- Your insurance policy legally requires you to perform emergency repairs to prevent further damage, known as the duty to mitigate.

- There is a massive difference between emergency stabilization (like tarping a roof) and permanent repairs (like installing new shingles). Permanent repairs before an inspection can destroy evidence and ruin your claim.

- Always take extensive photos and videos of the damage, including high-water marks and exact points of failure, before anyone alters the scene.

- Emergency mitigation costs are typically reimbursable, so keep every receipt and insist on highly detailed invoices from contractors.

- Never sign an Assignment of Benefits (AOB) contract under emergency pressure, as this signs away your claim rights to a contractor.

The First 24 Hours: Claim Survival vs. Claim Sabotage

You have just experienced a sudden disaster. Maybe a pipe burst flooding your kitchen, a tree crashed through your roof, or a fire left your living room exposed to the elements. Your immediate instinct is to fix it. You want to clean up the mess, rip out the ruined materials, and make your home safe again. I understand that panic completely.

However, as someone who reviews property claims and scope disputes daily, I need you to pause. The actions you take in the first few hours after a loss will either protect your insurance claim or give the adjuster the exact justification they need to deny it. You are walking a very thin line between fulfilling your responsibilities and inadvertently destroying the evidence of your own loss.

In my field experience, the most heartbreaking claim denials do not happen because the damage was excluded. They happen because a well-meaning homeowner threw away the burst pipe, ripped out all the wet drywall, and painted the walls before the insurance company could verify what actually happened.

You must act fast, but you must act strategically. Here is exactly what your policy requires right now, what will sabotage your settlement, and how to navigate this chaotic emergency phase.

When to Call the Insurer vs. the Contractor

Many homeowners freeze, wondering if they need the insurance company’s permission before calling a plumber or a water extraction crew. You do not need their permission to stop active damage, but you do have a duty to notify them promptly.

The best practice is simultaneous action. If a pipe bursts, shut off the water and call an emergency mitigation company immediately. While they are on their way, call your insurance claims hotline to report the loss. Tell the representative factually: “I have suffered sudden water damage, the water is off, and a mitigation team is en route to extract the standing water.”

This approach establishes your timeline on a recorded line, proves you are actively fulfilling your duty to protect the property, and gets the claim started without delaying critical stabilization work.

The Duty to Mitigate: What Your Policy Actually Requires

Many homeowners are terrified to touch anything after a disaster because they fear voiding their coverage. The reality is exactly the opposite. If you read the fine print of almost any standard homeowners insurance policy, you will find a clause outlining your “duties after a loss.”

One of the most critical duties is the requirement to mitigate your damages. This means you are contractually obligated to take reasonable steps to protect your property from sustaining further damage.

Key Point: Failing to perform emergency mitigation gives the insurance company grounds to deny coverage for any additional damage that occurs after the initial event.

If wind blows off a section of your shingles and you do nothing about it, the insurance company will likely cover the initial roof repair. However, if it rains three days later and ruins your hardwood floors because you failed to put a tarp over the exposed roof, the insurer can rightfully deny the interior water damage claim.

The insurer expects you to stabilize the situation. Understanding the boundary between stabilization and premature rebuilding is the secret to a smooth claim process.

