- Filing a claim is not just an administrative task; it is your first official recorded statement to the insurance company.

- Filing through an online portal allows you to control your narrative and avoid misspeaking, while phone filing creates an immediate audio record.

- Stick to the facts: state the date you discovered the damage and what you physically see. Never speculate about the cause or the timeline.

- Do not guess repair costs or admit to maintenance delays during your initial filing call.

- Ask if a “Sworn Proof of Loss” form is required, as missing this strict deadline can severely impact your claim.

The First 48 Hours: Why the Filing Call Determines Your Claim’s Trajectory

Filing a home insurance claim sounds like a simple, straightforward step. Damage happens, you call your insurance company, you report it, and you wait for an adjuster. But in reality, the moment you initiate that claim, you are officially on the record.

I have reviewed hundreds of claim files from the operational side, and I can tell you that the trajectory of a claim is almost always set in the first 48 hours. The initial report is not just a customer service interaction. It is a data-gathering exercise for the insurer. The words you use, the timeline you provide, and the details you volunteer are immediately logged into your file.

Short field observation from claims experience: I frequently see claims denied not because the damage was excluded, but because a stressed homeowner misspoke during the initial filing call. They guessed that a pipe ‘must have been leaking for months’ instead of simply stating they discovered water that morning. That one sentence shifted the claim from a covered sudden event to an uncovered maintenance issue.

Before you pick up the phone or log into your portal, you need to understand the mechanics of the filing act itself. This guide breaks down exactly how to file a home insurance claim step by step, what to say, what absolutely not to say, and how to protect your scope before the adjuster even arrives.

Call vs. Online Portal: Which Filing Method Should You Use?

Most major insurance carriers today offer two ways to formally open a claim: calling their 24/7 claims hotline or submitting a form through their online portal or mobile app. Homeowners often ask me which one is better, and the answer depends heavily on the severity of your damage and your ability to control your narrative under stress.

Filing by Phone

When you call the claims department, you are speaking to an intake representative. Their job is to open the file and ask a series of scripted questions. Keep in mind that these phone calls are almost always recorded. This creates a verbal statement right out of the gate.

Phone filing is typically necessary for severe, catastrophic losses where your home is uninhabitable and you need an immediate emergency advance for temporary housing. However, for standard claims, the phone call introduces the risk of human error. When you are stressed, it is easy to ramble, over-explain, or answer leading questions inaccurately.

Filing via Online Portal

Filing online removes the pressure of a live conversation. You are presented with text boxes and drop-down menus. This gives you time to review your words carefully before hitting submit. You can ensure your dates are accurate and your descriptions are strictly factual without being pushed by a representative’s questions.

| Filing Method | Pros | Cons |

|---|---|---|

| Online Portal / App | Time to review answers; no pressure from live agent; exact written record. | May delay immediate emergency housing assistance for catastrophic events. |

| Phone Call | Immediate response; can trigger emergency living expenses faster. | Recorded verbal statement; high risk of misspeaking under stress; leading questions. |

💡 Pro Tip: For standard water damage, minor fire, or storm claims where the home is still safe to occupy, I often recommend filing through the online portal. It allows you to report the loss promptly while keeping your initial statement concise and controlled.

Exactly What to Say When Filing Your Claim

Whether you are typing into a portal or speaking to an agent, your goal during the initial filing is simple: establish the date of loss and report the physical facts. You are not required to provide a comprehensive engineering assessment. You are only required to report the damage.

I advise homeowners to stick to a very specific communication formula when answering the “what happened” question.

[Date of discovery] + [What you observed physically] + [Any emergency action taken]

Here are examples of how to apply this formula safely:

“On October 12th at 8:00 AM, I discovered standing water on my kitchen floor and visible damage to the baseboards. I immediately shut off the main water valve to prevent further damage and contacted a plumber to identify the source.”

“Following the severe storm on the evening of May 4th, I observed missing shingles from my roof and a water stain developing on my upstairs bedroom ceiling. I have moved my personal belongings out of the room to prevent further damage.”

This formula provides the exact information the intake representative needs to open your file and assign an adjuster. By keeping your initial report concise and restricted strictly to your direct physical observations, you establish a clear, factual starting point for the claim.

What Not to Say: The Words That Complicate Claims

Knowing what not to say is often more important than knowing what to say. Insurance policies are contracts based on specific language, and using the wrong terminology casually can trigger policy exclusions. Here are the most common missteps homeowners make during the filing process.

