- Water claims trigger higher rate surcharges and stricter underwriting flags on your CLUE report compared to most other types of property damage.

- Filing for minor water damage that barely clears your deductible is the most common financial mistake homeowners make, often costing more in future premiums than the payout received.

- The hidden nature of water damage means you should never file based on what you can see on the surface; getting a professional scope assessment first is critical.

The Water Damage Dilemma: More Than Just a Wet Floor

I have sat across from insurance adjusters on hundreds of property claims, and I can tell you that water damage is the most common reason a homeowner picks up the phone to call their carrier. It is also the claim type where the decision to file is most often made in a panic, without calculating what it will actually cost over the next few years.

When you are staring at a ruined ceiling or a flooded kitchen, the instinct is to file immediately. You pay your premiums for exactly this reason, right? But deciding whether you should file a home insurance claim for water damage requires pausing to look at the math. A rushed decision can lead to a tiny settlement check followed by years of rate hikes, or worse, being dropped by your carrier entirely.

Before we look at the numbers, we need to clarify one thing: this guide is about the financial decision to file. It assumes your water damage is actually from a covered peril, like a sudden burst pipe or an accidental appliance overflow. If you are dealing with a slow, gradual leak that went unnoticed for months, or outside flood water, you are dealing with a coverage question first. But if you have a sudden water event and you are wondering if it is worth putting on your record, you are in the right place.

I want to walk you through the exact variables I use when advising homeowners on whether a water claim is actually worth the long term cost.

Why Water Claims Are Treated Differently by Insurers

You might think a $5,000 water claim and a $5,000 wind claim are the same in the eyes of your insurance company. They are not. Underwriters treat water claims with a specific kind of caution, and this directly impacts your filing decision.

First, water claims typically carry a higher rate impact than other types of damage. Insurers know that water often leads to secondary issues like mold, structural rot, or repeated failures if the plumbing system is aging. Because of this perceived ongoing risk, the premium surcharge applied to your policy at renewal is often steeper for a water event. Furthermore, state insurance departments typically allow carriers to keep this surcharge on your policy for three to five years, making the long term financial penalty inescapable.

Second, there is the CLUE report factor. Your Comprehensive Loss Underwriting Exchange report tracks your claims history. Water damage entries on a CLUE report are specifically flagged by many carriers when they are deciding whether to write a new policy. If you file a water claim today and try to switch insurance companies in two years to find a better rate, you may find that standard carriers will decline your application entirely, forcing you into high risk, expensive non standard markets.

I frequently review files where a homeowner filed a water claim for a minor toilet overflow, received a $1,200 payout after their deductible, and then found themselves entirely uninsurable by standard carriers when they tried to move houses two years later. The short term payout rarely justifies the long term penalty.

In many cases, the combination of losing your claim free discount and taking on a water specific rate surcharge means you will pay back the cost of a minor water claim to the insurance company anyway.

The ACV Trap: Calculating Your Real Deductible Math

Most homeowners know they need to compare the repair cost to their deductible. If the repair is $4,000 and the deductible is $1,000, filing makes sense, correct? Not always. This is where the Actual Cash Value (ACV) calculation catches people off guard.

If your policy, or the specific endorsement covering the damaged area, applies ACV rather than Replacement Cost Value (RCV), the insurer will apply depreciation based on the age and condition of the damaged materials before applying your deductible.

Assuming a $5,000 repair estimate minus a $1,000 deductible equals a $4,000 settlement check from the insurance company.

Understanding that a $5,000 repair on 15 year old hardwood floors might be depreciated by 50%. The $2,500 ACV minus your $1,000 deductible leaves a net payout of only $1,500.

When you realize the net payout might only be $1,500, the decision to file becomes much harder. This is why you must check your policy declarations page to confirm your deductible type and how depreciation will be handled before you file.

When to File vs When to Absorb the Cost

To make this practical, I divide water claims into clear categories. While every situation is unique, these are the baseline thresholds I use when evaluating a new client’s file.

When Water Damage is Almost Always Worth Filing

If you hit any of these criteria, the repair costs will almost certainly outpace the long term premium penalties, making a claim necessary:

- Multiple rooms or floors affected: If water traveled from a second floor bathroom down through the ceiling into the living room, the mitigation and drywall replacement costs will be massive.

- Habitability is compromised: If the home requires a professional dry out, your kitchen is unusable, or you need temporary housing, you need to file.

