- Personal property coverage (Coverage C) protects your belongings, but it rarely covers everything at full value by default.

- Most policies contain “sub-limits” that severely restrict payouts for high-value items like jewelry, electronics, and firearms, regardless of your total coverage amount.

- Whether you have Actual Cash Value (ACV) or Replacement Cost Value (RCV) determines if you get a fraction of an item’s original cost or enough money to buy a new one today.

- Without detailed documentation and an understanding of your policy limits, contents claims are frequently underpaid.

The Personal Property Coverage Reality Check

Coverage C, also known as personal property coverage, sounds incredibly comprehensive on paper. When homeowners look at their declarations page and see a six-figure number allocated to their belongings, they naturally assume everything inside their house is fully protected. Unfortunately, this assumption often collapses the moment they actually need to file a claim.

I have sat across from insurance adjusters on hundreds of claims, and I can tell you that personal property is where the most painful surprises happen. A homeowner will lose a $5,000 wedding ring or a basement full of expensive tools, file the paperwork, and wait for a check. Weeks later, they receive a settlement for a fraction of the value. They feel cheated, but when we pull the policy jacket, the insurance company has followed the contract exactly.

The gap between what you think is covered and what the policy actually pays comes down to how your contract defines limits, sub-limits, and depreciation. Your belongings – furniture, clothing, electronics, appliances, and sports equipment – are indeed protected against covered perils like fire, windstorm, and theft. But they are protected under very strict mathematical rules.

If you want to understand how this fits into your broader safety net, you can review what standard homeowners insurance covers across the board. In this guide, we are going to focus entirely on your stuff. We will look at how your limits are calculated, the hidden traps that shrink your payouts, and how to protect yourself before an adjuster starts depreciating your life’s possessions.

How Your Coverage C Limits Are Calculated

Personal property coverage is almost never a random number you pick out of thin air. In standard homeowners policies, Coverage C is tied directly to Coverage A (your dwelling coverage). It is typically set at 50 to 70 percent of the amount your house is insured for.

For example, if your home is insured for $400,000, your personal property coverage will likely sit between $200,000 and $280,000. At first glance, $200,000 sounds like more than enough money to replace the contents of an average home. However, when you experience a total loss like a major fire, you quickly realize how much it actually costs to replace every single item you own: every sock, every fork, every piece of furniture, and every book.

The Inventory Problem

The limit itself is rarely the issue in small claims. If a pipe bursts and ruins a single sofa, your $200,000 limit is plenty. The problem arises during major disasters. Adjusters require an itemized list of everything lost. I often see homeowners leave tens of thousands of dollars on the table simply because they cannot remember what was in their closets or attic.

⚠️ Warning: The insurance company will not just write you a check for your total Coverage C limit simply because your house burned down. You must prove the existence and value of the items up to that limit.

This strict requirement for documentation leads directly into the next major hurdle homeowners face: navigating the hidden caps on their most valuable items.

The Sub-Limit Trap: Where Most Claims Shrink

This is the most critical section of this guide. Even if you have $200,000 in total personal property coverage, you do not have $200,000 to spend on whatever was destroyed. Standard policies carve out specific categories of high-value items and cap the payout for those categories. These are called sub-limits.

Insurers use sub-limits because certain items are highly susceptible to theft, easily lost, or difficult to value accurately. If they covered everyone’s Rolex watches under the base premium, insurance would be unaffordable for the average person.

In my field experience, sub-limits cause more anger than almost any other policy clause. I routinely see homeowners file a $15,000 claim for stolen jewelry only to discover their policy caps jewelry theft at $1,500 total. The adjuster is simply applying the contract, but to the homeowner, it feels like a broken promise.

