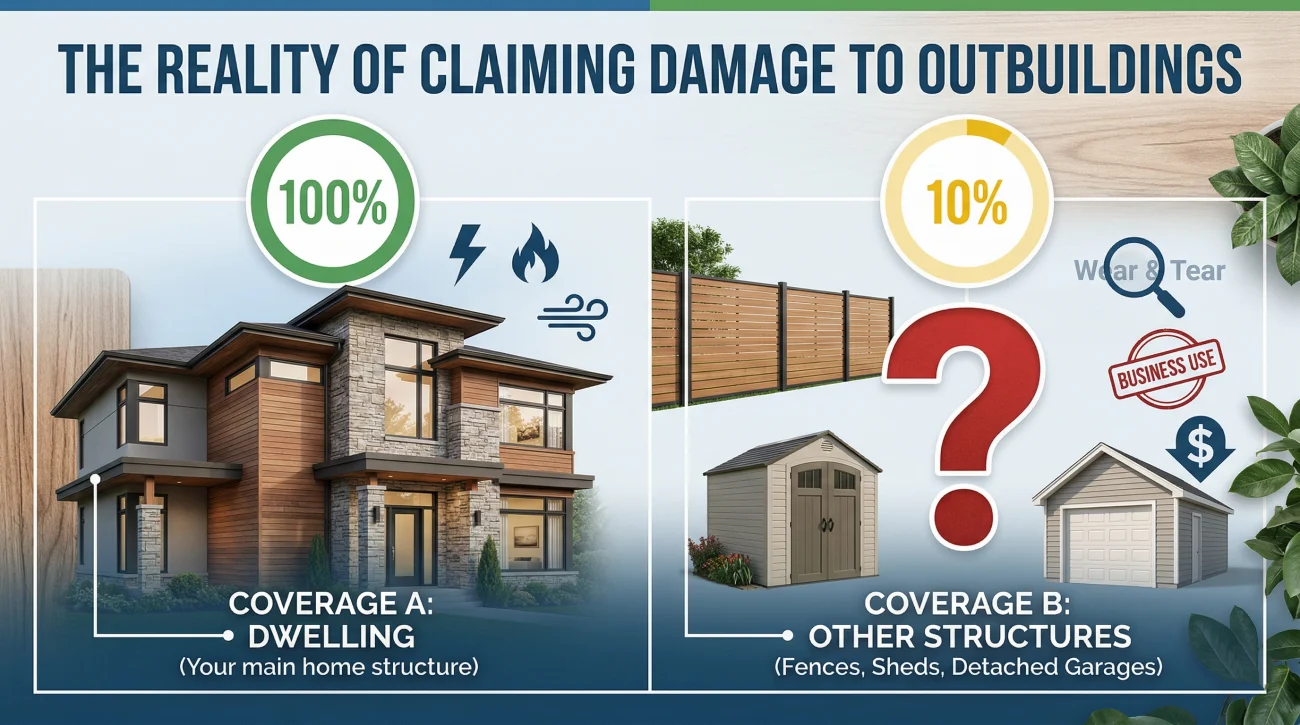

- Damage to fences, detached garages, sheds, and pools is generally covered by standard homeowners insurance under “Coverage B” (Other Structures).

- Coverage B is typically limited to 10 percent of your total dwelling coverage. If your home is insured for $300,000, you have $30,000 to repair or replace all detached structures.

- Outbuildings are covered against the same sudden and accidental perils as your main house, such as fire, windstorms, hail, and falling trees.

- Structures used for any type of business purpose or rented out to others are almost always excluded from standard Coverage B protection.

- Fences and sheds are heavily subjected to depreciation. Adjusters often cite “wear and tear” or pre-existing rot to reduce the payout on older wooden structures.

