- A denied claim does not simply disappear. It is logged in a national database called the CLUE report as a claim closed without payment, which underwriters review closely.

- Depending on your insurance company’s rating model, a zero-dollar claim can still trigger a premium increase or flag your policy for non-renewal due to claims frequency.

- You have a limited window to fight an unfair denial before it becomes a permanent record, and you must proactively document out-of-pocket repairs to maintain your future insurability.

The Hidden Reality of Rejected Claims

When you receive a letter stating that your insurance company will not pay for your property damage, your immediate focus is usually on how to cover the repair costs out of pocket. Many homeowners assume that because the insurer did not write a check, the entire event is simply erased from the ledger. I often sit across from homeowners who are shocked to discover this is entirely incorrect. The truth is, if you are wondering whether a denied claim affects your future coverage, the answer depends heavily on a quiet backend system that tracks nearly every interaction you have with your carrier.

In my experience handling property claims, the lingering effects of a zero-dollar claim often catch people off guard years later when they try to switch carriers or buy a new policy. Insurance companies are incredibly diligent record keepers. They do not just track the money they spend. They track the frequency of incidents reported at your property, regardless of the financial outcome. Understanding how these records work is the first step in protecting your future risk profile.

The Costly Difference Between an Inquiry and a Claim

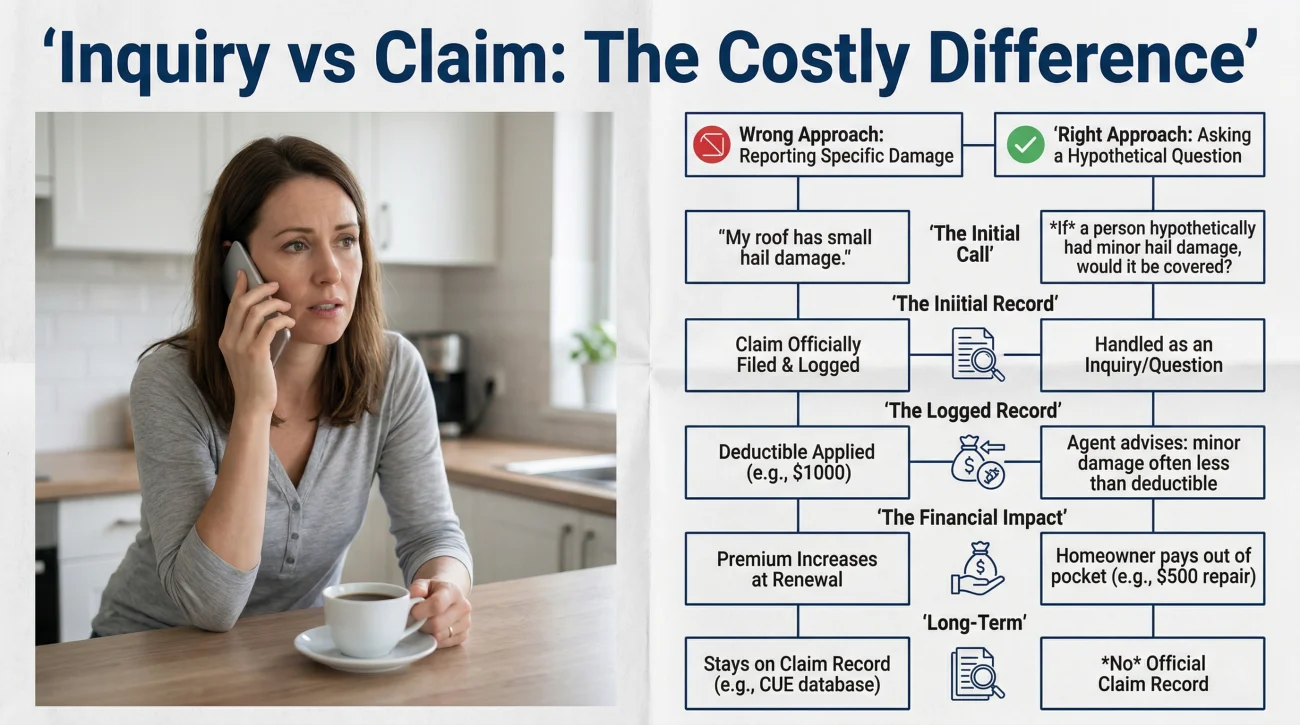

One of the most counter-intuitive traps in the insurance world is the phone call to your agent. Homeowners naturally want to ask their agent for advice before officially starting a stressful process. However, the exact words you use during that call determine whether a permanent record is created.

