- There is a strict legal distinction between an insurance adjuster making an honest mistake and an insurance company acting in bad faith.

- Unreasonable delays, misrepresenting your policy language, and failing to properly investigate your damage are recognized patterns of bad faith conduct.

- If your claim experience matches these specific patterns, the appropriate next step is typically a legal consultation rather than filing another standard appeal.

The Legal Line Between Error and Intent

Insurance companies process thousands of property claims every single day. In a system that massive, mistakes happen. Measurements get dropped, emails get lost in spam folders, and adjusters occasionally misread a repair estimate. However, there is a fundamental legal distinction between a frustrating administrative error and an insurance company acting in bad faith.

During my time reviewing claim files and settlement disputes, I have seen homeowners spend months writing appeal letters to correct what they thought was a simple misunderstanding. In reality, they were trapped in an intentional holding pattern. Most homeowners cannot tell the difference between a disorganized claims department and a company that is actively violating its legal duties.

If you have received a confusing denial or experienced impossible delays, you are likely wondering if your insurer’s conduct has crossed the line. Below, we will break down exactly what bad faith means in property insurance, how courts and regulators identify it, and the specific behavioral patterns that indicate your claim is no longer undergoing a normal review process.

What “Bad Faith” Actually Means in Property Insurance Law

To understand bad faith, you first have to understand the standard your insurance company is legally required to meet. When you purchase a homeowners insurance policy, you are not just buying a piece of paper. You are entering into a contract that includes an “implied covenant of good faith and fair dealing.”

In plain terms, this duty of good faith requires your insurance carrier to investigate, evaluate, and pay your valid claims fairly and reasonably. They are legally obligated to look for reasons to approve your claim, rather than actively hunting for loopholes to deny it. When an insurance company breaches that duty through unreasonable, unfair, or intentional misconduct, it is known as bad faith.

As I often explain to the homeowners I work with: “The insurance company has a duty to give your financial interests at least the same level of consideration as they give their own. When a carrier purposefully ignores evidence that proves your damage is covered simply to protect their profit margins, they have abandoned that duty.”

Bad faith is not just a strong phrase you use when you are angry at customer service. It is a specific legal concept. If you are trying to understand where your situation fits within the broader landscape of the most common types of home insurance claim denials, identifying bad faith is the most critical step you can take.

The Key Distinction: Adjuster Error vs. Bad Faith

The most common question I hear from frustrated policyholders is whether a terrible settlement offer automatically counts as bad faith. The answer is no. A low settlement offer, by itself, is often just a valuation dispute. The dividing line comes down to the basis of the decision and the reasonableness of the conduct.

An honest mistake, a simple disagreement over the cost of labor in your zip code, or an adjuster who poorly documented a room because they were rushing does not typically rise to the level of bad faith. These are errors that can usually be corrected through standard negotiation or appraisal.

The field adjuster inspects your flooded kitchen, misses a hidden pocket of moisture behind the cabinets, and issues a settlement that does not include mold remediation.

You provide the adjuster with a certified moisture reading from an independent contractor proving the walls are saturated, and the insurer still denies the remediation cost without conducting any further investigation of their own.

Bad faith involves a lack of reasonable basis for a denial or delay. If the insurer has all the facts needed to pay the claim and still refuses to do so without a justifiable reason, the conduct shifts from error to bad faith.

What Bad Faith Is NOT

To avoid overreacting, it helps to know what normal friction looks like in the claims process. The following scenarios are highly frustrating, but they are generally not bad faith:

- 💡 Catastrophe Season Delays: Waiting four weeks for an adjuster after a major hurricane is usually a logistical reality, not an intentional tactic.

- 💡 Initial Low Estimates: Receiving a low first offer based on standard software pricing is common. The supplement process is designed to bridge this exact gap.

- 💡 Scope Disagreements: The adjuster refusing to pay for a full roof replacement when they believe only a few shingles are damaged is a standard valuation dispute, addressable via the appraisal clause.

