- Theft of your personal belongings is generally protected under your policy’s personal property coverage, but critical sub-limits strictly cap the payout for high-value items.

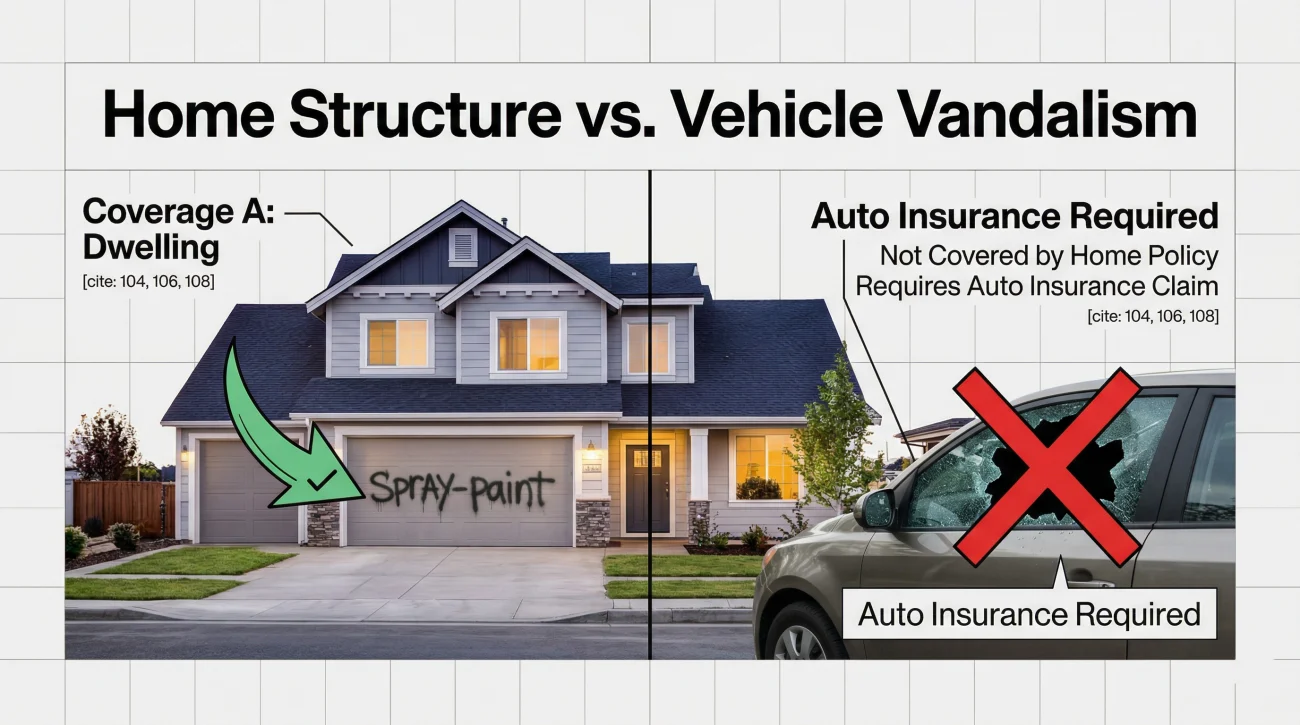

- Vandalism to your home’s physical structure falls under your dwelling coverage, but vandalism to your vehicle in the driveway requires a completely separate auto insurance claim.

- Without replacement cost coverage, stolen items are heavily depreciated based on their age and condition before any payout is issued to you.

The Reality of Stolen Property Claims

Discovering that your home has been broken into or vandalized is an incredibly violating experience. In the immediate aftermath, you just want to secure your property and replace what was taken. I have reviewed hundreds of property files following break-ins, and the initial relief homeowners feel when they learn theft and vandalism are covered by standard policies often fades quickly. The frustration usually begins when they see exactly how the policy limits the payout.

Standard homeowners policies absolutely provide coverage for these events. However, the coverage has strict boundaries, category caps, and valuation rules that most people only discover after they have filed their claim. My goal here is to walk you through exactly how insurance adjusters classify stolen property and structural damage, so you know exactly what to expect when you submit your inventory list.

A common documentation gap I see in the field involves homeowners submitting a massive list of stolen electronics without realizing their policy caps that specific category. The adjuster applies the sub-limit, and a claim the homeowner thought was worth thousands pays out only a fraction of that amount.

Before you start buying replacements, you need to understand how your policy divides the damage. The rules change depending on what was stolen, where it was stolen from, and whether the damage affected your house or your car.

