- An insurance attorney takes over all communication with your insurer, legally preventing the adjuster from contacting you directly and protecting you from making accidental misstatements.

- Their primary role involves translating your policy exclusions, coordinating independent forensic experts, and leveraging the threat of litigation to force a fair settlement negotiation.

- Attorneys do not manufacture damage or override legitimate exclusions. Their job is to hold the insurer strictly accountable to the written contract you purchased.

The Black Box of Legal Representation in Property Claims

In my years of reviewing complex property claims, I have spoken to countless homeowners who feel trapped by a denied or severely underpaid claim. When the frustration peaks, the natural thought is to hire legal help. But most homeowners hesitate for one specific reason. They do not actually know what a home insurance claim attorney does on a day-to-day basis.

If you hire a contractor, you know they will show up with tools and lumber. If you hire a lawyer for an insurance dispute, the deliverables are invisible to the naked eye. It is easy to assume they just write a few angry letters on heavy cardstock and wait for a check to arrive. The reality of property insurance litigation is far more mechanical, highly strategic, and heavily reliant on evidence gathering.

Understanding the exact steps a lawyer takes after you sign a retainer agreement is the only way to evaluate if their involvement will actually add value to your situation. If you are still trying to figure out when legal help is necessary, it helps to start with a broad overview. But if you want to know what happens behind the scenes once an attorney takes over your file, this guide will walk you through their exact operational playbook.