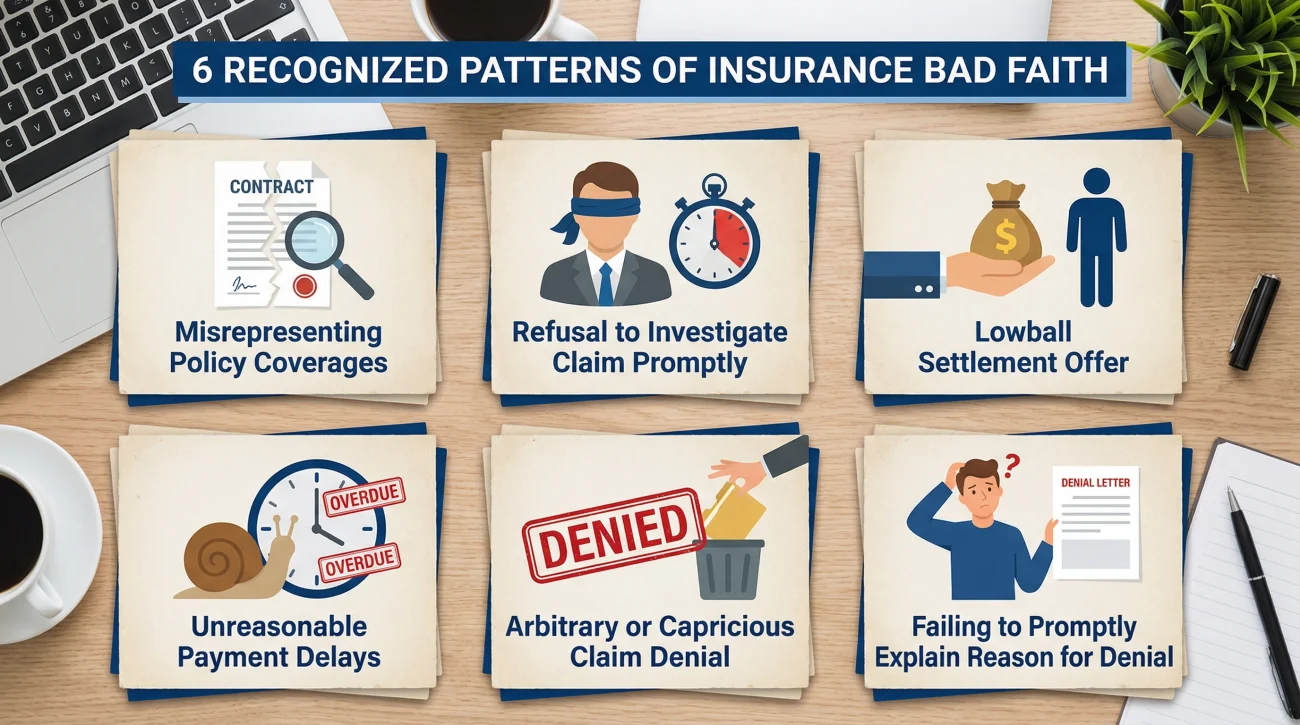

Recognized Patterns of Bad Faith Conduct

Courts and regulatory agencies have identified specific patterns of behavior that strongly indicate an insurance company is acting in bad faith. If you recognize any of these patterns in your own claim file, you are not dealing with a normal adjustment process.

1. Denying a Claim Without a Legitimate Basis

Insurance companies must have an actual, factual reason to deny your claim. They cannot simply say “we do not believe this is covered.” If they issue a denial, they must point to a specific exclusion in your policy and pair it with physical evidence from their investigation. Denying a claim based on assumptions, generalizations, or internal company quotas is a classic bad faith indicator.

2. Misrepresenting Policy Language or Exclusions

Insurance policies are dense, and carriers know that most homeowners cannot interpret the legal jargon. A severe bad faith tactic involves an adjuster intentionally misquoting your policy limits or telling you that a specific peril is excluded when your policy actually covers it. For example, telling a homeowner that a sudden pipe burst is excluded under the “wear and tear” provision is a deliberate misrepresentation of how sudden water damage is handled.

3. Failing to Conduct a Proper Investigation

Your insurer cannot deny your claim from behind a desk without looking at the evidence. They have a legal duty to conduct a prompt, thorough, and objective investigation. If you suffered a massive house fire and the adjuster spends exactly twenty minutes walking around the perimeter of the property before issuing a denial, they have failed their duty to investigate.

4. Offering a Lowball Settlement Without Factual Basis

There is a difference between a strict negotiation and an insulting lowball offer. If your independent contractor estimates a repair at $60,000, and the insurance company offers you $4,000 without providing any line-item explanation or alternative contractor bid to justify their math, they are likely attempting to force you into a corner. This is an abuse of their superior financial position.