If you call your carrier’s main 1-800 number and say, “A tree branch fell on my roof, should I file a claim?”, the representative is often required by protocol to open a claim file right then and there. Even if the adjuster comes out the next day and confirms the damage is only $500, falling well below your deductible, the file is closed without payment. You now have a formal denied claim on your record.

I recently reviewed a file where a homeowner was rejected for coverage by a new carrier. They had no idea why. We pulled their database report and found three ‘claims’ listed. All three were zero-dollar claims from their previous insurer where they simply called to ask if a minor leak might be covered. Those casual phone calls severely impacted their risk profile.

Calling the claims department and describing specific damage to your property to find out if it is worth filing.

Asking your local agent a purely hypothetical question about how your policy language handles a certain type of peril, without reporting actual damage to your specific property.

⚠️ Warning: Never file a formal claim just to see if something is covered. If the damage is obviously minor or likely falls below your deductible, getting an independent contractor estimate first will save you from adding a permanent zero-dollar mark to your insurance record.

How Insurers Track Denied Claims on the CLUE Report

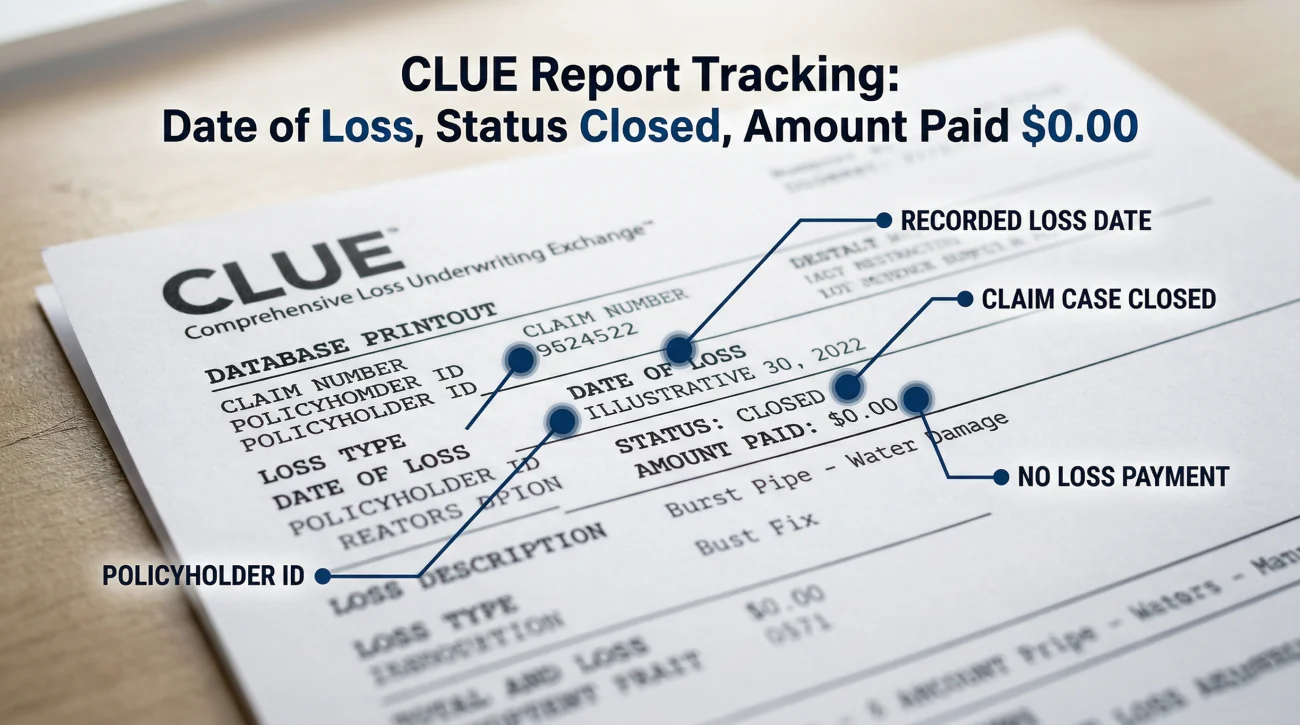

To understand how a denied claim haunts your future, you need to understand the Comprehensive Loss Underwriting Exchange, commonly known as the CLUE report. Managed by LexisNexis, this database is the central nervous system of the property insurance industry. When you apply for a policy, the underwriter pulls your CLUE report to see the claims history for both you as an individual and the physical address of the property over the last five to seven years.