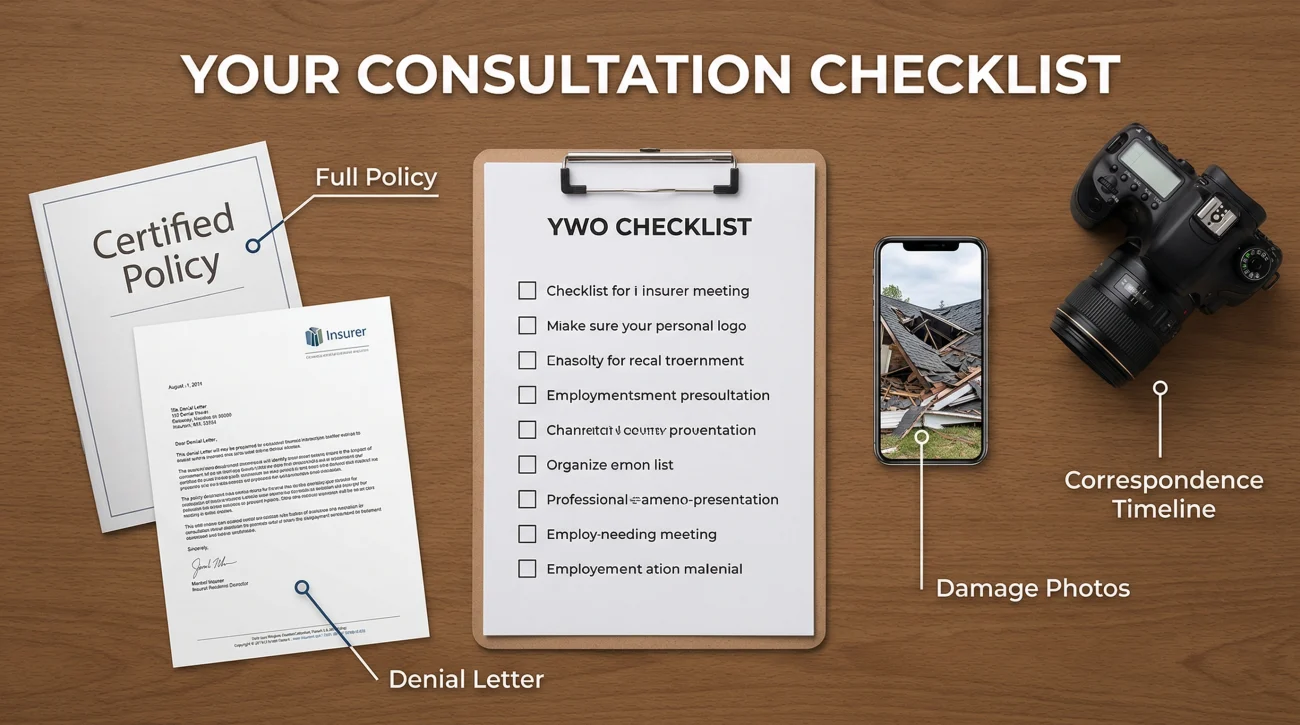

What to Prepare Before Your First Attorney Meeting

Before an attorney can step in and execute their playbook, they need the raw materials of your claim. Providing an organized file immediately changes how quickly an attorney can evaluate your situation. A practical checklist for your initial consultation should include:

- 👉 A certified copy of your full policy document (not just the summary page).

- 👉 The official denial or settlement letter from the insurer.

- 👉 A timeline of all correspondence, including emails and portal messages.

- 👉 Contractor repair estimates and any independent expert reports you have gathered.

- 👉 Clear before-and-after photos or videos of the property damage.

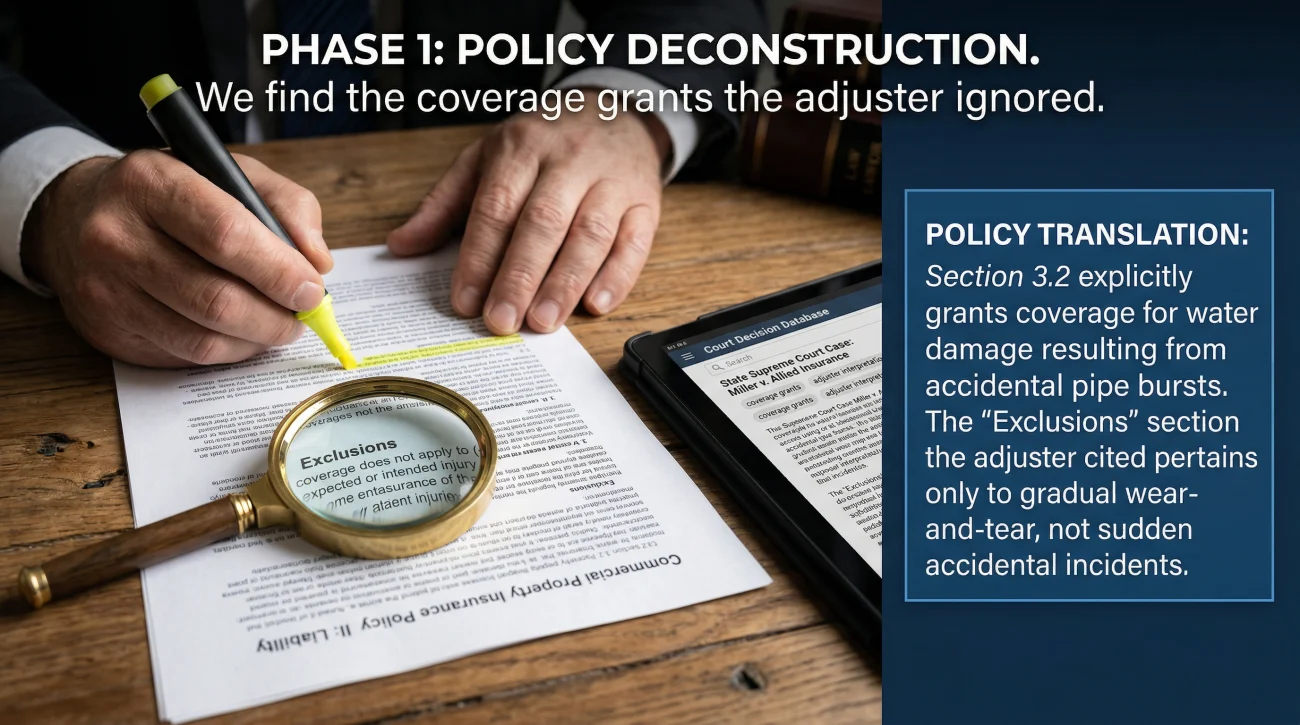

Phase One: Deconstructing the Policy Language

The very first thing an insurance attorney does is request a certified copy of your complete homeowners insurance policy. They do not look at the marketing brochure or the simple summary page. They read the policy as a binding legal contract, focusing heavily on the dense language governing exclusions, endorsements, and conditions.