The Reality of Claiming Damage to Outbuildings

When a severe storm rolls through a neighborhood, the main house gets all the attention. But in my years of reviewing property claims, I have seen that the secondary damage often causes the most frustration. A large oak tree crushes a custom built shed, high winds tear down a hundred feet of privacy fence, or a detached garage suffers a partial roof collapse. Most homeowners immediately assume these structures are fully covered just like their living room.

The truth is that your homeowners insurance does cover fences, detached garages, and other structures, but it does not protect them to the same extent as your main dwelling. These items fall under a specific section of your policy called Coverage B, also known as “Other Structures” coverage. And the rules governing Coverage B are where many homeowners find themselves completely caught off guard.

I always tell homeowners that the insurance process treats your property as a strict hierarchy. The structure you sleep in gets the primary protection. Everything else is secondary, and it comes with strict financial caps. The biggest shock usually happens when a homeowner realizes that a total loss of their expensive detached workshop might only yield a fraction of what it costs to rebuild.

If you have just experienced damage to an outbuilding, or if you are trying to understand your policy before a bad storm hits, you need to know exactly how this coverage limit works. You also need to understand how insurance adjusters evaluate damage to these structures, because the inspection process for a fence is very different from the inspection process for a kitchen.

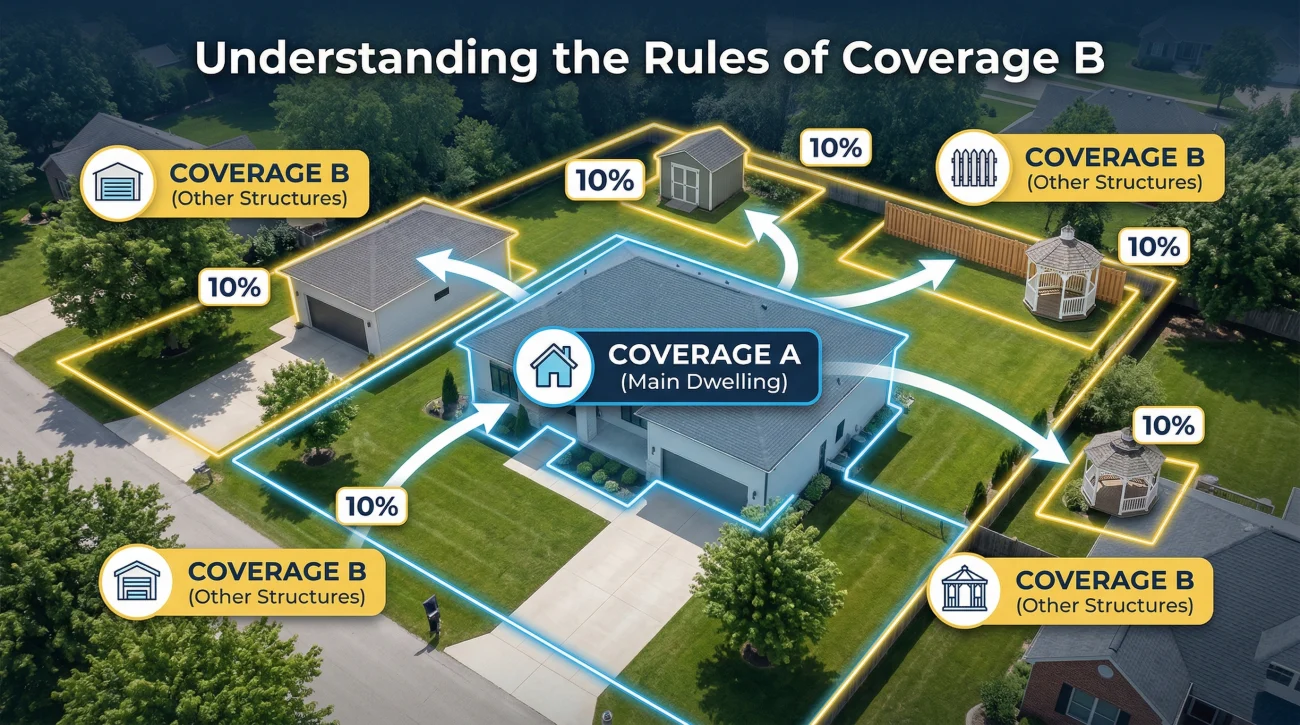

Understanding the Rules of Coverage B

To understand what is protected, you first need to understand the physical boundary line that insurance companies draw. Coverage A protects your main dwelling and anything physically attached to it, like an attached garage or a deck bolted to the side of the house. Coverage B protects structures on your property that are set apart from the dwelling by a clear space.