Insurers are generally required to report all filed claims to this database. The critical detail here is the word “filed,” not “paid.” When you open a claim, a file is created. If that claim is ultimately denied, the file is not deleted. Instead, it is closed and updated with specific coding that indicates the insurance company made no financial payout.

Date of Loss: 04/12/2023

Claim Type: Wind/Hail

Status: Closed

Amount Paid: $0.00

Future underwriters do not see a detailed narrative explaining that your claim was denied due to a technicality or a maintenance issue. They simply see that an incident occurred and the carrier paid nothing. This leaves a raw data point on your record that underwriters are trained to view as a potential ongoing risk.

The Risk of Policy Non-Renewal

Beyond premium increases, the more severe consequence of a denied claim is a policy non-renewal. Because underwriters heavily weigh the frequency of incidents over the severity of a single payout, multiple zero-dollar claims can easily make your property look uninsurable.

An underwriter might look past a single massive fire claim because it is a random, catastrophic event. However, I have seen numerous homeowners dropped by their carriers simply because they filed two claims in three years that were both denied or fell slightly below the deductible. The insurer decided that the administrative cost of investigating the claims, combined with the statistical probability of a future payout, made the policy unprofitable.

If you are ever unsure about the root cause of your rejection, it is wise to review the foundational differences in how insurers view these situations in our overview of why home insurance claims are denied before you attempt to file again.

How to Check What Is Actually on Your Record

The most frustrating part of this process for a homeowner is the feeling of operating in the dark. You know you had a claim denied, but you might be getting unusually high quotes from new agents and wondering if that old denial is the invisible anchor dragging down your options. You do not have to guess. You have the legal right to see exactly what the insurance company reported to the national database.

| Step | Action Required |

|---|---|

| 1. Request Report | Visit the LexisNexis consumer portal online or call their automated line to request your free annual CLUE Property report under the Fair Credit Reporting Act. |

| 2. Verify Identity | You will need to provide your Social Security Number, date of birth, and address history to prove you are the property owner. |

| 3. Audit the Data | Look specifically at the “Amount Paid” column and the “Claim Status” column for any incidents you recognize. |

| 4. File a Dispute | If an inquiry was falsely coded as a formal claim, or if the dates are completely wrong, you must file a formal dispute directly with LexisNexis. |

Sometimes, an agent will accidentally code a simple phone inquiry as a formal claim. If you find errors, you must submit a dispute to LexisNexis. They have thirty days to investigate the discrepancy with your insurance carrier. If the carrier cannot verify the accuracy of the data, LexisNexis is legally required to remove the entry from your report.

Switching Insurers With a Denied Claim on Record

If your current insurer raises your rates or drops your coverage, your immediate reaction will be to shop for a new policy. This requires careful handling on your part. New underwriters will want to know why a past claim was filed and why nothing was paid. They do not want to inherit an active problem on the property. Your job is to document that the issue is fully resolved.

Last year, I helped a homeowner who was rejected by three standard carriers. They had a zero-dollar claim from a minor roof leak two years prior. The new underwriters assumed the roof was still leaking. Once the homeowner provided the $800 paid invoice from a roofer proving they fixed it out of pocket, a carrier approved the policy the next day.

“I have a zero-dollar claim on my record from 2022. A tree branch scraped the roof, and the adjuster determined the damage was entirely cosmetic and fell below my $2,000 deductible. The claim was closed without payment. I hired a local contractor to replace the four affected shingles out of pocket. I can provide the paid invoice and current photos of the roof to show the property is fully repaired.”

By providing a clear narrative and proof of repair, you turn a red flag into a minor administrative note. It shows the new underwriter that you are a responsible property owner who maintains the home, rather than a risky prospect trying to hide preexisting damage.

Water Damage: The Ultimate Underwriting Red Flag

Not all denied claims are treated equally. A zero-dollar wind or hail claim is fairly common and easy to explain. However, a denied water damage claim is viewed by underwriters as a massive liability. Unresolved water issues often lead to structural rot, hidden mold, and catastrophic secondary damage.

If you have a denied water claim on your record, simply telling a new insurer that you fixed the pipe is rarely enough. You must provide extensive documentation. This usually includes the original plumber’s invoice, a moisture reading report showing the area was properly dried, and photos of the repaired drywall. Without these, many carriers will outright refuse to issue a new policy, assuming a massive mold claim is waiting for them.

When Is a Denial Worth Fighting?

Because a denied claim leaves a lasting footprint on your insurability, it is vital to ensure that the denial itself is completely valid before you simply accept it and move on. Many homeowners receive a rejection letter and immediately give up. In my experience, initial denials are frequently based on rushed adjuster inspections or misapplied policy language.

