- Filing a complaint with your state’s Department of Insurance triggers a regulatory review to ensure the insurer followed proper laws and procedures. It is not a lawsuit.

- The state can fine insurers for procedural violations, require them to respond to ignored communications, and investigate bad faith tactics.

- The state cannot force an insurance company to pay a disputed claim or make final determinations on whether your specific damage is covered.

- Filing is most effective when you have documented proof of unreasonable delays, missing denial explanations, or incorrect policy citations.

- When you file, the insurance company will transfer your case from the local adjuster to a specialized compliance department to answer the state’s inquiry.

The Reality of Reporting Your Insurer

When communication breaks down and frustration peaks, many homeowners want to know how to file complaint against home insurance company representatives. You might feel ignored, unfairly denied, or trapped in an endless loop of documentation requests. At this stage, escalating the issue to a government authority feels like the only logical next step.

However, in my experience working alongside homeowners during complex claim disputes, there is a massive misunderstanding about what this escalation actually achieves. Most people assume that reporting the insurance company to the state is equivalent to suing them. You expect the state to look at your photos, look at the adjuster’s low estimate, and order the insurance company to cut you a check. That is not how the system works.

Filing a state insurance department complaint homeowners process is a regulatory mechanism, not a legal judgment. The state insurance commissioner exists to ensure that insurance companies operate legally and follow state-mandated claims handling rules. They are referees for the rules of the game, not judges who declare a winner in a specific contract dispute. Knowing exactly what this process can and cannot do will save you weeks of waiting for an outcome the state simply cannot provide.

Regulatory Review Versus Legal Action

To use this tool effectively, you must understand the difference between a procedural violation and a valuation dispute. The department of insurance complaint process is entirely focused on procedure and regulation compliance.

If your insurer ignores your emails for forty days, fails to provide a written explanation for a denial, or cites a policy exclusion that does not actually exist in your contract, they have broken claims-handling regulations. The state cares very much about these infractions. For context on how a standard claim timeline should ideally function, you can review our general overview of the claim denial process.

Conversely, if your insurer agrees your roof is damaged but their estimate is $10,000 while your contractor’s estimate is $25,000, that is a valuation dispute. Both parties are looking at the same damage and simply disagreeing on the cost to fix it. The state department of insurance will almost never intervene in a pure math argument.

I consistently see homeowners file angry, five-page complaints to the state commissioner arguing about the price of drywall or roofing square footage. Weeks later, they receive a polite letter back stating the department cannot settle factual disputes. The complaint is closed, and the homeowner has lost a month of valuable time.

What the Department of Insurance Can Do

When you file complaint with insurance commissioner offices, you are activating a powerful oversight body. While they will not write you a settlement check, they have significant authority to make the insurance company uncomfortable if rules were broken.