This definition seems simple, but in the field, I often see it become a point of heavy debate. For example, if your garage is connected to your house by nothing more than a fence or a utility line, the insurance company will classify it as a detached structure under Coverage B. The physical detachment is the sole deciding factor.

I recently reviewed a file where a homeowner’s detached garage was connected to the main house by a simple wooden breezeway. Because there was a continuous roofline, the homeowner successfully argued it was part of the main dwelling, shifting the damage from the restrictive Coverage B limit to the much larger Coverage A limit. Details matter.

The Ten Percent Limit Explained

The most critical thing to know about Coverage B is the standard percentage cap. In most standard homeowners policies, your other structures coverage is automatically set at 10 percent of your Coverage A dwelling limit. Insurance companies do not calculate the actual replacement cost of your specific fence or shed when they write the policy. They simply assign a blanket 10 percent.

Let us look at how this math plays out in the real world. If your main house is insured for $250,000, your policy provides exactly $25,000 to cover all detached structures combined. If a massive fire destroys your $20,000 detached garage, your $8,000 custom shed, and your $5,000 vinyl fence, your total loss is $33,000. However, the policy will only pay out the $25,000 limit. You are left paying the $8,000 difference out of your own pocket.

This is why understanding what your standard homeowners insurance policy covers across the board is so crucial. If your main house is underinsured, your Coverage B limit is automatically suppressed as well.

How to Protect High-Value Outbuildings

If you realize that your 10 percent limit is not enough to rebuild your detached garage, extensive fencing, and custom gazebo, you do not have to accept the default cap. You can request a Coverage B endorsement from your agent to increase this limit to 20 or 25 percent.

Before a storm hits, walk your property and make a rough estimate of what it would cost to rebuild every detached structure today. If that number exceeds 10 percent of your main house’s insured value, call your broker. Increasing your Coverage B limit is usually a very inexpensive addition to your premium, often costing just a few extra dollars a month, but it saves thousands during a catastrophic loss.

