- A denial letter is not just a rejection notice. It is a highly structured legal document that outlines the exact foundation of the insurance company’s position.

- By law, the letter must cite the specific policy language and exclusion clauses the adjuster is using to deny your payout.

- Most denials fall into four categories: coverage exclusions, insufficient documentation, procedural lapses, or investigation findings.

- You must locate your dispute window printed in the letter immediately. If the mail was delayed, keep your postmarked envelope as proof.

The First Read and The Emotional Trap

I have reviewed hundreds of denial letters handed to me by frustrated, exhausted homeowners. Usually, we are sitting at their kitchen table, and they are holding the document like it is a final verdict. I watch them fall into the exact emotional traps the insurance company anticipates. Some immediately pick up the phone to yell at the desk adjuster without a plan, handing over recorded statements that hurt their case. Others just throw the letter in a drawer because they are too stressed to deal with it, quietly letting their appeal window expire.

If you are holding a denial letter right now, I need you to pause. Do not dial that 800-number yet. A denial letter is not simply a “no.” It is a map. It tells you exactly what the insurance company thinks happened, exactly which paragraph of your massive policy booklet they are hiding behind, and exactly what kind of evidence you will need to break their argument apart.

Before you can decide what to do next, you have to decode what the document actually says. Let us translate the insurance jargon into plain English so you can spot the specific flaws in their reasoning.

What the Adjuster is Required to Tell You

Despite how absolute that letter feels, insurance companies cannot just stamp “Denied” on your file and walk away. Because claims handling practices are strictly regulated, every valid denial letter must contain a few specific elements by law, even if the formatting looks different from carrier to carrier.

When you read through the document, you should be able to easily identify a clear, written reason for the rejection. The adjuster cannot rely on vague statements like “this does not meet our criteria.” They must point to something concrete.

Second, they are required to copy and paste the exact policy language they are using to justify their decision. If they say your claim is denied due to earth movement, the letter must include the paragraph from your policy that excludes earth movement.

Finally, the letter must outline your rights to dispute the decision and provide a timeline for doing so. If any of these elements are missing, the letter itself may be procedurally flawed.

Identifying Your Specific Type of Denial

Not all rejections are the same. In my experience reviewing claim files, almost every letter falls into one of four distinct categories. Identifying which category you are in is the most important part of reading the letter.

1. The Coverage Exclusion

This is the most common type. The letter will state that the specific peril (the cause of the damage) is explicitly not covered by your contract. Common examples include flood damage on a standard policy, or earth movement. The letter is basically saying: “Even if your damage is real, you never bought the specific product that covers this event.”

2. Insufficient Documentation

Sometimes, the letter denies the claim not because the event is excluded, but because the adjuster claims you did not prove your case. They might state that you failed to provide a timely inventory list, or that your photos do not clearly show the origin of a water leak.

A common tactic I see is an adjuster issuing a denial based on ‘insufficient evidence of sudden damage.’ Homeowners read this and think their policy is worthless. In reality, the insurer is just saying you haven’t given them enough proof yet. This type of denial is often highly reversible if you know what documents to send.

3. Policy Lapse or Premium Issue

This is a procedural denial. The letter will claim that your policy was not active on the exact date the damage occurred, usually due to a missed premium payment or a cancelled policy. This has nothing to do with the damage itself and everything to do with billing records.

4. Investigation-Based Denial

This occurs when the insurer has investigated the site and determined the damage was caused by something you did or failed to do. The letter might use terms like “negligence,” “failure to mitigate,” or state that the damage was a long-term wear and tear issue rather than a sudden storm event.

This is the most highly disputed category of all denials. Adjusters frequently look at wind-lifted roof shingles and classify them as “age-related deterioration.” They are arguing about the timeline of your property. To beat this denial, you must shift the focus back to the sudden event by using independent contractor reports and historical weather data to prove exactly when the damage occurred.

How to Decode the Cited Policy Language

The most intimidating part of the letter is usually page two or three, where you see a massive block of legal text pulled directly from your policy. It usually looks something like this:

When you see a block like this, do not panic. Your first job is to pull out your actual, physical policy booklet (or the PDF version) and look up that exact section. You need to verify two things.

First, does that section actually exist in your specific policy? Insurance companies use templates, and desk adjusters sometimes copy and paste exclusions from standard policy forms that do not match the specific endorsements you purchased.

Second, you need to ask yourself if the language actually describes what happened to your house. If the letter cites “mechanical breakdown” but a heavy tree limb clearly smashed your HVAC unit, the adjuster has applied the wrong language to the physical evidence. Your counter-argument here is not about debating contract law; it is about providing clear photos of the impact zone to prove the adjuster’s baseline assumption is entirely wrong.