How Theft Falls Under Coverage C

When belongings are stolen from your home, the claim is processed under Coverage C, which is known as your personal property coverage. This section of your policy is designed to protect your physical items against covered perils. Theft is universally recognized as one of those primary perils.

If someone breaks in and steals your television, your living room furniture, or your clothing, your policy may cover the loss up to your total Coverage C limit, minus your chosen deductible. It sounds very straightforward. However, proving what you owned is where the claims process becomes rigorous:

Identify stolen item + Provide proof of ownership + Apply Coverage C rules

Adjusters look for concrete evidence that the items existed and that you owned them at the time of the break-in. Without receipts, photographs, or owner manuals, getting full value for stolen personal property becomes a steep uphill climb. When I look at a theft file, the first thing I check is the quality of the inventory list.

Writing “one flat screen TV” and estimating the value from memory.

Listing “Samsung 65-inch 4K Smart TV, Model QN90A, purchased 2022,” accompanied by a digital receipt or a photo of the TV in your living room.

If you are unsure whether a specific type of property falls under this category, taking a step back and reviewing what standard homeowners insurance actually covers is always a smart first step.

Vandalism to Your Home Versus Your Car

Vandalism claims require a very clear separation between what was damaged. Vandalism to your home’s physical structure is typically covered under Coverage A, known as dwelling coverage. If someone spray-paints your vinyl siding, smashes your front window, or damages your front door to gain entry, the repair costs fall under this structural category.

However, the boundaries change the moment the damage involves your vehicle. Vandalism to your vehicle is not covered by your homeowners policy. It does not matter if the car was parked safely inside your locked garage or out in your driveway. Damage to the car itself falls exclusively under your auto insurance policy.

⚠️ Warning: Filing a homeowners claim for a smashed car window will result in a swift denial for that portion of the damage. You must file a comprehensive claim with your auto insurer to fix the vehicle.

I frequently see homeowners get frustrated by this rule. They assume that because the event happened on their property, one policy should handle everything. Unfortunately, the insurance industry keeps property risk and auto risk in entirely separate lanes.

The Sub-Limit Surprise for High-Value Items

The most painful part of a theft claim is almost always the application of sub-limits. Most standard policies set much lower limits for specific high-value categories. These caps apply regardless of how high your total personal property coverage limit is.

If your total Coverage C limit is $150,000, you might logically assume your stolen $8,000 engagement ring is fully covered. This is rarely the case. In most standard policies, categories like jewelry, firearms, art, and electronics are commonly sub-limited well below the general personal property amount.

| Stolen Item Category | Typical Standard Sub-Limit | What This Means For You |

|---|---|---|

| Jewelry and Watches | $1,500 to $2,500 total | An $8,000 stolen ring will only yield a maximum payout of the sub-limit. |

| Firearms | $2,000 to $2,500 total | Theft of multiple firearms will likely exceed this cap immediately. |

| Cash and Securities | $200 to $500 total | Keeping large amounts of cash at home is practically uninsured. |

Often, these sub-limits are the reason a homeowner feels cheated by their insurer. Adjusters will strictly enforce these caps. Grouping your stolen items properly on your inventory is critical, but you cannot bypass a category cap just because you have leftover room in your overall limit.

To understand exactly how these category caps restrict your payout, reviewing the complete breakdown of personal property coverage limits is a necessary step. The only way around these limits is if you purchased a specific scheduled endorsement before the theft occurred.

Theft From Your Vehicle and Off-Premises

We have established that physical damage to your car falls under auto insurance. However, the items stolen from inside the car often trigger a homeowners claim. Most policies extend Coverage C to property stolen from your vehicle up to your policy limits. If a thief smashes your car window and steals your golf clubs, your home insurance is generally the policy that responds to the stolen items.

This off-premises protection also applies when you travel. Most policies cover personal property stolen anywhere in the world. However, insurers cap this coverage because items outside your home carry a much higher risk of theft. In many standard policies, off-premises coverage is limited to ten percent of your total Coverage C limit.

Keep in mind that off-premises limits and category sub-limits stack. If your $3,000 laptop is stolen from your hotel room, the adjuster will apply the ten percent off-premises cap and the electronics sub-limit, ultimately paying you whichever limit is lower.

I always advise homeowners to look for the phrase “unattended vehicle” in their policy. Many insurers require proof of forced entry, like a smashed window, to approve a claim. If you left your car doors unlocked and your laptop was taken, the insurer will likely deny the theft claim entirely, citing a failure to properly secure your property.