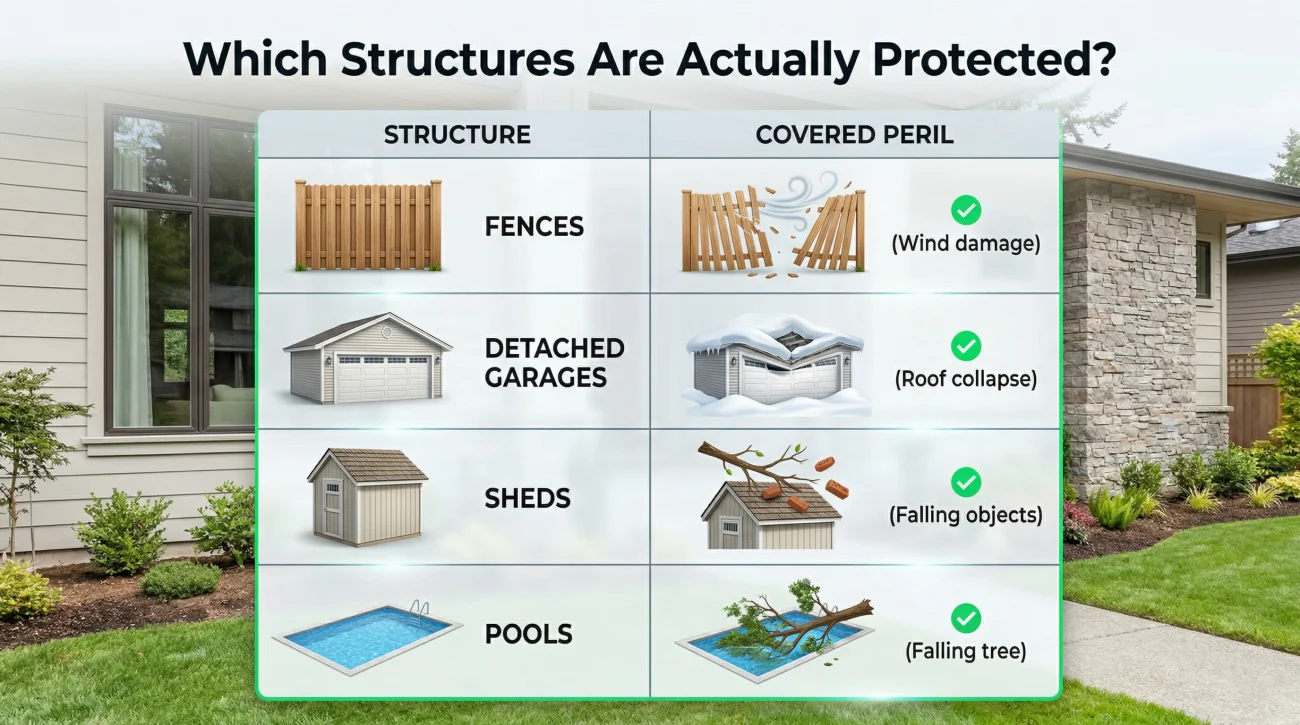

Which Structures Are Actually Protected?

Coverage B protects your outbuildings against the exact same sudden and accidental perils that apply to your main house. If your policy covers wind, hail, fire, lightning, and falling objects for the dwelling, those same protections extend out into your yard.

But because these structures are built differently and are constantly exposed to the elements, adjusters scrutinize them differently. Here is how they typically classify and evaluate common yard structures during a claim inspection.

Fences and Gates

Fences are the most frequently claimed item under Coverage B. Windstorms and falling tree branches are the usual culprits. However, fences are also the most aggressively depreciated items in the entire insurance process. Wood fences age poorly, and adjusters are trained to look closely at the base of the posts. If a windstorm blows your fence down, but the adjuster notes that the posts were completely rotted at the soil line, they may deny the claim by stating the fence failed due to wear and tear, not the wind.

Detached Garages and Sheds

Whether you have a fully finished two car detached garage or a simple prefabricated tool shed, these structures are covered. The adjuster will estimate the cost to repair the roof, siding, and framing just as they would for a house. However, it is very important to separate the structure from the contents inside. The lawnmower inside the shed is not part of Coverage B. That falls under your personal property coverage.

Swimming Pools, Driveways, and Retaining Walls

These items often confuse homeowners. The concrete shell or structural liner of an in ground swimming pool is generally considered an “other structure.” A driveway is also a structure.

Retaining walls are complex. They are typically covered for sudden impacts (like a vehicle hitting them or a massive tree falling), but they are strictly excluded if the damage is caused by the gradual pressure of underground water (hydrostatic pressure) or earth movement over time.

| Structure Type | Standard Coverage Status | Common Adjuster Focus |

|---|---|---|

| Wood Privacy Fence | Covered under Coverage B | High depreciation, checking for wood rot or termite damage. |

| Detached Garage | Covered under Coverage B | Verifying no business operations are taking place inside. |

| Prefabricated Shed | Covered under Coverage B | Checking if the structure is anchored to the ground properly. |

| Swimming Pool Shell | Covered under Coverage B | Verifying damage is from a sudden event, not ground shifting or freezing. |

| Retaining Wall | Fact-specific (Often Covered) | Excluded if damage is caused by gradual hydrostatic pressure or earth movement. |

The Exclusions That Trigger Surprise Denials

Even if a structure is clearly located on your property and gets destroyed by a covered peril, the insurance company has strict exclusions that can completely void your coverage. I have seen many homeowners accidentally talk their way out of a settlement by casually mentioning something that triggers a hard exclusion.