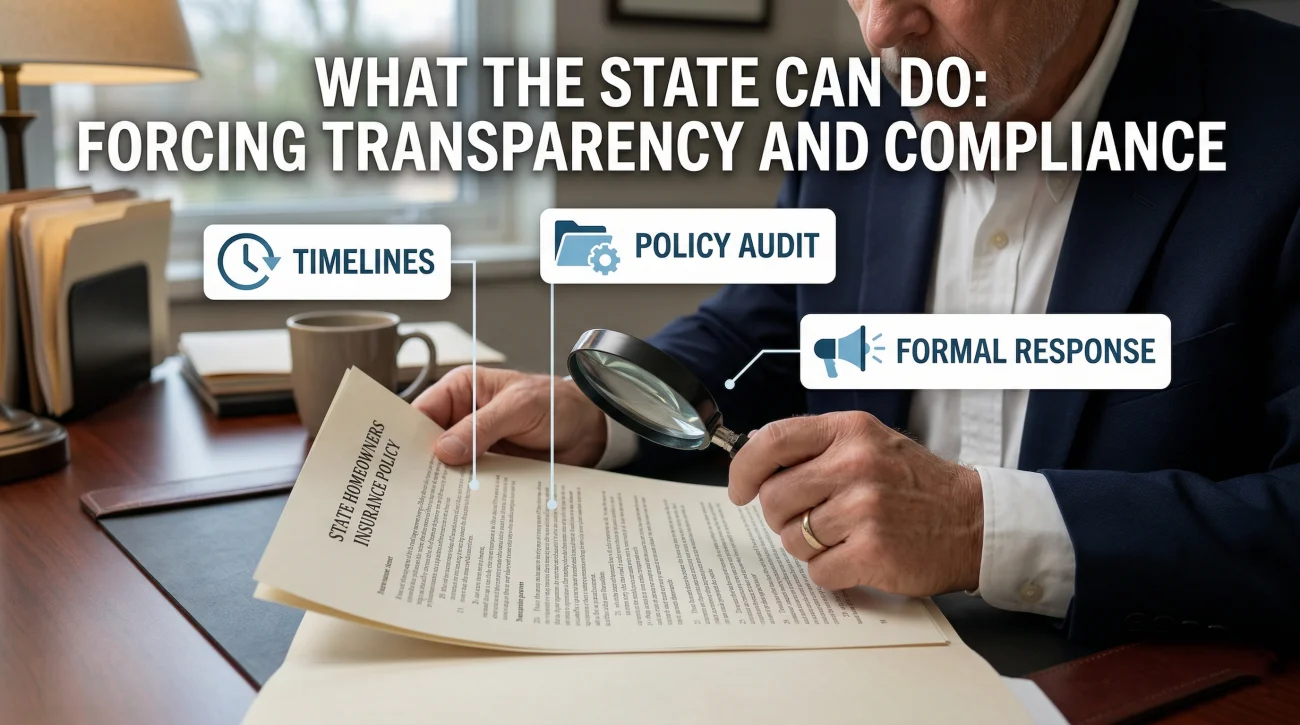

Here is exactly what the state can do on your behalf:

- Investigate timelines: Every state has strict laws dictating how many days an insurer has to acknowledge a claim, inspect the property, and issue a decision. The state will investigate if the insurer missed these deadlines.

- Force a formal response: If your adjuster has gone completely silent, a state complaint forces the insurance company to legally reply to both you and the department of insurance.

- Audit policy language: The state can verify if the reason for denial actually aligns with the legal language filed in your policy documents.

- Impose fines: If the insurer is found to have violated state regulations or engaged in deceptive practices, the state can levy heavy fines against the company.

- Mediate minor disputes: In some specific states, the department offers voluntary mediation programs to help both sides reach an agreement without going to court. Mediation is often highly effective for bridging small valuation gaps or resolving minor scope disagreements. However, it is generally not an effective tool for cases involving complete coverage denials or severe bad faith conduct.

What the Department of Insurance Cannot Do

The most common question I hear is whether the state can fix an unfair payout. People often ask, can state insurance department force insurer to pay? The short answer is almost always no.

| What Homeowners Expect | What the State Actually Does |

|---|---|

| Determine exactly how much the repairs should cost. | Tells you that pricing disputes must be resolved via your policy’s appraisal clause or litigation. |

| Act as your personal lawyer to negotiate a higher settlement. | Acts as a neutral regulatory body ensuring basic compliance laws were not broken. |

| Decide definitively if a specific gray-area peril is covered. | Reviews if the insurer provided a legal justification for their decision, without deciding who is right. |

The department of insurance cannot act as your legal counsel. They cannot override an adjuster’s factual observation that a pipe leaked slowly rather than bursting suddenly. If the insurance company provides a legally sound, albeit highly debated, reason for their denial, the state will likely close the complaint and advise you to seek private legal counsel.

Step-by-Step: How to Report an Insurance Company to the State

If your situation involves a true procedural violation, filing is incredibly straightforward. You do not need to mail physical letters in most jurisdictions. The process is handled almost entirely online through your state government portals.

Step 1: Locate Your State’s Portal

Search online for your specific state’s insurance regulatory body. Keep in mind that the exact name varies by location; you will typically be looking for the “Department of Insurance”, the “Office of the Insurance Commissioner”, or the “Division of Financial Services.” Navigate to their consumer protection or complaint section, where they will have a dedicated online portal for filing.

Step 2: Gather Your Documentation

The state investigator needs proof, not just a story. Before you open the form, ensure you have digital copies of the following documents:

- Policy declarations page: This proves your coverage was active during the event.

- Complete denial letter: This shows the exact reason and policy language the insurer cited.

- Independent estimates: Include any contractor quotes you have received.

- Communication log: A chronological record showing the exact dates of all emails and phone calls. This is the most critical piece of evidence for proving procedural violations.

Step 3: Write a Factual Complaint Description

This is where most homeowners fail. Emotion does not help your case. The state investigator reads dozens of these daily. You need to present the facts clinically, focusing specifically on the rules the insurer broke rather than how stressed you feel.

“My insurance company is running a scam. They took my premiums for ten years and now they refuse to pay for my ruined kitchen. The adjuster was incredibly rude to my wife and they are offering pennies on the dollar. Help me make them pay.”

“On October 1st, I filed a water damage claim. The insurer failed to acknowledge the claim within the 15-day state requirement. On November 20th, I received a denial letter citing an exclusion for ‘earth movement’, which does not apply to my burst pipe scenario. They have not responded to three subsequent requests for clarification.”

Notice that the correct approach highlights specific timeline violations and policy misapplications. This gives the state investigator a clear regulatory target to investigate.

💡 Pro Tip: Keep your complaint description under five hundred words. Bullet points outlining the timeline of events are highly effective. If you are unsure where to start, you can use the template below.