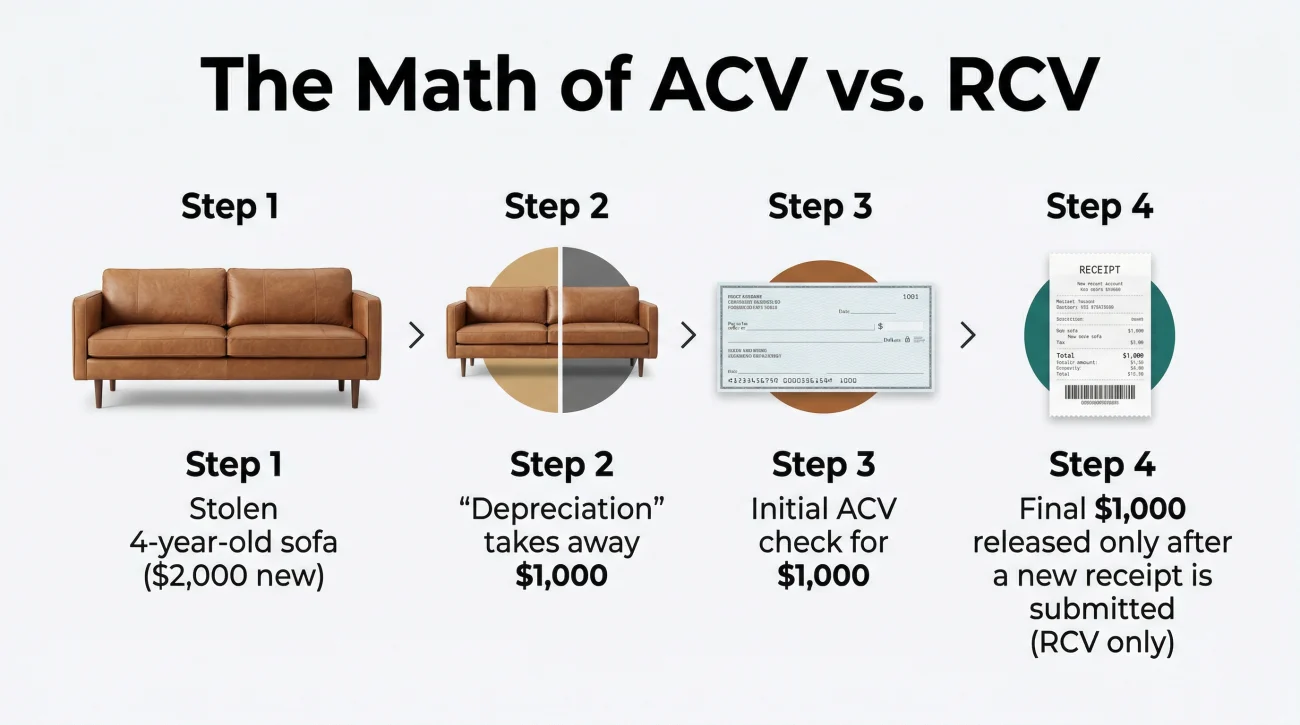

ACV Versus RCV For Stolen Items

If you clear the hurdles of proving ownership and navigating sub-limits, you face the final calculation. This is where the difference between Actual Cash Value (ACV) and Replacement Cost Value (RCV) drastically changes your settlement.

If your policy pays ACV for contents, your stolen items are depreciated based on their age and condition before any payment is issued. An adjuster will look at a laptop you bought three years ago for a thousand dollars and apply severe depreciation because electronics lose value quickly. You might receive a check for three hundred dollars.

If you have RCV coverage, the insurer still typically pays the depreciated ACV amount first. To get the rest of the money, you must actually purchase a replacement laptop and submit the new receipt to the insurer. Only then will they release the recoverable depreciation to make you whole.

Stolen item: 4-year-old leather sofa

Cost to buy new today: $2,000

Depreciation applied (age/wear): -$1,000

Initial ACV Check to Homeowner: $1,000

If RCV policy: Homeowner buys new sofa, submits receipt, gets final $1,000.

If ACV policy: The $1,000 check is the final payout.

Understanding this math is critical. Many homeowners assume the initial ACV check is a lowball offer, not realizing they have to complete the replacement process to unlock the rest of their funds.

The Most Common Adjuster Tactics on Theft Claims

You can usually tell a theft claim is going sideways when you look at how the adjuster groups the damage on their initial estimate. The confusion often peaks during dual-event scenarios where a break-in involves both your house and your car simultaneously.