⚠️ Warning: The absolute fastest way to get an outbuilding claim denied is to mention that you use it to run a business.

Standard homeowners policies are strictly for personal, residential use. If you have converted your detached garage into a woodworking shop where you build furniture to sell online, or if your shed is used to store inventory for your landscaping business, the insurance company will likely deny coverage entirely. The structure loses its residential status the moment it is used for commercial enterprise. If you run a business from home, you need a specific commercial endorsement.

Beyond business use, there are several other major exclusions that frequently wipe out outbuilding claims:

- 👉 Rented Structures: If you converted a detached garage into a living space and rent it out on an app, standard Coverage B will not protect it without a specific landlord policy.

- 👉 Flood and Earth Movement: Standard policies do not cover external flooding or earthquakes. If a nearby river overflows and destroys your shed, or a landslide takes out your fence, Coverage B will not apply.

- 👉 Ordinance or Law Requirements: If your older garage burns down and the city now requires you to rebuild it with upgraded, more expensive electrical codes, the policy will not pay for those upgrades unless you have Ordinance and Law coverage.

Finally, remember that the land itself is never covered. If a storm washes away your expensive landscaping, the dirt, and your prized garden beds, you cannot claim them under Coverage B.

Knowing these boundaries prevents you from accidentally voiding your own coverage during an inspection. If you want to verify exactly what scenarios your policy outright refuses to pay for, you should review the complete list of standard policy exclusions so you know exactly what the adjuster will be looking to deny.

The ACV vs RCV Trap for Fences and Sheds

Understanding the exclusions helps you avoid saying the wrong thing during an inspection. However, even if your claim clears the coverage hurdles, you still have to navigate how the insurance company calculates the payout. This valuation process is arguably the most painful part of an other structures claim.

When you buy insurance, you typically choose between Actual Cash Value (ACV) and Replacement Cost Value (RCV) for your main dwelling. Many homeowners assume that if they have RCV for their house, they automatically get brand new replacement cost for their fence. This is frequently not the case.

Many insurance policies explicitly state that while the main dwelling is covered at RCV, fences, awnings, and outdoor equipment are only paid at Actual Cash Value. ACV means the insurance company pays you what the item is worth today, taking its age and condition into account. This is called depreciation.

I remember reviewing a case where a family lost a ten-year-old custom gazebo. It would cost $12,000 to rebuild today, but the adjuster applied 60 percent depreciation due to ‘weathering.’ The family was handed a check for $4,800 and told to rebuild. That is the ACV trap in action.

If you have a wooden privacy fence that gets blown down, the adjuster will not give you full price to build a new one. They will argue that a wood fence has a lifespan of about 15 years. Since it is ten years old, it has lost roughly 66 percent of its value. Your settlement offer will reflect that massive deduction. This gap between the insurance check and the actual cost of hiring a contractor is a harsh reality of property claims.

You must check your specific policy documents to see if your Coverage B items are settled at ACV or RCV. Even if you do have RCV coverage, remember the golden rule of claims: the insurer will still pay you the ACV amount first. They will only release the remaining depreciation funds after you prove the structure has been fully rebuilt.

How to Document Outbuilding Damage Like a Pro

The best way to fight back against aggressive depreciation starts before the storm even arrives. When an adjuster visits your property after a major storm, their primary focus will be your main house. They will climb the roof, check the siding, and look for interior leaks. Outbuildings are often treated as an afterthought. It is your responsibility to make sure the detached structures are thoroughly inspected.