Insurance companies often deny claims by citing a specific exclusion in your policy. For example, they might cite an exclusion for “earth movement” when your foundation cracks due to a plumbing leak. When a homeowner reads that denial letter, it looks official and final. When an attorney reads it, they look for the exceptions to the exclusion.

Field Note: A common pattern I see in denied claims is an adjuster applying a broad exclusion out of context. An experienced attorney will cross-reference the denial reasoning with prior court decisions to see if judges have previously struck down the insurer’s interpretation of that exact paragraph.

During this initial review, the attorney is specifically searching for coverage grants that the adjuster may have overlooked. They are also auditing your timeline to ensure no strict contractual deadlines, like the window to file a proof of loss, are about to expire.

Phase Two: The Communications Takeover

Once you formally retain an attorney, they will send a document to your insurance company called a Letter of Representation. This is a critical turning point in your claim. From the moment the insurer receives this letter, they are legally prohibited from contacting you directly regarding the dispute.

Every phone call, email, and letter from the adjuster or the insurance company’s legal department must go through your attorney. This communications takeover serves a highly specific purpose. It protects you from yourself.

Insurance adjusters are trained to ask questions that can inadvertently elicit answers harmful to your claim. A simple question like “When did you first notice the water spot?” can result in a denial if you casually answer “I think maybe a few months ago,” triggering a gradual damage exclusion. By taking over the communications, the attorney ensures that all information provided to the insurer is factually accurate, legally sound, and immune to twisting.

Writing emotional emails to the adjuster explaining how stressful the damage is and begging for a fair payout.

Sending sterile, fact-based correspondence citing specific policy provisions and demanding written justification for every deducted line item.

Phase Three: Coordinating Independent Assessments

A lawyer cannot argue a property damage claim based on legal theory alone. They need hard, physical evidence to counter the insurance company’s findings. Because attorneys are not structural engineers or roofers, a massive part of their job involves coordinating independent experts.

If your insurer claims your roof damage is due to age rather than a recent hail storm, your attorney will not just argue with them. They will hire an independent forensic meteorologist to pull weather data and an independent engineer to inspect the impact marks. If you have a fire claim and the insurer is refusing to clean your ductwork, the attorney will bring in an industrial hygienist to take air quality samples.

This is where the playing field begins to level. The insurance company relies on experts they pay to generate reports that often minimize damage. Your attorney builds an independent evidentiary file that challenges the insurer’s data point by point.

Phase Four: The Demand and Negotiation Process

Once the evidence is gathered and the policy has been analyzed, the attorney drafts a formal Demand Letter. This is not a polite request for reconsideration. It is a comprehensive legal document that outlines the facts of the loss, details the ways the insurer has breached the contract, presents the independent expert findings, and demands a specific dollar amount to settle the claim.

When an insurer receives a demand letter from a law firm, the file is usually pulled away from the standard desk adjuster and reassigned to a complex claims unit or the insurer’s internal legal counsel. This changes the entire negotiation dynamic.

A homeowner negotiating alone only has the leverage of filing a regulatory complaint. An attorney negotiates with the implicit and explicit leverage of impending litigation. The insurance company’s counsel has to calculate the risk of going to court, the cost of paying their own defense attorneys, and the potential exposure to bad faith penalties.

