- Your claim check may include your mortgage company’s name because they have a legal financial interest in the property, requiring you to work with their loss draft department to access funds.

- If your check is larger than your repair costs, you can often keep the difference, but doing so on an RCV policy usually means forfeiting your final depreciation holdback payment.

- Accepting a lump sum cash settlement typically closes your claim permanently, blocking you from requesting supplements if hidden damage is discovered later.

Decoding Your Claim Payment: What to Do When the Check Arrives

If you are holding your settlement check right now, you are entering the final stages of the standard claim resolution timeline. But before you take that check to the bank, you need to understand exactly what accepting those funds means for your property and your legal rights regarding the damage.

In my time reviewing property claims, I have seen many homeowners stare at their payout in confusion. Sometimes the check has multiple names printed on it. Other times, it is surprisingly larger than the contractor’s estimate, leaving the homeowner wondering if they can legally pocket the difference. And frequently, it comes with complicated release language that makes people afraid to deposit it at all.

Receiving the payment does not always mean the process is completely over. The way you handle this piece of paper determines whether your repairs move forward smoothly or get stalled in administrative bottlenecks.

Why Your Claim Check Is Made Out to You and Your Mortgage Company

One of the most common surprises for a homeowner is seeing their lender’s name printed right next to theirs on the payout check. If you have a mortgage, your lender has an “insurable interest” in your home. To the bank, your house is the collateral for their loan.

To protect their investment, mortgage agreements contain a clause requiring the lender to be named on any insurance payouts over a certain dollar amount. This ensures you actually use the money to fix the house, rather than spending it elsewhere and leaving the bank with a damaged asset.

I frequently see homeowners delay their own repairs by weeks simply because they endorsed the check and dropped it in the mail to their mortgage company without calling first. The check sits in a mailroom because there was no claim number or loss draft packet attached to it.

Navigating the Loss Draft Department

When a check has both names on it, you cannot just deposit it into your personal checking account. You have to go through your mortgage company’s “loss draft” department, a team that handles insurance payouts for mortgaged properties. Here is the safest way to handle it without delaying your repairs:

Call Loss Draft Dept + Request Required Doc List + Endorse Check + Send via Tracked Mail

- Step 1: Call your mortgage servicer and ask for the loss draft department.

- Step 2: Ask for their exact checklist. They will usually require the adjuster’s estimate, a signed contractor contract, and an endorsed claim check.

- Step 3: Ask how the funds will be released. For smaller claims, they might endorse the check and send it back to you. For larger claims, they will put the money into an escrow account and release it in portions (like 33% upfront, 33% halfway, and the rest upon final inspection).

⚠️ Warning: Never send your original, endorsed check to your mortgage company without a tracking number. If it gets lost in standard mail, having the insurance company stop payment and reissue a dual-party check can take weeks.

What to Do When the Mortgage Company Holds Funds Too Long

Sometimes you provide all the required documents, but the mortgage company still stalls the release of your funds, leaving your contractor unpaid and your home vulnerable. If you are stuck waiting for weeks, you need to escalate the issue.

Start by requesting a supervisor in the loss draft department to manually review your file. If they are unresponsive, file a formal complaint with the servicer’s customer advocacy team. If the delay stretches into unreasonable territory and halts your repairs, filing a complaint with the Consumer Financial Protection Bureau (CFPB) can prompt a formal review of your case by the lender’s executive resolution team.

What to Do If the Check Is Too Low (The Underpayment Gap)

It is incredibly common to receive a settlement check that is significantly lower than your contractor’s repair quote. When this happens, homeowners often panic, assuming they have to pay the difference out of pocket. In reality, a low check is usually just a partial payment resulting from missing items on the adjuster’s initial scope.

Before you argue with the adjuster over the final dollar amount, you have to find out exactly where the gap is. Look at the line-item estimate the insurance company sent with the check (usually an Xactimate report). Compare it side by side with your contractor’s bid.

You are looking for specific omissions. Adjusters frequently undercount items that are obvious to contractors but invisible on a standard form. Did the adjuster include the cost of removing the debris? Did they account for the current local market price of drywall? Did they include overhead and profit? Identifying these specific missing line items is the key to requesting a supplement. For a deeper breakdown of why these gaps happen, see our guide on how to handle an adjuster estimate that falls short.