💡 Pro Tip: If the letter is filled with dense jargon and you cannot tell if the cited exclusion accurately applies to your specific physical damage, getting a professional second opinion from a licensed public adjuster can clarify the language before you make your next move.

Once you understand why they are denying the claim, the next critical piece of information is figuring out how long you have to fight it.

Locating Your Appeal Deadline

Somewhere in that letter, usually near the very end, there will be a sentence regarding your right to dispute the decision. Finding this sentence is the most time-sensitive task you have.

The phrasing will often say something like: “If you disagree with this determination, you may submit additional information for review within 30 days of the date of this letter.”

Assuming you have 30 days from the day you opened the envelope to figure out your response.

Checking the date printed at the very top of the letter, and circling the date 30 days from then on your calendar.

The clock almost always starts on the date the letter was drafted and mailed, not the date it arrived in your mailbox. If the letter got delayed in the mail for a week, you have already lost seven days of your response window.

If the letter arrived weeks late and you have already missed the printed window, do not panic and do not assume your claim is dead. Keep the postmarked envelope as proof of transit delay. You can often force the window back open by submitting that envelope and demanding a formal extension.

Signs Your Denial Letter Contains Errors

Because these letters are often generated using templates by desk adjusters handling hundreds of files, they are prone to mistakes. Here are the clearest signs that the letter you are holding is fundamentally flawed:

- ❌ The cited exclusion does not match your policy: The letter quotes a policy section that literally does not exist in your actual declarations page or policy booklet.

- ❌ The section numbers are wrong: The letter references “Section I – Exclusion B” to deny a roof leak, but in your booklet, Exclusion B is about nuclear hazards.

- ❌ The damage description is vague: The letter says “we do not cover the damage to your property” without specifying whether they mean the drywall, the flooring, or the roof.

- ❌ The appeal deadline is missing: The letter states the claim is closed but fails to provide any timeline or instructions for submitting a dispute.