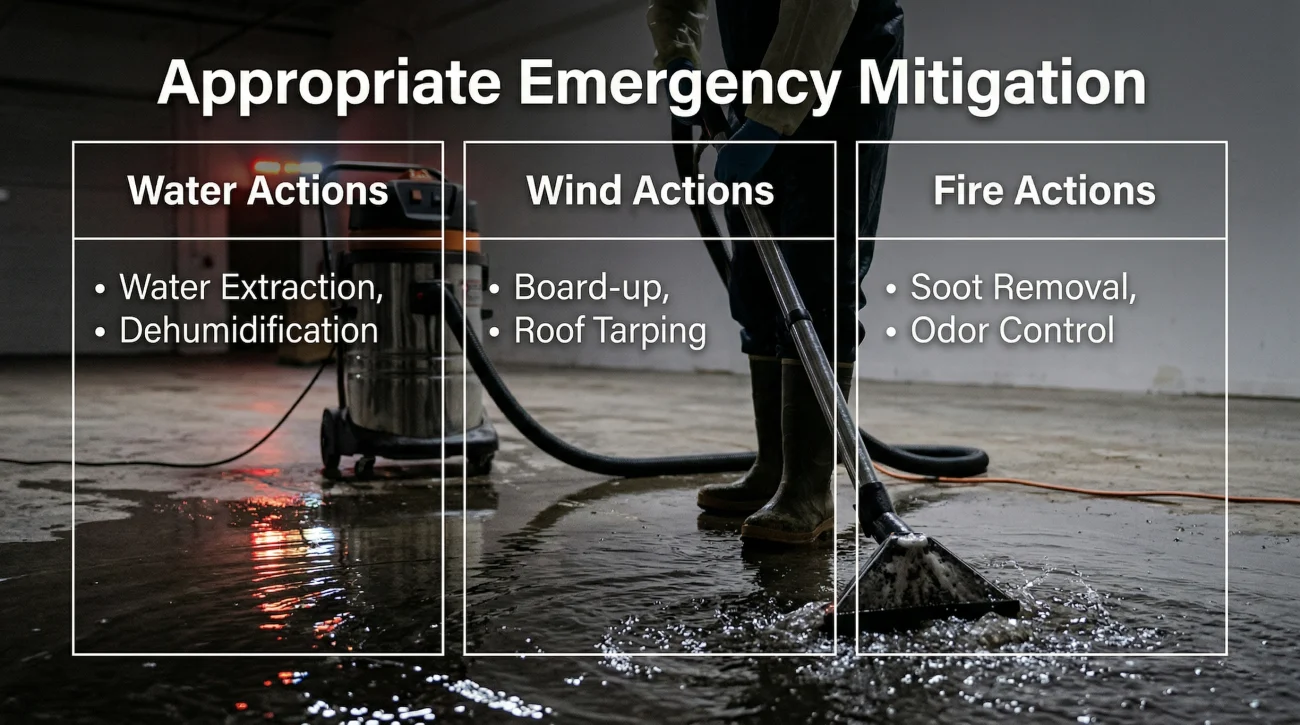

What Counts as Appropriate Emergency Mitigation

When I advise homeowners on emergency steps, I always focus on stopping the bleeding. Your goal is simply to freeze the scene so the damage does not spread. Here are the most common, expected, and appropriate emergency actions you should take immediately.

Emergency Actions for Water Damage

- 💧 Shut off the water source: Find your main water valve and turn it off immediately to stop the flow.

- 💧 Extract standing water: Using a wet vacuum or calling an emergency mitigation company to extract pooling water is highly recommended. Mold begins to form within 24 to 48 hours in damp conditions, making immediate extraction a critical mitigation step.

- 💧 Move unaffected property: Relocate dry furniture, rugs, and electronics away from the wet zone.

Emergency Actions for Roof and Wind Damage

- 🌪️ Tarp the roof: Hiring a contractor to secure a heavy duty tarp over missing shingles or structural penetrations is the textbook definition of proper mitigation.

- 🌪️ Board up broken windows: Securely boarding up broken glass prevents rain entry and deters theft.

Emergency Actions for Fire and Smoke

- 🔥 Secure the perimeter: Boarding up doors and windows and placing temporary fencing around a severely burned structure is required to prevent liability issues and looting.

- 🔥 Winterize plumbing: If the fire leaves your home without heat during the winter, draining your pipes prevents a secondary freezing and bursting disaster.

Notice what is missing from these lists. There is no replacing of materials, no painting, and no structural rebuilding. It is pure preservation.

Will Insurance Reimburse My Emergency Repair Costs?

A frequent question I hear is whether homeowners have to pay out of pocket for these emergency steps. The answer is yes, initially, but the costs are typically fully reimbursable under your policy.

Most standard policies have a provision that covers the reasonable cost of emergency measures taken to protect covered property. If you pay a roofer $500 to tarp your roof on a Sunday night, that $500 should be added to your total claim payout.

💡 Pro Tip: Adjusters will heavily scrutinize emergency invoices. A receipt that just says “Emergency Service: $2,500” is a red flag. You must demand an itemized invoice from your emergency contractor.

When you hire an emergency water extraction crew or a board up service, require them to document exactly what they are doing. Below is a template I recommend my clients use when requesting an invoice from an emergency contractor.

Hello [Contractor Name],

Before you finalize the invoice for the emergency stabilization work at my property, please ensure it includes the following details for my insurance adjuster:

1. The exact date and time the emergency work was performed.

2. A brief description of the cause of loss you observed upon arrival.

3. An itemized breakdown of labor hours, equipment used (e.g., number of dehumidifiers and days running), and materials consumed.

4. Photos of the damage taken prior to your mitigation efforts.

Thank you for helping me keep my claim file accurate.

Emergency Contractor Red Flags and the AOB Trap

During major weather events, aggressive emergency contractors often appear at your door. While you need fast help, you must remain in control of your claim. Be extremely cautious if a contractor demands you sign a complex document before providing an itemized estimate.