- Custom or high end finishes are ruined: Solid hardwood floors, custom cabinetry, and high end tile are incredibly expensive to replace.

- Category 3 water (sewage): Any sewage backup requires specialized biohazard cleanup, tear out, and sanitization. This is never a cheap DIY fix.

When to Think Carefully Before Filing

These are the marginal scenarios where you should heavily consider absorbing the cost:

- The damage is isolated and visible: A leaky supply line under the sink that only damaged a small piece of easily accessible particle board.

- You already had a claim recently: In my experience, if this is your second claim of any type within a three to five year window, filing puts you at extreme risk for a non renewal letter. I recently reviewed a case where a homeowner filed a $1,500 water claim two years after a hail claim, and their carrier dropped them at the next renewal. Insurers view multiple claims as a behavioral pattern of risk, not bad luck.

Three Red Flags That Should Pause Your Claim

When I sit down with homeowners who are panicking over a wet floor, I look for three specific red flags that tell me we need to pause and rethink the filing strategy immediately.

1. The Percentage Deductible Surprise

I frequently talk to homeowners who assume they have a standard $1,000 deductible, only to discover they have a percentage deductible. If your home is insured for $400,000 and you have a 1% water deductible, your out of pocket threshold is actually $4,000 before the insurer pays a single dime. Filing for a $3,500 repair in this scenario simply puts a zero payout claim on your permanent record.

2. You Cleaned Up Before Documenting

I see this fatal mistake every single week: a homeowner panics, tears out the wet carpet, throws away the ruined baseboards, mops everything up, and then calls the insurance company. By destroying the evidence before taking comprehensive photos and writing down exactly what happened, you give the adjuster grounds to deny the severity of the claim. If you have already removed all evidence of the damage, filing a claim now will likely result in a heavy dispute.

3. You Plan to Sell the House Soon

As we discussed regarding the CLUE report earlier, a water claim follows the property, not just you. If you are planning to sell your house in the next year or two, buyers and their insurance agents will pull that report. A recent water claim can scare off buyers or make the home difficult for them to insure, complicating your sale over a minor repair you could have afforded out of pocket.

Final: Your Immediate Action Plan

The water damage filing decision is complex, but the steps you should take right now are straightforward. Do not let the stress of the moment push you into an impulsive decision.