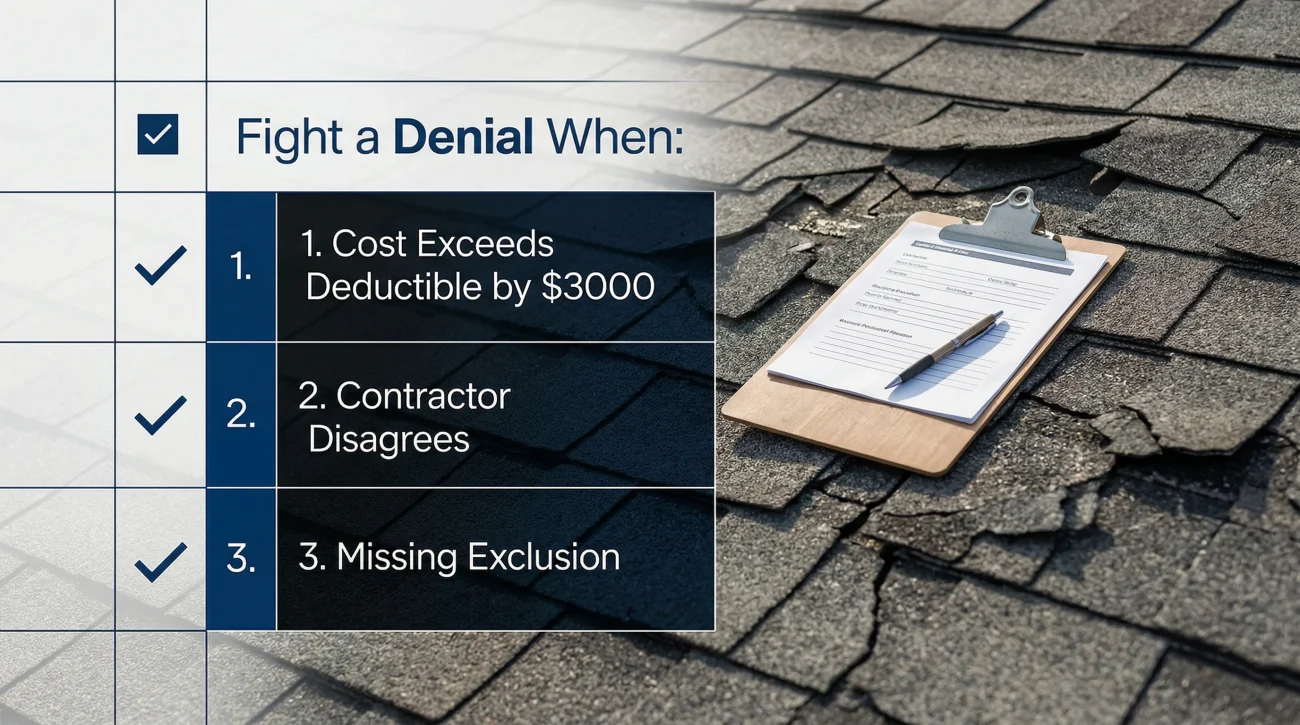

You should strongly consider fighting the denial if you meet any of these thresholds:

- 👉 The out-of-pocket repair cost exceeds your deductible by more than $3,000.

- 👉 Your independent contractor’s assessment directly contradicts the adjuster’s cause of loss (e.g., they say wear and tear, your roofer says fresh wind damage).

- 👉 The denial letter cites a policy exclusion that you cannot actually find in your policy documents.

If the denial is based on a massive gap in how the damage was scoped, do not accept a zero-dollar mark quietly. It is often wise to seek a free claim review from a licensed public adjuster to determine if the insurer missed critical evidence. Successfully reopening the file and securing a settlement changes the nature of the database entry from a frequency warning sign into a standard paid claim.

The 30-Day Action Timeline After a Denial

If you decide your claim might be worth challenging, time is your enemy. The longer a claim sits closed, the harder it is to reopen successfully. Here is the exact timeline I recommend homeowners follow once that zero-dollar letter arrives.

| Timeframe | Action | Details |

|---|---|---|

| Day 1 to 7 | Secure the paper trail | Demand a written explanation citing specific policy sections, and do not make any permanent repairs yet (only temporary mitigation). |

| Day 8 to 14 | Gather counter-evidence | Hire an independent contractor to provide a detailed estimate and written statement regarding the cause of the damage. |

| Day 15 to 30 | Evaluate the gap | Compare the contractor’s evidence to the denial letter. If a clear contradiction exists, decide whether to file a formal appeal yourself or escalate to a professional. |

To understand the complete landscape of your available escalation options and learn how to choose the right path for your specific situation, review our detailed breakdown on how to challenge an unfavorable claim decision.

