- Receiving a settlement check that doesn’t cover your contractor’s quote is incredibly common and usually fixable through the formal supplement process.

- Most gaps happen because adjusters use standardized pricing software (Xactimate) that often lags behind local market labor rates, or because they withhold depreciation.

- You can file a supplement request to bridge the gap if your contractor discovers missing scope items, hidden damage, or missing overhead and profit (O&P).

- If the insurer refuses to pay the difference on covered items, you may need to invoke the appraisal clause to resolve the valuation dispute.

The Shock of the Final Settlement Check

Opening an envelope from your insurance company, seeing a check, and then realizing it covers less than half of what your local contractors quoted is one of the most frustrating moments in the claims process. I have sat across the table from hundreds of homeowners who felt completely defeated in this exact scenario. You assume that because a check was issued, the claim is closed, and you are stuck paying the rest out of pocket.

In most standard policies, that is simply not true. A homeowners insurance underpaid claim is rarely the end of the road. If you’ve already received your settlement check and it doesn’t cover your repairs, this post is for you. (Note: If your claim is still active and the initial adjuster estimate just came in low, the steps are slightly different. Similarly, if the insurer explicitly refused to cover certain items entirely, you are dealing with a partial claim denial involving a coverage dispute, which requires a different approach.)

When the insurer acknowledges the damage is covered but the final insurance settlement is not enough for repairs, you are dealing with a valuation gap. My goal is to walk you through exactly why this gap exists, how to read the estimate to find the missing money, and what practical steps you can take to get the settlement aligned with reality.

From my claims experience, I regularly see initial settlement checks fall 30% to 40% short of the actual repair costs. This isn’t always malicious; it is often a byproduct of the standardized software adjusters use and the fact that a visual inspection cannot account for hidden damage.

Why Your Settlement is Lower Than the Repair Cost

To fix an underpaid homeowners insurance claim, you first have to understand where the math went wrong. Insurers do not just pull numbers out of thin air; they build an estimate line by line. The discrepancy between what they offer and what your contractor demands usually boils down to three core issues.

The Xactimate vs. Local Market Pricing Gap

Almost all major insurance carriers use estimating software, most commonly Xactimate, to calculate the cost of materials and labor. While this software updates its pricing databases monthly, it relies on regional averages. If you live in an area experiencing a sudden boom in construction, or if a recent storm has driven up local labor demand, Xactimate pricing will often underestimate the real-world cost of hiring a qualified professional.

Your contractor is pricing the job based on what it actually costs to buy materials this week and pay a skilled crew today. The insurance adjuster is pricing it based on an algorithm’s average from last month. This alone can account for a massive shortfall.

Missing Line Items and Hidden Scope

Insurance adjusters are trained to write estimates for what they can physically see during their 45-minute site visit. If a water leak ruined your hardwood floors, they will write an estimate to replace the floors. But what about the moisture barrier underneath? What about the cost of detaching and resetting the baseboards? What about the hours required to move your heavy furniture out of the room before work begins?