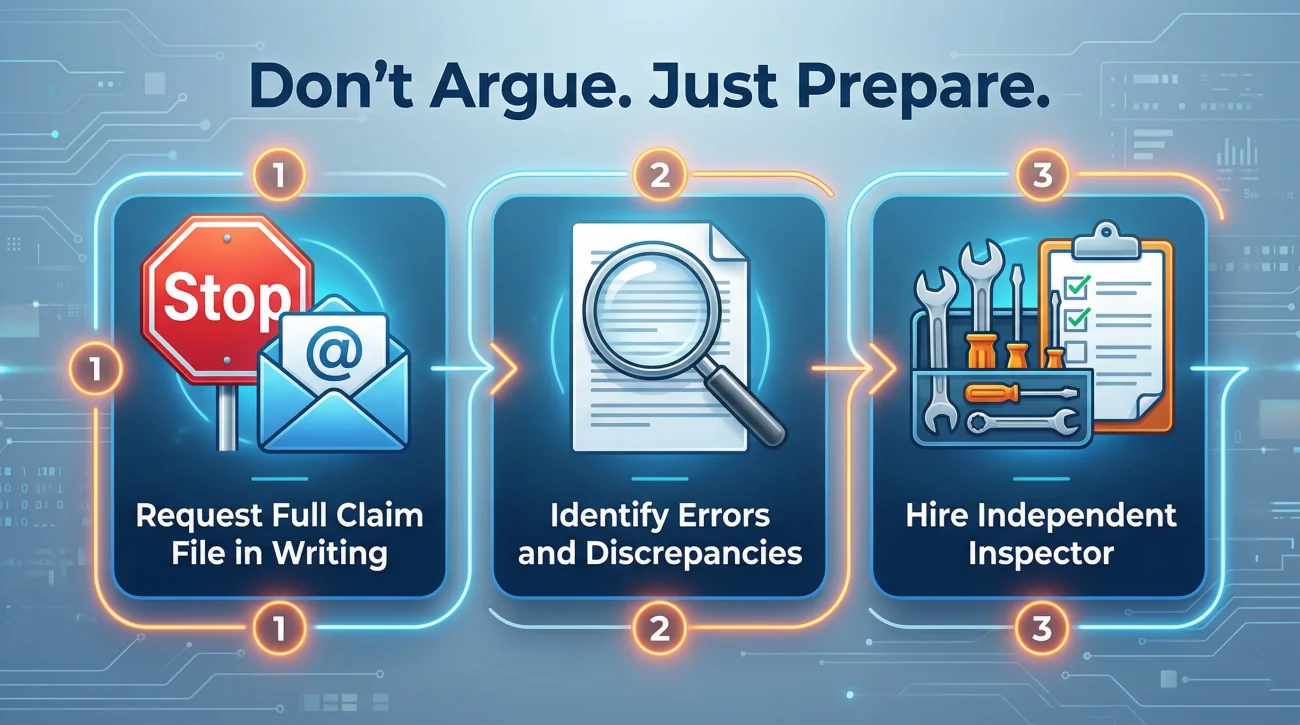

The First 24 Hours After Reading the Letter

Now that you have decoded their reasoning and found your deadline, you need to transition from reacting to preparing. Here is exactly what you should do in the first 24 hours after opening that envelope.

- 🛑 Step 1: Do not call to argue. Anything you say on a recorded line right now can be used to solidify their denial. Keep all future communication strictly in writing.

- 🛑 Step 2: Request your full claim file. Reply via email asking for the adjuster’s full unedited report, all photos they took, and their exact field notes. You have a right to see the evidence they used against you before you file an appeal. You will use this file to find exact inconsistencies between what the adjuster saw on-site and their final denial reason.

- 🛑 Step 3: Get an independent assessment. If their logic does not match your reality, choosing the right strategy to fight the decision requires a second professional opinion. Have an independent contractor or public adjuster document the site before you clean anything up or make permanent repairs.

Final Thoughts

A denial letter is intentionally designed to look like the absolute end of the road. But in reality, it is simply the insurance company putting their opening argument down on paper. Do not let the dense formatting, the cited legal codes, or the “claim closed” stamp intimidate you into walking away. By taking the time to decode their exact reasoning and mapping out a response plan, you take the control back. Protect your deadline, gather your evidence, and remember that you always have the right to push back.

❓ FAQ

📄 What does “peril not covered” mean in my letter?

It means the insurance company believes the specific event that caused your damage (like a flood or an earth tremor) is explicitly excluded from your policy contract.

📅 Does the appeal clock start when I receive the letter?

Generally, no. The timeline usually begins on the date printed at the top of the letter. If mail delays caused you to miss this window, you must retain the postmarked envelope to prove the insurer delayed the notification.

🔍 Why did they quote a policy section I cannot find?

Adjusting software often auto-populates exclusions. If the cited paragraph is genuinely missing from your policy booklet, the denial lacks a contractual basis and is highly vulnerable to being overturned.

📝 What does “insufficient evidence” mean if I sent photos?

It means your photos likely documented the resulting damage, but failed to prove the original cause of the loss to the adjuster’s satisfaction.

🛑 Is a denial letter the absolute final decision?

No. A denial letter is the insurance company’s initial determination based on their first review. It can frequently be overturned with new evidence or professional representation.

📖 Do I need to read my whole policy to understand the letter?

No. You only need to locate and carefully read the specific section numbers and paragraphs that the adjuster cited in the denial letter.

⏱️ What happens if my letter has no deadline listed?

If the letter lacks an appeal deadline or dispute instructions, it may be procedurally flawed. You should request your dispute rights in writing immediately.

🏚️ Why does my letter say “wear and tear” for storm damage?

The insurer is arguing that your property was already deteriorating before the storm hit, and that age, not the weather, is the primary reason the materials failed.

⚖️ Does “under investigation” mean I am being accused of fraud?

Not necessarily. While it can relate to fraud, it often just means the insurer has paused the claim to verify your policy timeline, coverage limits, or cause of loss.

✉️ Should I call the adjuster to argue about the letter?

Verbal conversations leave no paper trail and can easily be misrepresented later. It is always safer to communicate exclusively in writing so every piece of evidence and policy question is permanently documented in your claim file.

A denial sits inside a larger picture. These explain the parts around it.

- How the settlement process works after damage is reported

- Which parts of your policy apply when damage is involved

- How your damage type affects what the insurer is required to pay

- Whether the damage you have is actually worth filing for

- What happens when the claim you filed gets rejected

- How independent representation changes what gets documented

- When a disputed claim moves into legal territory

Not all denials are final. The path forward depends on why it happened.

- Whether your damage assessment left money on the table

- What the inspector who came to your home was actually there to do

- The parts of water damage that standard inspections routinely miss

- What fire and smoke assessments leave out of the scope

- Why the insurer's roof estimate is almost always lower than the roofer's

- When the denial crosses from a dispute into something that needs legal leverage

- Four options to fight back, including one most homeowners never use

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.