5. Demanding Excessive or Irrelevant Documentation

This is often called the “moving goalpost” tactic. You submit exactly what the adjuster asks for. Two weeks later, a new adjuster takes over the file and asks for the exact same documents again. Then, they ask for ten years of your personal tax returns for a basic roof damage claim. Requesting burdensome, irrelevant documentation solely to delay the process is a recognized bad faith tactic.

6. The Shifting Position (Changing Denial Reasons)

This is one of the most glaring and documentable signs of bad faith. The insurer initially denies the claim stating the repair falls below your deductible. When you provide contractor estimates proving the repair actually costs $20,000, they suddenly issue a new letter claiming the damage is due to “pre-existing wear and tear.” When an insurer’s written correspondence contradicts itself to avoid payment, they are actively hunting for loopholes.

How Insurance Delay Tactics Cross into Bad Faith

Of all the patterns listed above, delay deserves a closer look because it is the one most easily dismissed as normal. Delays are a reality of the insurance world, especially when local adjusters are overwhelmed. However, there is a strict difference between a logistical backlog and an intentional strategy to exhaust the policyholder.

In many states, insurance companies are bound by specific statutory timelines. They have a set number of days to acknowledge your claim, decide whether to approve or deny it, and issue the check once approved. When an insurer ignores these deadlines without a valid, documented excuse, it crosses into bad faith territory.

| Legitimate Claim Delay | Bad Faith Delay Tactic |

|---|---|

| Adjuster needs 14 days to schedule a specialist engineer for a complex foundation crack. | Adjuster goes completely silent for 45 days and ignores six of your follow-up emails. |

| Insurer pauses payment because your provided receipts are blurry and illegible. | Insurer refuses to release undisputed funds while arguing over a separate, unrelated room. |

| Processing slows down because a Category 5 hurricane hit your state last week. | Processing stops entirely because the insurer keeps rotating your file to different desk adjusters. |

