- A home insurance denial is rarely a simple “yes” or “no.” It usually falls into one of two distinct categories: a full coverage denial or a partial denial.

- A full denial means the insurer is stating your policy does not cover the event at all. A partial denial means they agree the event is covered, but they are disputing the cost, extent, or cause of specific damage items.

- Knowing your exact denial type is the most critical step you can take, because your dispute options depend entirely on which type of denial you received.

- Formal dispute tools, such as the appraisal process, strictly apply to valuation disagreements (partial denials), not full coverage denials.

- Always read your settlement letter carefully. If there is a check attached for some damage but language rejecting other repairs, you are dealing with a partial denial.

The Confusion of the Settlement Check and the Rejection Letter

One of the most confusing moments for any homeowner navigating the claims process happens at the mailbox. You open an envelope from your insurance company and find a settlement check. Relief washes over you for a brief second, until you look at the amount and realize it covers less than half of what your contractor quoted. Then, you read the attached letter, which explicitly states that certain repairs have been “denied.”

You are left holding a check in one hand and a rejection letter in the other. In my time working through property claims, I have seen hundreds of homeowners freeze at this exact moment. They do not know whether they should cash the check, fight the letter, or start over. They ask themselves if their claim was approved or rejected.

The answer is that it was partially approved and partially denied. There are two fundamentally different types of denied home insurance claims, and they require completely different responses. Most homeowners do not know which type they have, which leads them to use the wrong dispute strategy, waste months of time, and ultimately leave thousands of dollars on the table.

I once reviewed a file where a homeowner spent six months writing angry appeal letters to their insurer over the cost of a roof replacement. They kept demanding to use the appraisal clause. What they failed to realize was that the insurer had issued a full coverage denial citing ‘wear and tear.’ You cannot appraise a claim that the insurer says is not covered in the first place. The homeowner was using the wrong tool for the job.

Before you draft an appeal, hire a professional, or threaten legal action, you must correctly classify your situation. Understanding the full landscape when your home insurance claim is denied begins with separating full coverage rejections from partial scope disputes.

Full Denial vs. Partial Denial: The Practical Difference

To fight back effectively, we have to define exactly what the insurance company is saying in their correspondence. Insurers use highly specific language, and translating that language into plain terms is the first step toward recovery.