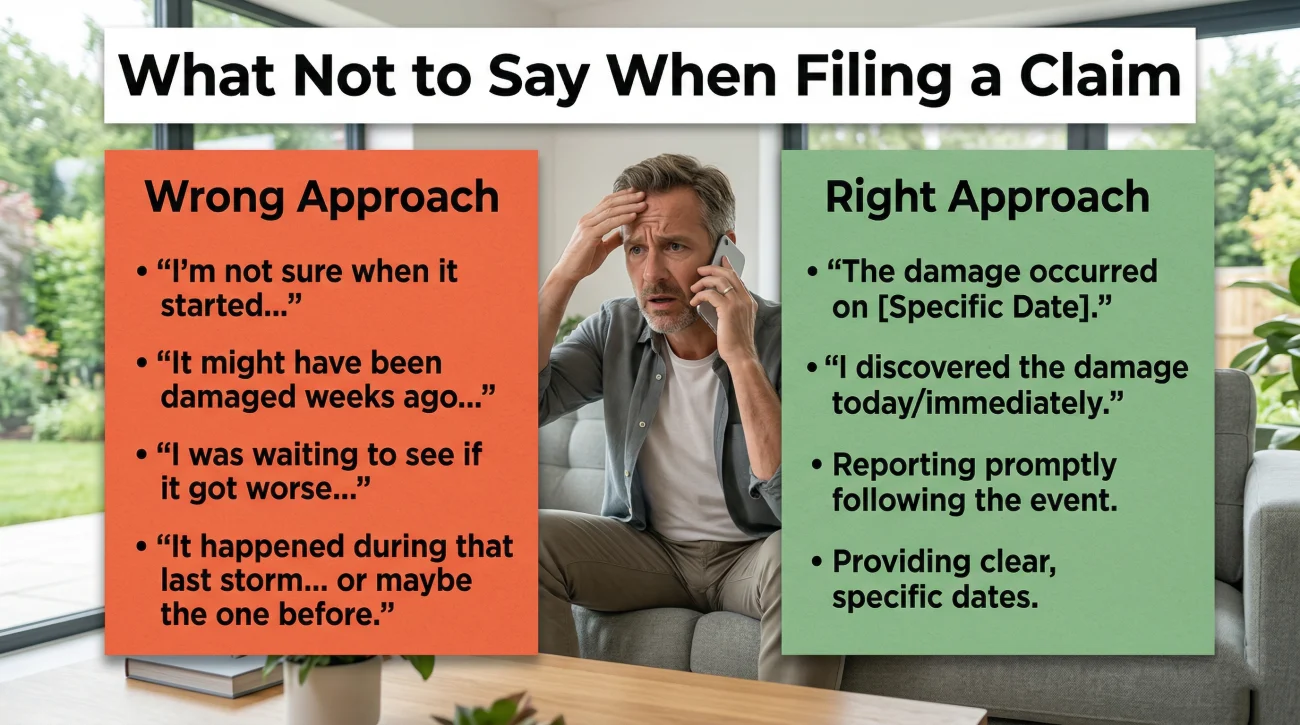

Do Not Speculate on the Timeline

Insurance covers sudden and accidental damage. It generally does not cover long-term wear and tear, deferred maintenance, or gradual leaks. If you guess that a problem has been happening for a long time, you are giving the insurer a reason to investigate a denial based on delayed discovery.

“I think this pipe behind the wall has probably been leaking for a few weeks before it finally broke through the drywall.”

“I discovered the water damage on the drywall today at 4:00 PM.”

Do Not Estimate Repair Costs

During the filing call, a representative might ask, “How much do you think the damage will cost to repair?” Never guess. If you throw out a number like “$2,000” because it sounds like a lot of money to you, that note goes in your file. When your actual contractor estimate comes back at $15,000 because of hidden structural damage, the insurer will look at your initial low guess with suspicion. Insurers use your initial estimate to set a preliminary reserve, the pool of money set aside for your file. If you anchor that reserve artificially low, it becomes a significant administrative hurdle for the adjuster to request authorization for a much higher payout later.

The correct answer is always: “I have not had a professional scope assessment yet, so I cannot provide an accurate estimate at this time.”

Do Not Volunteer Information About Delayed Maintenance

Do not use the filing call to confess your home improvement sins. Saying things like, “I knew that roof was getting old and I meant to replace it last summer,” or “That toilet has been acting weird for a year,” introduces maintenance neglect into the file. Stick to the facts of the sudden event that caused the damage you are reporting right now.