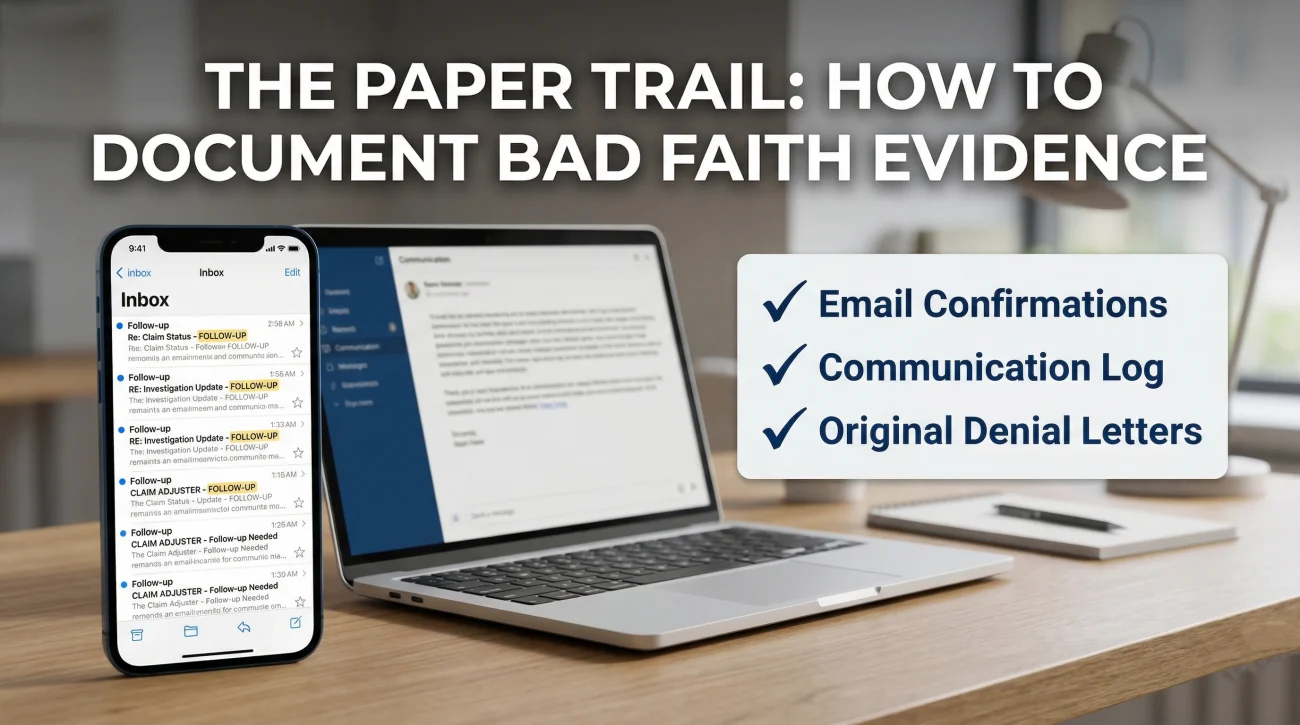

What to Say When You Suspect Bad Faith: Building Your Paper Trail

If you suspect you are the victim of bad faith, your frustration is not enough to prove it. You need meticulous documentation. If your claim eventually escalates to a legal review, the entire history of your correspondence will become the foundation of your case.

You must transition from having phone calls to strictly communicating in writing. It is not about drafting a legal script; it is about using communication principles that signal you are paying attention, without triggering defensive behavior. If an adjuster calls you and makes a promise, immediately send a follow-up email confirming exactly what they said.

💡 Pro Tip: Keep a master log of every interaction. Record the date, the time, the name of the representative, and the exact reason they gave for any delay or denial.

Here are two practical scenarios showing how to document bad faith patterns in writing to protect yourself:

Scenario A: The “Moving Goalpost” (Repeated Document Requests)

Dear [Adjuster Name],

I am writing to confirm receipt of your email today requesting my contractor’s itemized estimate. As noted in my previous emails dated October 4th and October 18th, this exact document was already submitted and acknowledged by your office. I have attached it here for the third time. Please confirm receipt and provide a specific date when a coverage decision will be made, as these continuous duplicate requests are causing an unreasonable delay in my repairs.

Scenario B: The “Shifting Position” (Changing Denial Reasons)

Dear [Adjuster Name],

I received your letter dated November 2nd stating my claim is denied due to “pre-existing wear and tear.” However, in your previous letter dated October 15th, the stated reason for denial was that the damages fell below my deductible. I have attached both letters for your reference. Please provide a clear, written explanation of why the company’s position on the cause of loss has changed immediately after I submitted estimates proving the repair exceeds my deductible.

Creating this kind of paper trail is essential. If the situation becomes completely unmanageable, some homeowners consider filing a formal complaint with their state department of insurance. While a regulatory complaint can force an insurer to respond to procedural violations, it is important to understand that the state cannot act as your lawyer or award you bad faith damages.

What Bad Faith Damages Can Mean Beyond Your Claim

The reason the distinction between a simple error and bad faith matters so much is the legal remedy available to you. If your insurance company simply made a math error, your remedy is usually limited to the actual amount they owed you under the policy in the first place.

However, when an insurer commits bad faith, the legal landscape changes entirely. In many states, bad faith opens the door to extra-contractual damages. This means that a court can penalize the insurance company for their misconduct above and beyond the original value of your property damage.

Depending on your jurisdiction, a successful bad faith claim can result in the insurer being forced to pay your attorney fees, compensation for the emotional distress their tactics caused, and in severe cases, punitive damages designed to punish the company for egregious behavior. This is why insurers take bad faith allegations incredibly seriously once formal legal representation is involved.

Diagnostic Signs You Are Facing Bad Faith

It is easy to second-guess yourself when dealing with massive insurance corporations. They handle claims every day, and they use highly authoritative language that makes homeowners feel like they are in the wrong. If you are questioning whether your experience is normal, review this diagnostic checklist. If your claim matches these patterns, this is not normal claims handling:

- ⚠️ The denial letter cites a policy exclusion that simply does not appear anywhere in your actual policy documents.

- ⚠️ Your home suffered a large, complex loss, but the field adjuster’s visit lasted barely 20 minutes before they left.

- ⚠️ The insurance company issued a flat denial without ever requesting your photos, contractor estimates, or supporting documentation.

- ⚠️ The insurer’s written position keeps shifting. They change their reasoning for the denial immediately after you provide evidence that disproves their first excuse.

- ⚠️ Your payment delays are now measured in months, and the adjuster provides no written explanation for the stall.