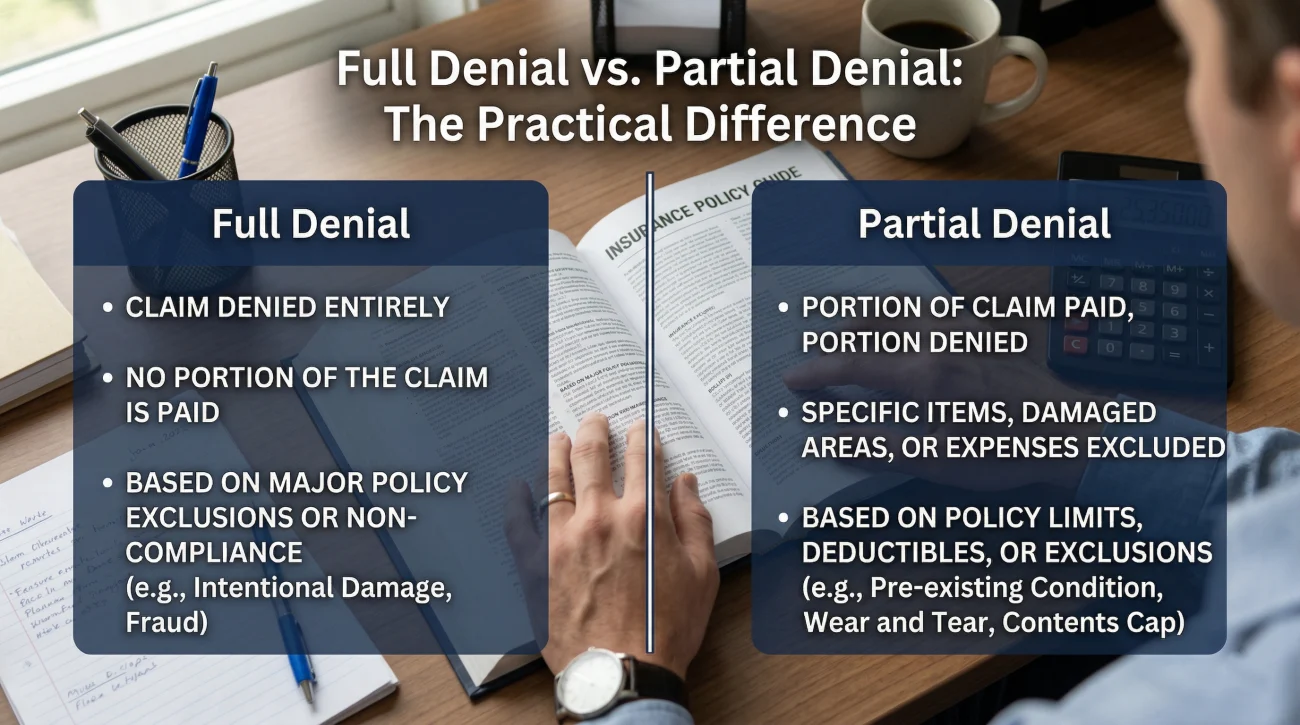

The Full Coverage Denial

A full denial means the insurance company is taking the position that the loss itself is not covered under your policy. They are not arguing about how much the drywall costs; they are stating that they owe you absolutely nothing for this specific event.

Common examples of full denials include a flood claim filed on a standard policy that explicitly excludes flood water, a roof leak where the adjuster determines the sole cause was long-term wear and tear, or a claim denied because the policy had lapsed due to non-payment. In these scenarios, the insurer closes the file without issuing a single dollar.

The Partial Denial (Valuation and Scope Dispute)

A partial denial is entirely different. In this scenario, the insurer acknowledges that a covered event occurred and that your policy applies. However, they are disputing the scope of the damage, the method of repair, or the actual cost to fix it. They will issue payment for what they agree is covered and formally deny the rest.

Common examples include a kitchen fire where the insurer pays to replace the burned cabinets but denies the cost to clean smoke out of the HVAC system, or a water damage claim where they pay to dry the floors but deny the contractor’s request to replace the saturated subfloor. They agree you had a fire or a leak, but they disagree on the math.

“We investigated your roof leak and determined it was caused by age. Your policy excludes wear and tear. No payment will be issued.”

“We agree the storm damaged the front slope of your roof. We are issuing $4,500 for those repairs. We are denying the contractor’s request to replace the rear slope, as we found no storm damage there.”

Why This Distinction Dictates Your Next Move

Knowing your exact denial type is the single most critical step in your recovery because your available dispute paths depend entirely on it. If you choose the wrong path, your dispute will be dismissed on procedural grounds, regardless of how strong your evidence is.

If you have a full coverage denial, your goal is to force the insurer to reverse their legal interpretation of the event. To do this, you might focus on filing a formal internal appeal with new evidence proving the cause of loss, filing a complaint with the Department of Insurance, or engaging legal representation.

If you have a partial denial, you are dealing with a pricing or scope disagreement. This opens up entirely different mechanisms. You can submit a formal contractor supplement to address missing line items. More importantly, a partial denial allows you to consider invoking the appraisal clause. This is a binding dispute resolution process specifically designed for disagreements over the dollar value of a loss, but insurers will immediately reject any attempt to use it if they have issued a full coverage denial.

How to Identify Your Denial Type from the Letter

Insurance letters are notoriously dense, heavily populated with legal jargon and policy citations. However, you do not need a law degree to classify your denial. You just need to look for specific structural clues within the paperwork.

First, look for an attached estimate. If your denial letter comes with a multi-page line-item estimate (often generated by software like Xactimate) and a settlement check, you have a partial denial. The insurer is establishing their version of the repair scope and paying you for it, while rejecting your contractor’s wider scope.

Second, look at the specific phrasing used to reject the disputed items. A partial denial letter will usually list the approved items first, followed by a section detailing what was excluded.

“We have reviewed the estimate submitted by ABC Contracting. We have approved the line items for drywall removal and baseboard replacement. However, we are unable to approve the line items for complete floor replacement, as our adjuster noted the hardwood in the adjacent room was unaffected by the water event. Therefore, this portion of your claim is denied.”

Conversely, a full coverage denial rarely includes an estimate. It gets straight to the point, usually citing a specific exclusion code in your policy booklet. It will state that the investigation has concluded and that the carrier is unable to provide coverage for the loss.

The Scope vs. Coverage Line: Where Things Get Messy

In theory, the line between a coverage dispute and a scope dispute is clear. In practice, the insurance company sometimes blurs this line, creating situations that frustrate even seasoned professionals.

The most important distinction within partial denials is determining whether the insurer is saying your damage is not covered (a mini coverage dispute) or if they agree it is covered but disagree on the cost (a pure scope/valuation dispute). This gray area often appears in matching disputes.