A common scenario I see is a thief breaking into a garage, vandalizing the car, and stealing expensive tools. Homeowners naturally try to submit one massive claim to their home insurer. In reality, you must file a dwelling claim for the garage door, an auto claim for the car damage, and a personal property claim for the tools. If you mix these up on one form, adjusters will simply deny the misplaced items, causing massive delays.

Another major red flag is deliberate miscategorization to force your belongings under a strict sub-limit. For example, an adjuster might try to classify a $4,000 professional photography camera under a general $1,500 “household electronics” cap. If your settlement estimate groups distinct, high-value items into broad, low-limit categories, your payout will be severely suppressed.

What to Do When the Settlement Falls Short

Theft and vandalism coverage frequently runs into sub-limits and depreciation issues that reduce the payout significantly. Insurers often rely on dense policy language to justify these low offers, but you have the right to challenge their math and their categorizations.

Adjusters sometimes apply incorrect depreciation rates, miscategorize items to force them under restrictive sub-limits, or wrongly deny off-premises coverage due to a misunderstanding of the police report. If you are looking at a settlement check that barely covers the cost of replacing your front door, let alone the items stolen from inside, you do not have to simply accept it.

Getting a second set of eyes on the policy language and the adjuster’s worksheet can reveal whether the calculation was done correctly. Exploring the option of having a licensed public adjuster review the settlement calculation is often the most effective way to determine if money was left on the table. They understand exactly how to read the depreciation schedules and dispute miscategorized items.

Final Thoughts on Theft and Vandalism Claims

Recovering from a break-in requires moving quickly and methodically. Your first call is always to the police, as insurance companies will not process a theft or vandalism claim without a formal police report number. Once your property is secure, focus on gathering whatever proof of ownership you can find before the adjuster arrives.

Do not let the initial ACV check discourage you if you have replacement cost coverage, and always question heavy depreciation on items that hold their value. Be proactive, communicate in writing, and remember that the first settlement offer is based on the insurer’s evaluation of your proof. For a broader view on what gets excluded entirely, you can always check the standard policy exclusions list to ensure you are not expecting coverage for something the policy explicitly forbids.

❓ FAQ

🕵️ Does homeowners insurance cover theft of cash?

Yes, but standard policies place a very strict sub-limit on cash, typically between $200 and $500 total, regardless of how much was actually stolen.

🚗 Does home insurance cover a stolen car from my driveway?

No. The theft of a motor vehicle is excluded from homeowners insurance and must be filed under the comprehensive coverage of your auto insurance policy.

💍 Does homeowners insurance cover stolen jewelry?

Yes, but jewelry is subject to a strict sub-limit, often capped between $1,500 and $2,500. To fully cover expensive jewelry, you must purchase a scheduled personal property endorsement beforehand.

📦 What happens if a package is stolen from my porch?

Porch piracy is generally covered under your personal property coverage, but because the value of the package is usually lower than your deductible, filing a claim rarely makes financial sense.

📱 Does home insurance cover a stolen cell phone?

Yes, a stolen cell phone is considered personal property. However, after applying your deductible and potential depreciation, the payout may be minimal.

🚲 Is my stolen bicycle covered by homeowners insurance?

Yes, bicycles are covered under Coverage C. Even if it is stolen while you are away from home, it is typically protected under your off-premises coverage limits.

🧳 Does homeowners insurance cover theft while traveling?

Yes, most policies provide off-premises coverage for your belongings while traveling, usually capped at a percentage (often 10%) of your total personal property limit.

🏚️ Does homeowners insurance cover vandalism to a vacant home?

Usually no. Most standard policies have a vacancy clause that excludes vandalism and theft coverage if the home has been unoccupied for more than 30 to 60 consecutive days.

🧾 How do I prove I owned an item that was stolen?

Adjusters accept purchase receipts, credit card statements, owner’s manuals, appraisals, or photographs of the item inside your home as proof of ownership.

📈 Will my insurance go up if I file a theft claim?

In many cases, yes. Filing any claim, including theft or vandalism, can result in the loss of a claims-free discount and may increase your premium at renewal.

Understanding the whole process changes how you handle each stage.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

Low offers and scope disputes are common. These explain what to do.

- 5 patterns that signal your settlement is probably short

- Who the adjuster at your door actually works for

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When a denial needs legal leverage, not just negotiation

- Four paths to fight a denial, including one most homeowners miss

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.