What If the Check Is More Than Your Repair Cost?

Occasionally, you might find a contractor willing to do the repairs for less than the amount your insurance company paid out. This immediately leads to the question of whether you can keep the excess claim money.

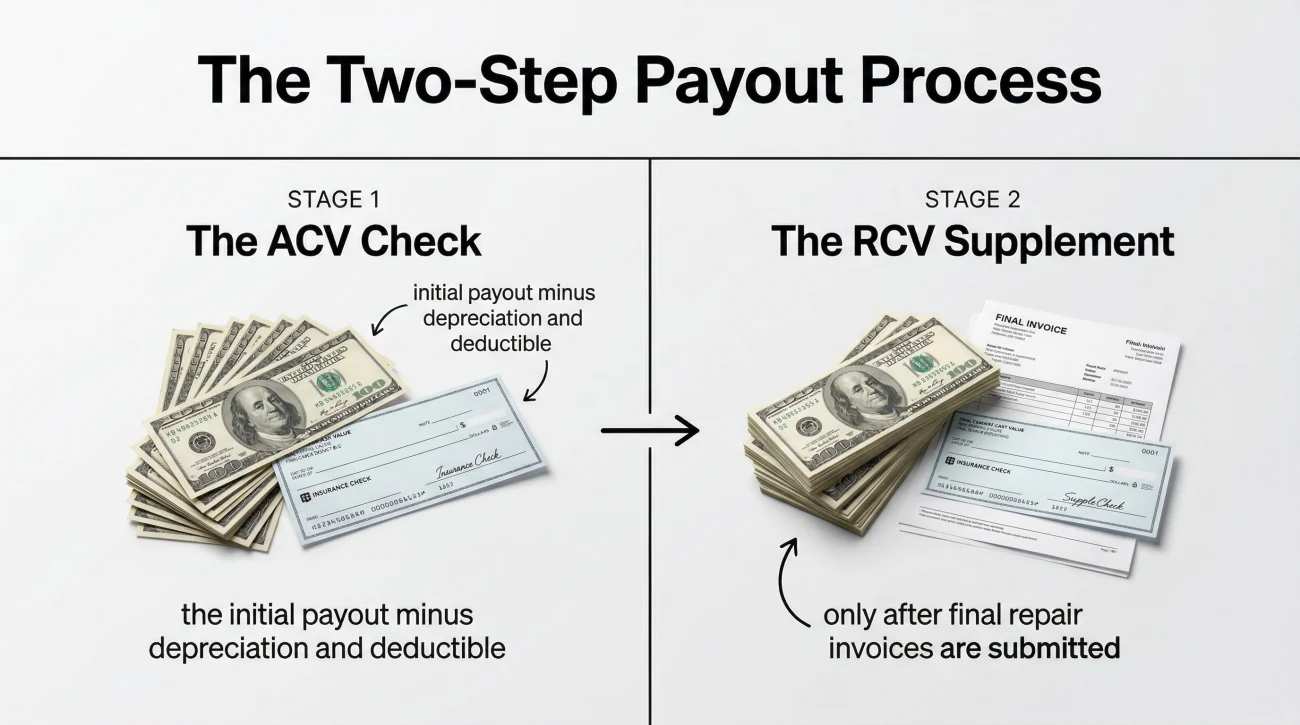

The short answer is generally yes, but there is a massive catch that depends entirely on how your policy is structured. It all comes down to whether you are dealing with an Actual Cash Value (ACV) payout or a Replacement Cost Value (RCV) payout.

Taking the initial check, finding the cheapest possible handyman to do the work for half the price, and assuming you beat the system while leaving the rest of your claim open.

Understanding that the first check is only the ACV portion. If you repair the damage for less than that initial check, you are legally allowed to keep the difference, but you will forfeit the right to claim the remaining depreciation money.

When you receive your first check, the insurer has likely applied depreciation. To claim the rest of the money, you have to submit final contractor invoices proving you actually spent the money to repair the home. If your final invoice is lower than the initial estimate, the insurance company will adjust their final payment downward. They only reimburse you for what you actually spent. For a full breakdown of this two-part mechanic, read our detailed guide on the depreciation holdback process.