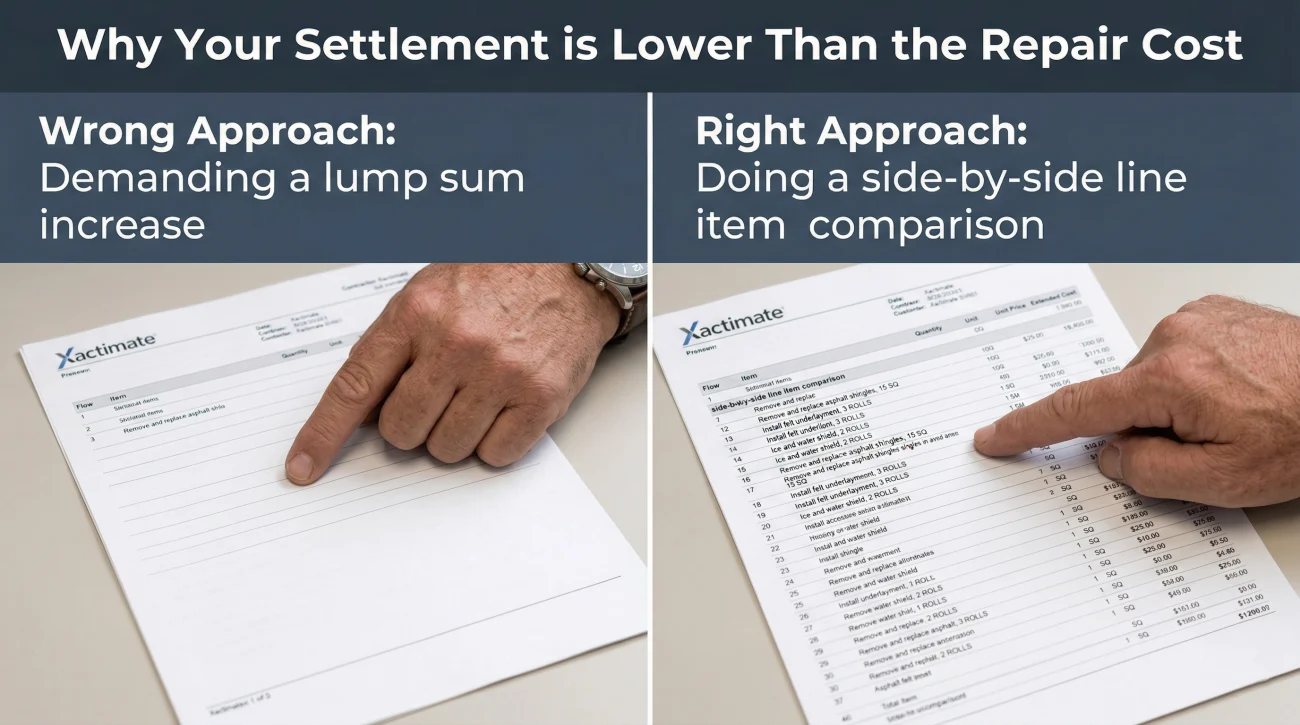

Arguing with the adjuster by simply saying, “My contractor wants $15,000 and you only gave me $9,000. You need to pay more.”

Having your contractor compare their bid side-by-side with the insurance estimate to identify the exact line items the adjuster missed (e.g., “Estimate is missing 40 linear feet of baseboard removal, debris haul-away fees, and subfloor sealing”).

The Overhead and Profit (O&P) Dispute

If your home suffered complex damage that requires coordinating multiple trades, for example, a plumber, a drywaller, a painter, and a flooring installer, you generally need a General Contractor (GC) to manage the project. GCs charge Overhead and Profit (O&P), which typically adds 20% (10% for overhead, 10% for profit) to the total repair bill.

Many insurers will intentionally leave O&P off the initial estimate, arguing that your project isn’t “complex enough” to warrant a general contractor. If your real-world repair requires a GC, but the insurance company underpaying your claim stripped out the O&P, you are instantly starting in a 20% deficit.

The ACV vs. RCV Holdback (The Most Common Confusion)

Before you panic about an insurance settlement being less than the repair cost, you need to check if depreciation was withheld. I cannot overstate how many homeowners I’ve spoken to who thought they were being lowballed, when in reality, they were just looking at the first phase of a two-part payment.

If you have a Replacement Cost Value (RCV) policy, your insurer owes you enough to replace the damaged items with new ones. However, they almost never pay this full amount upfront. Instead, they write the first check for the Actual Cash Value (ACV), which is the replacement cost minus depreciation based on the age and condition of the item.

[Total Repair Cost] - [Deductible] - [Depreciation] = [Your Initial Settlement Check]

The money withheld for depreciation is not gone; it is called Recoverable Depreciation. To get that money, you usually have to actually complete the repairs and submit the final contractor invoices to the insurer. Once they verify the work is done and you actually incurred the cost, they release the second check to cover the depreciation gap.