The Pre-Storm Home Inventory

The best way to fight heavy depreciation on a fence or shed is to prove it was in excellent condition before the storm hit. Every spring, walk your yard and take clear, timestamped photos of your fences, detached garages, and pool structures. Keep receipts for any wood stain, paint, or roofing materials you use to maintain them. If an adjuster tries to claim your fence collapsed due to “long-term rot,” handing them a timestamped photo from two months prior showing a perfectly maintained, freshly stained fence will instantly shut down that argument.

Handling the Inspection

I always advise homeowners not to wait for the adjuster to find the damage. You need to present the damage to them clearly and in writing.

- 📸 Photograph the structure from all angles, capturing the entire footprint of the damage.

- 🔍 Capture close-ups of the connection points, roof lines, and base posts to prove the break was sudden.

- 📝 Send an email confirming the exact scope of the inspection the same day the adjuster leaves.

Assuming the adjuster saw the crushed fence in the backyard while they were looking at the roof, and waiting for the estimate to arrive.

Walking the adjuster to the fence, pointing out exactly how many linear feet are damaged, and sending a follow up email the same day summarizing that the fence and the shed must be included in the report.

If the adjuster is rushing, or if you want to ensure the detached structures are formally on the record before they write their estimate, use a simple, polite written confirmation. Creating a paper trail is the single most effective way to prevent items from being “accidentally” forgotten.

Hello [Adjuster Name],

Thank you for visiting my property today to inspect the wind damage. As we discussed, the primary dwelling suffered roof damage.

I am writing to formally confirm that we also documented damage to the detached structures under Coverage B. Specifically, the east-facing 60 feet of the wooden privacy fence was blown down, and the aluminum roof of the detached tool shed was punctured by flying debris.

Please ensure these Coverage B items are fully included in your scope of loss and initial estimate. Let me know if you need any additional photographs of these specific structures.

Sincerely,

[Your Name]

Signs Your Other Structures Claim Is Off Track

Because Coverage B is a secondary part of the policy, it is highly prone to corner cutting. Adjusters who are overloaded with claims will often rush the valuation of a fence or a shed, relying on generic pricing software rather than local contractor realities. If you are dealing with a damaged outbuilding, you are likely feeling the stress of a settlement offer that simply does not reflect reality.

In my daily work with claims, I see the same patterns of underpayment happen repeatedly. Here are the clear signals that your Coverage B claim is not being handled correctly:

- 👉 The cause of loss was switched: A windstorm destroyed your fence, but the denial letter claims the fence collapsed due to “long term wood rot” or “wear and tear.”

- 👉 The inspection was skipped: The adjuster wrote an estimate for your detached garage without ever stepping foot inside it to check for structural framing damage.

- 👉 Excessive depreciation was applied: The insurer applied a 70 or 80 percent depreciation holdback on a shed that you can prove was recently renovated.

- 👉 The 10% limit is being used as a shield: The adjuster is capping your payout without verifying if your main Coverage A dwelling limit was accurately set in the first place.

When a storm destroys multiple outbuildings at once, hitting the 10 percent cap is common. I frequently see adjusters allocate the entire payout to the detached garage, completely leaving the ruined fence off the paperwork. Homeowners have the right to a full accounting of all damaged property, even if the financial cap has been reached, because it affects how depreciation is recovered later.

If your garage, pool structure, or fence settlement is far below the actual repair estimate, you do not have to simply accept the insurance company’s math. Incomplete inspections and incorrect depreciation calculations affect other structures exactly the same way they affect main dwellings.

When the gap between the insurance offer and the contractor’s bid is in the thousands, having a licensed public adjuster review the scope is often the smartest next step. A public adjuster’s specific job is to ensure every damaged structure was thoroughly inspected, verify that correct local labor rates were applied, and fight back when an insurer tries to use Coverage B caps to artificially shrink your payout.

Final Thoughts on Outbuilding Claims

Detached structures add immense value to your property, both practically and financially. While standard homeowners insurance does provide a safety net for these items through Coverage B, that net has a very firm ceiling. Knowing your exact limits before a storm hits allows you to make informed decisions about whether you need an endorsement to protect your custom garage or extensive fencing.