The Supplement Window: When Is It Too Late to Ask for More Money?

If you cashed an ACV check to get repairs started and later find hidden damage, you might wonder if it is too late to reopen the discussion. Cashing an initial check does not automatically close your claim.

As long as you did not sign a document explicitly labeled “full and final release,” you generally have a window of time to submit supplement requests for newly discovered damage or to claim your recoverable depreciation. This window is defined in your policy documents. Check the specific deadline language before assuming you have time to wait. Missing this window means leaving money on the table permanently.

The Cash Settlement Option: Pros and Cons

In some scenarios, an adjuster might offer you a cash settlement. This is a lump sum payment offered in lieu of the traditional repair and supplement process. When you accept a cash settlement, you are agreeing to take a specific amount of money right now, and in exchange, you release the insurance company from any further financial obligation regarding that specific loss.

A cash settlement typically makes sense only in situations where you do not plan to repair the damage. For example, if a severe storm damages an old, detached shed that you were planning to tear down anyway, taking the lump sum and walking away is a perfectly logical choice. You get the money, the shed stays broken or gets removed, and the claim is closed.

However, applying a cash settlement to your primary dwelling is incredibly risky. Hidden damage is common in major property claims. Water travels behind drywall, smoke penetrates subflooring, and structural shifts are not always visible to the naked eye during the first inspection.

Typical Release Language Example:

📌 Note: If you sign a full release and later discover that the water damage reached your electrical wiring, you cannot go back and ask for a supplement. The claim is dead. Never accept a final cash settlement on your main home until a trusted, independent contractor has opened up the walls and confirmed the absolute worst-case scenario.

Are Home Insurance Claim Payments Taxable?

A sudden influx of twenty, fifty, or a hundred thousand dollars into your bank account can trigger a lot of anxiety come tax season. The most common question I hear after a major payout is whether home insurance claim money is taxable.

The general principle applied by the IRS is the concept of being “made whole.” Insurance payouts are designed to compensate you for a loss, bringing you back to the financial position you were in before the disaster struck. Because it is compensation for a physical loss rather than newly generated income, the payout is generally not considered taxable income by the federal government.

💡 Pro Tip: While standard repair payouts are typically non-taxable, I am a claims writer, not a certified public accountant. If your home was a total loss, or if you received a massive payout that you chose not to reinvest into repairs, the smartest move you can make is a quick consultation with a qualified tax professional to confirm your specific liabilities.

Doing Your Own Repairs After a Claim

For the handy homeowner, a property claim looks like an opportunity. If a pipe bursts and ruins a section of drywall, and you know how to hang, tape, and paint drywall, you might wonder if you can just do your own repairs after a home insurance claim.

The answer is yes. The insurance company cannot force you to use their preferred vendor network, nor can they legally stop you from swinging the hammer yourself. However, choosing the DIY route drastically changes how your final payout is handled.

I recently looked at a file where a homeowner repaired his own hardwood floors. He did a beautiful job. But when he tried to claim his $4,000 depreciation holdback, he was denied. He had receipts for the wood, but he could not produce a labor invoice for himself.

Here is the reality of DIY claim repairs:

| Repair Approach | Initial Payout (ACV) | Final Payout (RCV Supplement) |

|---|---|---|

| Licensed Contractor | You receive the ACV check. | You submit the contractor’s final invoice. Insurer pays the remaining depreciation for both materials and professional labor. |

| DIY (Doing it yourself) | You receive the ACV check. | You submit receipts from the hardware store. Insurer reimburses depreciation on the materials only. Your personal labor is “sweat equity” and cannot be billed. |

Your policy also requires that repairs be completed to a professional standard. If you do the plumbing work yourself, do it incorrectly, and it leaks again six months later, your insurance company will likely deny the subsequent claim citing faulty workmanship. If the damage is superficial, DIY makes sense. If it involves electrical, plumbing, or structural work, the risk usually outweighs the reward.