To help you identify these hidden caps before they catch you off guard, here are the standard sub-limits you will find in almost every base homeowners policy:

| Item Category | Typical Sub-Limit Amount | What It Usually Applies To |

|---|---|---|

| Jewelry and Watches | $1,500 to $2,500 | Theft of rings, necklaces, watches, gems. |

| Firearms | $2,000 to $2,500 | Theft of guns and related equipment. |

| Silverware and Goldware | $2,500 | Theft of precious metal flatware or tea sets. |

| Cash and Securities | $200 to $500 | Cash in a drawer, gift cards, physical stocks. |

| Business Property | $1,500 to $2,500 | Laptops or tools used primarily for your business. |

| Watercraft | $1,500 | Small boats, jet skis, trailers. |

It is very important to note that many of these sub-limits apply specifically to the peril of theft. If your $5,000 wedding ring is destroyed in a house fire, it might be covered up to your overall Coverage C limit. But if it is stolen, the $1,500 sub-limit kicks in immediately. You can learn more about how this specific peril works in our guide on theft and vandalism coverage.

The Electronics Squeeze

While standard electronics (TVs, computers) usually fall under your general Coverage C limit, some modern policies are beginning to introduce sub-limits for high-end electronics, data recovery, or smart home systems. Always check your specific declarations page to see if a separate cap exists for electronics, especially if you have a massive home theater setup or gaming rigs.

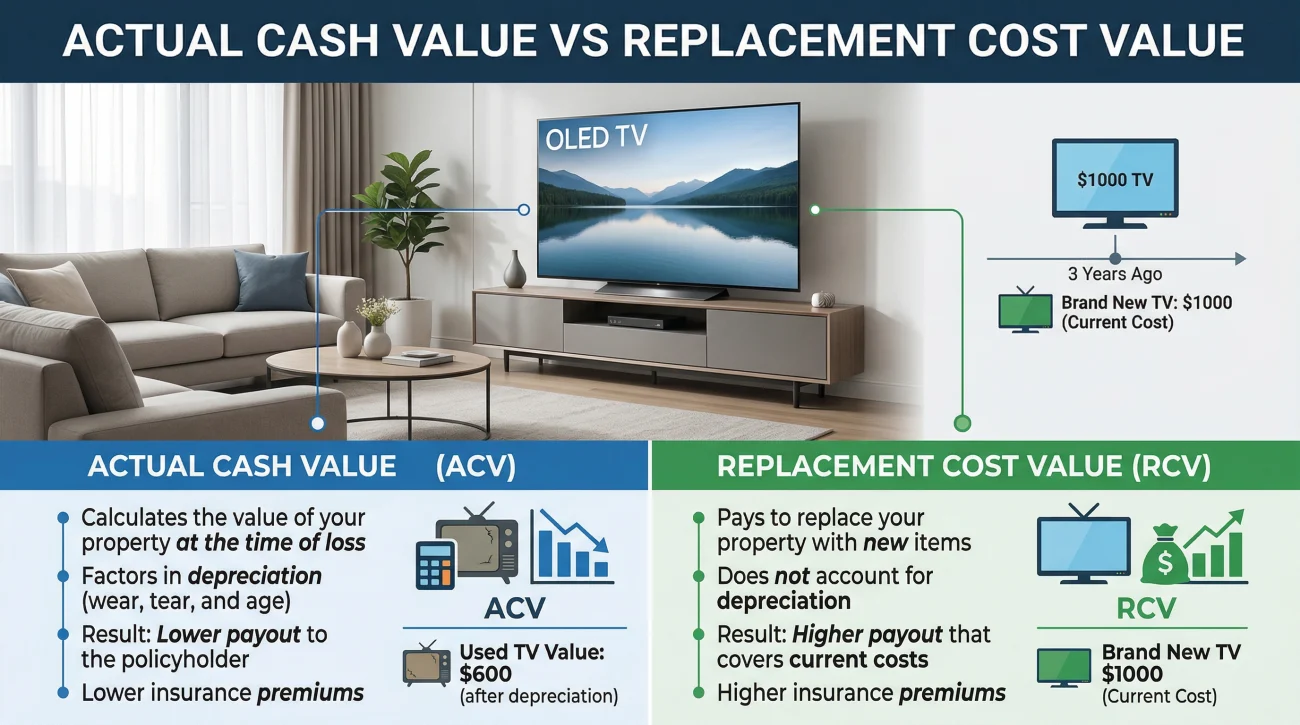

Actual Cash Value vs Replacement Cost Value

If sub-limits are the first trap, depreciation is the second. When you buy homeowners insurance, you make a crucial choice regarding your personal property: Actual Cash Value (ACV) or Replacement Cost Value (RCV).