💡 Pro Tip: If the insurer pays to replace three damaged cabinets but refuses to pay for the rest of the undamaged cabinets so they match, are they denying coverage or disputing scope? If they cite a “no matching” endorsement in your policy, they are making a coverage argument. If they argue that the contractor can simply stain the new cabinets to match the old ones perfectly, they are making a scope and valuation argument.

This nuance matters deeply. If the dispute is purely about repair methodology or cost, you can usually proceed directly to a valuation dispute. If the insurer is pointing to specific policy language to exclude an item entirely, you must defeat their policy interpretation before you can argue about the price.

Signs You Might Be Misreading Your Situation

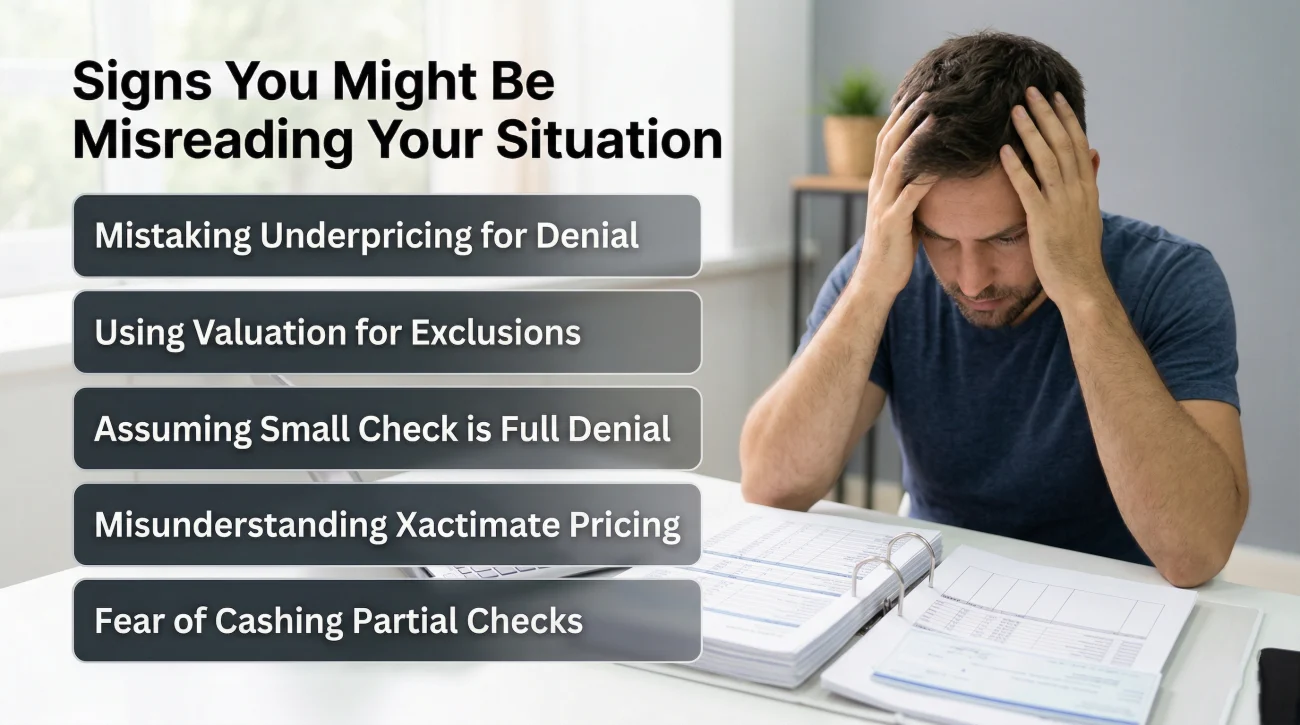

The line between scope and coverage is where most claims get tangled. Misinterpreting the insurer’s position is the fastest way to derail your own recovery. Before you finalize your strategy, review your documentation to ensure you are not making one of these common diagnostic errors.

- 🛑 The Error: You are preparing a formal appeal arguing that your roof has storm damage, but the letter actually approved the storm damage and simply severely underpriced the labor rates.

The Fix: You need a contractor supplement to correct the pricing, not a coverage appeal. Arguing facts the insurer already agreed to wastes time. - 🛑 The Error: You are demanding a formal valuation review to force the insurer to pay your contractor’s invoice, but the insurer’s letter explicitly cited the “earth movement” exclusion.

The Fix: Valuation panels cannot overturn legal exclusions. You must address the cause of loss and defeat the exclusion first. - 🛑 The Error: You believe you received a full denial because the initial check was shockingly small, but the letter actually contains a detailed summary of covered line items.