Signs Your Payment Process Has Gone Wrong

The post-payment phase of a claim is where many homeowners realize they made a mistake earlier in the process. If you are experiencing any of the following scenarios, your payment process is stuck or compromised:

- Your funds are locked in your lender’s escrow queue, and they will not release the first draw because the insurance check is lower than the contractor’s required upfront deposit.

- The settlement check arrived and cleared, but it is dramatically less than your contractor’s quote, leaving you unable to start the work.

- You accepted a quick cash settlement without realizing the release document closed out your claim permanently, and now your contractor has found massive hidden water damage.

- You completed the repairs yourself to save money, but because you lack professional labor invoices, the insurer is refusing to release your RCV supplement.

Payment complications almost always trace back to scope issues in the original settlement. If your check is significantly lower than your actual repair costs, the problem is not usually the math. The problem is that the adjuster missed items on their initial inspection.

Before you deposit a check that seems too low, or before you sign a release that closes your claim, you have options. Having an independent professional compare your contractor’s bid against the adjuster’s line-item estimate is the most effective way to uncover missing funds. If you are staring at a check that will not cover your repairs, you should strongly consider getting a free claim review from a licensed public adjuster to protect the value of your home.

Final Thoughts on Managing Your Claim Payment

Navigating the payout phase is ultimately about careful execution. You did the hard work of filing the claim, documenting the damage, and getting through the inspection. Now, it is just a matter of following the administrative steps to actually access your funds and complete the restoration of your home.

Protect the funds, communicate clearly with your mortgage company’s loss draft department, document every penny you spend on materials, and keep a close eye on your policy’s supplement deadlines. By understanding the mechanics behind the checks you receive, you ensure that your home is fully repaired without absorbing unfair out-of-pocket costs.

❓ FAQ

⏱️ How long is a home insurance claim check valid?

Most insurance checks are valid for 90 to 180 days from the date of issue. The exact expiration date is usually printed on the front of the check. If it expires, you must call the insurer to have it reissued.

🏦 Can I deposit an insurance check with two names on it?

No. If the check includes your mortgage company’s name, your personal bank will not let you deposit it directly. You must contact your lender’s loss draft department and follow their specific endorsement procedures.

✍️ Do I have to use the contractor my insurance suggests?

No. You have the legal right to hire any licensed and insured contractor of your choice. You are not obligated to use the insurance company’s preferred vendor network to receive your claim money.

📈 Will cashing the check close my claim automatically?

Cashing an initial ACV check does not usually close your claim. However, if the check is accompanied by a document stating it is a full and final settlement, cashing it may release the insurer from further liability.

🏠 What if my mortgage company refuses to release the funds?

Mortgage companies withhold funds when their documentation requirements are not met. They usually need the adjuster’s worksheet, a signed contractor estimate, and proof that the contractor is licensed. Provide these exactly as requested.

🛠️ Can I use the money to upgrade my kitchen instead of fixing the bedroom?

If you do not repair the damaged area, you cannot claim your RCV depreciation holdback. Furthermore, if you leave the damage unfixed and it causes future issues, the insurer will deny subsequent claims due to unresolved prior damage.

📄 Do I have to show receipts to the insurance company?

If you have an RCV policy, yes. You must submit final contractor invoices and receipts showing you actually incurred the cost of repairs in order for the insurance company to release the second check.

💸 What happens if I cash the check and do not do the repairs?

You lose the right to claim the remaining depreciation money. Also, when you eventually sell the home, or if you file a future claim, the un-repaired damage will be noted on your record, potentially voiding future coverage for that area.

🛑 Can the insurance company ask for the money back?

It is rare, but if the insurer later discovers the claim was fraudulent, or if they accidentally overpaid you due to a clerical error, they can legally demand the funds be returned.

📉 Is it normal for the first check to be so low?

Yes, the first check is almost always the Actual Cash Value, meaning depreciation and your deductible have been subtracted. It is just the starting payment, not the final total to complete your repairs.

Understanding the whole process changes how you handle each stage.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

Low offers and scope disputes are common. These explain what to do.

- 5 patterns that signal your settlement is probably short

- Who the adjuster at your door actually works for

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When a denial needs legal leverage, not just negotiation

- Four paths to fight a denial, including one most homeowners miss

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.