This is not a claiming mechanic you can negotiate later; this is a strict coverage decision embedded in your policy from day one. Many homeowners select ACV because it makes the monthly premium cheaper. They usually regret it.

- 👉 Actual Cash Value (ACV):

The insurance company pays you what the item was worth on the day it was destroyed, factoring in age and wear and tear. - 👉 Replacement Cost Value (RCV):

The insurance company pays you what it costs to buy a brand new version of that item at today’s retail prices.

Let us look at a practical example. Imagine a pipe bursts and ruins your living room television. You bought this TV five years ago for $1,200.

If you have an ACV policy, your contents claim will be heavily depreciated. Clothing, furniture, and electronics lose value incredibly fast on paper. If you want to understand the exact mechanics of how these payments are distributed during a claim, review our guide on how ACV and RCV claims are processed.

Scheduled Personal Property: Protecting High-Value Items

Once you realize that your $10,000 engagement ring or your $8,000 collection of photography gear is trapped by a $1,500 sub-limit, the next logical question is how to fix it. The answer is a Scheduled Personal Property endorsement, sometimes called a “floater.”

Scheduling an item means you are removing it from the general Coverage C pool and insuring it individually for a specific, agreed-upon value. When you schedule an item, the standard sub-limits no longer apply, and your deductible often does not apply either.

To schedule an item, the insurer will almost always require proof of its value. This is not something you can guess.

Action Step: Get a professional appraisal, submit it to your insurer, and add the scheduled endorsement to ensure full protection.

You must provide a recent professional appraisal or a very clear, recent receipt. If you buy a new piece of fine art or an expensive musical instrument, do not wait until your annual renewal to tell your insurance agent. Get it scheduled immediately. Items that are typically scheduled include jewelry, fine art, antiques, high-end bicycles, cameras, and rare collectibles.

Off-Premises Coverage: When Things Break Outside the Home

One of the hidden benefits of Coverage C is that it usually follows you outside your house. For example, if your luggage is stolen from an airport carousel, or your laptop is taken from a local coffee shop while you grab a drink, your homeowners policy is often the safety net that responds.

However, this off-premises coverage comes with its own set of rules. Most standard policies limit off-premises coverage to 10 percent of your total Coverage C limit. If your total personal property limit is $150,000, you have $15,000 of coverage for items outside the home.

💡 Pro Tip: When claiming theft from a vehicle, remember that the homeowners policy only covers the items inside the car, not the damage to the car itself (like a broken window). The vehicle damage falls under your auto insurance. You may end up having to file two separate claims and pay two separate deductibles.