Documenting the Act of Filing Itself

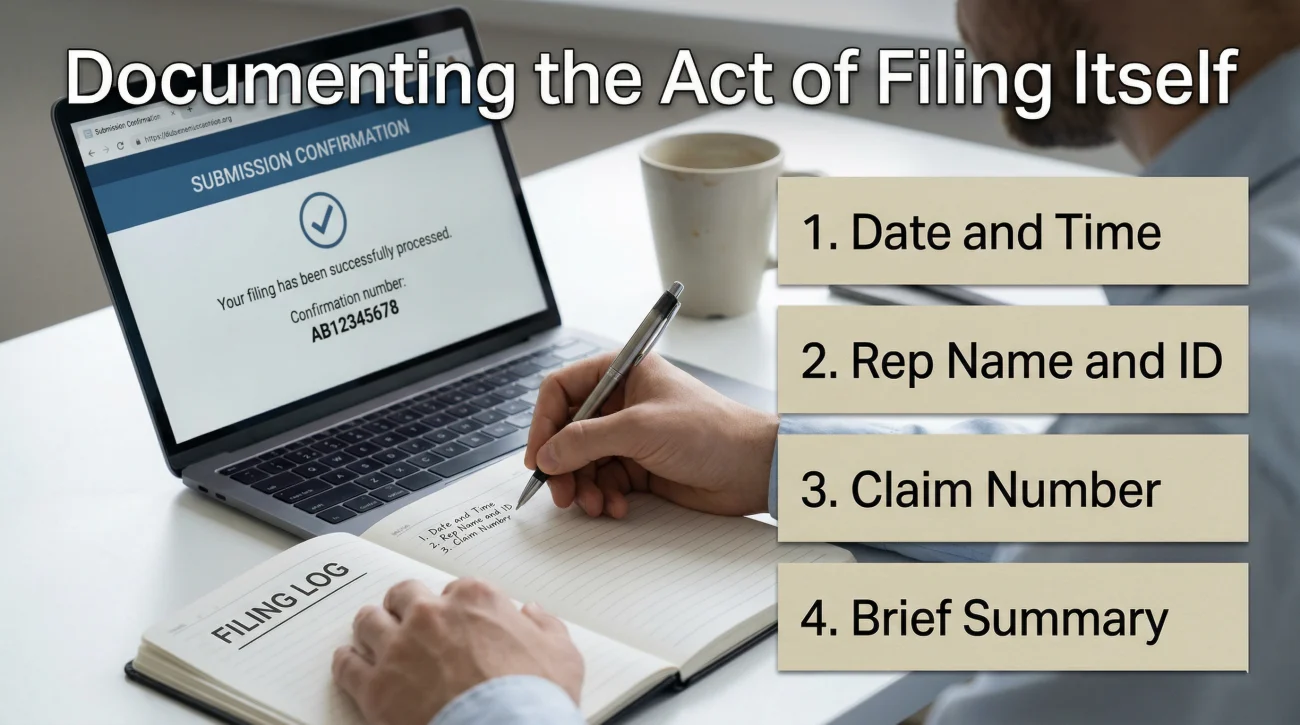

The moment you hang up the phone or hit submit on the portal, you need to create your own record of the interaction. Insurance claims departments process thousands of reports daily, meaning files can get lost in the system, transferred between multiple adjusters during a shift change, or delayed without notice. Your personal documentation of the filing act is your protection against administrative errors.

If you file by phone, keep a notebook dedicated solely to your claim. Immediately after the call, log the following:

- 👉 The exact date and time of the call.

- 👉 The full name and ID number of the intake representative.

- 👉 The claim number you were provided.

- 👉 A brief summary of exactly what you reported.

If you file online, take a screenshot of the final submission page showing your claim number and the date. Save any confirmation emails you receive in a dedicated digital folder. This level of organization signals to the insurer that you are an engaged, detail-oriented policyholder, which often leads to more respectful communication throughout the process.

Warning: Be sure you have started documenting home damage for your insurance claim visually before you make this call. You want photos of the immediate aftermath secured before the insurer begins asking for evidence.

The Sworn Proof of Loss Form: The Deadline You Cannot Miss

When discussing how to file a home insurance claim, many guides skip one of the most critical documents: the Sworn Proof of Loss. This is not the initial report you make on day one. It is a formal, legal document that lists all damaged property, the extent of the damage, and the exact dollar amount you are claiming.