Template: Sample Complaint Language

“On [Date], I filed claim #[Claim Number] for [Type of Damage]. Under state regulations, the insurer is required to [specific action, e.g., acknowledge the claim] within [X] days. As of today, [X] days have passed without a response. Furthermore, their letter dated [Date] cites [Policy Section], which does not accurately reflect my policy language. I have attached my communication log and policy declarations page for your review.”

Once you hit submit, the process moves out of your hands and into the state’s regulatory system.

What Happens When You File an Insurance Complaint

The timeline begins the moment your complaint is officially filed. Many people wonder how long does insurance department complaint take to resolve. While it varies by state, the general cycle takes between 30 and 90 days from start to finish.

When the state receives your file, they first review it to ensure it falls within their jurisdiction. If it does, they forward a formal copy of your complaint directly to your insurance company. This is a critical moment. Your claim file is typically removed from the desk of your original adjuster.

Insurance companies have specialized compliance and regulatory response teams. A higher-level representative must now review the entire file and draft a formal legal response to the state, explaining exactly why they handled the claim the way they did. The insurer is usually given 15 to 30 days to provide this response.

After receiving the insurer’s response, the state investigator reviews both sides. If the insurer made a procedural error, the state will demand they correct it, which might force them to reopen the claim or issue a new letter. If the insurer proves they followed state guidelines, the department will close the case and send you a letter explaining their findings.

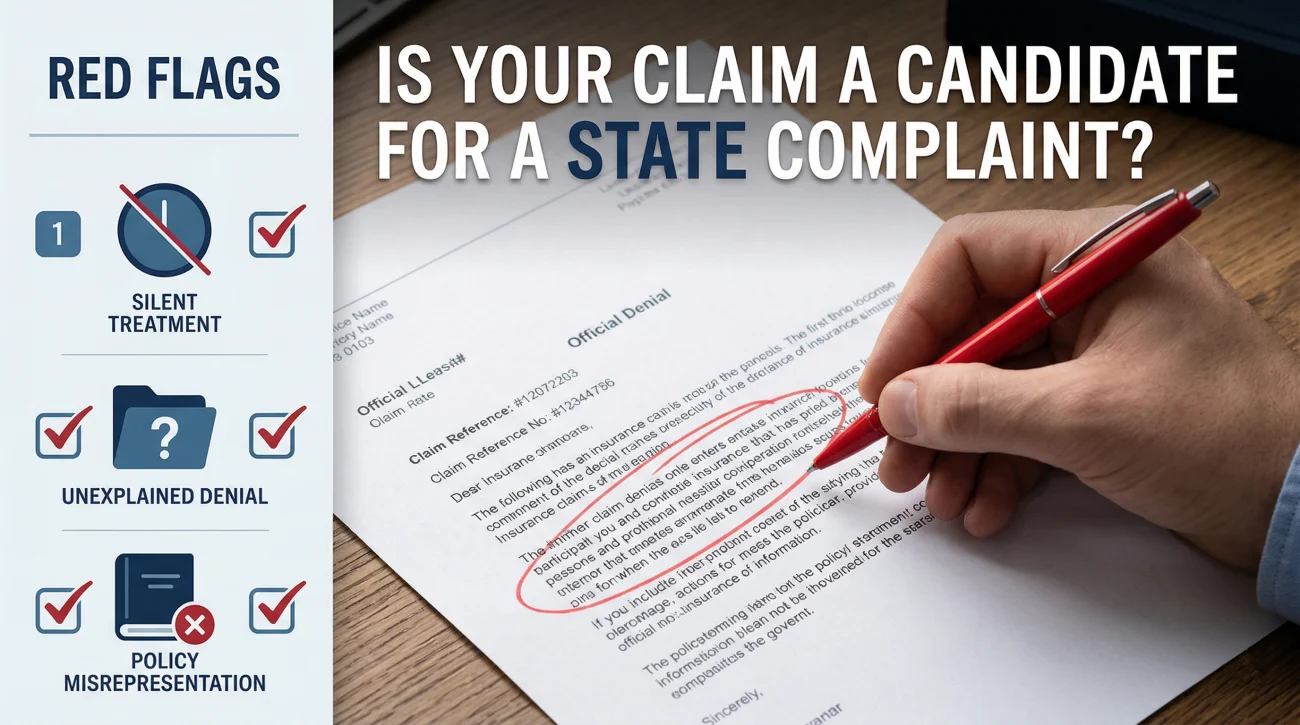

Signs Your Situation Fits a Procedural Complaint

Because the state only handles specific types of infractions, you must diagnose the root cause of your frustration before filing. If you file a complaint for the wrong reason, you simply waste time. Here are the clear signs that an insurance commissioner complaint home insurance inquiry is the right tool for your situation:

- The Unexplained Denial: The insurer sent a letter stating your claim is denied but completely failed to cite a specific policy section or explain the reasoning.