How Long Does a Denied Claim Stay on Your Record?

If you ultimately decide the claim is not worth fighting or the denial is legitimate, you need to know how long the ghost of that claim will follow you. In the insurance industry, time eventually heals all database wounds. A denied claim, just like a paid claim, will remain visible on your standard CLUE report for up to seven years from the date of the loss.

However, the practical impact of that record diminishes much sooner. Most standard insurance carriers focus heavily on the previous three to five years of your claims history when calculating your premium. An underwriter is generally much more concerned about a denied claim that happened six months ago than one that happened four and a half years ago. As time passes without any new claims activity, the algorithmic weight of that old denial decreases significantly.

Final Steps to Protect Your Insurability

A denied claim is a frustrating experience, but ignoring its backend consequences will only compound the problem. Do not wait for a non-renewal letter to arrive in the mail to find out your risk profile has changed.

The most actionable step you can take today is organizing your documentation. If you were denied, hire a contractor, fix the damage, and create a physical folder containing the before photos, the denial letter, the contractor’s invoice, and proof of your payment. Keep this folder in a safe place. The next time you shop for insurance, this folder will be the only thing standing between you and an underwriter labeling your property as too risky to cover.

❓ FAQ

🕵️ Will insurance go up if a claim is denied?

It can. Many insurers use frequency-based rating models where the simple act of filing a claim, regardless of whether they paid out money, counts against your claims-free discount and can trigger a premium increase.

🤐 What happens if I do not disclose a denied claim to a new insurer?

Hiding it is pointless and dangerous. The new insurer will automatically pull your CLUE report and see the denial. If they discover you intentionally lied on the application, they can legally rescind your policy later, meaning they will not pay future claims.

💳 Does a denied home insurance claim affect my credit score?

No. Insurance claims, whether paid or denied, are tracked on your Comprehensive Loss Underwriting Exchange report, not your financial credit report. It impacts your insurance premiums, but not your ability to get a loan.

🏦 Will my mortgage lender be notified of a denied claim?

Usually, yes. Your lender is listed as a payee on your policy. If a claim is opened and subsequently denied, the carrier will typically send a copy of the closing notice to the lender. If the damage was severe, the lender may require proof that you fixed it.

👨⚖️ Can a public adjuster remove a denied claim from my record?

No one can erase a factually accurate record. A public adjuster cannot “delete” the claim. However, if they successfully appeal the denial and get you a settlement, the database entry changes from a zero-dollar claim to a standard paid claim.

🏠 Will a denied claim stop me from selling my house?

No, it will not prevent a sale, but it can complicate it. A prospective buyer’s insurance company will see the zero-dollar claim on the property’s record. You may need to provide proof to the buyer that the underlying damage was fully repaired out of pocket.

⛈️ Are weather-related denials treated differently than liability denials?

Yes. Underwriters generally view weather denials (like wind or hail) as acts of nature. However, a liability denial (someone got hurt on your property but coverage was denied) is viewed as a severe behavioral risk flag for future lawsuits.

📉 Does a zero dollar payout mean a denied claim?

Usually, yes. A zero-dollar payout on a database report indicates that a file was opened but the insurer paid nothing. This happens due to outright denials or when covered damage falls entirely below your policy deductible.

📞 Does calling my agent count as a claim?

It can, depending on the agent and carrier. If you call to ask about coverage for specific damage and the agent formally logs the inquiry, it can show up on your database report as a zero-dollar claim. Always speak hypothetically if you are unsure.

📄 Can I get a copy of my CLUE report if I am not the current property owner?

No. Under the Fair Credit Reporting Act, you can only request the report for a property you currently own or rent. If you are buying a home, you must ask the current seller to pull the report and share it with you.

A denial sits inside a larger picture. These explain the parts around it.

- How the settlement process works after damage is reported

- Which parts of your policy apply when damage is involved

- How your damage type affects what the insurer is required to pay

- Whether the damage you have is actually worth filing for

- What happens when the claim you filed gets rejected

- How independent representation changes what gets documented

- When a disputed claim moves into legal territory

Not all denials are final. The path forward depends on why it happened.

- Whether your damage assessment left money on the table

- What the inspector who came to your home was actually there to do

- The parts of water damage that standard inspections routinely miss

- What fire and smoke assessments leave out of the scope

- Why the insurer's roof estimate is almost always lower than the roofer's

- When the denial crosses from a dispute into something that needs legal leverage

- Four options to fight back, including one most homeowners never use

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.