💡Pro Tip: Because attorneys typically work on a percentage basis, you should clearly understand how contingency fees work before signing a retainer. This ensures you know exactly how the final negotiated settlement will be divided.

| Legal Phase | Typical Timeline Expectations |

|---|---|

| Policy Review & Letter of Representation | 1 to 2 weeks |

| Expert Coordination & Inspections | 2 to 6 weeks |

| Demand Letter Drafting | 4 to 8 weeks |

| Negotiation & Mediation | Weeks to several months |

| Active Litigation (if required) | 12 to 24 months |

Signs the Attorney’s Involvement Has Changed the Dynamic

If you are wondering whether hiring a lawyer actually forces the insurance company to behave differently, the answer is usually visible within the first few weeks. Based on operational patterns, here are the clear signs that an attorney’s presence has disrupted the insurer’s original strategy.

- 🚩 Sudden communication improvements: The adjuster who previously ignored your emails for three weeks suddenly responds to your attorney within twenty-four hours of receiving the Letter of Representation.

- 🚩 Unprompted settlement increases: Shortly after your attorney sends a demand letter, the insurer issues a supplemental check “discovering” coverage for items they previously denied, hoping to close the file quickly.

- 🚩 Requests for new inspections: The insurer realizes their original adjuster’s report is too weak to hold up in court, so they demand a new inspection using a different, more credentialed engineering firm.

- 🚩 A shift in tone: The correspondence from the insurer shifts from dismissive and vague language to highly technical, careful legal phrasing, indicating their legal department is now reviewing all outgoing mail.

These shifts happen because the insurer recognizes that the cost of defending a poorly handled claim in front of a judge is often much higher than simply paying what is rightfully owed.

Phase Five: Mediation and Active Litigation

Many property damage claims resolve during the demand and negotiation phase. However, if the insurance company refuses to make a fair offer or stubbornly stands by an incorrect denial, the attorney will advise you on whether it is time to formally escalate.

Mediation as a Middle Step

Before plunging into a full lawsuit, cases frequently go through mediation. This is a formal settlement conference guided by a neutral third party. Your attorney will present the evidence and attempt to hammer out a binding resolution directly with the insurer’s decision-makers, without the extreme costs and prolonged timeline of a trial.

If mediation fails and a lawsuit is filed, the attorney’s role shifts into active litigation, which involves several highly structured procedural steps.

The Discovery Process

The attorney will use the court’s authority to force the insurance company to hand over their internal documents. This includes the complete claim file, internal emails between adjusters discussing your property, and drafts of the original repair estimates that may have been altered by management.

Depositions and Trial Experts

Your attorney will put the insurance adjusters, supervisors, and the insurer’s hired engineers under oath during depositions. The goal is to question them aggressively about their methods and why they made specific decisions on your file. Finding inconsistencies here is often what forces the insurer to settle.

If the case proceeds all the way to a courtroom trial, your attorney will put their own retained expert witnesses on the stand to testify regarding the true scope and cause of your damage.

Taking a case to this level requires a firm with actual courtroom experience. Knowing how to filter through marketing noise and vetting legal representation properly is vital, as an attorney who never goes to trial offers very little leverage.

Your Responsibilities During This Process

While the attorney takes over the heavy lifting, you are not entirely off the hook. A successful claim requires your ongoing cooperation in a few specific areas to ensure the legal strategy remains intact.

- 👉 Gathering continuous documentation: You must provide all requested photos, mitigation receipts, and historical repair records promptly when the attorney requests them.

- 👉 Maintaining silence: You must resist the urge to call or email your adjuster directly, even if you are frustrated by a delay in the process.

- 👉 Being available: You must make yourself available for independent inspections, formal Examinations Under Oath (EUOs), or depositions if litigation begins.

- 👉 Reviewing offers: The attorney handles the aggressive negotiations, but they cannot legally accept a settlement without your final, informed approval.

While the litigation phase showcases an attorney’s full capabilities, it is equally important to understand their practical limitations before you proceed.