⚠️ Warning: A common mistake is accepting the initial ACV check, deciding the repair is too expensive to start, and abandoning the project. By doing this, you forfeit the recoverable depreciation entirely. Always check your paperwork to see how long you have to claim it, usually 180 days to one year.

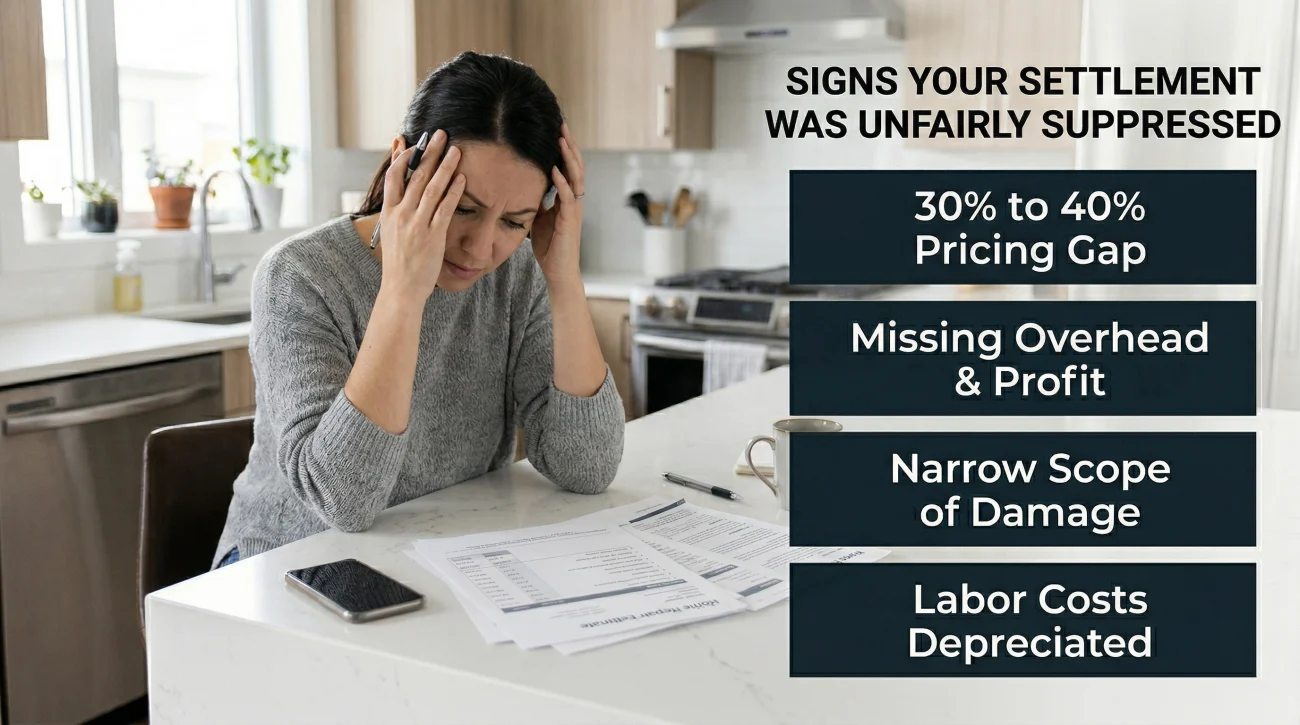

Signs Your Settlement Was Unfairly Suppressed

Once you confirm whether depreciation is holding back your funds, you need to look at the actual numbers. Sometimes the gap isn’t just a simple misunderstanding about ACV and RCV; sometimes, the estimate is fundamentally flawed. When evaluating whether to dispute a low home insurance settlement, you need to look for specific diagnostic markers in the adjuster’s paperwork.

