a provision usually titled something like “Suit Against Us” or “Legal Action Against Us.” This is your suit limitations clause.

This clause dictates exactly how long you have to file a lawsuit against the insurance company if a dispute arises. In most standard policies, this window is incredibly short. It typically ranges from one to two years. More importantly, courts in most jurisdictions view this contract language as legally binding, meaning it overrides the state’s longer default deadlines.

When Does the Clock Actually Start?

This is where the vast majority of homeowners make a critical mistake. Logical thinking suggests that you cannot sue an insurance company until they have actually denied your claim or breached the contract. Therefore, you might think the clock should start on the date of the denial letter.

However, insurance policies do not follow that logic. Standard suit limitations clauses almost universally state that legal action must be started within one or two years “from the date of loss.” The date of loss is the exact calendar day the physical damage occurred.

Calculating your deadline to sue based on the date the insurance company finally issued your denial letter.

Calculating your absolute deadline to sue starting from the actual calendar date the physical damage occurred to your home.

If your policy gives you one year from the date of loss to sue, and the insurer takes ten months to investigate and finally deny the claim, you only have two months left to find an attorney, prepare a case, and file a lawsuit.

The State Statute of Limitations (The Default Deadline)

The second clock is the state statute of limitations. Every state has laws setting maximum time limits for filing different types of civil lawsuits. For property insurance disputes, you are generally dealing with deadlines for “breach of contract” (the insurer failed to pay what they promised) and sometimes “bad faith” (the insurer acted unreasonably).

State deadlines for breach of contract are usually generous. They often range from three to six years, and sometimes up to ten years depending on the jurisdiction. However, because your policy contains that shorter suit limitations clause we just discussed, the longer state deadline often becomes irrelevant.

The state statute of limitations typically only controls your timeline if:

- ✅ Your specific state has passed a law explicitly prohibiting insurance companies from shortening the state deadline via contract.

- ✅ Your policy does not contain a suit limitations clause (which is incredibly rare).

- ✅ The insurer acted in a way that legally “waived” their right to enforce their shorter policy deadline.

Furthermore, if your situation involves egregious insurer behavior, you might be looking at a bad faith claim. It is important to know that the state deadline for a homeowners insurance bad faith lawsuit is often categorized differently. It is sometimes treated as a “tort” rather than a contract breach, which means it might have a completely different, often shorter, statute of limitations than a standard contract dispute.

What Pauses or Resets the Clock?

Understanding both deadlines is only half the battle. The other half is knowing what can and cannot pause them. When an insurer keeps asking for more documents, schedules a third inspection, or simply goes quiet, homeowners often assume the legal deadline is paused. In legal terms, pausing the clock is called “tolling.”

Do not assume the clock is paused just because your claim is active. In many states, an ongoing investigation or a pending internal appeal does absolutely nothing to stop the suit limitations clock from ticking closer to zero. There are very few exceptions to this rule, such as statutory tolling temporarily applying if your state’s governor declares an official state of emergency after a widespread natural disaster.

| Event During the Claim | Does it Pause the Lawsuit Deadline? |

|---|---|

| Filing an internal appeal with the insurer | Usually No (unless state law explicitly allows it) |

| The insurer scheduling a new inspection | Usually No |

| Accepting a partial settlement payment | No, the clock for disputed items keeps running |

| Filing a complaint with the Dept of Insurance | Usually No |

The Appraisal Clause: A Different Path With Its Own Clock

Many homeowners who reach a stalemate with their insurer try to use the “Appraisal Clause.” This is an out-of-court dispute resolution process built into most policies, designed specifically for disputes over the amount of damage rather than coverage denials.

It is critical to understand that demanding appraisal does not automatically pause your deadline to file a lawsuit. If the appraisal process drags on for months, your suit limitations clock is still ticking. Homeowners frequently make the mistake of letting the appraisal process push them past their one-year or two-year anniversary, only to find out later that the insurer rejected the appraisal award and the homeowner can no longer sue to enforce it.

Warning Signs You Are Approaching a Deadline Trap

Insurance litigation deadlines are unforgiving. Do not rely on verbal assurances from your adjuster that “we have plenty of time to work this out,” as they are not obligated to warn you when your legal window is closing.

If any of these scenarios match your current situation, your legal rights are actively at risk:

- 🚩 The Anniversary Offer: The insurer suddenly offers a partial settlement just weeks before the one-year mark, hoping you sign a release and inadvertently waive your right to sue for the remainder.

- 🚩 The Endless Review: Your claim has been marked “under review” or “pending management approval” for over six months, and you are slowly approaching the anniversary of the damage.

- 🚩 The Distraction Tactic: The adjuster keeps requesting minor, repetitive documents like asking for the same contractor invoice for a third time as the date of loss anniversary looms closer.

- 🚩 The State Law Assumption: You received a denial, but you put off taking action because you googled your state’s breach of contract laws and assumed you have four to six years to figure it out.

What the Insurer Will Argue in Court if You Are Late

It is crucial to understand how strictly courts enforce these deadlines. If you file a lawsuit one day after your policy’s suit limitations clause expires, the insurance company’s attorneys will not argue about your roof or your water damage. They will immediately file a Motion for Summary Judgment based entirely on the expired deadline.