What an Insurance Attorney Does Not Do

To have a successful working relationship with legal counsel, you must have realistic expectations about the boundaries of their power. There are several things a property damage attorney simply cannot do, no matter how skilled they are.

| Homeowner Expectation | The Operational Reality |

|---|---|

| The attorney will guarantee a specific dollar payout. | No ethical attorney will guarantee an outcome. They can only guarantee they will maximize the available legal leverage. |

| The attorney can make a clearly excluded peril covered. | If you do not have flood insurance and a river overflows into your home, an attorney cannot magically create coverage for that event. |

| The attorney will resolve the claim in a few weeks. | Litigation is slow. While a demand letter might trigger a quick settlement, a full lawsuit can easily take twelve to twenty-four months. |

| The attorney will fabricate evidence to boost the claim. | Attorneys rely on independent experts. They will not ask a contractor to inflate an invoice or lie about the cause of loss. |

Evaluating the Value of Legal Help

Knowing exactly what an attorney does removes the mystery from the process. They are not miracle workers. They are highly trained contract specialists who use procedural rules, independent evidence, and legal leverage to force insurance companies to honor their obligations.

If your claim is stalled, denied without a clear factual basis, or severely underpaid, the steps outlined above are exactly what is required to break the stalemate. You do not have to fight a massive corporation on your own. If your situation feels like it has moved beyond a simple customer service dispute, exploring a free legal consultation is the most practical way to find out if an attorney can change the trajectory of your claim.

❓ FAQ

⚖️ Will I have to go to court if I hire an insurance attorney?

Not necessarily. The vast majority of property insurance disputes are settled through negotiation or mediation after a lawsuit is filed, long before a trial actually takes place.

📞 Can I still talk to my adjuster after hiring a lawyer?

No. Once your attorney sends a Letter of Representation, the insurance company is legally required to route all communication through your legal counsel.

🔍 How does an attorney prove the insurance adjuster was wrong?

Attorneys do not rely on their own opinions. They hire independent experts, such as forensic engineers or industrial hygienists, to provide documented proof that contradicts the adjuster’s findings.

⏳ When does the attorney take over the insurance claim?

An attorney takes over the moment you sign the retainer agreement. They immediately notify the insurer, request the claim file, and assume control of all deadlines and correspondence.

📑 Does the attorney review my policy before taking the case?

Yes, reviewing the declarations page, exclusions, and endorsements is usually the first step an attorney takes during the initial consultation to determine if you have a viable case.

💡 What happens if the attorney cannot get the insurance company to pay?

If they cannot reach a settlement and the case is lost at trial, you typically owe the attorney nothing for their time under a standard contingency fee agreement.

📁 Can my lawyer see the adjuster’s internal notes?

Yes. If the case enters litigation, your attorney can use the discovery process to legally compel the insurance company to turn over their internal claim file and email communications.

🗣️ Who handles the settlement negotiation with the insurance company?

Your attorney handles all negotiations directly with the insurer’s legal team or complex claims unit. They will present settlement offers to you for your final approval.

📝 What is a demand letter in an insurance claim?

It is a formal legal document outlining the facts, the specific policy breaches by the insurer, and a required dollar amount to resolve the dispute.

🛑 Can an attorney fix a claim where I accidentally admitted fault?

It is difficult, but an attorney can review the context of your recorded statement. Sometimes they can prove your statement was taken under duress, or that the facts prove otherwise despite your initial misunderstanding.

Most disputes start with a payout disagreement. These cover the earlier stages.

- The claim lifecycle a PA or attorney works inside

- The policy language that determines what professional help can recover

- How damage classification affects what an expert can negotiate

- Whether the situation you have justifies bringing in outside help

- When a denial is the outcome a PA could have prevented

- What a public adjuster actually does inside a claim

- When the dispute has moved past what a PA can handle

Two paths, two different situations. These clarify which one fits yours.

- How to tell if your situation actually warrants hiring one

- The difference between the adjuster you hired and the one who showed up

- When water damage scope gaps make independent review necessary

- When fire damage complexity makes independent representation worth it

- When the gap between estimates is large enough to bring in a PA

- When bad faith makes legal action the only path that works

- PA, attorney, or appraisal clause: which path fits your denial

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.