Here are the clearest signs that your settlement was improperly suppressed and is ripe for a challenge:

- 📉 The 30% to 40% Gap: If three independent, licensed contractors quote a price that is 30% higher than the insurance estimate, the Xactimate pricing being used is likely out of touch with your local market reality.

- 🚫 Missing O&P on Complex Jobs: If your repair involves three or more trades, but the 10/10 Overhead and Profit line items are completely absent from the final page of the adjuster’s estimate.

- 🔍 Narrow Scope of Damage: The adjuster wrote to replace individual shingles on a roof rather than the whole slope, or wrote to patch a 2×2 square of drywall instead of painting the continuous wall corner-to-corner.

- ❌ Labor Costs Depreciated: The insurer applied depreciation to labor costs. This is worth flagging in your supplement because it is a commonly contested line item that your contractor can specifically challenge based on your local regulations.

If your final paperwork exhibits any of these patterns, the gap is not a miscommunication. It is a structural flaw in the estimate, and it is entirely appropriate to formally request a revision.

How to Execute the Supplement Request Process

If you are wondering what to do when your home insurance paid too little, the answer usually lies in the supplement process. Most homeowners don’t know that a final settlement can be reopened. A supplement is not a complaint; it is a documented request for additional funds to cover newly discovered facts. Here is the order of operations for filing a supplement claim.

1. Build the Documentation Package

You cannot simply call the adjuster and say the check is too small. You must prove it. Have your contractor write an itemized bid that mirrors the formatting of the insurance estimate. If the insurer missed 20 items, your contractor needs to list those exact 20 items, explain why they are required by local building codes or manufacturer specifications, and price them out.

If the dispute is over the price of materials (like lumber during a shortage), your contractor should provide actual supply house invoices showing the current market cost.

2. Submit the Formal Request

Send the supplement package to your desk adjuster in writing. Keep your emotions out of it; treat it as a routine business transaction. In my experience, adjusters respond best to clear, organized data rather than frustration.

Hello [Adjuster Name],

Attached please find a supplement request and itemized estimate from my contractor, [Contractor Company Name], regarding the repairs at [Your Property Address].

Upon beginning the repair process, the contractor identified several necessary line items that were omitted from the original scope of work, as well as updated local market pricing required to complete the job. We have also included photographic evidence of the newly exposed damage behind the drywall.

Please review the attached line-item comparison. Let me know if you need to schedule a re-inspection of the property to approve these supplemental funds.

I look forward to your response by [Date, usually 7-10 days out].

Best regards,

[Your Name]

3. Manage the Timeline and Follow Up

Insurers frequently drag their feet on supplements. It is common for these requests to sit “under review” for weeks. You must actively manage the timeline by requesting status updates in writing every 3 to 5 days. If the delay feels like a pressure tactic to make you give up on the funds, that is a clear signal you may need professional help to push the claim forward.

If putting together this level of documentation feels overwhelming, or if your contractor isn’t experienced in speaking “insurance language” (specifically Xactimate), this is exactly when having a public adjuster review the scope before you accept defeat becomes highly valuable. They specialize in finding these missed line items, translating contractor bids into insurance-approved formatting, and fighting underpayment on your behalf.

When the Appraisal Clause is the Right Path

Sometimes, you submit a perfectly documented supplement, and the insurance company still refuses to budge. They might argue that your contractor’s labor rates are just too high, or they might stubbornly refuse to add Overhead and Profit. When you reach a complete standstill over the cost of repairs, but the insurer still agrees the damage is covered, you have a specific tool available.

Valuation disputes where coverage is not in question are the primary use case for invoking the appraisal clause. This is a binding dispute resolution mechanism found in most standard HO3 policies.

| Situation | Is Appraisal Clause Appropriate? |

|---|---|

| Insurer agrees the floor is damaged, but offers $4,000 while contractor says it costs $8,000. | Yes. This is a pure valuation dispute. |

| Insurer agrees the roof needs repair, but disputes whether it requires a full replacement or a patch. | Yes. This is a scope and valuation dispute. |

| Insurer says the water damage is from a long-term leak and denies the claim entirely. | No. Appraisal cannot decide coverage, only cost. |

If you find yourself in a deadlock over the dollar amount, you should familiarize yourself with how the home insurance appraisal process works mechanically. It requires hiring an independent appraiser, which costs money, so you must ensure the gap in your settlement is large enough to justify the expense.