In the vast majority of scenarios, the judge will grant that dismissal. It does not matter if the insurance company was completely wrong to deny your claim. It does not matter if they acted terribly. If you miss the contractual window, you permanently forfeit your right to force the insurer to pay through the legal system.

Field Note: I once reviewed a file where a homeowner’s attorney filed suit exactly one week after the one-year anniversary of a storm. The insurer’s defense team did not argue the merits of the denied roof claim at all. They pointed to the expired suit limitations clause, and the judge dismissed the case immediately. The homeowner lost a valid $60,000 claim over seven days.

Protecting Yourself While Still Negotiating

A major reason homeowners miss deadlines is the fear that hiring an attorney or filing a lawsuit means going to trial and destroying any chance of a peaceful settlement. This is a misconception.

Filing a lawsuit is simply the mechanism to preserve your legal rights. In practice, filing a suit often forces the insurance company to move the file from a desk adjuster to their litigation department. This shift frequently leads to renewed, more serious settlement negotiations. You can continue to negotiate a settlement long after a lawsuit is filed. In fact, the overwhelming majority of property insurance lawsuits settle out of court. Filing the suit just ensures the clock does not run out while you are talking.

Final Steps and Deadline Verification

Your immediate action item is not necessarily filing a lawsuit today. It is verifying your exact drop-dead date. Locate your policy booklet, turn to the Conditions section, and read the “Suit Against Us” provision to establish your timeline.

Because the intersection of state statutes and policy contracts is highly dependent on local laws, no online guide can calculate your precise date for you. If you are within a few months of the anniversary of your damage and the claim is still unresolved, you must secure a legal evaluation. You can use a property damage attorney network to find a professional who will review your policy, confirm your exact dates, and help you keep your recovery options open.

❓ FAQ

🕵️ What if I did not discover the hidden damage until months later?

This is known as the “discovery rule.” In some cases, the clock starts from the date the damage became appreciable or discoverable. However, insurers fight this aggressively. You must document exactly when and how the hidden damage was found to support your timeline.

🌪️ Does applying for FEMA assistance pause my lawsuit deadline?

No. FEMA processes, federal grants, and state disaster relief applications operate entirely independently of your private insurance contract. Waiting for a FEMA response does not stop your policy’s lawsuit deadline from running out.

📅 Where do I find the lawsuit deadline in my policy?

You need to look at your full policy jacket, not just the declarations page. Look in the “Conditions” section for a clause titled “Suit Against Us,” “Legal Action Against Us,” or similar wording.

⚖️ Can an insurance company legally shorten my state’s statute of limitations?

Yes, in many states, courts allow private contracts like your insurance policy to enforce a shorter deadline than the general state law, as long as the shortened timeframe is considered reasonable by state standards.

💸 If I accept a partial payment, does it reset the lawsuit clock for the rest?

No. Accepting an undisputed payment for one part of the claim does not reset the deadline to sue over the disputed, unpaid portions. The original date of loss still governs the overall timeline.

🏛️ Do I have to sue before the deadline, or just hire a lawyer?

You must actually have the lawsuit filed in the court system before the deadline expires. Hiring a lawyer on the last day is not enough, as they need time to draft the complaint and officially file it.

🚨 What if the insurance company tricked me into missing the deadline?

If you can prove the insurer engaged in active fraud or deliberate misrepresentation specifically to run out the clock, a court might excuse the missed deadline. However, this is exceptionally difficult to prove and requires heavy legal intervention.

📝 Does filing a complaint with the Department of Insurance extend my time?

Filing a regulatory complaint with your state’s Department of Insurance generally does not pause or extend your contractual deadline to file a civil lawsuit against the carrier.

🔎 Is the deadline to sue different for a bad faith claim?

Yes, it can be. Bad faith is often treated as a tort rather than a breach of contract, meaning it falls under a different state statute of limitations. A lawyer must map out both timelines for you.

⏱️ How long does an attorney need to prepare before the deadline?

Attorneys prefer at least 30 to 60 days before a deadline expires to review your file, draft a proper complaint, and ensure all pre-suit requirements are met. Do not wait until the week your deadline expires to seek counsel.

Most disputes start with a payout disagreement. These cover the earlier stages.

- The claim lifecycle a PA or attorney works inside

- The policy language that determines what professional help can recover

- How damage classification affects what an expert can negotiate

- Whether the situation you have justifies bringing in outside help

- When a denial is the outcome a PA could have prevented

- What a public adjuster actually does inside a claim

- When the dispute has moved past what a PA can handle

Two paths, two different situations. These clarify which one fits yours.

- How to tell if your situation actually warrants hiring one

- The difference between the adjuster you hired and the one who showed up

- When water damage scope gaps make independent review necessary

- When fire damage complexity makes independent representation worth it

- When the gap between estimates is large enough to bring in a PA

- When bad faith makes legal action the only path that works

- PA, attorney, or appraisal clause: which path fits your denial

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.