Many standard homeowners policies require you to submit this document within a specific timeframe after the loss occurs – typically 60 days, though you must check your specific policy documents to confirm your exact window. Missing the Proof of Loss deadline is one of the few ways an insurer can completely deny an otherwise valid claim based purely on a technicality.

During your initial filing call, always ask the representative:

“Are you requiring a Sworn Proof of Loss form for this claim, and if so, what is my exact deadline to submit it?”

Document their answer. Do not confuse a contractor’s estimate or the adjuster’s initial report with a Proof of Loss. It is a specific form provided by the insurer that must be signed and often notarized.

What Happens Immediately After You Hit Submit

Once your claim is officially filed, a cascade of internal processes begins at the insurance company. Here is what you should expect in the first few days.

First, an internal claim number is generated. This number will be required on every piece of correspondence moving forward. Next, the file is routed to an adjusting team. Here is an operational reality most homeowners do not know: filing late on a Friday afternoon often means your claim sits in an unassigned queue until Monday morning. Filing on a Tuesday morning typically results in much faster routing. Furthermore, if you are filing during a regional catastrophe (like a major hurricane), that standard 24 to 48-hour adjuster assignment window can stretch into weeks.

Simultaneously, the investigation clock starts. Insurers are typically required to acknowledge, investigate, and decide on a claim within strict timelines set by their regulatory obligations. Your filing date is day zero for these timelines.

Finally, if your home is actively taking on water or exposed to the elements, this is the window where you must fulfill your duty to mitigate. Securing a tarp or extracting water is required to prevent secondary damage. Taking action on emergency home repairs before your insurance claim adjuster arrives is expected, provided you document the scene thoroughly before the cleanup begins.

Signs Your Initial Filing Call Created a Complication

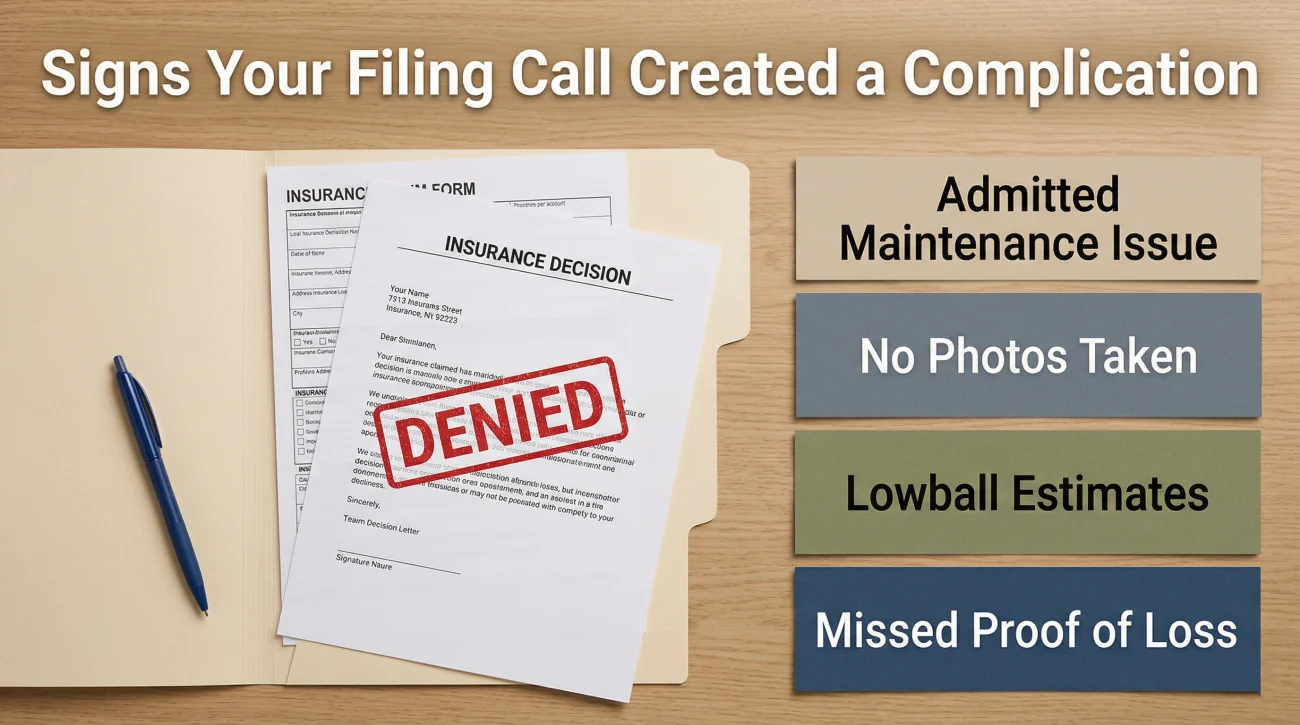

The stress of discovering property damage often causes homeowners to rush the filing process. Unfortunately, rushing leads to missteps that can haunt the claim for months. You might be dealing with a complicated filing situation if you are experiencing any of these signs:

- 👉 You used language that categorized the damage as a maintenance issue rather than a sudden event, shifting the focus of the investigation.

- 👉 You filed the claim before gathering any photographic evidence, and cleanup crews have already destroyed the original scene.

- 👉 You submitted initial, lowball contractor estimates during the filing process that did not account for hidden structural damage, and the insurer is now locking you into that low number.

- 👉 The insurer did not mention a Proof of Loss form, and you are nearing your policy’s deadline without having submitted one.

If you realize you misspoke or rushed the process, do not attempt to call back and casually “change your story.” This often looks like insurance fraud to an investigator. Instead, you need to rely on objective, written documentation to clarify the facts of the loss.

Final Thoughts Before You Make the Call

Filing your claim sets the frame for the entire investigation. The decisions made in that first interaction, and the words used to describe your loss, are much harder to undo than most homeowners realize. If you feel unprepared to make that initial report, you do not have to do it alone.

To understand where this initial step fits into the broader picture of your recovery, review the full home insurance claim process steps so you know exactly what is coming next.

If you are dealing with a large, complex loss, such as a major fire or extensive hidden water damage, you may want professional representation before you ever call the insurer. Getting an independent assessment of your scope, and understanding how a public adjuster differs from the insurance adjuster assigned to your file, can protect your position and ensure the claim is framed correctly from day one.

❓ FAQ

📞 How do I actually file a home insurance claim?

You can file a claim by calling your insurance company’s 24/7 claims hotline, logging into your online customer portal, or using the insurer’s mobile app. Online filing is often best for minor claims to control your written statement.

💻 Is it better to file a home insurance claim online or by phone?

Online is generally safer for standard claims because it prevents you from misspeaking on a recorded line. Phone filing should be used for catastrophic emergencies where you need immediate temporary housing assistance.

🗣️ What should I say when calling my insurance company about a claim?

Keep it factual. State the exact date and time you discovered the damage, describe what you physically see (e.g., “water on the floor”), and mention any emergency mitigation steps you have taken. Do not speculate on the cause.

🤐 What should you absolutely not say to home insurance?

Never guess the cost of repairs, never speculate that a leak has been happening for a long time, and never admit to delaying maintenance. Stick only to the sudden event you are reporting.

⏱️ How long does it take to file a home insurance claim?

The actual act of filing takes about 10 to 15 minutes online or over the phone. However, gathering your initial photos and emergency details before you make the call may take an hour or two.

📝 What is a proof of loss form for home insurance?

It is a formal, sworn legal document detailing the scope of your damage and the dollar amount you are claiming. It usually has a strict submission deadline set by your policy.

💧 How to file a home insurance claim for water damage specifically?

Shut off the water, document the standing water with photos, and file the claim stating a “sudden discharge of water.” Hire a mitigation company immediately to dry the area, but do not throw away the broken pipe.

📅 What happens right after you file a home insurance claim?

You will receive a claim number. Within 24 to 48 hours, an adjuster will contact you to schedule an on-site inspection, and the legal clock for the insurer to investigate your claim begins.

📸 Do I need all my photos ready before I file the claim?

You do not need a complete catalog of every damaged item, but you should take wide and close-up photos of the immediate damage scene before you start cleaning up or make the filing call.

🛑 Can I cancel a home insurance claim if I change my mind right after filing?

You can usually withdraw a claim, but the fact that you filed it will still likely show up on your CLUE report as an inquiry or zero-pay claim, which can still impact your future insurance rates.

Filing is just the beginning. These cover what the rest of it looks like.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

That gap is common and usually closeable. These explain how.

- 5 patterns that signal your settlement is probably short

- Who the adjuster at your door actually works for

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When a denial needs legal leverage, not just negotiation

- Four paths to fight a denial, including one most homeowners miss

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.