- The Silent Treatment: You have submitted all requested documentation, but the insurer has not responded in over 30 days, violating standard communication timelines.

- The Phantom Exclusion: The denial letter quotes a policy exclusion that literally does not exist in the policy documents you were provided when you purchased the coverage.

- The Endless Delay: The insurer keeps asking for the exact same documents you have already provided multiple times as a stalling tactic.

If your situation matches these signs, the state can force the insurer to adhere to the rules. If you suspect your insurer is engaging in intentional delay tactics or actively misrepresenting policy terms, you can review the recognized patterns of insurance bad faith conduct to see if their actions cross the legal line. Alternatively, if your denial is based on a simple misunderstanding of the scope rather than a regulatory violation, learning how the formal internal appeal process works is usually a better first step.

What to Do If the State Cannot Help

If the department closes your complaint because your issue is a factual dispute rather than a procedural one, your claim is not over. You simply need to use the correct tool for your specific problem:

- For valuation disputes: If the insurer agrees there is coverage but disagrees on the cost, invoking your policy’s appraisal clause is usually the most effective path.

- For scope misunderstandings: If the initial denial was based on a simple mistake by the adjuster, utilizing the formal internal appeal process allows you to submit new evidence.

- For bad faith or full denials: If you are facing an unfair complete denial of a massive loss, getting a professional legal evaluation is your strongest escalation path.

For a complete breakdown of every method available, read our guide on how to choose the right escalation path for your situation.

Final Thoughts Before You File

Filing a state complaint is a powerful tool, but it is a precision instrument, not a sledgehammer. I always advise homeowners to use it specifically when the insurance company refuses to play by the established rules of communication and procedure.

It is important to remember that this is only one of several escalation paths available to you. By understanding the limits of the state’s regulatory power, you can save valuable time and route your dispute through the channel that is actually designed to resolve it effectively.

❓ FAQ

📋 Does it cost money to file a complaint with the state?

No, filing a complaint with your state’s Department of Insurance is completely free. It is a consumer protection service provided by your state government.

⏱️ Is there a deadline to file an insurance complaint?

While there is no strict deadline to file the regulatory complaint itself, you must be aware of your state’s statute of limitations for taking formal legal action on property claims. Statutes of limitations vary widely by state. Please consult your policy documents or a legal professional for the applicable timeframe in your specific situation.

👨⚖️ Can the state insurance department force the insurer to pay?

No. The state can force an insurer to follow proper procedures, explain their actions, and correct timeline violations, but they cannot legally order an insurer to pay a disputed factual claim.

📝 What happens exactly when you file an insurance complaint?

The state reviews your submission and sends a formal inquiry to the insurance company. The insurer is then legally required to provide a detailed, written response explaining their handling of your claim to the state investigator.

📞 Should I tell my adjuster I am filing a state complaint?

It is not necessary to use it as a threat. Simply file the complaint. The state will officially notify the insurance company’s compliance department, which is far more effective than arguing with an individual adjuster.

📄 Do I need a lawyer to file a complaint with the insurance commissioner?

No, the process is designed specifically for everyday consumers. The online forms are straightforward and do not require legal representation to complete.

🛑 Will my insurance rates go up if I complain?

No. State laws strictly prohibit insurance companies from retaliating against consumers or raising premiums specifically because a regulatory complaint was filed against them.

🔎 Can I file a complaint while my claim is still open?

Yes, absolutely. In fact, filing while a claim is open is common when dealing with extreme delay tactics or adjusters who refuse to return phone calls for weeks at a time.

🏢 Is this different from a Better Business Bureau (BBB) complaint?

Yes, significantly different. The BBB has no legal or regulatory authority over an insurance company. The state Department of Insurance holds the company’s license to operate and can issue binding fines.

⚖️ What if the DOI says they cannot help me with my dispute?

If the state closes your complaint stating it is a factual dispute rather than a procedural one, your remaining options are typically invoking your policy’s appraisal clause or escalating to formal litigation.

A denial sits inside a larger picture. These explain the parts around it.

- How the settlement process works after damage is reported

- Which parts of your policy apply when damage is involved

- How your damage type affects what the insurer is required to pay

- Whether the damage you have is actually worth filing for

- What happens when the claim you filed gets rejected

- How independent representation changes what gets documented

- When a disputed claim moves into legal territory

Not all denials are final. The path forward depends on why it happened.

- Whether your damage assessment left money on the table

- What the inspector who came to your home was actually there to do

- The parts of water damage that standard inspections routinely miss

- What fire and smoke assessments leave out of the scope

- Why the insurer's roof estimate is almost always lower than the roofer's

- When the denial crosses from a dispute into something that needs legal leverage

- Four options to fight back, including one most homeowners never use

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.