The Fix: A small check is a low valuation, not a full denial. Do not throw the estimate away; use it as the exact baseline to build your supplement request. - 🛑 The Error: Your contractor is telling you to sue the insurance company for bad faith, when the dispute is actually a standard disagreement over Xactimate unit pricing.

The Fix: Escalate based on the actual roadblock. Most standard pricing software discrepancies can be solved with a well-documented supplement without needing a courtroom. - 🛑 The Error: You are terrified to cash the partial settlement check because you think it means you accept the denial of the remaining funds.

The Fix: In most situations, you can cash undisputed funds to start critical repairs while continuing to fight for the rest. However, you must meticulously check the letter and the back of the check to ensure there is no “full and final release” language printed on it.

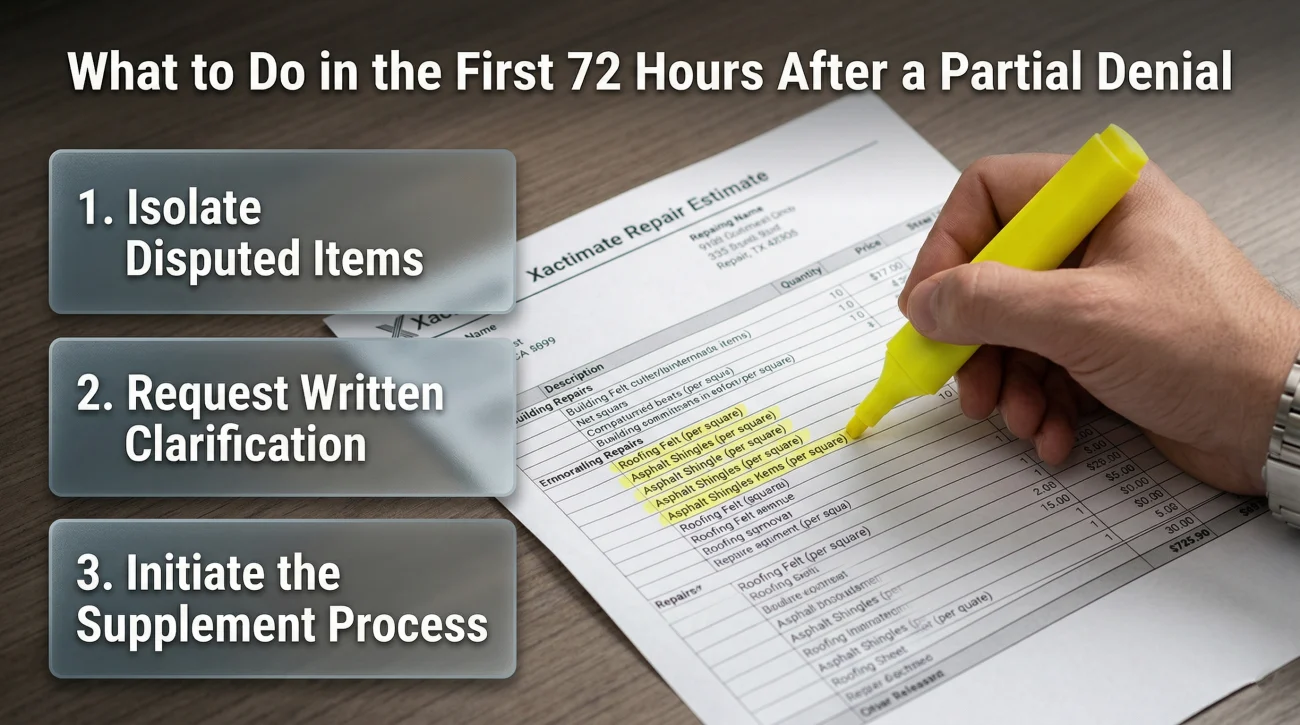

What to Do in the First 72 Hours After a Partial Denial

When that partial settlement packet arrives, taking immediate and organized action sets the tone for the rest of your claim. Here is exactly how to handle a partial denial in the first three days.

First, isolate the disputed items. Put your contractor’s estimate side-by-side with the insurer’s Xactimate estimate. Go line by line with a highlighter. Mark everything the insurer missed, underpriced, or explicitly excluded. This highlighted list becomes your roadmap.

Second, request written clarification for any excluded items. If the insurer dropped a line item without explaining why, email the adjuster immediately and ask: “Is this item excluded due to a specific policy provision, or is it excluded because you do not believe it is necessary for the repair?” Get their answer in writing.