During the claims process, remember that the burden of proof often falls on you. Never assume an adjuster will carefully evaluate a ruined fence or crushed shed with the same urgency as a leaking roof. You must present the damage proactively, provide pre-loss photos if you have them, and scrutinize the depreciation schedule they hand you. Treat your detached structures with the same level of claim discipline as your own living room, and you will greatly improve your chances of securing the payout required to rebuild your property properly.

❓ FAQ

🏠 Does homeowners insurance cover a detached garage?

Yes, standard homeowners policies cover a detached garage under Coverage B (Other Structures). It is protected against the same perils as your home, such as fire or wind, usually up to 10% of your total dwelling coverage limit.

🚧 Does homeowners insurance cover fence damage?

Yes, fences are protected under Coverage B against sudden and accidental covered perils, like a severe windstorm blowing panels down or a neighbor’s tree falling onto the fence line.

🛠️ Does homeowners insurance cover a shed?

Yes, storage sheds and tool sheds are covered as other structures. Keep in mind that the structure of the shed is covered under Coverage B, while the lawnmowers and tools inside are covered separately under your personal property coverage.

🏊 Does homeowners insurance cover a swimming pool?

The physical structure of an in-ground pool is typically covered under Coverage B against sudden perils like a falling tree. However, damage from freezing, earth movement, or slow leaks is usually excluded as a maintenance issue.

🛣️ Does homeowners insurance cover a cracked driveway?

It depends on the cause. If the driveway was damaged by a sudden, covered event like a falling tree or a fire, it may be covered. If it cracked slowly over time due to earth shifting or normal wear and tear, it will be denied.

💼 Are business structures covered under Coverage B?

No. If you use your detached garage, shed, or outbuilding to run a business or store commercial inventory, standard homeowners insurance will exclude it. You need a specific commercial endorsement for business structures.

🧱 Does homeowners insurance cover retaining walls?

Coverage for retaining walls is very specific. They are generally covered for sudden impacts (like a vehicle hitting them), but most policies exclude damage caused by the gradual pressure of water or earth pushing against the wall.

🌳 Will insurance pay to remove a tree that fell on my fence?

If a tree falls and damages a covered structure like a fence or a shed, the policy will typically pay to repair the structure and provide a limited amount (often around $500) to remove the tree from the property.

💸 What is the 10 percent rule for other structures?

Most standard policies limit Coverage B payouts to 10% of your main dwelling coverage. If your house is insured for $400,000, your policy will only pay a maximum of $40,000 combined for all damaged outbuildings on the property.

📉 Why was my fence claim payout so low?

Fence claims are usually paid at Actual Cash Value (ACV). The adjuster calculates the cost to build a new fence, then subtracts value for every year the fence has been standing. This depreciation makes payouts on older fences very small.

Knowing what is covered is step one. These explain what happens from there.

- How a claim moves from filing to final payment

- What your policy actually covers and what it does not

- Which damage types get paid and which get excluded

- When filing a claim makes sense and when it works against you

- What to do after a denial and what your actual options are

- What a public adjuster does and when you actually need one

- When legal help is the move that changes the outcome

These cover what to do when the offer does not match what your policy says.

- 5 patterns that signal your settlement is probably short

- Who the adjuster at your door actually works for

- Where water damage estimates most often fall short

- What fire damage settlements commonly leave out

- Why your roofer's number and the insurer's estimate do not match

- When a denial needs legal leverage, not just negotiation

- Four paths to fight a denial, including one most homeowners miss

Disclosure: I'm sharing my personal industry experience, but I am not an attorney or a licensed insurance agent. The guides on this site are for informational purposes to help you understand the operational side of property claims: process, organization, and documentation. Every policy is unique, so please defer to your specific policy language. For legal interpretation, contested situations, or binding advice, always consult a licensed professional in your jurisdiction.