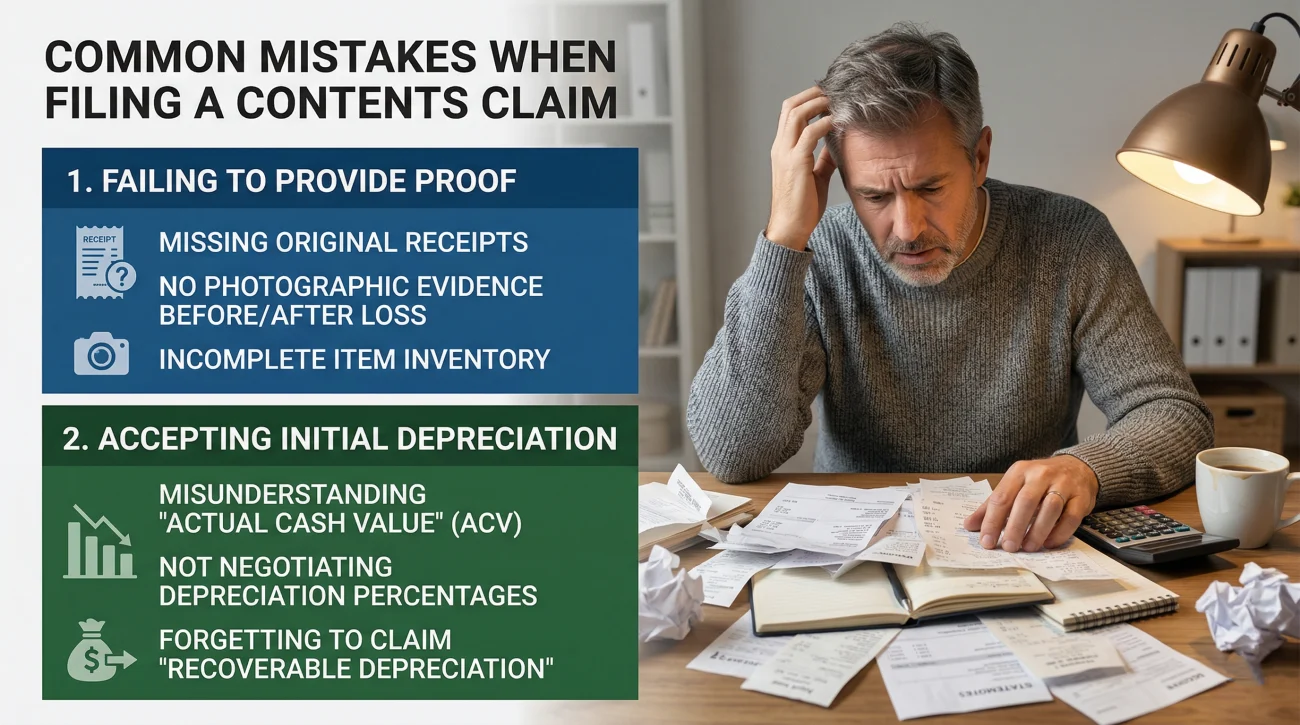

Common Mistakes When Filing a Contents Claim

When disaster strikes, homeowners are stressed and often rush through the contents portion of their claim. Adjusters rely on the documentation you provide. If you provide poor documentation, you will receive a poor settlement.

The most common mistake is failing to provide adequate proof of ownership or value. Adjusters are trained to push back on high-value line items that have no supporting evidence. If you claim you lost a $3,000 leather sofa but can only provide a blurry photo of a burnt frame, the adjuster may price it out as a generic $600 sofa.

If you do not have original receipts, you must get creative. A receipt is best, but adjusters will often accept a combination of other proofs.

Action Step: Gather old photographs, locate credit card statements, and find user manuals to create alternative proof of value.

Another major mistake is accepting the adjuster’s initial depreciation schedule without question. Adjusters use software to determine how long an item should last and how much value it has lost. These default software settings are often aggressive. If they depreciate your perfectly maintained solid wood dining table by 75 percent because it is ten years old, you have the right to push back. Here is a straightforward way to request that breakdown in writing:

Hello [Adjuster Name],

I am reviewing the initial settlement offer for the contents portion of my claim. Before I can accept this, I need to understand the valuation methods used.

Please provide the complete, itemized depreciation schedule showing the exact age, expected lifespan, and applied depreciation percentage for every item on my personal property list.

Thank you,

[Your Name]

Signs Your Personal Property Claim Is Off-Track

If you are in the middle of a claim, reading the adjuster’s estimate can be a frustrating experience. It is very common for homeowners to look at the bottom line and realize it is nowhere near enough to replace their life. Before you assume you just have bad coverage, you need to verify that the adjuster applied your coverage correctly.

There are several distinct signals that your personal property claim is being poorly handled or unfairly minimized. If you are experiencing any of the following, you need to pause before signing any final release forms:

- Your high-value items were paid out at ridiculously low numbers: If your settlement for jewelry, art, or electronics looks suspiciously low, the adjuster likely hit you with a sub-limit. You need to check your declarations page to confirm if that sub-limit actually exists in your contract.