Third, initiate the supplement process. Contact your contractor, provide them with the insurer’s estimate, and ask them to draft a formal Supplement Request. This document should detail the missing scope and include photographic evidence justifying why those specific missing items are required to restore the property.

Choosing the Right Path Based on Your Denial Type

Underpayment and partial rejections are not final, but you have to push back using the correct levers. If you have identified that you are dealing with a partial denial, your focus should be entirely on valuation, scope, and repair methodology.

This is the exact scenario where having a public adjuster review the scope before you accept the final numbers is highly effective. Instead of arguing legal principles, a licensed public adjuster takes your contractor’s real-world estimate and translates it into a formal Supplement Request using the exact billing codes the insurer uses. They identify missing line items, address overhead and profit gaps, and formally present the valuation dispute to the carrier on your behalf.

On the other hand, if you are staring at a full coverage denial, or a partial denial where the insurer is clearly misrepresenting your policy terms to avoid a massive payout, your strategy must shift toward policy enforcement. In cases involving potential bad faith or complex coverage interpretation, consulting an insurance claim attorney is often the most appropriate step.

Final Thoughts on the Claim Assessment

When an insurance company issues a partial denial and a small check, they are simply establishing their opening position on the value of your loss. They are banking on the complexity of the paperwork to make you accept that initial payment and walk away.

You do not have to accept an incomplete scope of repair. By carefully reading your settlement breakdown and confirming you are fighting a valuation gap rather than a full coverage exclusion, you take control of the narrative. Pinpoint the missing line items, structure your supplement correctly, choose the right response for that specific job, and seek a complete look at all available escalation paths after a denial to ensure your home is restored properly.

❓ FAQ

📄 What is a partial claim denial homeowners insurance?

A partial denial occurs when your insurance company accepts that a covered event happened but refuses to pay for certain line items, disputes the extent of the damage, or disagrees with your contractor’s repair costs.

💸 Why did my home insurance pay less than expected?

This usually happens because the adjuster’s pricing software underestimated local labor rates, they missed hidden damage during their visual inspection, or they applied heavy depreciation to your older property.

❌ Can an insurance company partially approve a claim?

Yes. It is very common for an insurer to approve the immediate emergency cleanup costs but partially or fully deny the subsequent reconstruction costs if they believe the repair scope is inflated.

⚖️ What is the difference between a scope dispute and a coverage dispute?

A scope dispute is an argument over how much material and labor is needed to fix covered damage. A coverage dispute is an argument over whether the policy actually covers the damage in the first place.

📝 My insurance denied part of my claim, what should I do?

First, review the adjuster’s line-item estimate against your contractor’s estimate to find the exact discrepancies. Then, submit a formal supplement request with your contractor’s documentation to challenge the missing items.

📉 Is an underpaid claim the same as a partial denial?

Functionally, yes. An underpaid claim means the insurer approved the loss but partially denied the full financial cost required to restore the property to its pre-loss condition.

🛑 Does a full denial mean I get absolutely nothing?

Yes, a full coverage denial means the insurer will not issue any payment for the claim. To get paid, you must successfully appeal the decision or pursue legal action to overturn the coverage interpretation.

🔨 Can I fix the approved items while fighting the partial denial?

In many cases, yes. You can usually cash the initial undisputed settlement check to begin critical repairs while formally disputing the denied items, but always verify there is no restrictive “final settlement” language attached to the check.

🤝 Can I use the appraisal process for a full coverage denial?

No. This mechanism is strictly for valuation and scope disputes. If the insurer has denied coverage entirely, the panel has no legal authority to force them to accept the claim.

⏳ How long do I have to dispute a partially denied claim?

The window to dispute a partial denial or file a supplement varies strictly by policy. Check your specific policy declarations for your exact deadline.

A denial sits inside a larger picture. These explain the parts around it.

- How the settlement process works after damage is reported

- Which parts of your policy apply when damage is involved

- How your damage type affects what the insurer is required to pay

- Whether the damage you have is actually worth filing for

- What happens when the claim you filed gets rejected

- How independent representation changes what gets documented

- When a disputed claim moves into legal territory

Not all denials are final. The path forward depends on why it happened.

- Whether your damage assessment left money on the table

- What the inspector who came to your home was actually there to do

- The parts of water damage that standard inspections routinely miss

- What fire and smoke assessments leave out of the scope

- Why the insurer's roof estimate is almost always lower than the roofer's

- When the denial crosses from a dispute into something that needs legal leverage

- Four options to fight back, including one most homeowners never use

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.