The biggest danger in the emergency phase is the Assignment of Benefits (AOB) contract. If a water mitigation crew asks you to sign an AOB at midnight, they are legally asking you to sign over your claim rights to them. They can then bill your insurance company directly. If the insurer refuses to pay their inflated rates, the contractor can sue you for the difference or place a lien on your home. Never sign an AOB under emergency pressure. Ask for a standard work authorization that covers only the emergency mitigation scope, not an assignment of your insurance benefits.

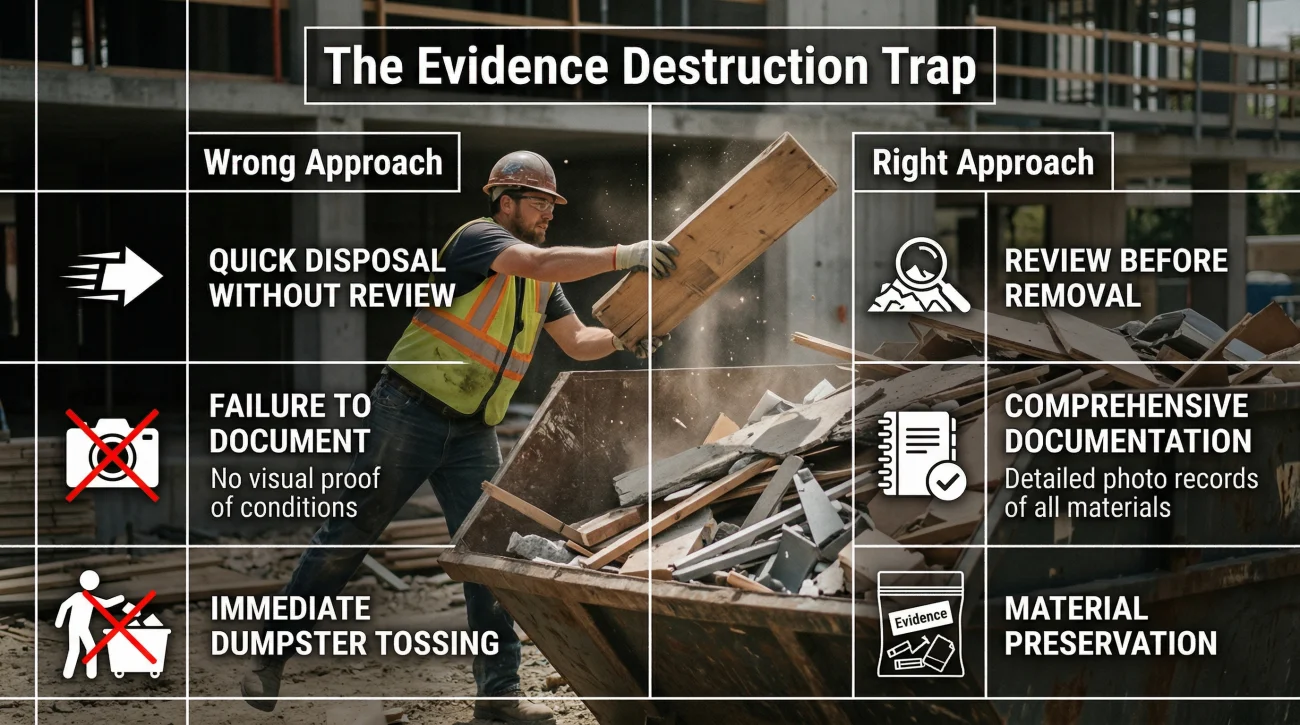

The Evidence Destruction Trap: The Danger of Over-Mitigation

This is where smart homeowners accidentally ruin their own claims. In the rush to clean up, they engage in over-mitigation. Over-mitigation is when you remove damaged materials or complete full repairs, effectively eliminating the physical evidence the adjuster needs to verify the scope of the loss.

Adjusters operate on a very strict rule. If they cannot see it, they will not pay for it. For instance, if you throw away a ruined custom vanity and replace it with a cheap stock cabinet before the inspection, the adjuster will write the estimate based on the cheap stock cabinet they see. You just lost thousands of dollars in legitimate replacement value simply because the physical proof is sitting in a landfill.

Never throw away the part that failed. If a supply line to your toilet bursts, keep the broken hose in a plastic bag. If a window shatters, keep a piece of the frame showing the impact point. This loss of proof has severe consequences. Spoliation of evidence is a primary defense used by insurers to deny coverage entirely.

The Golden Rule Before Touching Anything

Before you turn off the water, before the roofer lays the tarp, and before the mitigation crew brings in their fans, you must document the scene. Documentation is the only way to prove what existed before the cleanup altered the environment.

Do not just take random pictures. You need to capture specific details that adjusters look for. Photograph the high-water marks on the drywall before the water recedes. Take macro shots of the manufacturer labels and serial numbers on ruined appliances. Get clear images of the exact point of failure, whether that is a split washer hose or a cracked window seal, before anyone moves it.