Final Thoughts on Underpaid Claims

An underpaid homeowners insurance claim should never be viewed as the final word. The initial check is often just a starting point based on a brief visual inspection. Document the discrepancies, lean on your contractor for detailed line-item bids, and don’t be afraid to utilize the formal supplement process in writing. If you have escalated to a manager and the insurer is still digging their heels in, check our overview of the home insurance claim dispute landscape to route your next move, or dive directly into how to fight back when the insurer won’t budge.

❓ FAQ

🧐 What do I do if my insurance check is not enough for repairs?

Do not sign any release of liability forms. Ask your contractor to create a detailed, line-item estimate showing exactly what the insurance adjuster missed, and submit this to the insurer as a formal supplement request.

💸 Can I negotiate a final insurance settlement?

Yes. Insurance estimates are not final decrees. You can negotiate by providing objective evidence, such as independent contractor bids, local market material pricing, and photos of hidden damage that justify a higher payout.

🏚️ What if the contractor finds more damage after the insurance pays?

Instruct your contractor to stop work immediately, take clear photos of the newly discovered damage, and contact your desk adjuster to file a supplement before proceeding with the repairs.

📝 How do I file a supplement claim for my home?

Send a written email to your adjuster including your claim number, a brief explanation of the missing items, and attach your contractor’s detailed line-item estimate and supporting photos.

📉 Why did my insurance company depreciate my claim?

They hold back depreciation initially to pay the current, aged value of the item. Once you prove the repairs are completed, you can recover this withheld amount. (See the ACV vs. RCV section above for full details).

⏳ Does cashing the insurance check mean I accept the settlement?

Usually, no. Cashing the initial check does not close your claim or waive your right to file a dispute, provided you haven’t signed a document explicitly labeled “Full and Final Settlement” or a release of liability waiver.

📊 What happens if my contractor’s estimate is higher than Xactimate?

Your contractor must justify the difference. They need to show that Xactimate’s regional pricing is inaccurate by providing actual supply house invoices and local labor market rates for the specific trades required.

⚖️ How can I get the insurance to pay my contractor’s invoice?

Sending an invoice alone usually isn’t enough to secure payment. If negotiations and supplements fail on a covered loss, you must invoke the appraisal clause to have an independent umpire review the pricing and make a binding decision.

🤷♂️ What does overhead and profit mean on an insurance estimate?

Overhead and Profit (O&P) is a standard percentage addition to the total claim meant to cover the costs of a General Contractor managing a complex repair involving three or more different construction trades.

🧩 What if the insurer approves some supplement items but denies others?

This partial approval is very common. You can accept the funds for the approved items while continuing to dispute the denied ones. If you hit a wall, this is exactly when a public adjuster or the appraisal clause becomes necessary to resolve the remaining items.

A denial sits inside a larger picture. These explain the parts around it.

- How the settlement process works after damage is reported

- Which parts of your policy apply when damage is involved

- How your damage type affects what the insurer is required to pay

- Whether the damage you have is actually worth filing for

- What happens when the claim you filed gets rejected

- How independent representation changes what gets documented

- When a disputed claim moves into legal territory

Not all denials are final. The path forward depends on why it happened.

- Whether your damage assessment left money on the table

- What the inspector who came to your home was actually there to do

- The parts of water damage that standard inspections routinely miss

- What fire and smoke assessments leave out of the scope

- Why the insurer's roof estimate is almost always lower than the roofer's

- When the denial crosses from a dispute into something that needs legal leverage

- Four options to fight back, including one most homeowners never use

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.