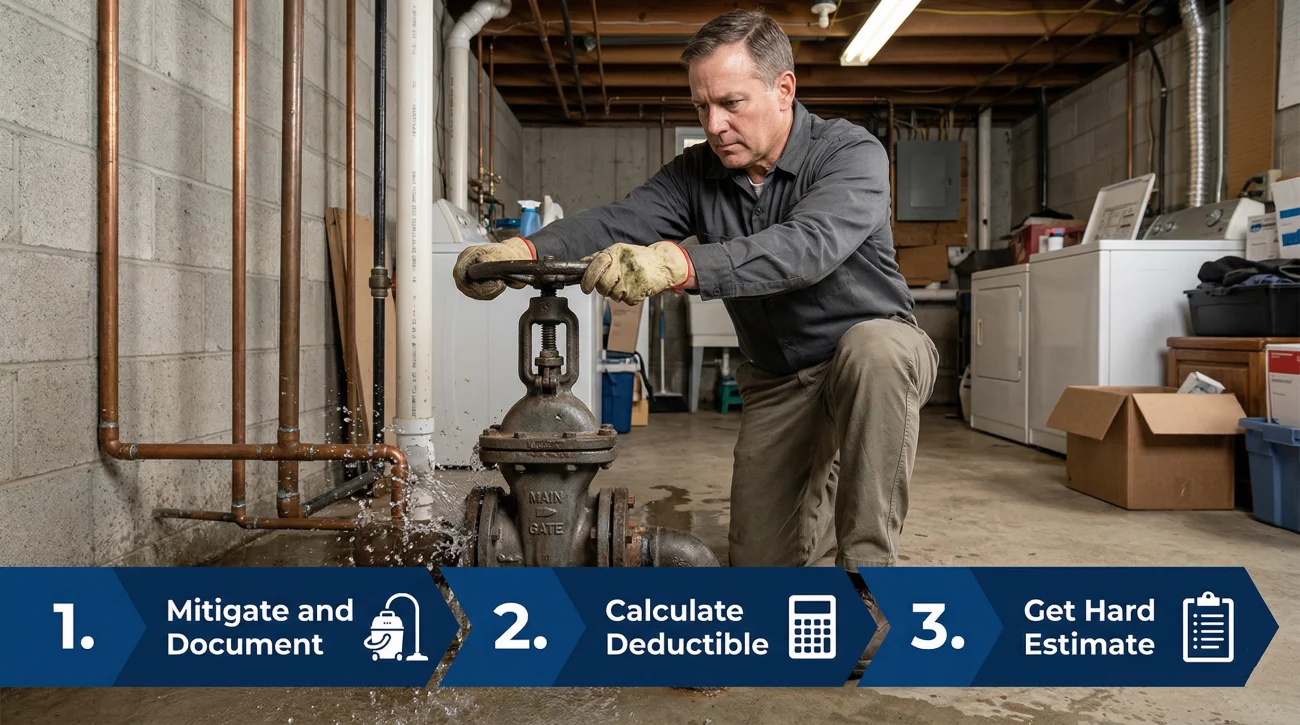

Step 1: Mitigate and Document. Turn off the main water valve immediately. Before you remove any ruined materials, take wide photos of the entire room and close up photos of the source of the water. Emergency mitigation protects the home and preserves your right to claim later without risking evidence destruction.

Step 2: Do the Math. Pull your policy declarations page right now. Find your exact deductible amount and check if your personal property and dwelling are covered at Replacement Cost or Actual Cash Value.

💡 Pro Tip: Never file a claim just to see what the insurance company will say. The moment you call and describe the damage, it is recorded as an inquiry or a claim, which can impact your rates even if you withdraw it later.

Step 3: Get a Hard Dollar Estimate. Before dialing the claims hotline, you need exact numbers. Have an independent professional inspect the property with a moisture meter to map the hidden water. Once you have a written repair estimate, run it through the full filing decision framework. Compare that exact dollar figure against your ACV depreciation, your percentage deductible, and the potential three year rate surcharge.

Get the facts, assess the scope, and make the decision that actually protects your financial future.

❓ FAQ

💧 Should I report a minor water leak to my home insurance?

Usually no. If the repair cost is close to or below your deductible, reporting it can still place a claim on your CLUE record and trigger rate increases without yielding any financial payout.

📈 How much will my insurance go up after a water damage claim?

While it varies widely by state, industry rate analyses often show that a single water claim can increase your rates by 10% to 30%, and state regulators typically allow carriers to keep this surcharge on your policy for three to five years.

🧮 Is it worth claiming for water damage under my deductible?

Never. If the damage is under your deductible, the insurer will pay nothing, but the claim will still be recorded on your loss history, negatively affecting your future rates and insurability.

🏚️ What happens if I fix water damage myself without telling insurance?

If you repair minor damage out of pocket, you preserve your claim free discount and keep your record clean. However, ensure the repair is done correctly, as insurers will not cover future damage caused by faulty DIY repairs.

🕒 How long do I have to file a water damage claim?

Most standard policies require you to file within one year of the date of loss, though some allow up to two years. Check your specific policy declarations for the exact timeline.

❌ Can my insurance drop me for filing one water claim?

While rare for a single, small claim, insurers can issue a non renewal notice if the water claim is large, if you live in a high risk market, or if it is your second claim of any type within a three to five year window.

📝 What if I file a water claim and then change my mind?

You can withdraw a claim before payout, but the fact that you opened the claim or even called to inquire about it may still remain on your CLUE report as a zero pay claim or an inquiry.

🔍 Do adjusters look for hidden water damage?

Company adjusters will look for visible signs, but they often rely on moisture readings provided by mitigation companies. They generally will not tear open dry walls without evidence, which is why independent scope assessments matter.

💰 Does a water damage claim affect my home’s resale value?

The damage itself might not if repaired properly, but the claim stays on the property’s CLUE report for up to seven years. This can make the home more expensive for a potential buyer to insure.

☔ Should I file a claim if a pipe burst but the damage seems small?

Before filing, get a professional to check for hidden moisture. A seemingly small burst pipe often saturates wall cavities and insulation, meaning the actual damage is much higher than what is visible.

Filing is just the beginning. These cover what the rest of it looks like.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

That gap is common and usually closeable. These explain how.

- 5 patterns that signal your settlement is probably short

- Who the adjuster at your door actually works for

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When a denial needs legal leverage, not just negotiation

- Four paths to fight a denial, including one most homeowners miss

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.