- Your payout is based entirely on ACV when you bought RCV: Adjusters sometimes default to ACV payouts. If you specifically pay for Replacement Cost Value coverage, you should not be eating massive depreciation penalties on your final settlement.

- The adjuster rejected items due to “lack of receipts”: If you provided alternative proof like owner’s manuals, credit card statements, or clear photographs, and the adjuster still zeroed out the item, they are being unreasonably strict.

- Every item has maximum depreciation applied: If the adjuster’s software has depreciated a solid oak table at the same rapid rate as a cheap particle-board desk, the math is wrong and favors the insurance company.

These recurring valuation issues are the most common reasons personal property claims pay out far less than expected. If your settlement was substantially below the value of what you lost, you do not have to just accept the initial numbers. Having a professional review the settlement calculation can quickly identify whether the correct limits and fair values were applied.

If you are looking at an estimate that does not cover your losses, having a public adjuster review the scope before you accept is often the smartest next step. They speak the adjuster’s language and can spot exactly where the valuation software was skewed against you.

Final Thoughts on Protecting Your Belongings

Your personal property coverage is a vital part of your financial safety net, but it requires active management. You cannot simply buy a policy, stuff your house full of valuable things, and assume the insurance company will write a blank check if disaster strikes. You must know your sub-limits, you must insist on Replacement Cost Value coverage, and you must document your belongings before you need to make a claim.

If you are currently fighting a claim, remember that the adjuster’s first itemized list is an offer, not a final verdict. Review every line, challenge aggressive depreciation, and do not let them hide behind exclusions that do not actually exist in your specific policy. For a broader look at what insurers routinely try to deny, read up on standard policy exclusions so you are fully prepared.

❓ FAQ

📱 Does homeowners insurance cover my phone if I drop it?

Usually no. Standard policies do not cover accidental drops or normal wear and tear. A phone is only covered if damaged by a listed peril, like a fire or theft.

💻 Will my home insurance pay for a new laptop if water ruins it?

It depends on the water source. If the water damage was sudden and accidental (like a burst pipe), it is typically covered. If you spilled coffee on it, it is usually not covered.

💍 How much will my insurance pay for a stolen wedding ring?

Unless you have a scheduled endorsement, theft of jewelry is strictly limited by a sub-limit, which is commonly capped between $1,500 and $2,500 total.

🛋️ Do I get enough money to buy new furniture after a fire?

This depends entirely on whether you have Replacement Cost Value (RCV) or Actual Cash Value (ACV) coverage. RCV pays for new furniture; ACV pays for the depreciated value of your old furniture.

🚗 Is my stuff covered if it gets stolen out of my car?

Yes, belongings stolen from your vehicle are usually covered under your homeowners policy’s off-premises coverage, typically up to 10% of your total personal property limit.

📸 Do I need receipts for every single item I claim?

Receipts are the best evidence, but if you do not have them, adjusters will often accept photographs, credit card statements, or original owner’s manuals as proof of ownership.

📦 What if I have expensive collectibles, are they fully covered?

Usually not under a standard policy. Fine art, antiques, and high-value collectibles are subject to strict sub-limits and should be protected with a separate scheduled endorsement.

🧥 Does personal property coverage include my clothes?

Yes, clothing is considered personal property. However, clothes depreciate very quickly in value, so an ACV policy will pay very little for an older wardrobe.

🏷️ What does scheduled personal property mean?

It is an add-on to your policy that insures a specific, high-value item (like an engagement ring) for its appraised value, bypassing the standard sub-limits and deductibles.

📝 Can I dispute the value the adjuster put on my belongings?

Yes. You can and should request the full depreciation schedule and challenge any valuation that applies aggressive depreciation to items that hold their value well.

Knowing what is covered is step one. These explain what happens from there.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

These cover what to do when the offer does not match what your policy says.

- 5 patterns that signal your settlement is probably short

- Who the adjuster at your door actually works for

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When a denial needs legal leverage, not just negotiation

- Four paths to fight a denial, including one most homeowners miss

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.