For the exact steps on capturing this evidence properly, review my detailed checklist for securing damage evidence.

You want to establish a bulletproof timeline. Use this simple sequence to ensure you never lose the narrative of your claim.

[Video walk-through of active damage] + [Wide and macro still photos] + [Emergency contractor written assessment] + [Retained physical samples]

What If You Already Started Permanent Repairs?

If you have already jumped the gun and paid a contractor to install new drywall or lay down flooring before calling your carrier, you are now fighting an uphill battle. You need to quickly understand the specific rules around filing an insurance claim after repairs are already completed to see if your remaining documentation is strong enough to salvage a payout.

To grasp why the insurer demands an inspection first, it helps to zoom out. For a complete understanding of how this initial emergency phase fits into how the standard home insurance claim process unfolds, reviewing the entire timeline can reduce a lot of your current anxiety.

Signs Your Emergency Actions Have Complicated Your Claim

It is critical to recognize when the insurance company is using your emergency actions or premature repairs against you. You should immediately reevaluate your strategy if you notice any of these warning signs.

- ⚠️ The adjuster is actively disputing damage that was cleaned up or removed before their physical inspection.

- ⚠️ Your insurer is sending letters claiming that subsequent damage occurred after the original event due to your lack of timely mitigation.

- ⚠️ You incurred thousands of dollars in emergency repair costs, but your contractor failed to provide the necessary itemized documentation, and the insurer is refusing to reimburse you.

- ⚠️ A contractor pressured you into signing an assignment of benefits contract during an emergency midnight service call.

Final Thoughts on Balancing Speed and Strategy

The emergency window is where property claims are either won or lost. Your prompt mitigation protects the integrity of the claim, while overzealous repair completely undermines it. The bridge between these two extremes is meticulous documentation. Tell your insurer exactly what you are doing, photograph why you are doing it, and never throw away the evidence.

If you are still weighing the financial pros and cons of moving forward with your carrier, read our full framework on deciding whether to file a home insurance claim to ensure the math actually makes sense.

However, if emergency decisions have already complicated your claim scope, or if the insurer is accusing you of destroying evidence, you should not fight that battle alone. Getting an independent review of your fire or severe damage claim from a licensed public adjuster can help assess what recovery is still legally available based on the documentation you preserved.

❓ FAQ

Can I do repairs before the insurance adjuster visits?

You have the right to hire professionals to secure the property immediately, like water extraction or boarding windows. However, hold off on any cosmetic or structural rebuilding until the adjuster has formally approved the scope of work.

Will home insurance pay for my temporary repairs?

Typically, yes. Standard policies reimburse reasonable expenses incurred for emergency measures taken to protect the property from further covered damage. You must keep all itemized receipts.

What should I tell my insurance company when I call to report the emergency?

Keep it factual. State the date, what you observed, and that you are actively taking emergency mitigation steps to stop further damage. Do not guess about the repair costs, admit fault, or speculate on the exact cause if you are unsure.

What happens if I throw away damaged items before the adjuster comes?

Throwing away damaged items destroys physical evidence. The insurer may deny compensation for those items because they cannot verify the damage or the item’s prior condition.

Can I hire my own emergency water extraction company?

Yes, you have the right to hire your own mitigation contractor. You do not have to wait for or use the insurer’s preferred vendor network to handle an immediate emergency.

Do temporary repairs negatively affect my insurance claim?

No, proper temporary repairs strengthen your claim by showing you fulfilled your contractual duty to mitigate. Only permanent repairs done prematurely will negatively affect the claim.

Should I board up broken windows myself or hire someone?

You can do it yourself if it is safe, and your materials will be reimbursed. If it requires specialized equipment or is unsafe, hiring a professional board-up service is recommended and usually covered.

What is considered “mitigation of damages” in home insurance?

It is the policyholder’s legal responsibility to take immediate, reasonable actions following a loss to prevent the damage from spreading or worsening, such as turning off the main water valve.

How do I prove what my home looked like before the emergency cleanup?

The only reliable way is through extensive photographic and video evidence taken immediately upon discovering the damage, before any water is extracted or debris is moved.

Can the insurance company deny my claim if I clean up the water too fast?

They will not deny the entire claim simply because you extracted the water. However, if you tear out drywall and discard carpet without photographing the extent of the damage first, they will likely underpay or deny those specific line items because they cannot verify the materials or the high-water mark.

Filing is just the beginning. These cover what the rest of it looks like.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

That gap is common and usually closeable. These explain how.

- 5 patterns that signal your settlement is probably short

- Who the adjuster at your door actually works for

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When a denial needs legal leverage, not just negotiation

- Four paths to fight a denial, including one most homeowners miss

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.