Moving from Frustration to Legal Review

If the patterns above match your experience, you have reached a critical juncture in your claim. Continuing to send standard appeal letters to an insurance company that is intentionally ignoring your evidence is a waste of your time. You cannot negotiate reasonably with a party that is acting unreasonably.

You paid your premium with the expectation that your insurance company would protect you when disaster struck. You fulfilled your end of the contract. When an insurer utilizes delay tactics, misrepresentation, or baseless shifting denials to protect their own bottom line, they are breaking that contract.

When an insurer’s conduct crosses the line into bad faith, the appropriate next step is an elevation of the dispute. Having your file reviewed by a legal professional changes the dynamic entirely. Document every interaction, save every email, and never assume that a denial letter is the final word.

To understand how a lawyer analyzes these exact conduct patterns, you should look into the process of consulting with a licensed insurance claim attorney who specializes in policyholder rights. For a broader picture of all your options, take time to review the available paths for how to fight a denied home insurance claim so you can make an informed decision on your next move.

❓ FAQ

📝 What is the legal definition of bad faith in insurance?

Bad faith refers to an insurance company’s unreasonable or intentional breach of their implied duty of good faith and fair dealing. This happens when they fail to investigate, evaluate, or pay a valid claim without a legitimate factual or legal basis.

⚠️ Can bad faith occur before a formal denial?

Yes. Bad faith can manifest during the initial investigation phase. If your insurer is ignoring your claim, refusing to send an adjuster, or intentionally stalling the assessment, that conduct can be considered bad faith long before an official denial letter is printed.

⚠️ How do I know if my claim delay is bad faith?

A delay crosses into bad faith when it is unreasonable and lacks a valid explanation. If the insurer ignores your communications for months, repeatedly asks for the same documents, or violates state response timelines without cause, it is likely a bad faith tactic.

💡 Can a low settlement offer be considered bad faith?

Yes, if the offer is intentionally insulting and lacks any factual basis. While insurers are allowed to negotiate, offering a severely low amount without providing a competing estimate or valid reasoning, specifically to force a desperate homeowner to settle, can constitute bad faith.

📝 Does a mistake by my adjuster count as bad faith?

Generally, no. An honest administrative error, a missed measurement, or a simple miscommunication is usually just negligence or a scope dispute. Bad faith requires an element of unreasonableness or an intentional refusal to honor the policy terms.

💡 What evidence do I need to prove bad faith?

You need a meticulous paper trail. This includes a chronological communication log, copies of all emails, the original denial letter citing incorrect policy language, and proof that you provided the necessary evidence which the insurer subsequently ignored.

📝 How long does an insurance company have to decide on my claim?

Timelines vary by state. Check your state’s department of insurance website for the specific statutory deadlines that apply to your policy. Many states require acknowledgment and coverage decisions within specific timeframes once proof of loss is submitted.

⚠️ Can I sue my insurance company for emotional distress?

Some jurisdictions allow policyholders to recover extra-contractual damages, which can include compensation for severe emotional distress as part of a bad faith claim. An insurance attorney can tell you whether this specific remedy applies in your state.

💡 Should I file a state complaint before claiming bad faith?

Filing a complaint with your state’s department of insurance can help resolve procedural violations and force the insurer to respond to you. However, a state agency cannot award bad faith damages or act as your lawyer; only a legal claim can do that.

💡 Do I need an attorney to prove bad faith?

Because bad faith involves complex legal standards and potential extra-contractual damages against well-funded corporate defense teams, consulting with an experienced insurance claim attorney is highly recommended to evaluate your specific options.

A denial sits inside a larger picture. These explain the parts around it.

- How the settlement process works after damage is reported

- Which parts of your policy apply when damage is involved

- How your damage type affects what the insurer is required to pay

- Whether the damage you have is actually worth filing for

- What happens when the claim you filed gets rejected

- How independent representation changes what gets documented

- When a disputed claim moves into legal territory

Not all denials are final. The path forward depends on why it happened.

- Whether your damage assessment left money on the table

- What the inspector who came to your home was actually there to do

- The parts of water damage that standard inspections routinely miss

- What fire and smoke assessments leave out of the scope

- Why the insurer's roof estimate is almost always lower than the roofer's

- When the denial crosses from a dispute into something that needs legal leverage

- Four options to fight back, including one most homeowners never use

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.